Aluminum Corp. Of China Business Model Canvas

Aluminum Corp. of China: Compact Business Model Canvas for Strategic Investors

Unlock the full strategic blueprint behind Aluminum Corp. Of China with a concise Business Model Canvas that maps its value propositions, key partners, revenue streams, and cost structure—perfect for investors, consultants, and entrepreneurs seeking actionable insights.

Partnerships

State-Owned Enterprise Strategic Alliances

CHALCO (Aluminum Corp. of China) leverages state-owned enterprise alliances and government ties to secure preferential roles in projects—49% of its 2024 domestic alumina supply came via SOE partners—and access low-cost state-linked financing (2024 weighted borrowing cost ~3.8% vs. 6.2% market). By end-2025 these links are vital for meeting China’s decarbonization rules and green-capex plans totaling RMB 12.3 billion.

Overseas Mining Joint Ventures

Aluminum Corp of China (Chalco) partners with foreign firms and governments—notably in Guinea and Indonesia—to secure bauxite; its 2024 Guinea joint ventures target ~20–25 Mt/year bauxite, cutting reliance on domestic reserves by ~35%.

These JVs co-invest in ports, rail and processing; Chalco disclosed ~USD 450–600m capex across West African logistics projects in 2023–24 to steady high-quality feedstock flows.

Energy and Utility Providers

CHALCO partners with power generators to secure stable, low-cost supply for smelting; in 2024 about 28% of its electricity came from renewables after deals adding 4.2 TWh hydro and 1.1 TWh wind/solar capacity, cutting coal share and locking long-term tariffs that shave ~8–12% off energy cost per tonne. These contracts also support CHALCO’s 2030 goal to cut scope 2 emissions 40% versus 2020, meeting investor ESG covenants.

Research and Academic Institutions

- 15%+ energy intensity reduction target by 2025

- 20% waste output reduction target by 2025

- Specialty alloys ≈12% of 2024 revenue

- Focus: aerospace, EV, semiconductor markets

Logistics and Maritime Shipping Partners

CHALCO locks multi-year contracts with global shipping lines and China Railway Corp to move ~18–22 million tonnes/year of bauxite, alumina, and aluminum between African mines, domestic refineries, and 2025 global buyers, cutting lead times and lowering inventory finance costs by an estimated 6–9% annually.

- Annual volume: 18–22 Mt

- Inventory cost cut: ~6–9%/year

- Key carriers: major global liners + China Railway

- Geography: Africa → China → global customers

CHALCO: SOE-backed low-cost finance, 49% domestic alumina, big green & overseas capex

CHALCO relies on SOE & government ties for low-cost finance (~3.8% 2024 borrowing), SOE-sourced 49% of domestic alumina 2024, and RMB12.3bn green capex through 2025; overseas JVs (Guinea/Indonesia) target 20–25 Mt/y bauxite and ~USD450–600m logistics capex (2023–24); power and renewables deals supplied 28% renewables in 2024, cutting energy cost 8–12%/t.

