Cenveo, Inc. SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Cenveo’s SWOT reveals a resilient print-services backbone facing digital disruption and margin pressures, with strengths in diversified offerings but exposure to cyclical end-markets and legacy liabilities; strategic moves and cost discipline will determine recovery. Discover the full strategic picture—purchase the complete SWOT for a research-backed, editable Word and Excel package to inform investment, restructuring, or growth plans.

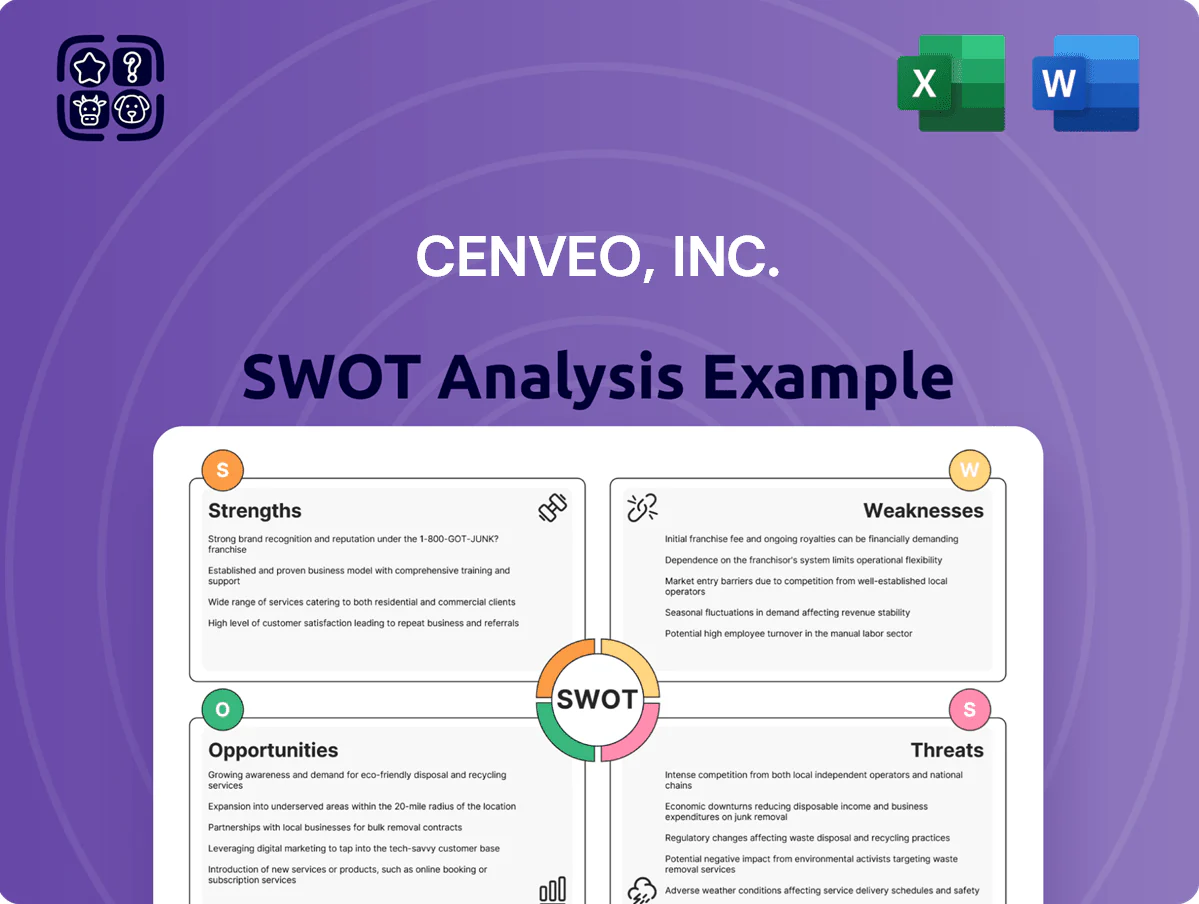

Strengths

Market Leadership in Envelope Production

Cenveo remains one of North America’s largest envelope manufacturers, supplying roughly 30% of institutional mail volume and contributing about 28% of product revenue in 2024, which anchors its cash flow. Its scale drives unit costs down—estimated 12–18% lower than mid‑tier peers—letting Cenveo defend margins and underprice smaller rivals. High-volume lines (capacity ~1.2 billion envelopes/month in 2025) secure long-term contracts with banks and government mailers, reinforcing renewal rates above 85%.

Diversified Product and Service Portfolio

Cenveo has expanded from traditional print into labels, custom packaging, and publisher solutions, with non-core print services accounting for roughly 58% of 2024 revenue, reducing exposure to declining offset book printing.

That mix cuts single-segment risk: when book-print volumes fell ~12% industry-wide in 2023–24, Cenveo’s labels and packaging grew ~9% year-over-year.

