Central Glass Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

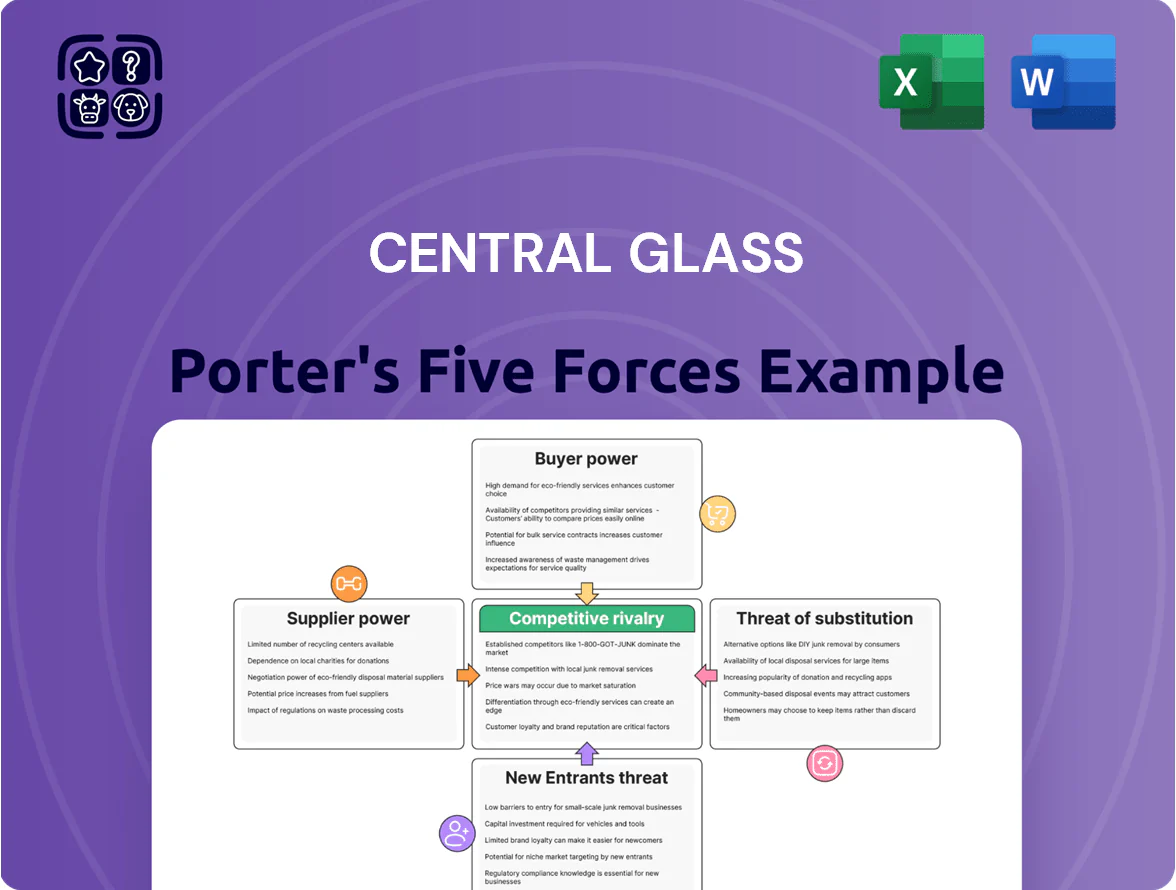

Central Glass faces moderate supplier power, steady buyer demand, and evolving substitute risks from specialty materials; industry rivalry hinges on scale and technological differentiation, while barriers to entry are tempered by capital intensity and certifications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Central Glass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Dependency for Glass Production

Central Glass relies on high-grade silica sand, soda ash, and limestone; soda ash is self-produced, but 60–80% of high-purity sand and specialty minerals come from a handful of global miners, creating supplier leverage over price and lead times.

Concentration of these resources means suppliers can push price swings of 10–25% year-on-year; Central Glass faces added risk when single-source shipments delay furnace runs.

