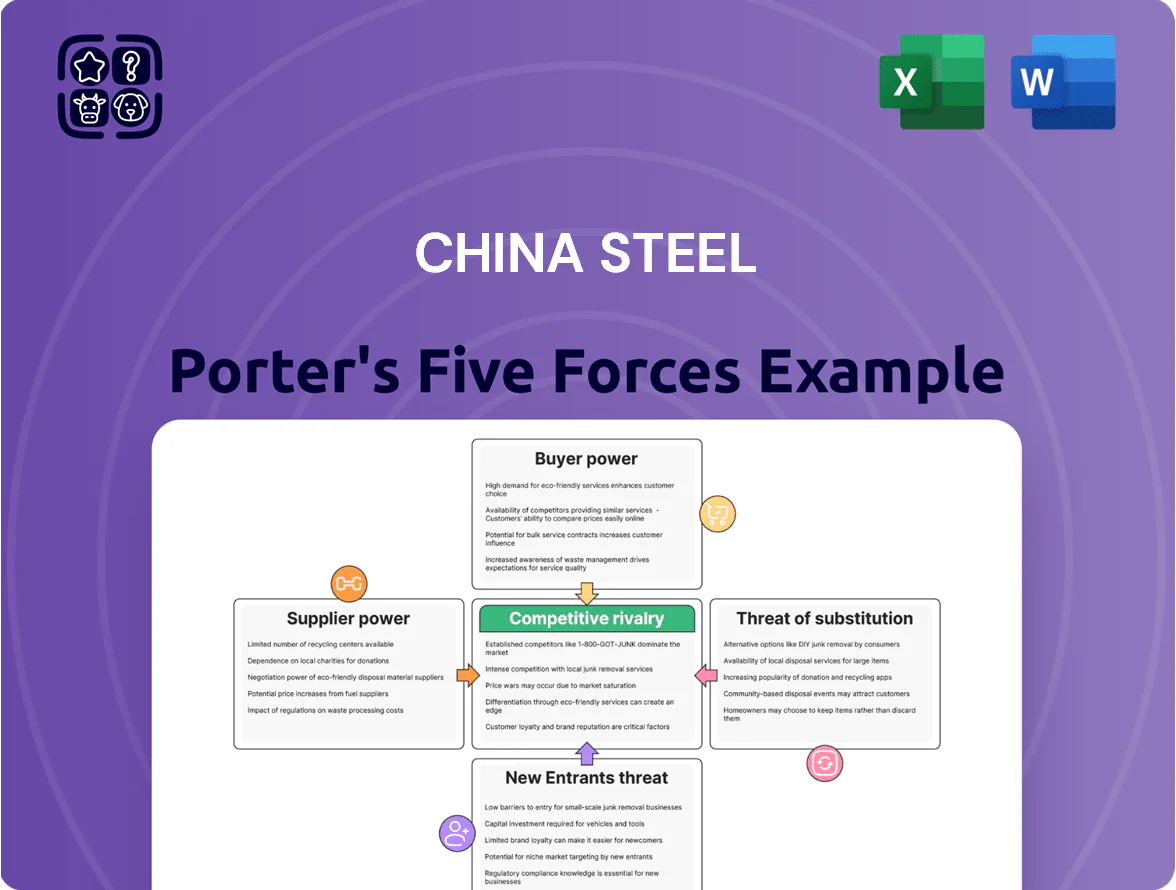

China Steel Porter's Five Forces Analysis

Don't Miss the Bigger Picture

China Steel operates in a high-capacity, commoditized market where buyer price sensitivity and intense rivalry compress margins, while supplier leverage and regulatory factors shape raw-material access and cost structures.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Raw Material Providers

By end-2025 China Steel depends on iron ore and coking coal largely supplied by a handful of miners: BHP, Rio Tinto, Vale and Glencore control roughly 60–70% of seaborne iron ore and the top five coal miners supply ~65% of met coal, giving suppliers strong pricing power.

Volatility in Energy and Electricity Costs

As a massive energy consumer, China Steel faces exposure to global fuel swings and Taiwan electricity tariffs; industrial power costs rose about 12% from 2021–2024 and can add ~3–5% to steel unit costs when LNG and coal prices spike. By 2025, shifting to renewables adds new variables—grid intermittency and PPA (power purchase agreement) pricing—raising CAPEX for onsite solar/wind; energy suppliers keep high bargaining power because few scalable alternatives exist for such large operations.

The Growing Strategic Importance of Steel Scrap

The shift to electric arc furnace (EAF) steel and greener methods has raised global demand for high-grade scrap; EAF share rose to 37% of global capacity by 2024, pushing premium scrap prices up ~22% YoY in 2023–24.