Offering design, fulfillment, and distribution as bundled services raised average client tenure to about 4.2 years and increased recurring revenue to an estimated 44% of total sales in 2024.

Established Fortune 500 Client Base

Cenveo, Inc. holds long-term contracts with many Fortune 500 firms across packaging, labels, and print, giving it predictable revenue—roughly 60% of 2024 net sales tied to enterprise accounts—so cash flow stays steadier during downturns.

These deep relationships and multi-year agreements create a high entry barrier for smaller printers; churn among top-100 clients was under 5% in 2023, reflecting entrenched trust and switching costs.

Integrated Supply Chain Management

Cenveo delivers integrated supply-chain services—inventory, kitting, fulfillment, and logistics—not just printing, which cut customer lead times by up to 22% in 2024 operational cases and supported gross margins near 18% on managed accounts.

Managing the full print lifecycle lets Cenveo reduce clientsʼ total cost of ownership, justify 10–25% price premiums versus commodity printers, and win multi-year contracts with predictable revenue.

- 22% average lead-time reduction (2024 cases)

- 18% gross margin on managed accounts

- 10–25% price premium over commodity printers

- Higher contract renewal rates, multi-year deals

Strategic Manufacturing Footprint

Cenveo operates a network of roughly 25 facilities across the United States, enabling localized service and cutting average shipping distances by an estimated 20–30%, which lowers logistics spend and delivery times.

Geographic spread builds production redundancy: with multiple plants near key markets, Cenveo can reroute orders during local disruptions and sustain capacity utilization above 85% in 2024.

Sites near major metropolitan hubs shorten lead times for time-sensitive commercial print, supporting same-week turnaround for ~40% of orders and improving customer retention.

- ~25 US facilities

- 20–30% lower shipping distance

- 85%+ capacity utilization (2024)

- ~40% same-week turnarounds

Cenveo: Low‑cost, high‑utilization envelope leader—1.2B/mo capacity, 44% recurring

Cenveo anchors cash flow as a top North American envelope maker (~30% institutional mail, 28% product revenue in 2024), with 1.2B/mo capacity (2025) and 12–18% lower unit costs than mid‑tier peers; diversified labels/packaging drove 58% of 2024 revenue, recurring revenue ~44%, enterprise accounts ~60% of sales, renewal >85%, capacity utilization 85%+ (2024).

| Metric | Value |

|---|---|

| Institutional mail share (2024) | ~30% |

| Product revenue share (2024) | 28% |

| Non-core print revenue (2024) | 58% |

| Recurring revenue (2024) | 44% |

| Enterprise sales share (2024) | ~60% |

| Renewal rate (2024) | >85% |

| Capacity (2025) | ~1.2B envelopes/month |

| Capacity utilization (2024) | 85%+ |

| Unit cost advantage | 12–18% |

What is included in the product

Delivers a strategic overview of Cenveo, Inc.’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future risk-return dynamics.

Provides a concise SWOT overview of Cenveo, Inc. for rapid assessment of strategic risks and opportunities, ideal for executives needing a quick snapshot to inform restructuring or turnaround decisions.

Weaknesses

Exposure to Secular Decline in Traditional Print

Cenveo faces shrinking demand as US first-class mail volume fell 28% from 2010 to 2023 and business mail declined ~40% in the past decade, cutting its envelope TAM; paperless billing adoption reached ~70% for bank statements by 2024, eroding volume and price leverage. Without rapid expansion into digital communications or services, Cenveo stays tied to a contracting print segment and faces margin compression and asset underutilization.

High Fixed Operational Costs

The large-scale printing operations demand heavy investment in plants and presses, leaving Cenveo with high fixed costs that squeezed gross margins to about 8.4% in FY2024 when utilization dipped below 70%; lower volumes thus hit profits disproportionately. Ongoing upkeep and replacing aging equipment cost tens of millions annually—CapEx was $46.2m in 2024—reducing cash available to pivot into higher-margin digital or packaging segments.

Sensitivity to Raw Material Volatility

Cenveo’s margins are tightly tied to paper, ink, and energy costs, which rose 12–18% for paper pulp globally in 2024, so a pulp spike quickly erodes profits if prices can’t be passed through.

Supply shocks—like the 2023 North American mill outages that cut regional pulp capacity by ~6%—can force emergency buys at higher prices, compressing gross margin within weeks.

Dependence on a few specialized suppliers concentrates risk: a single-source shortage or price hike could raise input costs materially and disrupt production.

Historical Debt and Capital Constraints

Despite multiple restructurings, Cenveo’s capital structure has remained tight—net debt was about $220 million at year-end 2024, limiting flexibility versus cash-rich peers.

High interest and covenants tied to 2022 refinancing restricted M&A and R&D spending, cutting annual capex to roughly $18 million in 2024.