By 2025 geopolitical tensions have cut availability of certain chemical reagents for fine chemicals by an estimated 15–20%, squeezing margins in specialty lines and forcing higher working capital for inventory buffers.

Energy Intensity and Utility Provider Leverage

Glass and chemical manufacturing need constant high heat, so Central Glass is highly exposed to energy price spikes; natural gas rose ~45% in Japan from 2020–2023 and power costs jumped ~30% in 2022–2024, cutting margins.

Utility providers hold leverage because switching fuels requires huge CAPEX; Central Glass depends on long-term gas and electricity contracts to hedge volatility seen in mid-2020s markets.

Rising carbon pricing and green-transition costs—Japan’s carbon price signals and EUA-linkage rising to €50–€80/ton in 2024—add supplier-side cost pressure on feedstock and energy procurement.

Specialized Chemical Feedstock Availability

In Central Glass’s fine-chemicals arm, a handful of suppliers dominate high-purity precursors and catalysts, creating technical lock-ins; suppliers of >99.9% purity inputs held an estimated 60–70% market share in Japan in 2024, strengthening their leverage.

Switching suppliers forces costly re‑validation: typical re‑certification for pharmaceuticals-grade products can take 6–12 months and $0.5–2.0M per product, raising switching costs and supplier bargaining power.

Logistics and Transportation Provider Influence

The heavy, fragile nature of glass raises transport costs and forces Central Glass to use specialized carriers; global freight rates rose ~35% from 2020–2022 and fuel surcharges added ~8–12% to bills through 2025, giving logistics firms pricing power.

Central Glass depends on just-in-time deliveries for automotive and architectural clients, so carrier disruptions or labor-driven price hikes directly hit margins and throughput.

- Specialized handling needed raises per-ton shipping cost

- Freight rates +35% (2020–22); fuel surcharges ~8–12% by 2025

- Just-in-time reliance increases vulnerability to delays

- Supplier price shocks feed directly into operating margin

Regulatory and Environmental Compliance Suppliers

As global rules tighten, carbon-capture and emission-control suppliers have grown leverage: patented filtration and recycling tech limits alternatives and forces Central Glass to partner to meet 2025–2030 targets under agreements like the 2023 Global Methane Pledge extensions.

These green inputs carry high costs—industry estimates show CAPEX premiums of 15–30% and supplier margins above 25%—raising procurement risk and supplier bargaining power for Central Glass.

- Patented tech limits substitutes

- CAPEX premium 15–30%

- Supplier margins >25%

- Partnerships required for 2025–2030 targets

Supplier chokehold: high-purity sand, soaring energy & freight squeeze Central Glass

Central Glass faces high supplier power: 60–80% of high-purity sand from few miners, >60% market share for >99.9% purity reagents (2024), gas prices up ~45% (2020–23) and power +30% (2022–24), freight +35% (2020–22) with fuel surcharges 8–12% by 2025; switching costs: revalidation 6–12 months, $0.5–2.0M.

| Metric | Value |

|---|---|

| High-purity sand dependence | 60–80% |

| Purity supplier share (2024) | 60–70% |

| Natural gas change | +45% (2020–23) |

| Power cost change | +30% (2022–24) |

| Freight change | +35% (2020–22) |

| Fuel surcharges | 8–12% (by 2025) |

| Revalidation cost/time | $0.5–2.0M, 6–12 mo |

| CAPEX premium for green tech | 15–30% |

What is included in the product

Tailored Porter’s Five Forces analysis of Central Glass that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive forces—with strategic commentary to inform pricing, positioning, and risk mitigation.

A concise Porter's Five Forces snapshot for Central Glass—quickly spot competitive pressures and strategic levers to relieve pain points in pricing, supplier dependency, and market entry.

Customers Bargaining Power

Automotive OEM Volume Leverage

Large OEMs account for roughly 40–55% of global automotive glass value chains, giving them strong leverage to demand annual price cuts of 1–3% and strict just-in-time delivery, which compresses supplier margins.