China Steel faces tighter scrap supply: domestic processed scrap availability fell ~9% in 2024, letting recyclers and collectors extract higher premiums and shorter contract terms.

This strengthens supplier bargaining power vs China Steel, raising input-cost volatility and margin pressure—scrap now a strategic bottleneck.

Logistics and Maritime Shipping Constraints

China Steel relies on specialized bulk carriers and shipping lines to move ~50–60 million tons of iron ore and coal annually; in 2025 four major shipping alliances control ~70% of capacity, tightening vessel availability.

Stricter IMO 2023/2024 emission rules and higher scrubber/low-sulfur fuel costs raised freight rates; Baltic Dry Index averaged ~1,400 in 2025, up 22% year-on-year, increasing input shipping costs.

Limited modal alternatives (domestic rail/river can handle <20% of volume) grants maritime providers pricing power, raising volatility and pass-through risk to China Steel margins.

- Annual seaborne tonnage: ~50–60M tons

- Top 4 alliances: ~70% capacity

- Baltic Dry Index 2025 avg: ~1,400 (↑22% YoY)

- Land alternatives capacity: <20% of volumes

Specialized Technology and Equipment Vendors

Modernizing for carbon neutrality forces China Steel to buy proprietary tech from a handful of global engineering firms; top vendors (e.g., Siemens, Danieli, SMS Group) control key low‑carbon steel solutions and captured ~60–70% of global retrofitting contracts in 2023–24.

These vendors wield supplier power because their systems ensure compliance with EU ETS and IMO rules; replacing them risks costs of hundreds of millions USD and operational downtime, so China Steel avoids switching.

Here’s the quick list — concrete points:

- Vendor concentration: ~3–5 firms dominate low‑carbon retrofit market

- Contract share: vendors held 60–70% of retrofits (2023–24)

- Switching cost: often >$200M and months of downtime

- Regulatory dependency: systems needed for EU ETS/IMO compliance

Concentrated suppliers, rising EAF scrap & shipping power reshape steel costs

Suppliers hold strong power: top 4 miners 60–70% iron ore, top 5 coal ~65%; EAF scrap demand up (EAF 37% global cap, scrap +22% 2023–24; domestic scrap −9% 2024); shipping alliances ~70% capacity, BDI avg ~1,400 in 2025 (↑22% YoY); low‑carbon vendors 3–5 firms (60–70% retrofit share, switching cost >$200M).

| Item | 2024–25 |

|---|---|

| Miners’ share | 60–70% |

| Coal suppliers | ~65% |

| EAF share | 37% |

| Scrap price change | +22% |

| Domestic scrap | -9% |

| Shipping alliances | ~70% |

| BDI 2025 avg | ~1,400 |

| Vendor retrofit share | 60–70% |

| Switch cost | >$200M |

What is included in the product

Tailored Porter's Five Forces analysis for China Steel that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its profitability.

Compact Porter’s Five Forces snapshot for China Steel—instantly reveals supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Concentration of Domestic Downstream Industries

China Steel Corporation is the main supplier to Taiwan’s construction, automotive and shipbuilding sectors, where the top 5 firms account for roughly 65–75% of demand; these large buyers purchase millions of tonnes annually, letting them secure volume discounts up to 5–8% and extended payment terms of 60–120 days. Their negotiating power materially pressures China Steel’s domestic pricing and margins, remaining a key risk factor through end-2025.

Availability of Low-Cost International Imports

China Steel's strong domestic share still meets pressure because buyers can switch to low-cost imports from mainland China or Southeast Asia; in 2025 seaborne steel prices averaged about $640/ton, making comparisons easy.

Price transparency—real-time indices and weekly Shanghai and Singapore quotes—lets customers demand parity, so a >3% local premium risks volume loss.

Demand for High-Value and Green Steel Products

Sophisticated buyers in automotive and electronics now demand high-strength and low-carbon steel; global OEMs’ procurement standards rose 20% for carbon footprint reporting by 2024, boosting buyer leverage. These customers need technical certifications (e.g., IATF 16949, ISO 14001) and cradle-to-gate CO2 data, so China Steel faces higher bargaining power. Failure to meet specs risks losing high-margin contracts—automotive-grade steel buyers paid 15–25% premiums in 2024 and can shift to advanced foreign suppliers.

Cyclical Nature of End-User Markets

Customers’ purchasing power for China Steel swings with global GDP and China property cycles; in 2025 Chinese real estate investment fell 9% year-on-year through Q3, letting buyers delay projects and cut orders.

During downturns buyers push for discounts to protect cash, forcing plants to lower prices to keep utilization above ~70%, shifting bargaining power to buyers in lean years.