| Metric | 2024/Target |

|---|---|

| SOE alumina share | 49% |

| Borrowing cost | 3.8% (2024) |

| Bauxite JV target | 20–25 Mt/y |

| Logistics capex | USD450–600m (2023–24) |

| Renewable power | 28% (2024) |

| Green capex | RMB12.3bn (to 2025) |

What is included in the product

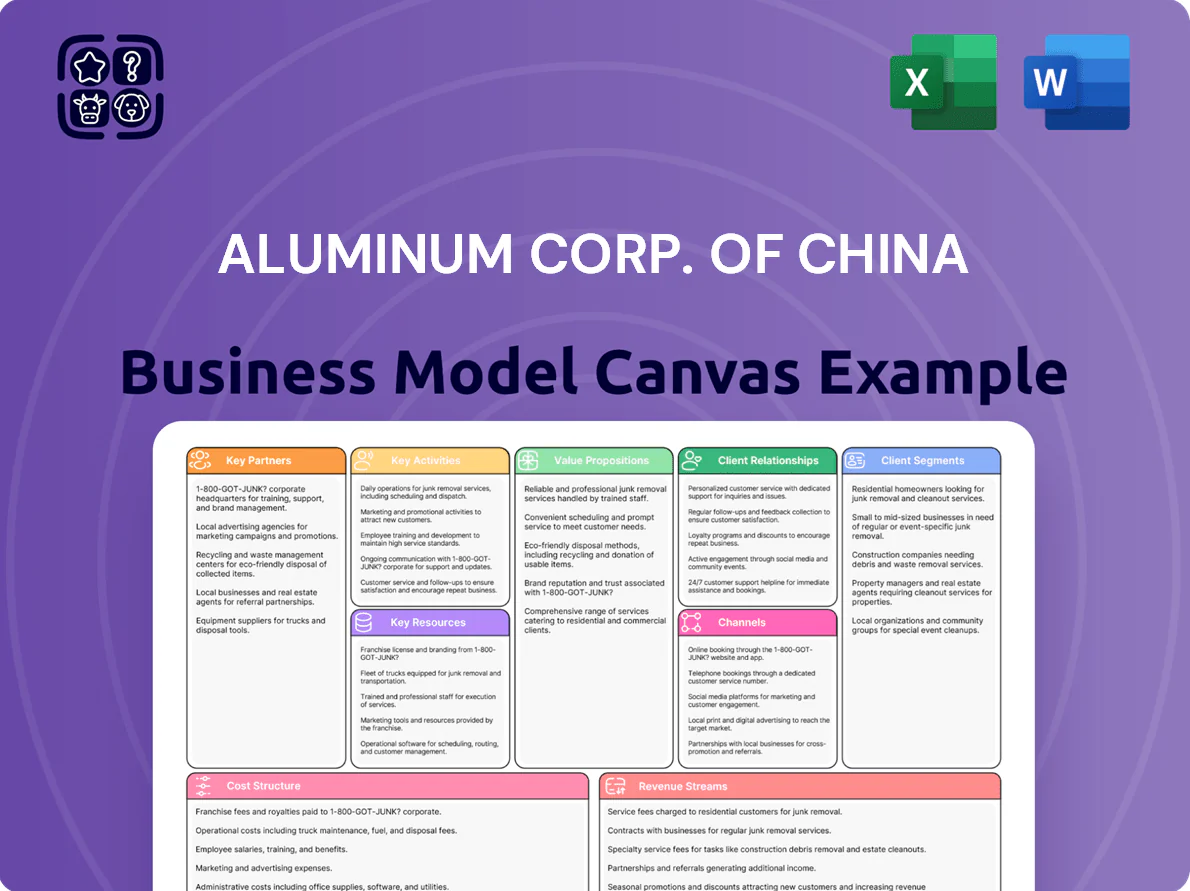

A concise, pre-written Business Model Canvas for Aluminum Corp. of China detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams aligned with its integrated alumina‑to‑aluminium operations and downstream markets.

High-level view of Aluminum Corp. of China's business model with editable cells, letting teams quickly pinpoint value drivers, cost structures, and supply-chain risks to streamline strategic decisions and investor briefings.

Activities

Bauxite Mining and Alumina Refining

The core of CHALCO operations is large-scale bauxite extraction and chemical refining into alumina, processing about 25 million tonnes of bauxite and producing ~8.2 million tonnes of alumina in 2024 to secure feedstock for smelting. Vertical integration cuts input costs and stabilizes quality, and by 2025 CHALCO improved alumina yield by ~3.5% and reduced red mud discharge intensity by ~18% through reprocessing and dry stacking.

Primary Aluminum Smelting

A significant portion of effort goes to electrolytic reduction of alumina into primary aluminum, where Chalco managed 2024 electrolytic capacity of ~4.2 million tonnes and targeted 8% potline efficiency gains to protect margins amid LME aluminum averaging $2,300/ton in 2024; tight power load management and pot efficiency keep production costs near RMB 14,000/ton, while quality controls sustain >99.7% purity and steady industrial volumes for auto and construction clients.

Research and Product Development

CHALCO invests ~RMB 2.3 billion in R&D (2024) to develop lightweight, high-strength aluminum alloys for automotive, aerospace and electronics, targeting EV bodies and battery enclosures that cut vehicle mass 10–15% and improve range; R&D also advances low-carbon smelting (aim: 30% CO2 reduction per ton by 2030 vs 2020) to lower production emissions and energy intensity.

Energy Management and Coal Production

Aluminum Corp. of China runs captive coal mines and 7.4 GW of thermal power to feed 2024 smelting of ~3.6 Mt Al, while adding wind/solar and 1.2 GW hydro to cut scope 2 emissions toward China’s 2060 target; energy control trims input-cost volatility and protected 2024 EBITDA margin by an estimated 120–180 bps versus peers.

- Captive coal & power: 7.4 GW thermal

- Green build: +1.2 GW hydro; incremental wind/solar

- 2024 smelting: ~3.6 Mt Al

- Margin benefit: ~120–180 bps vs peers in 2024

Commodity Trading and Marketing

Aluminum Corp. of China trades alumina, primary aluminum and inputs on domestic and LME markets, using hedges (forwards, options) to cut price volatility and shift ~2024 sales to higher-margin quarters; commodity sales made up ~28% of 2024 revenue (RMB basis) and helped protect EBITDA vs spot swings.

