Chongqing Changan Auto Porter's Five Forces Analysis

From Overview to Strategy Blueprint

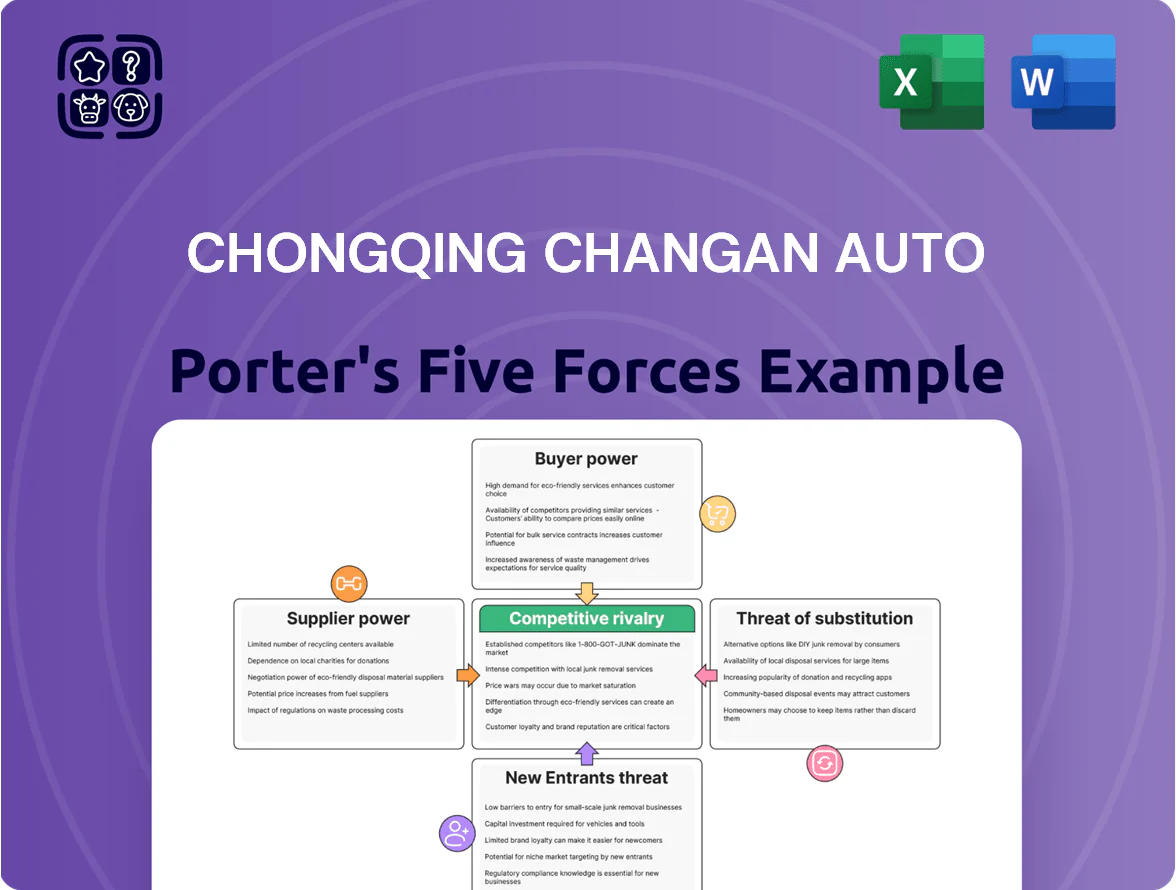

Chongqing Changan Auto faces intense rivalry from domestic and global OEMs, rising buyer expectations on EVs, and supplier pressures amid localized supply chains; regulatory shifts and tech change raise entry barriers but also open disruptor opportunities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Chongqing Changan Auto’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of EV battery supply

The bargaining power of suppliers is high because a few firms—led by CATL (Contemporary Amperex Technology Co. Limited), which held about 35% global EV battery capacity in 2024—dominate supply, giving them pricing leverage over Changan.

Batteries are Changan’s largest new-energy vehicle cost component, roughly 30–40% of EV BOM (bill of materials), so supplier price moves materially affect margins.

By late 2025 Changan has diversified contracts with BYD and Gotion, but technical specs and scale needs for high-energy-density cells keep the pool of viable partners small, constraining bargaining power.

Strategic dependence on semiconductor and AI chip providers

Changan’s shift to intelligent and autonomous driving raises strategic dependence on high-end semiconductor firms such as Nvidia and Qualcomm; in 2025 these vendors account for roughly 60–70% of AI compute modules used in China’s mid-to-high EV segment.