- 2025 China property INV -9% YTD through Q3

- Industry utilization target ~70% to cover fixed costs

- Buyers can defer orders, press for price cuts

Low Switching Costs for Commodity Grade Steel

For commodity products like hot-rolled coils and basic bars, switching costs are low—buyers in China can shift to the lowest-priced regional supplier within weeks, pressuring margins; China Steel saw flat HRC ASPs in 2024 vs 2023 while domestic spot spreads fell ~8% year-on-year.

- Undifferentiated product → price-driven purchases

- Low switching time: weeks to a month

- 2024 spot spread decline ~8%

- Retention via service, delivery reliability, credit terms

Top‑5 Taiwanese Buyers Drive Discounts, Terms & Low‑carbon Premiums; >3% Local Premium Risks Volume

Large Taiwanese buyers (top 5 = 65–75% demand) secure 5–8% volume discounts and 60–120 day terms, pushing domestic margins; buyers can switch to imports as 2025 seaborne HRC averaged ~$640/ton, so >3% local premium risks volume loss. Automotive/electronics demand for low‑carbon steel (15–25% premiums in 2024) raises specs and buyer leverage; downturns (China property INV -9% YTD through Q3 2025) let buyers defer orders and force price cuts.

| Metric | Value |

|---|---|

| Top‑5 buyer share | 65–75% |

| Volume discounts | 5–8% |

| Payment terms | 60–120 days |

| Seaborne HRC 2025 avg | $640/ton |

| Auto‑grade premium 2024 | 15–25% |

| China property INV 2025 YTD | -9% |

| Spot spread change 2024 vs 2023 | -8% |

Full Version Awaits

China Steel Porter's Five Forces Analysis

This preview shows the exact China Steel Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

China Steel operates in a high-capacity, commoditized market where buyer price sensitivity and intense rivalry compress margins, while supplier leverage and regulatory factors shape raw-material access and cost structures.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Steel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Raw Material Providers

By end-2025 China Steel depends on iron ore and coking coal largely supplied by a handful of miners: BHP, Rio Tinto, Vale and Glencore control roughly 60–70% of seaborne iron ore and the top five coal miners supply ~65% of met coal, giving suppliers strong pricing power.

Volatility in Energy and Electricity Costs

As a massive energy consumer, China Steel faces exposure to global fuel swings and Taiwan electricity tariffs; industrial power costs rose about 12% from 2021–2024 and can add ~3–5% to steel unit costs when LNG and coal prices spike. By 2025, shifting to renewables adds new variables—grid intermittency and PPA (power purchase agreement) pricing—raising CAPEX for onsite solar/wind; energy suppliers keep high bargaining power because few scalable alternatives exist for such large operations.

The Growing Strategic Importance of Steel Scrap

The shift to electric arc furnace (EAF) steel and greener methods has raised global demand for high-grade scrap; EAF share rose to 37% of global capacity by 2024, pushing premium scrap prices up ~22% YoY in 2023–24.

China Steel faces tighter scrap supply: domestic processed scrap availability fell ~9% in 2024, letting recyclers and collectors extract higher premiums and shorter contract terms.

This strengthens supplier bargaining power vs China Steel, raising input-cost volatility and margin pressure—scrap now a strategic bottleneck.

Logistics and Maritime Shipping Constraints

China Steel relies on specialized bulk carriers and shipping lines to move ~50–60 million tons of iron ore and coal annually; in 2025 four major shipping alliances control ~70% of capacity, tightening vessel availability.

Stricter IMO 2023/2024 emission rules and higher scrubber/low-sulfur fuel costs raised freight rates; Baltic Dry Index averaged ~1,400 in 2025, up 22% year-on-year, increasing input shipping costs.

Limited modal alternatives (domestic rail/river can handle <20% of volume) grants maritime providers pricing power, raising volatility and pass-through risk to China Steel margins.

- Annual seaborne tonnage: ~50–60M tons

- Top 4 alliances: ~70% capacity

- Baltic Dry Index 2025 avg: ~1,400 (↑22% YoY)

- Land alternatives capacity: <20% of volumes

Specialized Technology and Equipment Vendors

Modernizing for carbon neutrality forces China Steel to buy proprietary tech from a handful of global engineering firms; top vendors (e.g., Siemens, Danieli, SMS Group) control key low‑carbon steel solutions and captured ~60–70% of global retrofitting contracts in 2023–24.

These vendors wield supplier power because their systems ensure compliance with EU ETS and IMO rules; replacing them risks costs of hundreds of millions USD and operational downtime, so China Steel avoids switching.

