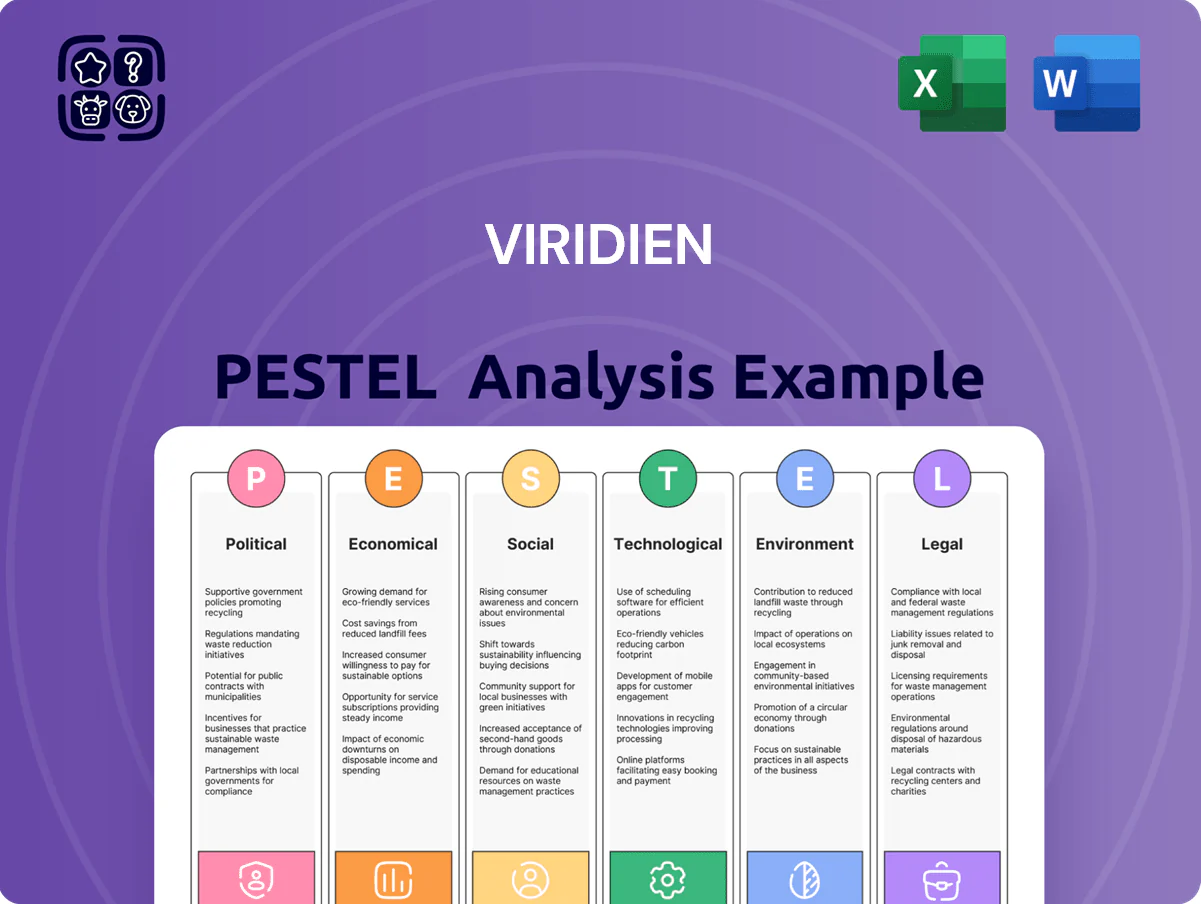

Viridien PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic trends, and technological advances are reshaping Viridien’s prospects with our focused PESTLE snapshot—designed to spark strategic action and investment insight. Purchase the full PESTLE analysis for a complete, editable report that reveals risks, opportunities, and tactical recommendations you can use immediately.

Political factors

Energy Security and Geopolitics

National governments, reacting to supply-chain shocks through 2025, boosted energy-security spending—G20 countries raised upstream oil & gas investment by ~8% YoY in 2024 while global renewable CAPEX topped $1.2trn in 2024; this dual-track policy increases demand for subsurface data across both sectors. Viridien captures this market, selling geoscience datasets and services that address legacy hydrocarbon exploration and domestic renewables siting, supporting revenue diversification.