Specialized chips power smart cockpits and ADAS (advanced driver-assistance systems), and global supply tightness kept fab utilization above 90% in 2024, driving chip premiums of 15–25% versus commodity ICs.

This scarcity plus integration complexity gives suppliers leverage to affect Changan’s production timing and BOM (bill of materials) costs, where AI module spend can be 8–12% of vehicle unit cost in flagship models.

Partnerships with technology giants like Huawei

Changan’s deep collaboration with Huawei via Avatr creates a supplier dynamic where Huawei supplies core software, cloud services, and chips for intelligent driving, making provider switching costly; Avatr sales reached about 38,000 units in 2024, tying tech identity to Huawei’s stack. This elevates Huawei’s bargaining power above a typical parts maker, since losing Huawei would erode features and brand positioning and require large R&D and integration spend to replace.

Raw material price volatility impact

Suppliers of lithium, cobalt, and nickel keep price volatility high; lithium carbonate rose ~60% in 2021–22 and metal prices still swing 20–40% year-to-year, pressuring Changan’s EV cost base.

Changan uses multi-year contracts and spot buys, but upstream supply tied to China, Congo, and Australia markets means sudden spikes can erode margins; flexible procurement and hedging are essential.

- 2024 lithium avg price ≈ $60,000/ton

- Nickel spot up 25% YoY (2024)

- Long-term contracts cover ~30–50% of needs

Lower power of traditional mechanical component suppliers

Lower supplier power for traditional mechanical parts: unlike semiconductors, suppliers of engines, chassis parts, and interior trims face low bargaining power because these are standardized; over 300 domestic and 120 international vendors can meet Changan's specs as of 2025, enabling competitive bids and unit-cost reductions of ~3–5% annually on non-electronic components.

Supplier Dominance: CATL & AI Chips Drive EV/AI Cost Risk amid Lithium Volatility

Suppliers hold high power: CATL ~35% global EV battery capacity (2024), batteries = 30–40% EV BOM, chip suppliers (Nvidia/Qualcomm) supply 60–70% AI compute (2025), AI modules = 8–12% unit cost, commodity metal volatility (lithium ≈ $60,000/t in 2024) raises margin risk; traditional mechanical parts have low supplier power (300+ domestic vendors, 120+ international, 3–5% annual cost decline).

| Item | Metric |

|---|---|

| CATL share | ~35% (2024) |

| Battery share of BOM | 30–40% |

| AI chip vendors | 60–70% (2025) |

| Lithium price | ~$60,000/t (2024) |

What is included in the product

Tailored Five Forces analysis for Chongqing Changan Auto uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitution risks, highlighting disruptive threats, pricing leverage, and strategic levers to protect market share.

A concise Chongqing Changan Auto Porter’s Five Forces one-sheet—quickly highlights supplier power, buyer leverage, rivalry intensity, entry threats, and substitutes to speed strategic choices and investor briefings.

Customers Bargaining Power

High price sensitivity in a crowded market

By end-2025, intense price competition in China gives buyers strong leverage; new-car price cuts averaged 6–8% across urban markets in 2024–25, pushing customers to compare Changan directly with BYD, Geely, and Tesla on price and features.

Changan faces high price sensitivity: online price-shoppers exceed 70% in tier-1 cities, so the firm often uses discounts or adds features—Changan reported a 4.2% average transaction discount in H1 2025—to defend share.

Low switching costs for vehicle buyers

The EV shift has cut switching barriers: by end-2024 China had 14.3 million NEVs and 680,000 public chargers, making charging largely interoperable, so buyers face few technical hurdles moving from Changan to rivals.

Standardized charging standards (GB/T and increasingly CCS2) and converging in-car UIs reduce lock-in, so price, range, and software updates drive brand choice.

Abundance of choice across all segments

In 2025 consumers can choose from over 6,000 passenger vehicle SKUs in China across sedans, SUVs and MPVs, so Changan faces intense choice-driven bargaining power.

Changan competes with domestic rivals like Geely and BYD, global groups such as Volkswagen and Toyota, plus tech-led entrants (e.g., Xpeng), raising price and feature sensitivity.

Market saturation means a 1% slip in perceived value or a 0.5‑point drop in JD Power satisfaction can shift buyers to alternatives, so innovation and service are decisive.