By 2025, consolidation left top 10 global car groups controlling ~60% of volume, enabling them to set specs for smart glass and HUDs, forcing suppliers into costly R&D and certification.

Central Glass must match Tier-1 quality, hit sub-ppm defect rates, and offer competitive pricing near industry averages (gross margins 12–18%) or risk displacement by global glass giants.

Construction Industry Cyclicality and Price Sensitivity

Architectural glass buyers—large developers and construction firms—are highly price-sensitive; global construction starts fell 6% in 2024 and high U.S. rates into 2026 have delayed projects, giving buyers more leverage to push prices down.

Standard flat glass is treated as a commodity, triggering price wars that compressed margins by ~180 basis points for glass makers in 2024; Central Glass faces the same pressure.

To defend pricing, Central Glass must sell energy-efficient coatings and value-added units—low-E coatings can justify 8–12% price premiums—so differentiation is essential.

Specialized Requirements of Pharmaceutical Clients

The fine‑chemicals arm serves pharma and electronics, where buyers wield strong leverage: 78% of pharma suppliers report routine audits and customers demand multi‑year contracts for supply security, forcing transparency on unit manufacturing costs. High integration raises switching costs—estimated retention >85% after qualification—so buyers extract favorable pricing and clauses up front. By late 2025, ~62% of top pharma buyers require certified sustainable/ethical inputs, increasing procurement demands.

Retail and Fertilizer Distribution Networks

In chemicals (fertilizers, soda), bargaining power rests with large agri-distributors and industrial wholesalers who control market access and can switch suppliers on price and credit; commodity NPK margins fell 12% in 2024, so Central Glass faces market-clearing prices set by these buyers.

To hold share, Central Glass must invest in brand loyalty and logistics—its 2024 distribution capex rose 18% to ¥3.6bn to improve delivery reliability.

- Buyers: large distributors, wholesalers

- Switching: easy on price/credit

- Price power: market-clearing; NPK margins −12% (2024)

- Response: brand + logistics; 2024 distribution capex ¥3.6bn (+18%)

Demand for High-Tech Specialty Glass

Customers in electronics and renewable energy demand specialty glass for touchscreens and solar panels, pushing Central Glass to invest in R&D (company R&D ~3.2% of sales in FY2024) to meet specs.

These buyers can co-develop or switch suppliers, so Central Glass faces high bargaining power and must keep prices tight while offering integration.

Fast tech obsolescence—smartphone and PV module cycles under 3 years—forces ongoing innovation and capex pressure (capex ~¥18bn in 2024).

- R&D 3.2% sales (FY2024)

- Capex ¥18bn (2024)

- Product cycles <3 years

- High switch/co‑develop risk

OEMs squeeze margins—top 10 car groups ~60%, price cuts 1–3% p.a., capex ¥18bn

Buyers (OEMs, developers, distributors, pharma, electronics) hold high bargaining power—top 10 car groups ~60% volume (2025), OEMs push 1–3% annual price cuts, commodity margins fell ~180 bps (2024); Central Glass R&D 3.2% sales (FY2024), capex ¥18bn (2024), distribution capex ¥3.6bn (+18%).

| Metric | Value |

|---|---|

| Top car group share (2025) | ~60% |

| OEM price cuts | 1–3% p.a. |

| Margins impact (2024) | −180 bps |

| R&D | 3.2% sales (FY2024) |

| Capex | ¥18bn (2024) |

| Dist. capex | ¥3.6bn (+18%) |

Preview the Actual Deliverable

Central Glass Porter's Five Forces Analysis

This preview shows the exact Central Glass Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise, actionable insights. You’re viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Central Glass faces moderate supplier power, steady buyer demand, and evolving substitute risks from specialty materials; industry rivalry hinges on scale and technological differentiation, while barriers to entry are tempered by capital intensity and certifications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Central Glass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Dependency for Glass Production

Central Glass relies on high-grade silica sand, soda ash, and limestone; soda ash is self-produced, but 60–80% of high-purity sand and specialty minerals come from a handful of global miners, creating supplier leverage over price and lead times.

