Cenveo, Inc. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

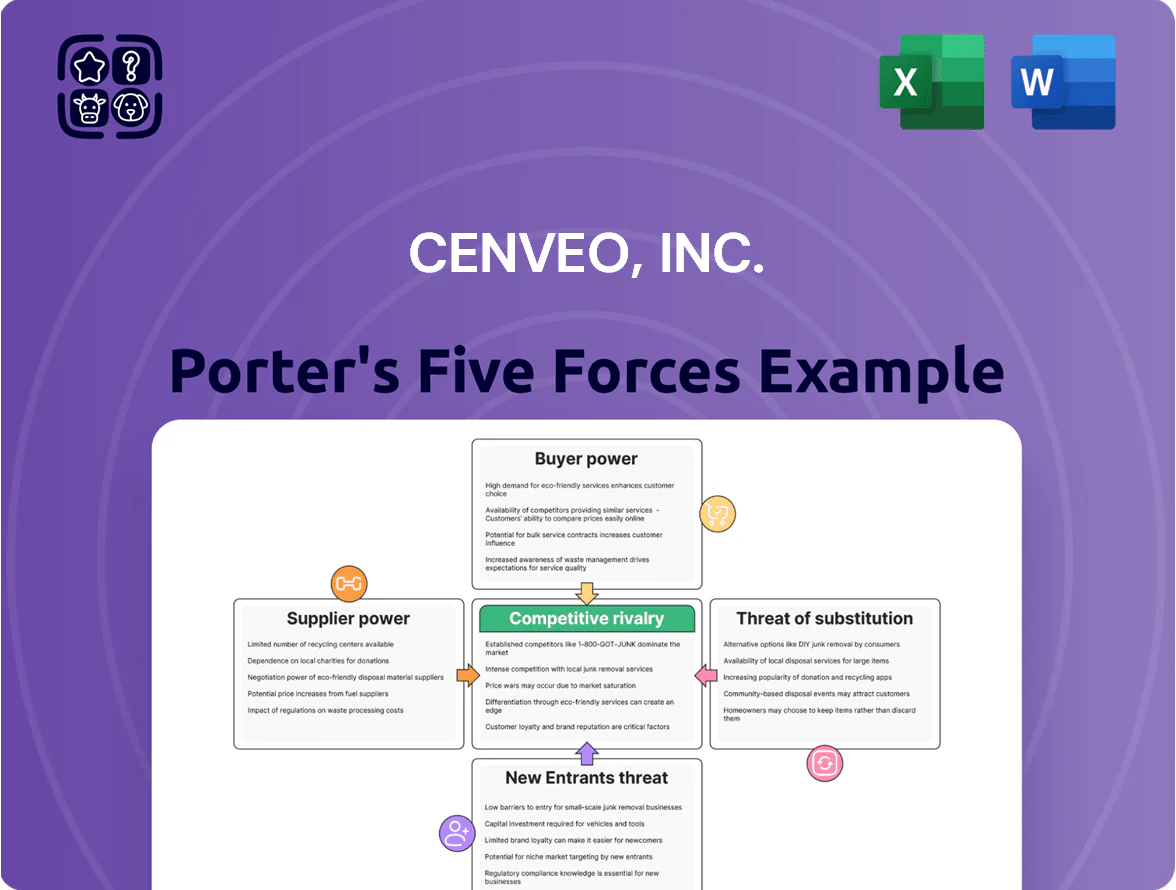

Cenveo faces intense rivalry from consolidated printers and digital disruptors, moderate supplier leverage for paper and inks, and steady buyer pressure from large commercial customers seeking lower costs.

Barriers to entry are moderate—capital-intensive but eroded by digital alternatives—while substitutes from digital media pose a growing threat to traditional print volumes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cenveo, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Paper and Pulp Mills

Industry consolidation has cut primary paper and pulp vendors, leaving Cenveo with fewer suppliers and less bargaining room; global top 10 mills controlled about 58% of kraft pulp capacity by Q4 2025.

