Chewy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

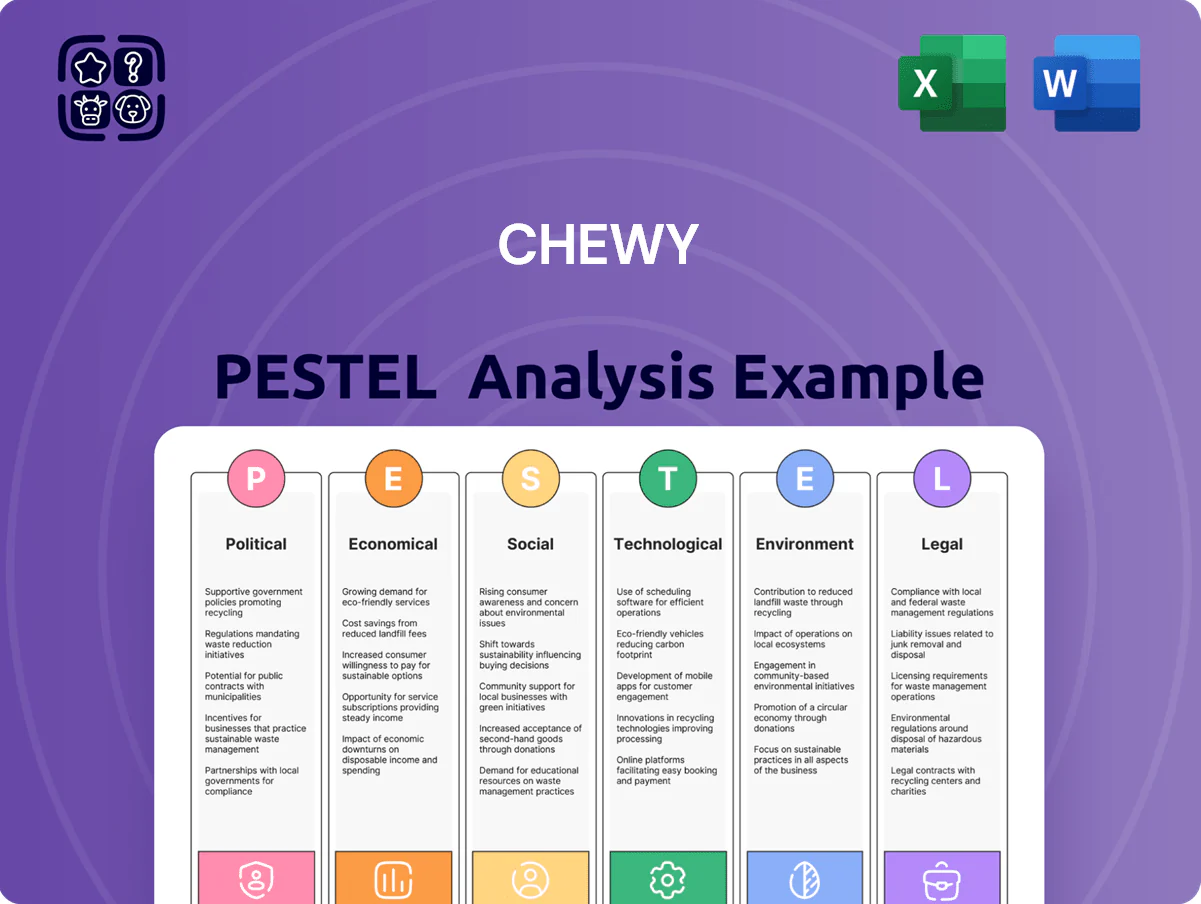

Gain a strategic edge with our PESTLE Analysis of Chewy—concise, current, and tailored to highlight political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists. Purchase the full report to access actionable insights, data-driven risk forecasts, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

International Trade and Tariff Policies

As of late 2025, US trade frictions with China and Southeast Asian manufacturers have contributed to a ~6–8% rise in imported pet hard goods costs year-over-year, pressuring Chewy’s gross margin (FY2024 gross margin 29.2%).