Increased transparency through digital platforms

The rise of automotive social media and review platforms has pushed information transparency: 2024 surveys show 72% of Chinese EV buyers consult online reviews and real-world range reports before purchase, up from 58% in 2021.

Easy access to software-bug logs, ownership forums, and dealership service ratings limits Changan’s control of the narrative and increases bargaining power of informed buyers.

- 72% of buyers use online reviews (2024)

- Real-world range reports lower trust variance by 35%

- Dealership service ratings drive 15% purchase deferral

Rising demand for personalized and smart features

Customers now expect deep customization and smart features as standard, driving Changan to refresh software and hardware faster; Chinese new-energy vehicle buyers rated in 2024 that 62% view in-car software updates as a key purchase factor.

This customer power forces higher R&D spend—Changan increased R&D to 6.2% of revenue in 2024—to keep pace with seasonal 'must-have' features and shorten product cycles.

- 62% of NEV buyers prioritize software updates

- Changan R&D = 6.2% of revenue (2024)

- Shorter product cycles raise development costs

Buyers Win: 6–8% Price Cuts, 14.3M NEVs & Changan’s 6.2% R&D Push

Buyers hold strong leverage: 6–8% average new-car price cuts (2024–25), 70%+ online price-shoppers in tier‑1, 72% consult reviews (2024), 14.3M NEVs and 680k public chargers (end‑2024) lower switching costs; Changan R&D hit 6.2% of revenue (2024) to compete on software, range and price.

| Metric | Value |

|---|---|

| Price cuts | 6–8% |

| Online shoppers | 70%+ |

| Review users | 72% |

| NEVs | 14.3M |

| Chargers | 680k |

| Changan R&D | 6.2% |

Full Version Awaits

Chongqing Changan Auto Porter's Five Forces Analysis

This preview shows the exact Chongqing Changan Auto Porter Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Chongqing Changan Auto faces intense rivalry from domestic and global OEMs, rising buyer expectations on EVs, and supplier pressures amid localized supply chains; regulatory shifts and tech change raise entry barriers but also open disruptor opportunities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Chongqing Changan Auto’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of EV battery supply

The bargaining power of suppliers is high because a few firms—led by CATL (Contemporary Amperex Technology Co. Limited), which held about 35% global EV battery capacity in 2024—dominate supply, giving them pricing leverage over Changan.

Batteries are Changan’s largest new-energy vehicle cost component, roughly 30–40% of EV BOM (bill of materials), so supplier price moves materially affect margins.

By late 2025 Changan has diversified contracts with BYD and Gotion, but technical specs and scale needs for high-energy-density cells keep the pool of viable partners small, constraining bargaining power.

Strategic dependence on semiconductor and AI chip providers

Changan’s shift to intelligent and autonomous driving raises strategic dependence on high-end semiconductor firms such as Nvidia and Qualcomm; in 2025 these vendors account for roughly 60–70% of AI compute modules used in China’s mid-to-high EV segment.

Specialized chips power smart cockpits and ADAS (advanced driver-assistance systems), and global supply tightness kept fab utilization above 90% in 2024, driving chip premiums of 15–25% versus commodity ICs.

This scarcity plus integration complexity gives suppliers leverage to affect Changan’s production timing and BOM (bill of materials) costs, where AI module spend can be 8–12% of vehicle unit cost in flagship models.

Partnerships with technology giants like Huawei

Changan’s deep collaboration with Huawei via Avatr creates a supplier dynamic where Huawei supplies core software, cloud services, and chips for intelligent driving, making provider switching costly; Avatr sales reached about 38,000 units in 2024, tying tech identity to Huawei’s stack. This elevates Huawei’s bargaining power above a typical parts maker, since losing Huawei would erode features and brand positioning and require large R&D and integration spend to replace.

Raw material price volatility impact

Suppliers of lithium, cobalt, and nickel keep price volatility high; lithium carbonate rose ~60% in 2021–22 and metal prices still swing 20–40% year-to-year, pressuring Changan’s EV cost base.

Changan uses multi-year contracts and spot buys, but upstream supply tied to China, Congo, and Australia markets means sudden spikes can erode margins; flexible procurement and hedging are essential.

- 2024 lithium avg price ≈ $60,000/ton

- Nickel spot up 25% YoY (2024)

- Long-term contracts cover ~30–50% of needs

Lower power of traditional mechanical component suppliers

Lower supplier power for traditional mechanical parts: unlike semiconductors, suppliers of engines, chassis parts, and interior trims face low bargaining power because these are standardized; over 300 domestic and 120 international vendors can meet Changan's specs as of 2025, enabling competitive bids and unit-cost reductions of ~3–5% annually on non-electronic components.