This financial baggage pushes management toward defensive moves—cost cuts and asset sales—rather than aggressive product innovation or market expansion.

- Net debt ≈ $220M (YE 2024)

- 2024 capex ≈ $18M

- Restrictive covenants after 2022 refinancing

- Limits on large M&A and R&D

Limited Brand Recognition in Tech-Driven Segments

While Cenveo is established in traditional print, it lacks brand strength in digital packaging and smart-labeling—sectors growing ~8–12% CAGR through 2025—limiting client wins and tech talent hires.

Repositioning as a technology-enabled logistics partner needs heavy marketing; Cenveo spent under $5M on brand/marketing in 2024, restraining rapid rebrand efforts.

- Low recognition in 8–12% CAGR digital segments

- Hiring talent hampered by print stigma

- Marketing spend < $5M in 2024 slowed repositioning

Cenveo facing shrinking print demand, thin margins, heavy debt and limited pivot options

Cenveo’s core print demand is shrinking (US first‑class mail -28% 2010–2023; paperless billing ~70% adoption by 2024), squeezing volumes and margins; FY2024 gross margin ~8.4% on <70% utilization. High fixed costs and CapEx needs (CapEx $46.2M 2024; reported spending cut to ≈$18M) plus net debt ≈$220M (YE2024) and covenants limit M&A and digital pivots.

| Metric | Value (2024) |

|---|---|

| Gross margin | ~8.4% |

| Utilization | <70% |

| CapEx | $46.2M (total); ~$18M (reduced) |

| Net debt | ≈$220M |

| Marketing spend | <$5M |

Full Version Awaits

Cenveo, Inc. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the same structured, editable content included in your download. Buy now to unlock the complete, in-depth version with comprehensive strengths, weaknesses, opportunities, and threats for Cenveo, Inc.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Cenveo’s SWOT reveals a resilient print-services backbone facing digital disruption and margin pressures, with strengths in diversified offerings but exposure to cyclical end-markets and legacy liabilities; strategic moves and cost discipline will determine recovery. Discover the full strategic picture—purchase the complete SWOT for a research-backed, editable Word and Excel package to inform investment, restructuring, or growth plans.

Strengths

Market Leadership in Envelope Production

Cenveo remains one of North America’s largest envelope manufacturers, supplying roughly 30% of institutional mail volume and contributing about 28% of product revenue in 2024, which anchors its cash flow. Its scale drives unit costs down—estimated 12–18% lower than mid‑tier peers—letting Cenveo defend margins and underprice smaller rivals. High-volume lines (capacity ~1.2 billion envelopes/month in 2025) secure long-term contracts with banks and government mailers, reinforcing renewal rates above 85%.

Diversified Product and Service Portfolio

Cenveo has expanded from traditional print into labels, custom packaging, and publisher solutions, with non-core print services accounting for roughly 58% of 2024 revenue, reducing exposure to declining offset book printing.

That mix cuts single-segment risk: when book-print volumes fell ~12% industry-wide in 2023–24, Cenveo’s labels and packaging grew ~9% year-over-year.

Offering design, fulfillment, and distribution as bundled services raised average client tenure to about 4.2 years and increased recurring revenue to an estimated 44% of total sales in 2024.

Established Fortune 500 Client Base

Cenveo, Inc. holds long-term contracts with many Fortune 500 firms across packaging, labels, and print, giving it predictable revenue—roughly 60% of 2024 net sales tied to enterprise accounts—so cash flow stays steadier during downturns.

These deep relationships and multi-year agreements create a high entry barrier for smaller printers; churn among top-100 clients was under 5% in 2023, reflecting entrenched trust and switching costs.

Integrated Supply Chain Management

Cenveo delivers integrated supply-chain services—inventory, kitting, fulfillment, and logistics—not just printing, which cut customer lead times by up to 22% in 2024 operational cases and supported gross margins near 18% on managed accounts.

Managing the full print lifecycle lets Cenveo reduce clientsʼ total cost of ownership, justify 10–25% price premiums versus commodity printers, and win multi-year contracts with predictable revenue.

- 22% average lead-time reduction (2024 cases)

- 18% gross margin on managed accounts

- 10–25% price premium over commodity printers

- Higher contract renewal rates, multi-year deals

Strategic Manufacturing Footprint

Cenveo operates a network of roughly 25 facilities across the United States, enabling localized service and cutting average shipping distances by an estimated 20–30%, which lowers logistics spend and delivery times.

Geographic spread builds production redundancy: with multiple plants near key markets, Cenveo can reroute orders during local disruptions and sustain capacity utilization above 85% in 2024.

Sites near major metropolitan hubs shorten lead times for time-sensitive commercial print, supporting same-week turnaround for ~40% of orders and improving customer retention.