Tariff changes on ingredients like poultry meal or packaging inputs could raise COGS materially; a 5% tariff uptick on key imports would add millions to annual COGS given Chewy’s $10.4B TTM revenue (2024).

Chewy mitigates risk by diversifying suppliers across Vietnam, Mexico, and domestic partners, expanding nearshore sourcing to reduce tariff and disruption exposure.

Veterinary Pharmacy Regulations

The political landscape for online pharmacy regulation is critical for Chewy's healthcare segment, as federal and 50 state-level laws affect prescription verification and dispensing practices that impact ~9% of Chewy's 2025 revenue from healthcare services. Recent 2024 state actions tightened teleprescribing rules in 12 states, creating operational hurdles but also market-entry opportunities where compliance is clearer. Chewy monitors legislation and adjusts its Connect with a Vet and pharmacy operations, while engaging in advocacy for streamlined digital pet-health access to protect growth.

Logistics and Postal Service Policy

Government decisions on USPS funding and rate changes directly affect Chewy's shipping costs; USPS handled about 30% of last-mile parcels in 2024 while marketplace carriers raised rates ~4–6% that year, pressuring Chewy's logistics spend.

Because Chewy depends on reliable home delivery for ~70% of orders, proposed delivery-standard rollbacks or fee hikes could reduce margins and increase shipping overhead.

Active lobbying and carrier partnerships are critical; in 2025 Chewy increased carrier contracts and advocacy spending to protect favorable rate structures and priority for e-commerce shipments.

Labor and Minimum Wage Legislation

Political pressure to raise federal or state minimum wages directly impacts Chewy’s large fulfillment and customer-service workforce; 2024 US proposals sought $15–$20/hr increases, while Chewy reported ~35,000 hourly employees in FY2024, raising potential labor costs materially.

Changes in worker classification and benefit mandates (e.g., gig-worker laws, expanded paid leave) can increase expenses and drive capital spending on automation—Chewy’s capital expenditures rose to $679M in 2024, signaling prior automation investment.

Chewy must comply politically while preserving competitive pricing for a price-sensitive customer base—net sales grew 12% to $10.5B in 2024, so margin pressure from higher labor costs could force price or efficiency shifts.

- ~35,000 hourly workers (FY2024)

- CapEx $679M (2024)

- Net sales $10.5B, +12% (2024)

- Minimum wage proposals $15–$20/hr (2024 political debates)

E-commerce Antitrust Scrutiny

As a dominant pet e-commerce player with 2025 net sales of $11.5B, Chewy faces rising antitrust scrutiny over platform dominance and third-party data use as regulators probe pricing influence by large online retailers.

Maintaining transparent data-sharing and pricing policies is vital to avoid fines or restrictive rules; U.S. and EU investigations into marketplaces increased 28% in 2024–25.

- 2025 net sales $11.5B

- Regulatory probes up 28% (2024–25)

- Risk: fines, behavioral remedies, data-use restrictions

Political headwinds—tariffs, wages, USPS risks squeeze Chewy’s margins and ops

Political risks—trade tariff volatility, USPS/carrier rate changes, state telepharmacy rules, wage mandates, and antitrust scrutiny—threaten Chewy’s margins and operations; key figures: 2025 net sales $11.5B, FY2024 gross margin 29.2%, TTM revenue ~$10.4B, ~35,000 hourly workers, CapEx $679M (2024), USPS ~30% last-mile share (2024).

| Metric | Value |

|---|---|

| Net sales (2025) | $11.5B |

| Gross margin (FY2024) | 29.2% |

| TTM revenue (2024) | $10.4B |

| Hourly workers (FY2024) | ~35,000 |

| CapEx (2024) | $679M |

| USPS last-mile share (2024) | ~30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Chewy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Concise, visually segmented Chewy PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and support quick strategic alignment.