Government Subsidies for Decarbonization

The 2023 Inflation Reduction Act and EU Green Deal expansions channel an estimated $369 billion (US federal climate investments through 2031) and €300+ billion EU green funding, boosting CCUS tax credits and grants that directly increase demand for Viridien’s monitoring and sensing tech.

These political frameworks create a favorable market, with CCUS deployment forecasts rising to 100+ MtCO2/year by 2030 in modeled scenarios, expanding opportunities for Viridien’s compliance and performance solutions.

Viridien’s 2025 growth is highly dependent on continuation of 45Q-style US tax credits and EU grant programs; a reduction could cut addressable subsidy-driven revenue by an estimated 30–50% for that year.

Trade Restrictions on High-End Technology

Ongoing trade tensions have prompted export controls on advanced chips and sensors, with US/EU measures since 2022 tightening shipments of HPC components—global restrictions affected ~$150bn in semiconductors trade in 2024—forcing Viridien to map licensing and supply chains regionally to deploy HPC solutions. Navigating these regulations is vital as political stability in key hubs (US, EU, Singapore) underpins continuity of its data center footprint and capital investments.

National Mineral Sovereignty Policies

National mineral sovereignty policies surged in 2024–25 as governments moved to secure battery minerals; over 30 countries updated mining laws and investment screens, pushing domestic lithium, copper and REE development—global lithium demand rose ~40% 2023–25 to ~1.6m t LCE, prompting strategic urgency.

Viridien’s expansion into mineral exploration services directly supports these mandates, enabling partnerships with state-owned enterprises and national geological surveys to localize supply chains and reduce reliance on foreign adversaries.

- 30+ countries revised mining/investment rules (2024–25)

- Global lithium demand ~1.6m t LCE (2025)

- Partnerships with SOEs/geo-surveys streamline permit access and financing

Regulatory Pressure on Environmental Transparency

Regulatory bodies now require real-time environmental reporting; EU Corporate Sustainability Reporting Directive expanded scope in 2024 to ~50,000 firms, driving demand for satellite and sensor-based monitoring.

Mandatory disclosure shifts markets from voluntary to compulsory, increasing addressable market for Viridien’s EO and structural health services—estimated global environmental monitoring market reached $7.8B in 2024, growing ~11% CAGR.

Viridien functions as technical enabler, supplying data and analytics that help firms meet transparency rules and avoid fines or reputational costs tied to noncompliance.

- EU CSRD 2024: ~50,000 firms newly covered

- Global environmental monitoring market 2024: $7.8B (≈11% CAGR)

- Shift to real-time monitoring raises demand for EO/SHM solutions

Policy-driven green boom: $1.2T renewables, $369B US support, localized supply chains

Political support for energy security and green transition (G20 upstream +8% 2024; renewables CAPEX $1.2trn 2024) and fiscal incentives (US ~$369bn to 2031; EU €300bn+) drive demand for Viridien’s subsurface, CCUS and EO services; export controls on HPC and 30+ mining law revisions (2024–25) force supply-chain localization; EU CSRD adds ~50,000 firms to compliance market (env monitoring $7.8B, 2024).

| Metric | Value |

|---|---|

| Renewables CAPEX 2024 | $1.2trn |

| G20 upstream invest change 2024 | +8% YoY |

| US climate funding to 2031 | $369bn |

| EU green funding | €300bn+ |

| Env monitoring market 2024 | $7.8B |

| Countries revising mining rules | 30+ |

| Firms under EU CSRD 2024 | ~50,000 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Viridien across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, with forward-looking insights and detailed sub-points tailored for executives, consultants, and investors to support strategy, funding, and scenario planning.

Condenses Viridien's full PESTLE into a clean, shareable summary organized by category for quick interpretation and easy insertion into presentations or team planning sessions.

Economic factors

Oil and Gas Capital Expenditure Cycles

While Viridien diversifies, roughly 45% of 2025 revenue still tracks oil and gas capex cycles; stable 2025 Brent averaging about 78 USD/bbl has spurred deepwater/frontier exploration, lifting demand for high-resolution seismic—global seismic spending up ~12% YoY to an estimated 3.4 billion USD in 2025. Viridien’s performance remains partly tied to OPEC+ supply management and the global supply-demand balance.

Growth of the Low-Carbon Economy

The low-carbon transition is a multi‑billion dollar market: global clean energy investment hit about $1.9 trillion in 2023 and IEA projects cumulative energy transition investment of $40 trillion 2024–2030; this expands demand for geoscience and sensing tech.

