Chemtrade Boston Consulting Group Matrix

Actionable Strategy Starts Here

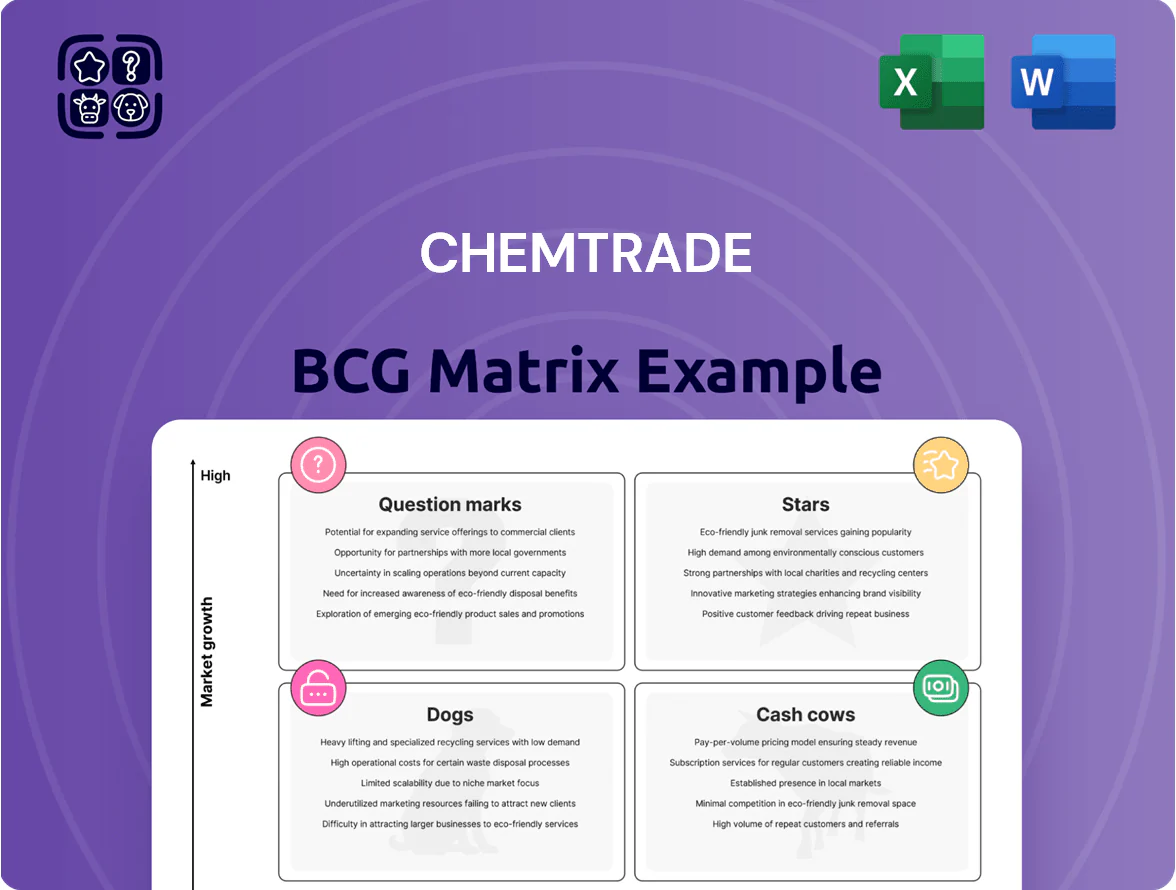

Chemtrade’s BCG Matrix preview highlights where core product lines sit across growth and market share—but there’s more beneath the surface. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed strategic recommendations, and clear guidance on which segments to invest in, harvest, divest, or develop. Get instant access to an editable Word report and high-level Excel summary so you can present and act confidently—buy now for the complete strategic playbook.

Stars

Ultra-Pure Sulfuric Acid for Semiconductors

As of late 2025, Chemtrade leads North American ultra-pure sulfuric acid for semiconductors, holding roughly 35% regional market share and supplying fabs tied to US CHIPS Act projects; semiconductor-grade demand rose ~18% CAGR 2022–2025. This Stars unit needs heavy capex (~$120–150M planned 2026) to meet <10 ppb impurity specs, but fuels revenue growth—expected to add $60–80M EBITDA by 2027—so continued investment is essential to turn it into a cash generator.