Marketing targets multi-year supply contracts with steel, auto and aerospace buyers worldwide, securing ~3–5 year off-take deals that reduce working-capital swings and improve forecastability.

- Trades on SHFE and LME

- Hedging: forwards, options

- 2024: ~28% revenue from commodity sales

- Focus: 3–5 year off-take contracts

CHALCO: Integrated bauxite-to-aluminium maker with 8.6 GW power, strong hedging & R&D

CHALCO runs integrated bauxite→alumina→smelting operations (2024: 25 Mt bauxite, ~8.2 Mt alumina, ~3.6 Mt Al), operates 7.4 GW thermal + 1.2 GW hydro/wind+solar, invested ~RMB 2.3 bn R&D (2024), and hedges commodities (2024: ~28% revenue) while securing 3–5yr off-take contracts to stabilize margins.

| Metric | 2024 |

|---|---|

| Bauxite | 25 Mt |

| Alumina | 8.2 Mt |

| Aluminum | 3.6 Mt |

| Power | 7.4 GW thermal +1.2 GW renew |

| R&D spend | RMB 2.3 bn |

| Commodity revenue | 28% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact Business Model Canvas for Aluminum Corp. of China—not a mockup or sample—and it’s the same file you’ll receive after purchase, ready for editing and presentation.

What you see is a direct snapshot of the final deliverable: upon completing your order you’ll instantly unlock the complete document in editable formats, structured and formatted exactly as previewed.

No placeholders or marketing examples—this live preview contains the real content and layout, so there are no surprises when you download the full file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Aluminum Corp. of China: Compact Business Model Canvas for Strategic Investors

Unlock the full strategic blueprint behind Aluminum Corp. Of China with a concise Business Model Canvas that maps its value propositions, key partners, revenue streams, and cost structure—perfect for investors, consultants, and entrepreneurs seeking actionable insights.

Partnerships

State-Owned Enterprise Strategic Alliances

CHALCO (Aluminum Corp. of China) leverages state-owned enterprise alliances and government ties to secure preferential roles in projects—49% of its 2024 domestic alumina supply came via SOE partners—and access low-cost state-linked financing (2024 weighted borrowing cost ~3.8% vs. 6.2% market). By end-2025 these links are vital for meeting China’s decarbonization rules and green-capex plans totaling RMB 12.3 billion.

Overseas Mining Joint Ventures

Aluminum Corp of China (Chalco) partners with foreign firms and governments—notably in Guinea and Indonesia—to secure bauxite; its 2024 Guinea joint ventures target ~20–25 Mt/year bauxite, cutting reliance on domestic reserves by ~35%.

These JVs co-invest in ports, rail and processing; Chalco disclosed ~USD 450–600m capex across West African logistics projects in 2023–24 to steady high-quality feedstock flows.

Energy and Utility Providers

CHALCO partners with power generators to secure stable, low-cost supply for smelting; in 2024 about 28% of its electricity came from renewables after deals adding 4.2 TWh hydro and 1.1 TWh wind/solar capacity, cutting coal share and locking long-term tariffs that shave ~8–12% off energy cost per tonne. These contracts also support CHALCO’s 2030 goal to cut scope 2 emissions 40% versus 2020, meeting investor ESG covenants.

Research and Academic Institutions

- 15%+ energy intensity reduction target by 2025

- 20% waste output reduction target by 2025

- Specialty alloys ≈12% of 2024 revenue

- Focus: aerospace, EV, semiconductor markets

Logistics and Maritime Shipping Partners

CHALCO locks multi-year contracts with global shipping lines and China Railway Corp to move ~18–22 million tonnes/year of bauxite, alumina, and aluminum between African mines, domestic refineries, and 2025 global buyers, cutting lead times and lowering inventory finance costs by an estimated 6–9% annually.