By late 2025 major mills managed capacity to protect margins, pushing US coated paper spot prices up roughly 22% year-over-year, increasing Cenveo’s input costs.

Cenveo thereby faces tighter terms—higher prices, longer lead times—or risks supply disruptions for inks and paper grades critical to its printing operations.

Volatility in Chemical and Ink Pricing

Suppliers of specialized inks, coatings, and adhesives face input swings tied to petroleum and rare-earth prices; Brent crude rose ~45% from Jan 2023 to Dec 2024, pushing raw-material costs for print inks up an estimated 12–18% industry-wide.

Tighter U.S. and EU environmental rules through 2025 have driven suppliers to invest in low-VOC and bio-based formulas, with compliance/R&D costs raising supplier prices by roughly 3–6% per supplier in 2024.

Cenveo’s dependence on these specialty inputs concentrates supplier leverage, so a 10% input-price spike can cut gross margins by ~1.5–2.5 percentage points, per peer cost models.

Energy Costs and Utility Dependence

The label and packaging process is energy-intensive, so Cenveo, Inc. was highly dependent on regional utilities; energy made up roughly 6–9% of manufacturing COGS in 2024 for comparable converters. As grids transition to renewables in late 2025, wholesale electricity price volatility rose ~18% year-over-year, keeping industrial rates non-negotiable. Limited on-site alternatives and modest capex for electrification left utilities with strong supplier power over Cenveo’s cost base.

Specialized Printing Equipment Maintenance

Cenveo depends on a few high-tech press makers for advanced offset and digital equipment; OEMs hold proprietary software and parts, causing vendor lock-in and higher switching costs.

In 2025 Cenveo reported capital expenditures of $18.4M and service spend ~12% of COGS, giving suppliers leverage on service contracts, parts pricing, and upgrade timing.

- Limited OEMs → high switching cost

- Proprietary parts/software → lock-in

- Service spend ≈12% of COGS (2025)

- CapEx $18.4M (2025)

Labor Shortages in Specialized Logistics

Third-party carriers gained leverage as persistent US driver shortages tightened capacity; Bureau of Labor Statistics data show heavy‑truck driver vacancies rose ~12% from 2021–24, pushing freight rates up ~18% and making transportation a major swing in Cenveo’s COGS by 2025.

As Cenveo competes for limited shipping slots, carriers impose higher rates and stricter terms—spot rates peaked 25% above contract levels in 2024—raising logistics expense volatility and margin pressure.

- Driver vacancies +12% (2021–24)

- Freight rates +18% (avg) to 2025

- Spot > contract by 25% in 2024

- Transport now key swing in COGS

Suppliers' leverage dents Cenveo margins: input shocks, rising freight & coated-paper surge

Suppliers hold high leverage over Cenveo due to industry consolidation, capacity management, specialized ink/media needs, energy and OEM lock-in; input-price shocks (10%) cut gross margin ~1.5–2.5 pts. Key 2025 metrics: kraft pulp top‑10 share ~58%, coated paper spot +22% YoY, CapEx $18.4M, service ≈12% COGS, freight +18% (to 2025).

| Metric | 2025 |

|---|---|

| Kraft pulp top‑10 share | ~58% |

| Coated paper spot YoY | +22% |

| CapEx | $18.4M |

| Service % COGS | ≈12% |

| Freight change | +18% |

What is included in the product

Tailored exclusively for Cenveo, Inc., this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, barriers to entry, substitutes, and disruptive threats shaping its pricing power and profitability—ready for inclusion in investor materials or strategy decks.

Concise Porter's Five Forces snapshot for Cenveo—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to inform operational and strategic choices.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A large share of Cenveo, Inc.’s 2024 net sales—about 58% of $1.1bn—came from large corporate accounts and national retailers that demand high-volume discounts. These sophisticated buyers run competitive bids that force Cenveo to lower margins; Cenveo reported a 6.8% adjusted operating margin in 2024 after such contract pressure. Because a single national client can represent 5–10% of revenue, these customers can move contracts and dictate pricing and payment terms.