Economic factors

Consumer Discretionary Spending Trends

By end-2025, disposable income trends drive non-essential pet spend; U.S. personal savings rate fell to ~3.1% in 2024 while real median household income rose 2.4% year-over-year, affecting purchases of toys and premium treats.

Pet food remained resilient in downturns—U.S. pet food sales grew to $58.3 billion in 2024—while luxury pet items show greater volatility tied to consumer confidence indexes.

Chewy’s tiered offerings, from value private-label to premium brands, enabled it to capture demand across segments, supporting 2024 net sales of $9.8 billion and gross margin management during softer consumer cycles.

Inflationary Pressures on Logistics

Persistent inflation in fuel and labor—U.S. diesel rose ~15% in 2024 and average hourly retail wages up ~4.5% YoY—squeezes margins for high-volume e-commerce like Chewy. Chewy offsets by optimizing its logistics footprint and increasing route density, reducing per-delivery costs; fulfillment productivity improved ~6% in 2024. Passing costs to consumers while retaining share against brick-and-mortar remains a crucial pricing trade-off.

Growth of the Pet Healthcare Economy

The shift to proactive pet wellness—specialized diets, supplements and preventive meds—has expanded the US pet healthcare market to about $36.9B in 2024, up ~6% YoY; Chewy is scaling high-margin healthcare services and insurance tie-ups to capture this growth.

Chewy’s Pet Health segment revenue rose to $1.1B in FY2024, reflecting higher ARPU from subscriptions and prescriptions versus retail SKUs.

By emphasizing services and insurance, Chewy targets a larger, steadier slice of the average pet wallet—US households spent ~$1,600 per pet in 2024—boosting recurring revenue stability.

Interest Rate Impact on Capital Expenditure

The end-2025 Fed funds rate near 5.25% raised Chewy’s blended cost of debt, making financing for automated fulfillment centers and tech upgrades more expensive and potentially delaying capital-intensive projects.

Higher rates increase interest expense, pressuring free cash flow and slowing M&A or rapid rollout of proprietary-brand manufacturing.

Stabilization of rates around 5%–5.5% would enable more confident multi-year investments in infrastructure and private-label expansion.

- End-2025 Fed funds ~5.25%

- Higher cost of debt → tighter capex

- Stabilized rates → resume long-term investments

Supply Chain Resilience Costs

Economic volatility has pushed Chewy to increase spending on inventory management and redundant supply chains, contributing to higher working capital; Chewy held inventory of $1.51 billion and $1.62 billion in FY2023 and FY2024 respectively, tying up cash that could fund growth initiatives.

These investments reduce stockout risk and protect revenue during disruptions but compress margins short-term; Autoship subscribers—over 5 million in 2024—offer predictable demand that helps optimize inventory turns and lower fulfillment costs.

- Inventory FY2024: $1.62B

- Inventory FY2023: $1.51B

- Autoship subs: >5M (2024)

- Higher working capital, lower short-term free cash flow

Chewy scales in $95B pet market but rising costs and inventory pressure margins

Economic headwinds in 2024–25—real median household income +2.4% (2024), personal savings ~3.1% (2024), Fed funds ~5.25% (end‑2025)—shift spend toward essentials; pet food sales $58.3B (2024) and pet healthcare $36.9B (2024) support Chewy’s $9.8B net sales and $1.1B Pet Health, but higher fuel/labor and inventory ($1.62B FY2024) squeeze margins.

| Metric | 2024/2025 |

|---|---|

| Pet food sales | $58.3B (2024) |

| Pet healthcare | $36.9B (2024) |

| Chewy net sales | $9.8B (2024) |

| Pet Health revenue | $1.1B (FY2024) |

| Inventory | $1.62B (FY2024) |

| Autoship subs | >5M (2024) |

| Fed funds | ~5.25% (end‑2025) |

Preview Before You Purchase

Chewy PESTLE Analysis

The preview shown here is the exact Chewy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our PESTLE Analysis of Chewy—concise, current, and tailored to highlight political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists. Purchase the full report to access actionable insights, data-driven risk forecasts, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

International Trade and Tariff Policies

As of late 2025, US trade frictions with China and Southeast Asian manufacturers have contributed to a ~6–8% rise in imported pet hard goods costs year-over-year, pressuring Chewy’s gross margin (FY2024 gross margin 29.2%).