Concentration of these resources means suppliers can push price swings of 10–25% year-on-year; Central Glass faces added risk when single-source shipments delay furnace runs.

By 2025 geopolitical tensions have cut availability of certain chemical reagents for fine chemicals by an estimated 15–20%, squeezing margins in specialty lines and forcing higher working capital for inventory buffers.

Energy Intensity and Utility Provider Leverage

Glass and chemical manufacturing need constant high heat, so Central Glass is highly exposed to energy price spikes; natural gas rose ~45% in Japan from 2020–2023 and power costs jumped ~30% in 2022–2024, cutting margins.

Utility providers hold leverage because switching fuels requires huge CAPEX; Central Glass depends on long-term gas and electricity contracts to hedge volatility seen in mid-2020s markets.

Rising carbon pricing and green-transition costs—Japan’s carbon price signals and EUA-linkage rising to €50–€80/ton in 2024—add supplier-side cost pressure on feedstock and energy procurement.

Specialized Chemical Feedstock Availability

In Central Glass’s fine-chemicals arm, a handful of suppliers dominate high-purity precursors and catalysts, creating technical lock-ins; suppliers of >99.9% purity inputs held an estimated 60–70% market share in Japan in 2024, strengthening their leverage.

Switching suppliers forces costly re‑validation: typical re‑certification for pharmaceuticals-grade products can take 6–12 months and $0.5–2.0M per product, raising switching costs and supplier bargaining power.

Logistics and Transportation Provider Influence

The heavy, fragile nature of glass raises transport costs and forces Central Glass to use specialized carriers; global freight rates rose ~35% from 2020–2022 and fuel surcharges added ~8–12% to bills through 2025, giving logistics firms pricing power.

Central Glass depends on just-in-time deliveries for automotive and architectural clients, so carrier disruptions or labor-driven price hikes directly hit margins and throughput.

- Specialized handling needed raises per-ton shipping cost

- Freight rates +35% (2020–22); fuel surcharges ~8–12% by 2025

- Just-in-time reliance increases vulnerability to delays

- Supplier price shocks feed directly into operating margin

Regulatory and Environmental Compliance Suppliers

As global rules tighten, carbon-capture and emission-control suppliers have grown leverage: patented filtration and recycling tech limits alternatives and forces Central Glass to partner to meet 2025–2030 targets under agreements like the 2023 Global Methane Pledge extensions.

These green inputs carry high costs—industry estimates show CAPEX premiums of 15–30% and supplier margins above 25%—raising procurement risk and supplier bargaining power for Central Glass.

- Patented tech limits substitutes

- CAPEX premium 15–30%

- Supplier margins >25%

- Partnerships required for 2025–2030 targets

Supplier chokehold: high-purity sand, soaring energy & freight squeeze Central Glass

Central Glass faces high supplier power: 60–80% of high-purity sand from few miners, >60% market share for >99.9% purity reagents (2024), gas prices up ~45% (2020–23) and power +30% (2022–24), freight +35% (2020–22) with fuel surcharges 8–12% by 2025; switching costs: revalidation 6–12 months, $0.5–2.0M.

| Metric | Value |

|---|---|

| High-purity sand dependence | 60–80% |

| Purity supplier share (2024) | 60–70% |

| Natural gas change | +45% (2020–23) |

| Power cost change | +30% (2022–24) |

| Freight change | +35% (2020–22) |

| Fuel surcharges | 8–12% (by 2025) |

| Revalidation cost/time | $0.5–2.0M, 6–12 mo |

| CAPEX premium for green tech | 15–30% |

What is included in the product

Tailored Porter’s Five Forces analysis of Central Glass that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive forces—with strategic commentary to inform pricing, positioning, and risk mitigation.