Low Switching Costs for Commodity Print

For standard commercial printing and basic envelopes, switching costs are low—buyers can change suppliers within days and price is the main decision driver; industry surveys show 63% of small print buyers ranked price as the top factor in 2024. This commoditization pressures Cenveo, whose 2024 commercial print revenue fell 7% year-over-year, to compete on price or service. To retain clients, Cenveo must innovate production efficiency or offer superior logistics and quality control. Otherwise churn risk rises as margins compress.

Demand for Sustainable Packaging Solutions

By end-2025, 78% of consumer-facing brands report binding ESG targets, shifting bargaining power as buyers demand certified low-carbon and plastic-free packaging, pressuring Cenveo to match specs or lose accounts.

Clients can switch quickly: 42% of brand RFPs in 2024 required carbon-neutral certification or equivalent, so competitors with compliant SKUs win share.

To retain customers, Cenveo must boost sustainable R&D spend—estimating an extra $15–25 million annually—to develop alternatives and reach industry certifications.

Price Transparency via Digital Procurement

The rise of e-procurement platforms like Jaggaer and Coupa lets buyers compare live prices across printers, cutting Cenveo’s ability to hide premium margins on complex jobs; industry surveys (2024) show 62% of corporate buyers use such tools, pushing average negotiated discounts to 8–12% on large print contracts.

Customers now use line-item analytics to negotiate down inks, finishing, and setup fees, squeezing Cenveo’s per-job gross margin and increasing pressure to justify value-added pricing.

- E-procurement adoption: 62% of buyers (2024)

- Typical negotiated discount: 8–12% on large contracts

- Key exposed items: inks, finishing, setup fees

Integration of In-House Printing Capabilities

Large publishers and retailers are piloting in-house digital print and labeling—about 18–25% of mid-run jobs (under 5,000 units) are cited in 2024 industry surveys as feasible to internalize, risking Cenveo’s high-margin short runs.

Even though Cenveo handles massive scale, losing these smaller jobs cuts gross margins: short-run work can carry 3–6 percentage points higher margin, so churn here raises renewal leverage for customers.

Customers’ backward integration plans give them negotiating power at contract renewal, especially if internal capex (small digital presses costing $150k–$400k) is amortized over 3–5 years.

- 18–25% of mid-run jobs feasible to internalize (2024 survey)

- Short-run margin premium: +3–6 percentage points

- Digital press capex: $150k–$400k, 3–5 year payback

Large-account pressure slashes margins—e-procurement, ESG & digital printing bite $15–25M/yr

Large corporate buyers (≈58% of $1.1bn 2024 sales) wield strong price leverage—single clients can be 5–10% of revenue—driving adjusted operating margin down to 6.8% in 2024; e-procurement adoption (62% in 2024) and typical negotiated discounts of 8–12% intensify pressure. ESG RFPs (42% carbon-neutral requirement, 2024) and in-house digital printing (18–25% mid-run internalizable) raise churn and force $15–25M/yr extra sustainable R&D or margin loss.

| Metric | Value (2024–25) |

|---|---|

| Share of sales from large accounts | 58% of $1.1bn |

| Adj. operating margin | 6.8% |

| E-procurement adoption | 62% |

| Negotiated discount | 8–12% |

| ESG RFPs | 42% |

| Internalizable mid-run jobs | 18–25% |

| Estimated extra R&D | $15–25M/yr |

Preview Before You Purchase

Cenveo, Inc. Porter's Five Forces Analysis

This preview shows the exact Cenveo, Inc. Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. You're viewing the final deliverable—ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cenveo faces intense rivalry from consolidated printers and digital disruptors, moderate supplier leverage for paper and inks, and steady buyer pressure from large commercial customers seeking lower costs.