Tariff changes on ingredients like poultry meal or packaging inputs could raise COGS materially; a 5% tariff uptick on key imports would add millions to annual COGS given Chewy’s $10.4B TTM revenue (2024).

Chewy mitigates risk by diversifying suppliers across Vietnam, Mexico, and domestic partners, expanding nearshore sourcing to reduce tariff and disruption exposure.

Veterinary Pharmacy Regulations

The political landscape for online pharmacy regulation is critical for Chewy's healthcare segment, as federal and 50 state-level laws affect prescription verification and dispensing practices that impact ~9% of Chewy's 2025 revenue from healthcare services. Recent 2024 state actions tightened teleprescribing rules in 12 states, creating operational hurdles but also market-entry opportunities where compliance is clearer. Chewy monitors legislation and adjusts its Connect with a Vet and pharmacy operations, while engaging in advocacy for streamlined digital pet-health access to protect growth.

Logistics and Postal Service Policy

Government decisions on USPS funding and rate changes directly affect Chewy's shipping costs; USPS handled about 30% of last-mile parcels in 2024 while marketplace carriers raised rates ~4–6% that year, pressuring Chewy's logistics spend.

Because Chewy depends on reliable home delivery for ~70% of orders, proposed delivery-standard rollbacks or fee hikes could reduce margins and increase shipping overhead.

Active lobbying and carrier partnerships are critical; in 2025 Chewy increased carrier contracts and advocacy spending to protect favorable rate structures and priority for e-commerce shipments.

Labor and Minimum Wage Legislation

Political pressure to raise federal or state minimum wages directly impacts Chewy’s large fulfillment and customer-service workforce; 2024 US proposals sought $15–$20/hr increases, while Chewy reported ~35,000 hourly employees in FY2024, raising potential labor costs materially.

Changes in worker classification and benefit mandates (e.g., gig-worker laws, expanded paid leave) can increase expenses and drive capital spending on automation—Chewy’s capital expenditures rose to $679M in 2024, signaling prior automation investment.

Chewy must comply politically while preserving competitive pricing for a price-sensitive customer base—net sales grew 12% to $10.5B in 2024, so margin pressure from higher labor costs could force price or efficiency shifts.

- ~35,000 hourly workers (FY2024)

- CapEx $679M (2024)

- Net sales $10.5B, +12% (2024)

- Minimum wage proposals $15–$20/hr (2024 political debates)

E-commerce Antitrust Scrutiny

As a dominant pet e-commerce player with 2025 net sales of $11.5B, Chewy faces rising antitrust scrutiny over platform dominance and third-party data use as regulators probe pricing influence by large online retailers.

Maintaining transparent data-sharing and pricing policies is vital to avoid fines or restrictive rules; U.S. and EU investigations into marketplaces increased 28% in 2024–25.

- 2025 net sales $11.5B

- Regulatory probes up 28% (2024–25)

- Risk: fines, behavioral remedies, data-use restrictions

Political headwinds—tariffs, wages, USPS risks squeeze Chewy’s margins and ops

Political risks—trade tariff volatility, USPS/carrier rate changes, state telepharmacy rules, wage mandates, and antitrust scrutiny—threaten Chewy’s margins and operations; key figures: 2025 net sales $11.5B, FY2024 gross margin 29.2%, TTM revenue ~$10.4B, ~35,000 hourly workers, CapEx $679M (2024), USPS ~30% last-mile share (2024).

| Metric | Value |

|---|---|

| Net sales (2025) | $11.5B |

| Gross margin (FY2024) | 29.2% |

| TTM revenue (2024) | $10.4B |

| Hourly workers (FY2024) | ~35,000 |

| CapEx (2024) | $679M |

| USPS last-mile share (2024) | ~30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Chewy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Concise, visually segmented Chewy PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and support quick strategic alignment.