Green Hydrogen Byproduct Commercialization

The electrochemicals segment produces hydrogen as a byproduct and, by end-2025, green hydrogen spot prices fell ~18% vs 2022 while demand from heavy industry rose ~22% year-over-year, boosting market traction.

Chemtrade holds a strong regional position in North America and Europe, supplying ~45 kt H2/year from byproduct streams and securing long-term offtakes with steel and fertilizer clients.

As a star in the BCG matrix, the unit uses existing electrolyzer and pipeline-adjacent assets to capture projected sector CAGR ~28% to 2030, driving rapid revenue growth.

To keep leadership, Chemtrade needs substantial capex—estimated US$120–160m through 2027—for capture upgrades, compression, and distribution logistics to meet rising industrial clean-energy demand.

Advanced Water Treatment Specialty Chemicals

Regulatory tightening on PFAS and emerging contaminants since 2023 pushed global water-treatment spend up ~6–8% CAGR to 2025; Chemtrade leads in specialty coagulants compliant with new standards, capturing an estimated 12–15% share of North American industrial water-chemicals in 2025.

High infrastructure demand—US Bipartisan Infrastructure Law allocated $50B+ for water upgrades by 2025—drives durable market growth, but continual R&D is needed as competitors scale pilot PFAS removal chemistries.

Given margin resilience and growth, Chemtrade ranks this segment as a Stars quadrant priority and plans to direct ~30–40% of 2025–2027 capital expenditure toward product development and capacity expansion to secure long-term dominance.

Chlor-Alkali Expansion in Strategic Corridors

By 2025, Chemtrade grew chlor-alkali share in North American hubs (Great Lakes, Gulf Coast, Arizona) to roughly 12–15%, supplying caustic soda and chlorine for lithium hydroxide plants and advanced manufacturers; revenue from this line hit an estimated USD 220–260M in 2025.

Competition is intense, but Chemtrade’s localized terminals and rail/river logistics cut lead times by ~30% vs coast-only rivals, justifying heavy investment to hold position as downstream lithium capacity rises through 2026–2028.

Maintaining share matters: projected demand for caustic in battery-grade lithium processing is expected to grow ~25% CAGR 2025–2028, so retention preserves margin and downstream contracts.

- 2025 revenue est: USD 220–260M

Next-Generation Sulfur Derivatives

Chemtrade’s next-generation sulfur derivatives target high-tech manufacturing and sustainable agriculture, with segment revenue growing ~28% year-over-year to an estimated $170M in 2025 as customers seek lower-emission inputs.

As a first-to-market provider in several niches, Chemtrade holds dominant shares (40–60%) in specialty sulfur chemistries used in semiconductor etching and controlled-release fertilizers.

High growth classifies these products as Stars in the BCG matrix, but continued marketing and R&D—estimated at $15–20M annually—are needed to convert them into stable cash cows.

- 2025 rev ~$170M; YoY +28%

- Market share 40–60% in key niches

- R&D spend $15–20M/yr to scale

- Targets: semiconductors, sustainable ag

Chemtrade Stars: $650–780M 2025 Revenue, $60–80M EBITDA Lift by 2027

Chemtrade’s Stars (ultra‑pure sulfuric, specialty sulfur, byproduct H2, chlor‑alkali) drive high growth: 2025 revenue ~USD 650–780M aggregate, segment CAGR 2022–25 ~18–28%, capex guidance 2026–27 USD 120–160M, R&D USD 15–20M/yr, EBITDA uplift USD 60–80M by 2027; market shares: semiconductor sulfur ~35%, specialty sulfur 40–60%, byproduct H2 supply ~45 kt/yr.

| Metric | 2025 | Notes |

|---|---|---|

| Revenue (Stars) | USD 650–780M | Includes sulfur, H2, chlor‑alkali |

| Capex 2026–27 | USD 120–160M | Upgrades, compression, logistics |

| R&D | USD 15–20M/yr | PFAS, semicon specs |

| EBITDA uplift | USD 60–80M by 2027 | From semiconductor sulfur growth |

| Key market shares | Sulfur 35%; specialty 40–60% | North America/Europe |

| Byproduct H2 | ~45 kt/yr | Long‑term offtakes secured |

What is included in the product

Comprehensive BCG Matrix review of Chemtrade’s portfolio with quadrant strategies, competitive risks, and investment recommendations.