Barriers to entry are moderate—capital-intensive but eroded by digital alternatives—while substitutes from digital media pose a growing threat to traditional print volumes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cenveo, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Paper and Pulp Mills

Industry consolidation has cut primary paper and pulp vendors, leaving Cenveo with fewer suppliers and less bargaining room; global top 10 mills controlled about 58% of kraft pulp capacity by Q4 2025.

By late 2025 major mills managed capacity to protect margins, pushing US coated paper spot prices up roughly 22% year-over-year, increasing Cenveo’s input costs.

Cenveo thereby faces tighter terms—higher prices, longer lead times—or risks supply disruptions for inks and paper grades critical to its printing operations.

Volatility in Chemical and Ink Pricing

Suppliers of specialized inks, coatings, and adhesives face input swings tied to petroleum and rare-earth prices; Brent crude rose ~45% from Jan 2023 to Dec 2024, pushing raw-material costs for print inks up an estimated 12–18% industry-wide.

Tighter U.S. and EU environmental rules through 2025 have driven suppliers to invest in low-VOC and bio-based formulas, with compliance/R&D costs raising supplier prices by roughly 3–6% per supplier in 2024.

Cenveo’s dependence on these specialty inputs concentrates supplier leverage, so a 10% input-price spike can cut gross margins by ~1.5–2.5 percentage points, per peer cost models.

Energy Costs and Utility Dependence

The label and packaging process is energy-intensive, so Cenveo, Inc. was highly dependent on regional utilities; energy made up roughly 6–9% of manufacturing COGS in 2024 for comparable converters. As grids transition to renewables in late 2025, wholesale electricity price volatility rose ~18% year-over-year, keeping industrial rates non-negotiable. Limited on-site alternatives and modest capex for electrification left utilities with strong supplier power over Cenveo’s cost base.

Specialized Printing Equipment Maintenance

Cenveo depends on a few high-tech press makers for advanced offset and digital equipment; OEMs hold proprietary software and parts, causing vendor lock-in and higher switching costs.

In 2025 Cenveo reported capital expenditures of $18.4M and service spend ~12% of COGS, giving suppliers leverage on service contracts, parts pricing, and upgrade timing.

- Limited OEMs → high switching cost

- Proprietary parts/software → lock-in

- Service spend ≈12% of COGS (2025)

- CapEx $18.4M (2025)

Labor Shortages in Specialized Logistics

Third-party carriers gained leverage as persistent US driver shortages tightened capacity; Bureau of Labor Statistics data show heavy‑truck driver vacancies rose ~12% from 2021–24, pushing freight rates up ~18% and making transportation a major swing in Cenveo’s COGS by 2025.

As Cenveo competes for limited shipping slots, carriers impose higher rates and stricter terms—spot rates peaked 25% above contract levels in 2024—raising logistics expense volatility and margin pressure.

- Driver vacancies +12% (2021–24)

- Freight rates +18% (avg) to 2025

- Spot > contract by 25% in 2024

- Transport now key swing in COGS

Suppliers' leverage dents Cenveo margins: input shocks, rising freight & coated-paper surge

Suppliers hold high leverage over Cenveo due to industry consolidation, capacity management, specialized ink/media needs, energy and OEM lock-in; input-price shocks (10%) cut gross margin ~1.5–2.5 pts. Key 2025 metrics: kraft pulp top‑10 share ~58%, coated paper spot +22% YoY, CapEx $18.4M, service ≈12% COGS, freight +18% (to 2025).

| Metric | 2025 |

|---|---|

| Kraft pulp top‑10 share | ~58% |

| Coated paper spot YoY | +22% |

| CapEx | $18.4M |

| Service % COGS | ≈12% |

| Freight change | +18% |

What is included in the product

Tailored exclusively for Cenveo, Inc., this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, barriers to entry, substitutes, and disruptive threats shaping its pricing power and profitability—ready for inclusion in investor materials or strategy decks.