Here’s the quick list — concrete points:

- Vendor concentration: ~3–5 firms dominate low‑carbon retrofit market

- Contract share: vendors held 60–70% of retrofits (2023–24)

- Switching cost: often >$200M and months of downtime

- Regulatory dependency: systems needed for EU ETS/IMO compliance

Concentrated suppliers, rising EAF scrap & shipping power reshape steel costs

Suppliers hold strong power: top 4 miners 60–70% iron ore, top 5 coal ~65%; EAF scrap demand up (EAF 37% global cap, scrap +22% 2023–24; domestic scrap −9% 2024); shipping alliances ~70% capacity, BDI avg ~1,400 in 2025 (↑22% YoY); low‑carbon vendors 3–5 firms (60–70% retrofit share, switching cost >$200M).

| Item | 2024–25 |

|---|---|

| Miners’ share | 60–70% |

| Coal suppliers | ~65% |

| EAF share | 37% |

| Scrap price change | +22% |

| Domestic scrap | -9% |

| Shipping alliances | ~70% |

| BDI 2025 avg | ~1,400 |

| Vendor retrofit share | 60–70% |

| Switch cost | >$200M |

What is included in the product

Tailored Porter's Five Forces analysis for China Steel that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its profitability.

Compact Porter’s Five Forces snapshot for China Steel—instantly reveals supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Concentration of Domestic Downstream Industries

China Steel Corporation is the main supplier to Taiwan’s construction, automotive and shipbuilding sectors, where the top 5 firms account for roughly 65–75% of demand; these large buyers purchase millions of tonnes annually, letting them secure volume discounts up to 5–8% and extended payment terms of 60–120 days. Their negotiating power materially pressures China Steel’s domestic pricing and margins, remaining a key risk factor through end-2025.

Availability of Low-Cost International Imports

China Steel's strong domestic share still meets pressure because buyers can switch to low-cost imports from mainland China or Southeast Asia; in 2025 seaborne steel prices averaged about $640/ton, making comparisons easy.

Price transparency—real-time indices and weekly Shanghai and Singapore quotes—lets customers demand parity, so a >3% local premium risks volume loss.

Demand for High-Value and Green Steel Products

Sophisticated buyers in automotive and electronics now demand high-strength and low-carbon steel; global OEMs’ procurement standards rose 20% for carbon footprint reporting by 2024, boosting buyer leverage. These customers need technical certifications (e.g., IATF 16949, ISO 14001) and cradle-to-gate CO2 data, so China Steel faces higher bargaining power. Failure to meet specs risks losing high-margin contracts—automotive-grade steel buyers paid 15–25% premiums in 2024 and can shift to advanced foreign suppliers.

Cyclical Nature of End-User Markets

Customers’ purchasing power for China Steel swings with global GDP and China property cycles; in 2025 Chinese real estate investment fell 9% year-on-year through Q3, letting buyers delay projects and cut orders.

During downturns buyers push for discounts to protect cash, forcing plants to lower prices to keep utilization above ~70%, shifting bargaining power to buyers in lean years.

- 2025 China property INV -9% YTD through Q3

- Industry utilization target ~70% to cover fixed costs

- Buyers can defer orders, press for price cuts

Low Switching Costs for Commodity Grade Steel

For commodity products like hot-rolled coils and basic bars, switching costs are low—buyers in China can shift to the lowest-priced regional supplier within weeks, pressuring margins; China Steel saw flat HRC ASPs in 2024 vs 2023 while domestic spot spreads fell ~8% year-on-year.

- Undifferentiated product → price-driven purchases

- Low switching time: weeks to a month

- 2024 spot spread decline ~8%

- Retention via service, delivery reliability, credit terms

Top‑5 Taiwanese Buyers Drive Discounts, Terms & Low‑carbon Premiums; >3% Local Premium Risks Volume

Large Taiwanese buyers (top 5 = 65–75% demand) secure 5–8% volume discounts and 60–120 day terms, pushing domestic margins; buyers can switch to imports as 2025 seaborne HRC averaged ~$640/ton, so >3% local premium risks volume loss. Automotive/electronics demand for low‑carbon steel (15–25% premiums in 2024) raises specs and buyer leverage; downturns (China property INV -9% YTD through Q3 2025) let buyers defer orders and force price cuts.

| Metric | Value |

|---|---|

| Top‑5 buyer share | 65–75% |

| Volume discounts | 5–8% |

| Payment terms | 60–120 days |

| Seaborne HRC 2025 avg | $640/ton |

| Auto‑grade premium 2024 | 15–25% |

| China property INV 2025 YTD | -9% |

| Spot spread change 2024 vs 2023 | -8% |

Full Version Awaits

China Steel Porter's Five Forces Analysis

This preview shows the exact China Steel Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.