A concise Porter's Five Forces snapshot for Central Glass—quickly spot competitive pressures and strategic levers to relieve pain points in pricing, supplier dependency, and market entry.

Customers Bargaining Power

Automotive OEM Volume Leverage

Large OEMs account for roughly 40–55% of global automotive glass value chains, giving them strong leverage to demand annual price cuts of 1–3% and strict just-in-time delivery, which compresses supplier margins.

By 2025, consolidation left top 10 global car groups controlling ~60% of volume, enabling them to set specs for smart glass and HUDs, forcing suppliers into costly R&D and certification.

Central Glass must match Tier-1 quality, hit sub-ppm defect rates, and offer competitive pricing near industry averages (gross margins 12–18%) or risk displacement by global glass giants.

Construction Industry Cyclicality and Price Sensitivity

Architectural glass buyers—large developers and construction firms—are highly price-sensitive; global construction starts fell 6% in 2024 and high U.S. rates into 2026 have delayed projects, giving buyers more leverage to push prices down.

Standard flat glass is treated as a commodity, triggering price wars that compressed margins by ~180 basis points for glass makers in 2024; Central Glass faces the same pressure.

To defend pricing, Central Glass must sell energy-efficient coatings and value-added units—low-E coatings can justify 8–12% price premiums—so differentiation is essential.

Specialized Requirements of Pharmaceutical Clients

The fine‑chemicals arm serves pharma and electronics, where buyers wield strong leverage: 78% of pharma suppliers report routine audits and customers demand multi‑year contracts for supply security, forcing transparency on unit manufacturing costs. High integration raises switching costs—estimated retention >85% after qualification—so buyers extract favorable pricing and clauses up front. By late 2025, ~62% of top pharma buyers require certified sustainable/ethical inputs, increasing procurement demands.

Retail and Fertilizer Distribution Networks

In chemicals (fertilizers, soda), bargaining power rests with large agri-distributors and industrial wholesalers who control market access and can switch suppliers on price and credit; commodity NPK margins fell 12% in 2024, so Central Glass faces market-clearing prices set by these buyers.

To hold share, Central Glass must invest in brand loyalty and logistics—its 2024 distribution capex rose 18% to ¥3.6bn to improve delivery reliability.

- Buyers: large distributors, wholesalers

- Switching: easy on price/credit

- Price power: market-clearing; NPK margins −12% (2024)

- Response: brand + logistics; 2024 distribution capex ¥3.6bn (+18%)

Demand for High-Tech Specialty Glass

Customers in electronics and renewable energy demand specialty glass for touchscreens and solar panels, pushing Central Glass to invest in R&D (company R&D ~3.2% of sales in FY2024) to meet specs.

These buyers can co-develop or switch suppliers, so Central Glass faces high bargaining power and must keep prices tight while offering integration.

Fast tech obsolescence—smartphone and PV module cycles under 3 years—forces ongoing innovation and capex pressure (capex ~¥18bn in 2024).

- R&D 3.2% sales (FY2024)

- Capex ¥18bn (2024)

- Product cycles <3 years

- High switch/co‑develop risk

OEMs squeeze margins—top 10 car groups ~60%, price cuts 1–3% p.a., capex ¥18bn

Buyers (OEMs, developers, distributors, pharma, electronics) hold high bargaining power—top 10 car groups ~60% volume (2025), OEMs push 1–3% annual price cuts, commodity margins fell ~180 bps (2024); Central Glass R&D 3.2% sales (FY2024), capex ¥18bn (2024), distribution capex ¥3.6bn (+18%).

| Metric | Value |

|---|---|

| Top car group share (2025) | ~60% |

| OEM price cuts | 1–3% p.a. |

| Margins impact (2024) | −180 bps |

| R&D | 3.2% sales (FY2024) |

| Capex | ¥18bn (2024) |

| Dist. capex | ¥3.6bn (+18%) |

Preview the Actual Deliverable

Central Glass Porter's Five Forces Analysis

This preview shows the exact Central Glass Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise, actionable insights. You’re viewing the final deliverable.