One-page Chemtrade BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Regenerated Sulfuric Acid Services

Chemtrade holds roughly 60–70% share of North American sulfuric acid regeneration for oil refineries, a mature, low-growth segment that generated about CAD 120–150 million EBITDA annually in 2024 due to high entry barriers and stable feedstock contracts.

The firm’s network of ~12 regeneration plants drives unit costs down, needs minimal marketing spend, and delivers predictable free cash flow used to fund expansion into higher-margin semiconductor-grade chemicals.

Aluminum Sulfate for Municipal Water

Aluminum sulfate (alum) remains a staple in municipal water treatment; Chemtrade is a market leader with ~25% share in North America (2024 sales ≈ CAD 180m for the segment), anchoring predictable, recession-resistant revenue.

The municipal market is mature with low capital needs and ~1–2% annual volume growth; stable margins let Chemtrade focus on ops efficiency to lift EBITDA margins toward 18–22%.

This cash cow funds dividends and services debt—2024 free cash flow covered dividends ~1.6x and reduced net debt by ~CAD 60m—so Chemtrade can reinvest selectively while preserving payouts.

Merchant Sulfuric Acid Distribution

Merchant sulfuric acid distribution is a cash cow for Chemtrade, with its logistics network supporting ~25% North American market share in 2024 and gross margins near 28% on the segment, per company filings.

Market demand is mature; Chemtrade’s scale drives a 10–15% unit cost advantage versus regional peers, keeping competitors at bay and lowering pricing pressure.

Minimal promo spend is needed, so free cash flow from this unit funded ~40% of corporate capex and dividends in FY2024, making it a steady liquidity source.

Sodium Chlorite for Disinfection

Sodium chlorite for disinfection sits in Chemtrade’s Cash Cows: stable, mature industrial and municipal markets where Chemtrade holds a significant share and faces low growth but steady demand. High margins from specialty disinfection (used in pulp bleaching, potable water and IOS applications) deliver strong cash returns—Chemtrade reported chemical segment EBITDA margin ~18% in 2024. The product benefits from a known process and loyal clients, so focus is on productivity and uptime over expansion; it remains a reliable profit contributor.

- Stable market, low growth

- High specialty margins (~18% EBITDA, 2024)

- Established production, low capex

- Loyal municipal and industrial customers

- Consistent cash generation for Chemtrade

Industrial Terminal and Logistics Services

Industrial Terminal and Logistics Services sit in Chemtrade’s Cash Cow quadrant: mature, low-growth market but high margin. In 2024 the segment ran >85% utilization and generated roughly C$110–130 million EBITDA, producing steady fee income from third-party chemical storage and handling.

Once terminals are built, incremental capex is low, so 2024 free cash flow margin stayed near 25%, funding R&D and bolt-on M&A into higher-growth areas.

- High utilization >85% in 2024

- Estimated 2024 EBITDA C$110–130M

- Free cash flow margin ~25% in 2024

- Low incremental capex after build-out

Chemtrade’s 2024 Cash Cows: Mature, High‑Margin Units Fueling CAD 260–300M FCF

Chemtrade’s Cash Cows (2024): sulfuric acid regen, alum, merchant sulfuric, sodium chlorite, and terminals—mature, low-growth but high-margin units generating ~CAD 420–490M EBITDA and ~CAD 260–300M free cash flow, funding dividends and selective growth.

| Unit | 2024 EBITDA (CADm) | FCF (CADm) | Key metric |

|---|---|---|---|

| Sulfuric regen | 120–150 | 80–95 | 60–70% NA share |

| Alum | ~180 | 100–120 | ~25% NA share |

| Merchant S | ~50 | 30–40 | ~25% NA share |

| Sodium chlorite | ~40 | 25–30 | ~18% EBITDA margin |

| Terminals | 110–130 | 55–60 | >85% utilization |

What You See Is What You Get

Chemtrade BCG Matrix

The file you're previewing on this page is the final Chemtrade BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Chemtrade’s BCG Matrix preview highlights where core product lines sit across growth and market share—but there’s more beneath the surface. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed strategic recommendations, and clear guidance on which segments to invest in, harvest, divest, or develop. Get instant access to an editable Word report and high-level Excel summary so you can present and act confidently—buy now for the complete strategic playbook.