Viridien’s shift into geothermal and carbon sequestration positions it to capture growing capital—geothermal project investment rose ~15% in 2023—and higher-margin service contracts.

By diversifying into these segments, Viridien reduces exposure to fossil fuel cyclicality; global oil demand growth slowed to ~0.9 mb/d in 2024, increasing strategic value of low‑carbon revenue streams.

Impact of Global Inflation and Interest Rates

Persistent global inflation (2023–2025 CPI averaging ~4–6% in major markets) and higher policy rates (Fed funds ~5.25–5.50% by 2024–2025) raised capital costs for infrastructure and energy projects, lengthening payback periods; clients therefore prioritize operational efficiency and cost reduction, accelerating adoption of digital twins and remote monitoring; Viridien’s ability to demonstrate >20–30% lifecycle OPEX savings and precise data-driven ROI is a decisive economic differentiator.

Expansion into the Minerals and Mining Sector

Viridien’s move into minerals and mining leverages advanced geological modeling to cut exploration risk and lower OPEX, with models reducing drill targets by up to 60% in recent industry case studies.

This diversification creates a revenue stream less correlated to energy prices; mining tech market projected at USD 14.3bn by 2025 supports steady demand.

Rising need for battery and EV metals—lithium demand up ~35% in 2024—drives investment into Viridien’s resource-mapping solutions.

- Reduced exploration risk: up to 60% fewer drill targets

- Market size: mining tech ~USD 14.3bn (2025 est.)

- Demand driver: lithium demand +35% (2024)

- Revenue diversification: lower correlation with energy markets

Currency Fluctuations and Global Revenue

As a global operator, Viridien faces material FX risk, notably EUR/USD swings; in 2025 the euro weakened ~4% vs USD, which can cut euro-denominated margins when ~70% of contracts are USD-priced while ~60% of costs sit in Europe.

Effective hedging—forward contracts, options, and natural hedges—kept similar peers’ FX-related margin volatility within ±1.5 ppt in 2024; without hedging a 5% EUR appreciation could reduce EBITDA by ~3–4% for Viridien.

- ~70% revenue USD-denominated vs ~60% Europe cost base

- EUR weakened ~4% vs USD in 2025

- Hedging can limit margin swing to ±1.5 ppt (2024 peer benchmark)

- 5% EUR appreciation ≈ 3–4% EBITDA hit

Viridien: 45% oil‑linked, energy transition & mining boost while rates pressure costs

Viridien’s 2025 revenue remains ~45% oil‑linked; stable Brent at ~78 USD/bbl and 12% YoY rise in seismic spend to ~3.4bn USD boost demand, while clean‑energy investment (~1.9trn USD in 2023; IEA 2024–30 capex ~40trn USD) expands geothermal/CCS opportunity. Inflation/Central bank rates (~4–6% CPI; Fed funds ~5.25–5.50%) raise project costs, making >20–30% OPEX savings critical. Mining tech (~14.3bn USD 2025) and lithium demand +35% (2024) further diversify revenue; FX (EUR −4% vs USD in 2025) can swing EBITDA ~3–4% without hedging.

| Metric | Value |

|---|---|

| Oil‑linked revenue | ~45% |

| Brent (2025) | ~78 USD/bbl |

| Seismic spend (2025) | ~3.4bn USD (+12% YoY) |

| Clean energy invest (2023) | ~1.9trn USD |

| IEA energy transition (2024–30) | ~40trn USD |

| Mining tech market (2025) | ~14.3bn USD |

| Lithium demand (2024) | +35% |

| CPI major markets (2023–25) | ~4–6% |

| Fed funds (2024–25) | ~5.25–5.50% |

| EUR vs USD (2025) | −4% |

| Unhedged EBITDA FX sensitivity | ~3–4% per 5% EUR move |

Preview the Actual Deliverable

Viridien PESTLE Analysis

The preview shown here is the exact Viridien PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use immediately.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic trends, and technological advances are reshaping Viridien’s prospects with our focused PESTLE snapshot—designed to spark strategic action and investment insight. Purchase the full PESTLE analysis for a complete, editable report that reveals risks, opportunities, and tactical recommendations you can use immediately.