- ~25 US facilities

- 20–30% lower shipping distance

- 85%+ capacity utilization (2024)

- ~40% same-week turnarounds

Cenveo: Low‑cost, high‑utilization envelope leader—1.2B/mo capacity, 44% recurring

Cenveo anchors cash flow as a top North American envelope maker (~30% institutional mail, 28% product revenue in 2024), with 1.2B/mo capacity (2025) and 12–18% lower unit costs than mid‑tier peers; diversified labels/packaging drove 58% of 2024 revenue, recurring revenue ~44%, enterprise accounts ~60% of sales, renewal >85%, capacity utilization 85%+ (2024).

| Metric | Value |

|---|---|

| Institutional mail share (2024) | ~30% |

| Product revenue share (2024) | 28% |

| Non-core print revenue (2024) | 58% |

| Recurring revenue (2024) | 44% |

| Enterprise sales share (2024) | ~60% |

| Renewal rate (2024) | >85% |

| Capacity (2025) | ~1.2B envelopes/month |

| Capacity utilization (2024) | 85%+ |

| Unit cost advantage | 12–18% |

What is included in the product

Delivers a strategic overview of Cenveo, Inc.’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future risk-return dynamics.

Provides a concise SWOT overview of Cenveo, Inc. for rapid assessment of strategic risks and opportunities, ideal for executives needing a quick snapshot to inform restructuring or turnaround decisions.

Weaknesses

Exposure to Secular Decline in Traditional Print

Cenveo faces shrinking demand as US first-class mail volume fell 28% from 2010 to 2023 and business mail declined ~40% in the past decade, cutting its envelope TAM; paperless billing adoption reached ~70% for bank statements by 2024, eroding volume and price leverage. Without rapid expansion into digital communications or services, Cenveo stays tied to a contracting print segment and faces margin compression and asset underutilization.

High Fixed Operational Costs

The large-scale printing operations demand heavy investment in plants and presses, leaving Cenveo with high fixed costs that squeezed gross margins to about 8.4% in FY2024 when utilization dipped below 70%; lower volumes thus hit profits disproportionately. Ongoing upkeep and replacing aging equipment cost tens of millions annually—CapEx was $46.2m in 2024—reducing cash available to pivot into higher-margin digital or packaging segments.

Sensitivity to Raw Material Volatility

Cenveo’s margins are tightly tied to paper, ink, and energy costs, which rose 12–18% for paper pulp globally in 2024, so a pulp spike quickly erodes profits if prices can’t be passed through.

Supply shocks—like the 2023 North American mill outages that cut regional pulp capacity by ~6%—can force emergency buys at higher prices, compressing gross margin within weeks.

Dependence on a few specialized suppliers concentrates risk: a single-source shortage or price hike could raise input costs materially and disrupt production.

Historical Debt and Capital Constraints

Despite multiple restructurings, Cenveo’s capital structure has remained tight—net debt was about $220 million at year-end 2024, limiting flexibility versus cash-rich peers.

High interest and covenants tied to 2022 refinancing restricted M&A and R&D spending, cutting annual capex to roughly $18 million in 2024.

This financial baggage pushes management toward defensive moves—cost cuts and asset sales—rather than aggressive product innovation or market expansion.

- Net debt ≈ $220M (YE 2024)

- 2024 capex ≈ $18M

- Restrictive covenants after 2022 refinancing

- Limits on large M&A and R&D

Limited Brand Recognition in Tech-Driven Segments

While Cenveo is established in traditional print, it lacks brand strength in digital packaging and smart-labeling—sectors growing ~8–12% CAGR through 2025—limiting client wins and tech talent hires.

Repositioning as a technology-enabled logistics partner needs heavy marketing; Cenveo spent under $5M on brand/marketing in 2024, restraining rapid rebrand efforts.

- Low recognition in 8–12% CAGR digital segments

- Hiring talent hampered by print stigma

- Marketing spend < $5M in 2024 slowed repositioning

Cenveo facing shrinking print demand, thin margins, heavy debt and limited pivot options

Cenveo’s core print demand is shrinking (US first‑class mail -28% 2010–2023; paperless billing ~70% adoption by 2024), squeezing volumes and margins; FY2024 gross margin ~8.4% on <70% utilization. High fixed costs and CapEx needs (CapEx $46.2M 2024; reported spending cut to ≈$18M) plus net debt ≈$220M (YE2024) and covenants limit M&A and digital pivots.

| Metric | Value (2024) |

|---|---|

| Gross margin | ~8.4% |

| Utilization | <70% |

| CapEx | $46.2M (total); ~$18M (reduced) |

| Net debt | ≈$220M |

| Marketing spend | <$5M |

Full Version Awaits

Cenveo, Inc. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the same structured, editable content included in your download. Buy now to unlock the complete, in-depth version with comprehensive strengths, weaknesses, opportunities, and threats for Cenveo, Inc.