Stars

Ultra-Pure Sulfuric Acid for Semiconductors

As of late 2025, Chemtrade leads North American ultra-pure sulfuric acid for semiconductors, holding roughly 35% regional market share and supplying fabs tied to US CHIPS Act projects; semiconductor-grade demand rose ~18% CAGR 2022–2025. This Stars unit needs heavy capex (~$120–150M planned 2026) to meet <10 ppb impurity specs, but fuels revenue growth—expected to add $60–80M EBITDA by 2027—so continued investment is essential to turn it into a cash generator.

Green Hydrogen Byproduct Commercialization

The electrochemicals segment produces hydrogen as a byproduct and, by end-2025, green hydrogen spot prices fell ~18% vs 2022 while demand from heavy industry rose ~22% year-over-year, boosting market traction.

Chemtrade holds a strong regional position in North America and Europe, supplying ~45 kt H2/year from byproduct streams and securing long-term offtakes with steel and fertilizer clients.

As a star in the BCG matrix, the unit uses existing electrolyzer and pipeline-adjacent assets to capture projected sector CAGR ~28% to 2030, driving rapid revenue growth.

To keep leadership, Chemtrade needs substantial capex—estimated US$120–160m through 2027—for capture upgrades, compression, and distribution logistics to meet rising industrial clean-energy demand.

Advanced Water Treatment Specialty Chemicals

Regulatory tightening on PFAS and emerging contaminants since 2023 pushed global water-treatment spend up ~6–8% CAGR to 2025; Chemtrade leads in specialty coagulants compliant with new standards, capturing an estimated 12–15% share of North American industrial water-chemicals in 2025.

High infrastructure demand—US Bipartisan Infrastructure Law allocated $50B+ for water upgrades by 2025—drives durable market growth, but continual R&D is needed as competitors scale pilot PFAS removal chemistries.

Given margin resilience and growth, Chemtrade ranks this segment as a Stars quadrant priority and plans to direct ~30–40% of 2025–2027 capital expenditure toward product development and capacity expansion to secure long-term dominance.

Chlor-Alkali Expansion in Strategic Corridors

By 2025, Chemtrade grew chlor-alkali share in North American hubs (Great Lakes, Gulf Coast, Arizona) to roughly 12–15%, supplying caustic soda and chlorine for lithium hydroxide plants and advanced manufacturers; revenue from this line hit an estimated USD 220–260M in 2025.

Competition is intense, but Chemtrade’s localized terminals and rail/river logistics cut lead times by ~30% vs coast-only rivals, justifying heavy investment to hold position as downstream lithium capacity rises through 2026–2028.

Maintaining share matters: projected demand for caustic in battery-grade lithium processing is expected to grow ~25% CAGR 2025–2028, so retention preserves margin and downstream contracts.

- 2025 revenue est: USD 220–260M

Next-Generation Sulfur Derivatives

Chemtrade’s next-generation sulfur derivatives target high-tech manufacturing and sustainable agriculture, with segment revenue growing ~28% year-over-year to an estimated $170M in 2025 as customers seek lower-emission inputs.

As a first-to-market provider in several niches, Chemtrade holds dominant shares (40–60%) in specialty sulfur chemistries used in semiconductor etching and controlled-release fertilizers.

High growth classifies these products as Stars in the BCG matrix, but continued marketing and R&D—estimated at $15–20M annually—are needed to convert them into stable cash cows.

- 2025 rev ~$170M; YoY +28%

- Market share 40–60% in key niches

- R&D spend $15–20M/yr to scale

- Targets: semiconductors, sustainable ag

Chemtrade Stars: $650–780M 2025 Revenue, $60–80M EBITDA Lift by 2027

Chemtrade’s Stars (ultra‑pure sulfuric, specialty sulfur, byproduct H2, chlor‑alkali) drive high growth: 2025 revenue ~USD 650–780M aggregate, segment CAGR 2022–25 ~18–28%, capex guidance 2026–27 USD 120–160M, R&D USD 15–20M/yr, EBITDA uplift USD 60–80M by 2027; market shares: semiconductor sulfur ~35%, specialty sulfur 40–60%, byproduct H2 supply ~45 kt/yr.

| Metric | 2025 | Notes |

|---|---|---|

| Revenue (Stars) | USD 650–780M | Includes sulfur, H2, chlor‑alkali |

| Capex 2026–27 | USD 120–160M | Upgrades, compression, logistics |

| R&D | USD 15–20M/yr | PFAS, semicon specs |

| EBITDA uplift | USD 60–80M by 2027 | From semiconductor sulfur growth |

| Key market shares | Sulfur 35%; specialty 40–60% | North America/Europe |

| Byproduct H2 | ~45 kt/yr | Long‑term offtakes secured |

What is included in the product

Comprehensive BCG Matrix review of Chemtrade’s portfolio with quadrant strategies, competitive risks, and investment recommendations.