Supplier Dominance: CATL & AI Chips Drive EV/AI Cost Risk amid Lithium Volatility

Suppliers hold high power: CATL ~35% global EV battery capacity (2024), batteries = 30–40% EV BOM, chip suppliers (Nvidia/Qualcomm) supply 60–70% AI compute (2025), AI modules = 8–12% unit cost, commodity metal volatility (lithium ≈ $60,000/t in 2024) raises margin risk; traditional mechanical parts have low supplier power (300+ domestic vendors, 120+ international, 3–5% annual cost decline).

| Item | Metric |

|---|---|

| CATL share | ~35% (2024) |

| Battery share of BOM | 30–40% |

| AI chip vendors | 60–70% (2025) |

| Lithium price | ~$60,000/t (2024) |

What is included in the product

Tailored Five Forces analysis for Chongqing Changan Auto uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitution risks, highlighting disruptive threats, pricing leverage, and strategic levers to protect market share.

A concise Chongqing Changan Auto Porter’s Five Forces one-sheet—quickly highlights supplier power, buyer leverage, rivalry intensity, entry threats, and substitutes to speed strategic choices and investor briefings.

Customers Bargaining Power

High price sensitivity in a crowded market

By end-2025, intense price competition in China gives buyers strong leverage; new-car price cuts averaged 6–8% across urban markets in 2024–25, pushing customers to compare Changan directly with BYD, Geely, and Tesla on price and features.

Changan faces high price sensitivity: online price-shoppers exceed 70% in tier-1 cities, so the firm often uses discounts or adds features—Changan reported a 4.2% average transaction discount in H1 2025—to defend share.

Low switching costs for vehicle buyers

The EV shift has cut switching barriers: by end-2024 China had 14.3 million NEVs and 680,000 public chargers, making charging largely interoperable, so buyers face few technical hurdles moving from Changan to rivals.

Standardized charging standards (GB/T and increasingly CCS2) and converging in-car UIs reduce lock-in, so price, range, and software updates drive brand choice.

Abundance of choice across all segments

In 2025 consumers can choose from over 6,000 passenger vehicle SKUs in China across sedans, SUVs and MPVs, so Changan faces intense choice-driven bargaining power.

Changan competes with domestic rivals like Geely and BYD, global groups such as Volkswagen and Toyota, plus tech-led entrants (e.g., Xpeng), raising price and feature sensitivity.

Market saturation means a 1% slip in perceived value or a 0.5‑point drop in JD Power satisfaction can shift buyers to alternatives, so innovation and service are decisive.

Increased transparency through digital platforms

The rise of automotive social media and review platforms has pushed information transparency: 2024 surveys show 72% of Chinese EV buyers consult online reviews and real-world range reports before purchase, up from 58% in 2021.

Easy access to software-bug logs, ownership forums, and dealership service ratings limits Changan’s control of the narrative and increases bargaining power of informed buyers.

- 72% of buyers use online reviews (2024)

- Real-world range reports lower trust variance by 35%

- Dealership service ratings drive 15% purchase deferral

Rising demand for personalized and smart features

Customers now expect deep customization and smart features as standard, driving Changan to refresh software and hardware faster; Chinese new-energy vehicle buyers rated in 2024 that 62% view in-car software updates as a key purchase factor.

This customer power forces higher R&D spend—Changan increased R&D to 6.2% of revenue in 2024—to keep pace with seasonal 'must-have' features and shorten product cycles.

- 62% of NEV buyers prioritize software updates

- Changan R&D = 6.2% of revenue (2024)

- Shorter product cycles raise development costs

Buyers Win: 6–8% Price Cuts, 14.3M NEVs & Changan’s 6.2% R&D Push

Buyers hold strong leverage: 6–8% average new-car price cuts (2024–25), 70%+ online price-shoppers in tier‑1, 72% consult reviews (2024), 14.3M NEVs and 680k public chargers (end‑2024) lower switching costs; Changan R&D hit 6.2% of revenue (2024) to compete on software, range and price.

| Metric | Value |

|---|---|

| Price cuts | 6–8% |

| Online shoppers | 70%+ |

| Review users | 72% |

| NEVs | 14.3M |

| Chargers | 680k |

| Changan R&D | 6.2% |

Full Version Awaits

Chongqing Changan Auto Porter's Five Forces Analysis

This preview shows the exact Chongqing Changan Auto Porter Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.