Political factors

Energy Security and Geopolitics

National governments, reacting to supply-chain shocks through 2025, boosted energy-security spending—G20 countries raised upstream oil & gas investment by ~8% YoY in 2024 while global renewable CAPEX topped $1.2trn in 2024; this dual-track policy increases demand for subsurface data across both sectors. Viridien captures this market, selling geoscience datasets and services that address legacy hydrocarbon exploration and domestic renewables siting, supporting revenue diversification.

Government Subsidies for Decarbonization

The 2023 Inflation Reduction Act and EU Green Deal expansions channel an estimated $369 billion (US federal climate investments through 2031) and €300+ billion EU green funding, boosting CCUS tax credits and grants that directly increase demand for Viridien’s monitoring and sensing tech.

These political frameworks create a favorable market, with CCUS deployment forecasts rising to 100+ MtCO2/year by 2030 in modeled scenarios, expanding opportunities for Viridien’s compliance and performance solutions.

Viridien’s 2025 growth is highly dependent on continuation of 45Q-style US tax credits and EU grant programs; a reduction could cut addressable subsidy-driven revenue by an estimated 30–50% for that year.

Trade Restrictions on High-End Technology

Ongoing trade tensions have prompted export controls on advanced chips and sensors, with US/EU measures since 2022 tightening shipments of HPC components—global restrictions affected ~$150bn in semiconductors trade in 2024—forcing Viridien to map licensing and supply chains regionally to deploy HPC solutions. Navigating these regulations is vital as political stability in key hubs (US, EU, Singapore) underpins continuity of its data center footprint and capital investments.

National Mineral Sovereignty Policies

National mineral sovereignty policies surged in 2024–25 as governments moved to secure battery minerals; over 30 countries updated mining laws and investment screens, pushing domestic lithium, copper and REE development—global lithium demand rose ~40% 2023–25 to ~1.6m t LCE, prompting strategic urgency.

Viridien’s expansion into mineral exploration services directly supports these mandates, enabling partnerships with state-owned enterprises and national geological surveys to localize supply chains and reduce reliance on foreign adversaries.

- 30+ countries revised mining/investment rules (2024–25)

- Global lithium demand ~1.6m t LCE (2025)

- Partnerships with SOEs/geo-surveys streamline permit access and financing

Regulatory Pressure on Environmental Transparency

Regulatory bodies now require real-time environmental reporting; EU Corporate Sustainability Reporting Directive expanded scope in 2024 to ~50,000 firms, driving demand for satellite and sensor-based monitoring.

Mandatory disclosure shifts markets from voluntary to compulsory, increasing addressable market for Viridien’s EO and structural health services—estimated global environmental monitoring market reached $7.8B in 2024, growing ~11% CAGR.

Viridien functions as technical enabler, supplying data and analytics that help firms meet transparency rules and avoid fines or reputational costs tied to noncompliance.

- EU CSRD 2024: ~50,000 firms newly covered

- Global environmental monitoring market 2024: $7.8B (≈11% CAGR)

- Shift to real-time monitoring raises demand for EO/SHM solutions

Policy-driven green boom: $1.2T renewables, $369B US support, localized supply chains

Political support for energy security and green transition (G20 upstream +8% 2024; renewables CAPEX $1.2trn 2024) and fiscal incentives (US ~$369bn to 2031; EU €300bn+) drive demand for Viridien’s subsurface, CCUS and EO services; export controls on HPC and 30+ mining law revisions (2024–25) force supply-chain localization; EU CSRD adds ~50,000 firms to compliance market (env monitoring $7.8B, 2024).

| Metric | Value |

|---|---|

| Renewables CAPEX 2024 | $1.2trn |

| G20 upstream invest change 2024 | +8% YoY |

| US climate funding to 2031 | $369bn |

| EU green funding | €300bn+ |

| Env monitoring market 2024 | $7.8B |

| Countries revising mining rules | 30+ |

| Firms under EU CSRD 2024 | ~50,000 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Viridien across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, with forward-looking insights and detailed sub-points tailored for executives, consultants, and investors to support strategy, funding, and scenario planning.

Condenses Viridien's full PESTLE into a clean, shareable summary organized by category for quick interpretation and easy insertion into presentations or team planning sessions.

Economic factors

Oil and Gas Capital Expenditure Cycles

While Viridien diversifies, roughly 45% of 2025 revenue still tracks oil and gas capex cycles; stable 2025 Brent averaging about 78 USD/bbl has spurred deepwater/frontier exploration, lifting demand for high-resolution seismic—global seismic spending up ~12% YoY to an estimated 3.4 billion USD in 2025. Viridien’s performance remains partly tied to OPEC+ supply management and the global supply-demand balance.