One-page Chemtrade BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Regenerated Sulfuric Acid Services

Chemtrade holds roughly 60–70% share of North American sulfuric acid regeneration for oil refineries, a mature, low-growth segment that generated about CAD 120–150 million EBITDA annually in 2024 due to high entry barriers and stable feedstock contracts.

The firm’s network of ~12 regeneration plants drives unit costs down, needs minimal marketing spend, and delivers predictable free cash flow used to fund expansion into higher-margin semiconductor-grade chemicals.

Aluminum Sulfate for Municipal Water

Aluminum sulfate (alum) remains a staple in municipal water treatment; Chemtrade is a market leader with ~25% share in North America (2024 sales ≈ CAD 180m for the segment), anchoring predictable, recession-resistant revenue.

The municipal market is mature with low capital needs and ~1–2% annual volume growth; stable margins let Chemtrade focus on ops efficiency to lift EBITDA margins toward 18–22%.

This cash cow funds dividends and services debt—2024 free cash flow covered dividends ~1.6x and reduced net debt by ~CAD 60m—so Chemtrade can reinvest selectively while preserving payouts.

Merchant Sulfuric Acid Distribution

Merchant sulfuric acid distribution is a cash cow for Chemtrade, with its logistics network supporting ~25% North American market share in 2024 and gross margins near 28% on the segment, per company filings.

Market demand is mature; Chemtrade’s scale drives a 10–15% unit cost advantage versus regional peers, keeping competitors at bay and lowering pricing pressure.

Minimal promo spend is needed, so free cash flow from this unit funded ~40% of corporate capex and dividends in FY2024, making it a steady liquidity source.

Sodium Chlorite for Disinfection

Sodium chlorite for disinfection sits in Chemtrade’s Cash Cows: stable, mature industrial and municipal markets where Chemtrade holds a significant share and faces low growth but steady demand. High margins from specialty disinfection (used in pulp bleaching, potable water and IOS applications) deliver strong cash returns—Chemtrade reported chemical segment EBITDA margin ~18% in 2024. The product benefits from a known process and loyal clients, so focus is on productivity and uptime over expansion; it remains a reliable profit contributor.

- Stable market, low growth

- High specialty margins (~18% EBITDA, 2024)

- Established production, low capex

- Loyal municipal and industrial customers

- Consistent cash generation for Chemtrade

Industrial Terminal and Logistics Services

Industrial Terminal and Logistics Services sit in Chemtrade’s Cash Cow quadrant: mature, low-growth market but high margin. In 2024 the segment ran >85% utilization and generated roughly C$110–130 million EBITDA, producing steady fee income from third-party chemical storage and handling.

Once terminals are built, incremental capex is low, so 2024 free cash flow margin stayed near 25%, funding R&D and bolt-on M&A into higher-growth areas.

- High utilization >85% in 2024

- Estimated 2024 EBITDA C$110–130M

- Free cash flow margin ~25% in 2024

- Low incremental capex after build-out

Chemtrade’s 2024 Cash Cows: Mature, High‑Margin Units Fueling CAD 260–300M FCF

Chemtrade’s Cash Cows (2024): sulfuric acid regen, alum, merchant sulfuric, sodium chlorite, and terminals—mature, low-growth but high-margin units generating ~CAD 420–490M EBITDA and ~CAD 260–300M free cash flow, funding dividends and selective growth.

| Unit | 2024 EBITDA (CADm) | FCF (CADm) | Key metric |

|---|---|---|---|

| Sulfuric regen | 120–150 | 80–95 | 60–70% NA share |

| Alum | ~180 | 100–120 | ~25% NA share |

| Merchant S | ~50 | 30–40 | ~25% NA share |

| Sodium chlorite | ~40 | 25–30 | ~18% EBITDA margin |

| Terminals | 110–130 | 55–60 | >85% utilization |

What You See Is What You Get

Chemtrade BCG Matrix

The file you're previewing on this page is the final Chemtrade BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.