- Annual volume: 18–22 Mt

- Inventory cost cut: ~6–9%/year

- Key carriers: major global liners + China Railway

- Geography: Africa → China → global customers

CHALCO: SOE-backed low-cost finance, 49% domestic alumina, big green & overseas capex

CHALCO relies on SOE & government ties for low-cost finance (~3.8% 2024 borrowing), SOE-sourced 49% of domestic alumina 2024, and RMB12.3bn green capex through 2025; overseas JVs (Guinea/Indonesia) target 20–25 Mt/y bauxite and ~USD450–600m logistics capex (2023–24); power and renewables deals supplied 28% renewables in 2024, cutting energy cost 8–12%/t.

| Metric | 2024/Target |

|---|---|

| SOE alumina share | 49% |

| Borrowing cost | 3.8% (2024) |

| Bauxite JV target | 20–25 Mt/y |

| Logistics capex | USD450–600m (2023–24) |

| Renewable power | 28% (2024) |

| Green capex | RMB12.3bn (to 2025) |

What is included in the product

A concise, pre-written Business Model Canvas for Aluminum Corp. of China detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams aligned with its integrated alumina‑to‑aluminium operations and downstream markets.

High-level view of Aluminum Corp. of China's business model with editable cells, letting teams quickly pinpoint value drivers, cost structures, and supply-chain risks to streamline strategic decisions and investor briefings.

Activities

Bauxite Mining and Alumina Refining

The core of CHALCO operations is large-scale bauxite extraction and chemical refining into alumina, processing about 25 million tonnes of bauxite and producing ~8.2 million tonnes of alumina in 2024 to secure feedstock for smelting. Vertical integration cuts input costs and stabilizes quality, and by 2025 CHALCO improved alumina yield by ~3.5% and reduced red mud discharge intensity by ~18% through reprocessing and dry stacking.

Primary Aluminum Smelting

A significant portion of effort goes to electrolytic reduction of alumina into primary aluminum, where Chalco managed 2024 electrolytic capacity of ~4.2 million tonnes and targeted 8% potline efficiency gains to protect margins amid LME aluminum averaging $2,300/ton in 2024; tight power load management and pot efficiency keep production costs near RMB 14,000/ton, while quality controls sustain >99.7% purity and steady industrial volumes for auto and construction clients.

Research and Product Development

CHALCO invests ~RMB 2.3 billion in R&D (2024) to develop lightweight, high-strength aluminum alloys for automotive, aerospace and electronics, targeting EV bodies and battery enclosures that cut vehicle mass 10–15% and improve range; R&D also advances low-carbon smelting (aim: 30% CO2 reduction per ton by 2030 vs 2020) to lower production emissions and energy intensity.

Energy Management and Coal Production

Aluminum Corp. of China runs captive coal mines and 7.4 GW of thermal power to feed 2024 smelting of ~3.6 Mt Al, while adding wind/solar and 1.2 GW hydro to cut scope 2 emissions toward China’s 2060 target; energy control trims input-cost volatility and protected 2024 EBITDA margin by an estimated 120–180 bps versus peers.

- Captive coal & power: 7.4 GW thermal

- Green build: +1.2 GW hydro; incremental wind/solar

- 2024 smelting: ~3.6 Mt Al

- Margin benefit: ~120–180 bps vs peers in 2024

Commodity Trading and Marketing

Aluminum Corp. of China trades alumina, primary aluminum and inputs on domestic and LME markets, using hedges (forwards, options) to cut price volatility and shift ~2024 sales to higher-margin quarters; commodity sales made up ~28% of 2024 revenue (RMB basis) and helped protect EBITDA vs spot swings.

Marketing targets multi-year supply contracts with steel, auto and aerospace buyers worldwide, securing ~3–5 year off-take deals that reduce working-capital swings and improve forecastability.

- Trades on SHFE and LME

- Hedging: forwards, options

- 2024: ~28% revenue from commodity sales

- Focus: 3–5 year off-take contracts

CHALCO: Integrated bauxite-to-aluminium maker with 8.6 GW power, strong hedging & R&D

CHALCO runs integrated bauxite→alumina→smelting operations (2024: 25 Mt bauxite, ~8.2 Mt alumina, ~3.6 Mt Al), operates 7.4 GW thermal + 1.2 GW hydro/wind+solar, invested ~RMB 2.3 bn R&D (2024), and hedges commodities (2024: ~28% revenue) while securing 3–5yr off-take contracts to stabilize margins.

| Metric | 2024 |

|---|---|

| Bauxite | 25 Mt |

| Alumina | 8.2 Mt |

| Aluminum | 3.6 Mt |

| Power | 7.4 GW thermal +1.2 GW renew |

| R&D spend | RMB 2.3 bn |

| Commodity revenue | 28% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact Business Model Canvas for Aluminum Corp. of China—not a mockup or sample—and it’s the same file you’ll receive after purchase, ready for editing and presentation.

What you see is a direct snapshot of the final deliverable: upon completing your order you’ll instantly unlock the complete document in editable formats, structured and formatted exactly as previewed.

No placeholders or marketing examples—this live preview contains the real content and layout, so there are no surprises when you download the full file.