Economic factors

Consumer Discretionary Spending Trends

By end-2025, disposable income trends drive non-essential pet spend; U.S. personal savings rate fell to ~3.1% in 2024 while real median household income rose 2.4% year-over-year, affecting purchases of toys and premium treats.

Pet food remained resilient in downturns—U.S. pet food sales grew to $58.3 billion in 2024—while luxury pet items show greater volatility tied to consumer confidence indexes.

Chewy’s tiered offerings, from value private-label to premium brands, enabled it to capture demand across segments, supporting 2024 net sales of $9.8 billion and gross margin management during softer consumer cycles.

Inflationary Pressures on Logistics

Persistent inflation in fuel and labor—U.S. diesel rose ~15% in 2024 and average hourly retail wages up ~4.5% YoY—squeezes margins for high-volume e-commerce like Chewy. Chewy offsets by optimizing its logistics footprint and increasing route density, reducing per-delivery costs; fulfillment productivity improved ~6% in 2024. Passing costs to consumers while retaining share against brick-and-mortar remains a crucial pricing trade-off.

Growth of the Pet Healthcare Economy

The shift to proactive pet wellness—specialized diets, supplements and preventive meds—has expanded the US pet healthcare market to about $36.9B in 2024, up ~6% YoY; Chewy is scaling high-margin healthcare services and insurance tie-ups to capture this growth.

Chewy’s Pet Health segment revenue rose to $1.1B in FY2024, reflecting higher ARPU from subscriptions and prescriptions versus retail SKUs.

By emphasizing services and insurance, Chewy targets a larger, steadier slice of the average pet wallet—US households spent ~$1,600 per pet in 2024—boosting recurring revenue stability.

Interest Rate Impact on Capital Expenditure

The end-2025 Fed funds rate near 5.25% raised Chewy’s blended cost of debt, making financing for automated fulfillment centers and tech upgrades more expensive and potentially delaying capital-intensive projects.

Higher rates increase interest expense, pressuring free cash flow and slowing M&A or rapid rollout of proprietary-brand manufacturing.

Stabilization of rates around 5%–5.5% would enable more confident multi-year investments in infrastructure and private-label expansion.

- End-2025 Fed funds ~5.25%

- Higher cost of debt → tighter capex

- Stabilized rates → resume long-term investments

Supply Chain Resilience Costs

Economic volatility has pushed Chewy to increase spending on inventory management and redundant supply chains, contributing to higher working capital; Chewy held inventory of $1.51 billion and $1.62 billion in FY2023 and FY2024 respectively, tying up cash that could fund growth initiatives.

These investments reduce stockout risk and protect revenue during disruptions but compress margins short-term; Autoship subscribers—over 5 million in 2024—offer predictable demand that helps optimize inventory turns and lower fulfillment costs.

- Inventory FY2024: $1.62B

- Inventory FY2023: $1.51B

- Autoship subs: >5M (2024)

- Higher working capital, lower short-term free cash flow

Chewy scales in $95B pet market but rising costs and inventory pressure margins

Economic headwinds in 2024–25—real median household income +2.4% (2024), personal savings ~3.1% (2024), Fed funds ~5.25% (end‑2025)—shift spend toward essentials; pet food sales $58.3B (2024) and pet healthcare $36.9B (2024) support Chewy’s $9.8B net sales and $1.1B Pet Health, but higher fuel/labor and inventory ($1.62B FY2024) squeeze margins.

| Metric | 2024/2025 |

|---|---|

| Pet food sales | $58.3B (2024) |

| Pet healthcare | $36.9B (2024) |

| Chewy net sales | $9.8B (2024) |

| Pet Health revenue | $1.1B (FY2024) |

| Inventory | $1.62B (FY2024) |

| Autoship subs | >5M (2024) |

| Fed funds | ~5.25% (end‑2025) |

Preview Before You Purchase

Chewy PESTLE Analysis

The preview shown here is the exact Chewy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.