Concise Porter's Five Forces snapshot for Cenveo—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to inform operational and strategic choices.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A large share of Cenveo, Inc.’s 2024 net sales—about 58% of $1.1bn—came from large corporate accounts and national retailers that demand high-volume discounts. These sophisticated buyers run competitive bids that force Cenveo to lower margins; Cenveo reported a 6.8% adjusted operating margin in 2024 after such contract pressure. Because a single national client can represent 5–10% of revenue, these customers can move contracts and dictate pricing and payment terms.

Low Switching Costs for Commodity Print

For standard commercial printing and basic envelopes, switching costs are low—buyers can change suppliers within days and price is the main decision driver; industry surveys show 63% of small print buyers ranked price as the top factor in 2024. This commoditization pressures Cenveo, whose 2024 commercial print revenue fell 7% year-over-year, to compete on price or service. To retain clients, Cenveo must innovate production efficiency or offer superior logistics and quality control. Otherwise churn risk rises as margins compress.

Demand for Sustainable Packaging Solutions

By end-2025, 78% of consumer-facing brands report binding ESG targets, shifting bargaining power as buyers demand certified low-carbon and plastic-free packaging, pressuring Cenveo to match specs or lose accounts.

Clients can switch quickly: 42% of brand RFPs in 2024 required carbon-neutral certification or equivalent, so competitors with compliant SKUs win share.

To retain customers, Cenveo must boost sustainable R&D spend—estimating an extra $15–25 million annually—to develop alternatives and reach industry certifications.

Price Transparency via Digital Procurement

The rise of e-procurement platforms like Jaggaer and Coupa lets buyers compare live prices across printers, cutting Cenveo’s ability to hide premium margins on complex jobs; industry surveys (2024) show 62% of corporate buyers use such tools, pushing average negotiated discounts to 8–12% on large print contracts.

Customers now use line-item analytics to negotiate down inks, finishing, and setup fees, squeezing Cenveo’s per-job gross margin and increasing pressure to justify value-added pricing.

- E-procurement adoption: 62% of buyers (2024)

- Typical negotiated discount: 8–12% on large contracts

- Key exposed items: inks, finishing, setup fees

Integration of In-House Printing Capabilities

Large publishers and retailers are piloting in-house digital print and labeling—about 18–25% of mid-run jobs (under 5,000 units) are cited in 2024 industry surveys as feasible to internalize, risking Cenveo’s high-margin short runs.

Even though Cenveo handles massive scale, losing these smaller jobs cuts gross margins: short-run work can carry 3–6 percentage points higher margin, so churn here raises renewal leverage for customers.

Customers’ backward integration plans give them negotiating power at contract renewal, especially if internal capex (small digital presses costing $150k–$400k) is amortized over 3–5 years.

- 18–25% of mid-run jobs feasible to internalize (2024 survey)

- Short-run margin premium: +3–6 percentage points

- Digital press capex: $150k–$400k, 3–5 year payback

Large-account pressure slashes margins—e-procurement, ESG & digital printing bite $15–25M/yr

Large corporate buyers (≈58% of $1.1bn 2024 sales) wield strong price leverage—single clients can be 5–10% of revenue—driving adjusted operating margin down to 6.8% in 2024; e-procurement adoption (62% in 2024) and typical negotiated discounts of 8–12% intensify pressure. ESG RFPs (42% carbon-neutral requirement, 2024) and in-house digital printing (18–25% mid-run internalizable) raise churn and force $15–25M/yr extra sustainable R&D or margin loss.

| Metric | Value (2024–25) |

|---|---|

| Share of sales from large accounts | 58% of $1.1bn |

| Adj. operating margin | 6.8% |

| E-procurement adoption | 62% |

| Negotiated discount | 8–12% |

| ESG RFPs | 42% |

| Internalizable mid-run jobs | 18–25% |

| Estimated extra R&D | $15–25M/yr |

Preview Before You Purchase

Cenveo, Inc. Porter's Five Forces Analysis

This preview shows the exact Cenveo, Inc. Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. You're viewing the final deliverable—ready for immediate use.