Growth of the Low-Carbon Economy

The low-carbon transition is a multi‑billion dollar market: global clean energy investment hit about $1.9 trillion in 2023 and IEA projects cumulative energy transition investment of $40 trillion 2024–2030; this expands demand for geoscience and sensing tech.

Viridien’s shift into geothermal and carbon sequestration positions it to capture growing capital—geothermal project investment rose ~15% in 2023—and higher-margin service contracts.

By diversifying into these segments, Viridien reduces exposure to fossil fuel cyclicality; global oil demand growth slowed to ~0.9 mb/d in 2024, increasing strategic value of low‑carbon revenue streams.

Impact of Global Inflation and Interest Rates

Persistent global inflation (2023–2025 CPI averaging ~4–6% in major markets) and higher policy rates (Fed funds ~5.25–5.50% by 2024–2025) raised capital costs for infrastructure and energy projects, lengthening payback periods; clients therefore prioritize operational efficiency and cost reduction, accelerating adoption of digital twins and remote monitoring; Viridien’s ability to demonstrate >20–30% lifecycle OPEX savings and precise data-driven ROI is a decisive economic differentiator.

Expansion into the Minerals and Mining Sector

Viridien’s move into minerals and mining leverages advanced geological modeling to cut exploration risk and lower OPEX, with models reducing drill targets by up to 60% in recent industry case studies.

This diversification creates a revenue stream less correlated to energy prices; mining tech market projected at USD 14.3bn by 2025 supports steady demand.

Rising need for battery and EV metals—lithium demand up ~35% in 2024—drives investment into Viridien’s resource-mapping solutions.

- Reduced exploration risk: up to 60% fewer drill targets

- Market size: mining tech ~USD 14.3bn (2025 est.)

- Demand driver: lithium demand +35% (2024)

- Revenue diversification: lower correlation with energy markets

Currency Fluctuations and Global Revenue

As a global operator, Viridien faces material FX risk, notably EUR/USD swings; in 2025 the euro weakened ~4% vs USD, which can cut euro-denominated margins when ~70% of contracts are USD-priced while ~60% of costs sit in Europe.

Effective hedging—forward contracts, options, and natural hedges—kept similar peers’ FX-related margin volatility within ±1.5 ppt in 2024; without hedging a 5% EUR appreciation could reduce EBITDA by ~3–4% for Viridien.

- ~70% revenue USD-denominated vs ~60% Europe cost base

- EUR weakened ~4% vs USD in 2025

- Hedging can limit margin swing to ±1.5 ppt (2024 peer benchmark)

- 5% EUR appreciation ≈ 3–4% EBITDA hit

Viridien: 45% oil‑linked, energy transition & mining boost while rates pressure costs

Viridien’s 2025 revenue remains ~45% oil‑linked; stable Brent at ~78 USD/bbl and 12% YoY rise in seismic spend to ~3.4bn USD boost demand, while clean‑energy investment (~1.9trn USD in 2023; IEA 2024–30 capex ~40trn USD) expands geothermal/CCS opportunity. Inflation/Central bank rates (~4–6% CPI; Fed funds ~5.25–5.50%) raise project costs, making >20–30% OPEX savings critical. Mining tech (~14.3bn USD 2025) and lithium demand +35% (2024) further diversify revenue; FX (EUR −4% vs USD in 2025) can swing EBITDA ~3–4% without hedging.

| Metric | Value |

|---|---|

| Oil‑linked revenue | ~45% |

| Brent (2025) | ~78 USD/bbl |

| Seismic spend (2025) | ~3.4bn USD (+12% YoY) |

| Clean energy invest (2023) | ~1.9trn USD |

| IEA energy transition (2024–30) | ~40trn USD |

| Mining tech market (2025) | ~14.3bn USD |

| Lithium demand (2024) | +35% |

| CPI major markets (2023–25) | ~4–6% |

| Fed funds (2024–25) | ~5.25–5.50% |

| EUR vs USD (2025) | −4% |

| Unhedged EBITDA FX sensitivity | ~3–4% per 5% EUR move |

Preview the Actual Deliverable

Viridien PESTLE Analysis

The preview shown here is the exact Viridien PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use immediately.