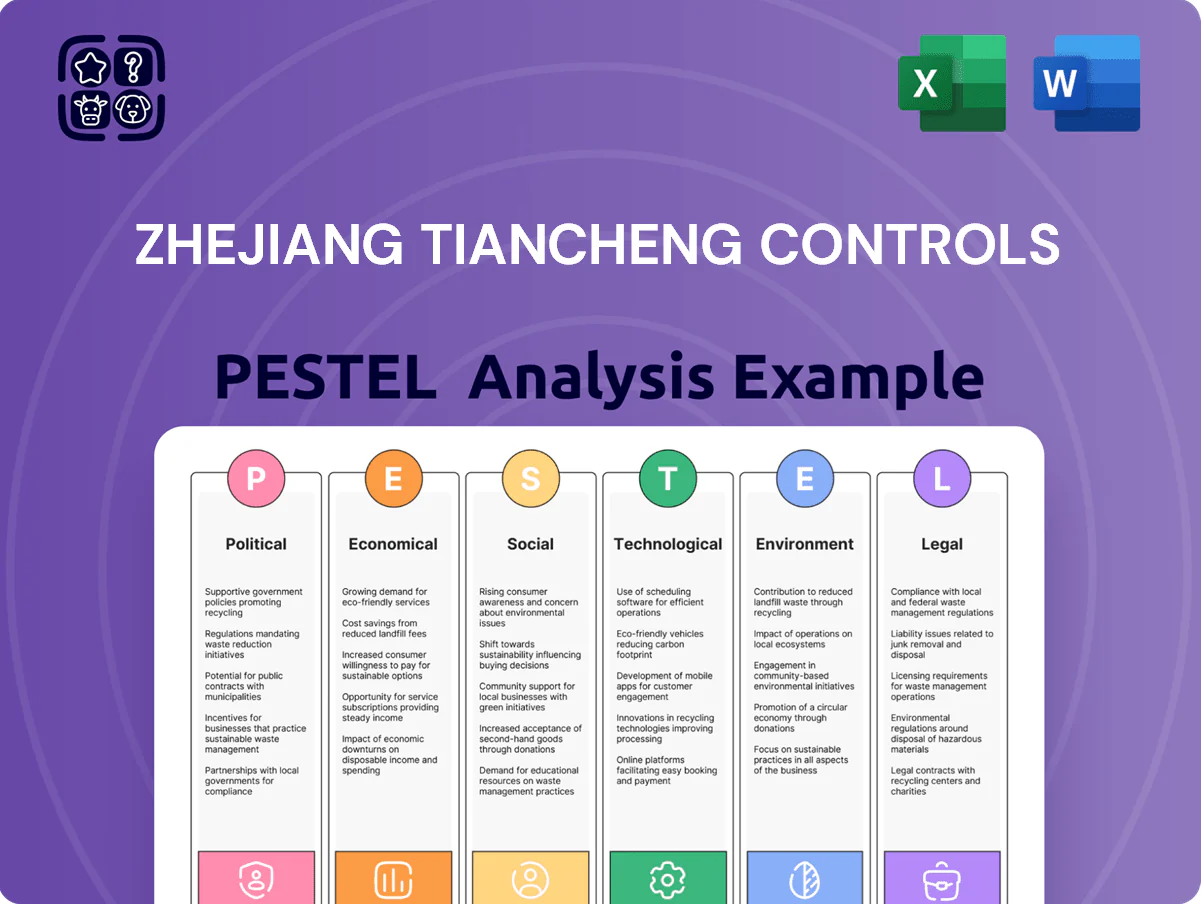

Zhejiang Tiancheng Controls PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Zhejiang Tiancheng Controls—pinpoint how political shifts, economic cycles, and tech trends affect growth and risk. Tailored for investors and strategists, this concise briefing reveals actionable insights you can apply immediately. Purchase the full report to access detailed implications, supporting data, and editable charts for quicker, smarter decisions.

Political factors

Industrial Policy Support

The Chinese government continued prioritizing automotive and high-end equipment manufacturing through policies in 2025–2026, directing over CNY 120 billion in targeted incentives; Zhejiang Tiancheng Controls benefits as a domestic supplier of vehicle control components.

Geopolitical Trade Relations

Ongoing trade tensions between China and Western economies complicate exports of automotive seats and agricultural machinery components, with US-China tariffs affecting $650m in bilateral automotive parts trade in 2024 and EU anti-dumping probes rising 18% year-on-year. Tariff volatility from the US or EU can squeeze margins and alter international pricing, risking single-digit market share declines in vulnerable regions. Management should diversify production: increasing ASEAN output (Vietnam/Thailand share rose to 14% of Chinese parts exports in 2025) and deepening regional partnerships to hedge geopolitical risk.

New Energy Vehicle Subsidies

Government support for New Energy Vehicles remains pivotal through 2025, with China allocating about CNY 1.2 trillion (2024–25) to EV infrastructure and supply-chain incentives; direct consumer subsidies have declined by ~40% since 2020.

Policy emphasis now targets charging stations and battery supply chains—over 2.1 million public chargers nationwide by end-2024—benefiting component suppliers like Zhejiang Tiancheng Controls.

Tiancheng aligns R&D to EV mandates, positioning to win contracts from state-backed OEMs; BYD, SAIC, and Geely account for ~45% of EV output in 2024, representing key addressable demand.

Safety Regulation Mandates

Strict political oversight on vehicle safety compels Zhejiang Tiancheng Controls to invest continually in seat-control innovation and reinforced structures; China updated GB safety standards in 2024, tightening crashworthiness and seat anchorage rules that affect ~26 million new vehicle registrations in 2024.

Frequent government revisions aim to cut road/workplace fatalities—China reported 59,000 traffic deaths in 2023—forcing rapid product updates for passenger and industrial seats.

The company must sustain regulatory engagement; noncompliance risks recalls and revenue loss—automotive OEM recalls in China rose 18% in 2024—so close ties with agencies are essential.

- 2024 GB updates affect seat anchorage and airbag interlocks

- ~26M new vehicles in China (2024) enlarge compliance scope

- 59,000 traffic deaths (2023) drive stricter rules

- 18% rise in OEM recalls (2024) increases risk

Rural Development Initiatives

China's rural revitalization and agricultural modernization policies, including subsidies and mechanization targets, boost demand for specialized farming machinery seats; Ministry of Agriculture aims to raise farm mechanization above 70% by 2025, supporting Tiancheng's agricultural-seat segment.

Government procurement and subsidy programs (rural equipment investment grew ~8% YoY in 2024) provide a stable revenue base, cushioning Tiancheng against passenger-car cyclicality where auto sales fell ~3% in 2024.

- Mechanization target >70% by 2025

- Rural equipment investment +8% YoY (2024)

- Agricultural-seat demand stabilizes revenue vs auto downturns

Tiancheng primed by massive EV & rural equipment stimulus, but export rules raise risks

Strong state support for EVs and equipment manufacturing (CNY 1.2T EV incentives 2024–25; 2.1M public chargers by 2024) and rural mechanization (>70% target by 2025; rural equipment investment +8% YoY 2024) boosts Tiancheng; trade tensions (US tariffs impacting $650M parts trade 2024) and tighter GB safety rules (affecting ~26M new vehicles 2024) raise compliance and export risks.

| Metric | Value |

|---|---|

| EV incentives (2024–25) | CNY 1.2T |

| Public chargers (end-2024) | 2.1M |

| Rural mechanization target | >70% (2025) |

| Rural equipment invest 2024 | +8% YoY |

| US-China parts trade affected | $650M (2024) |

| New vehicles impacted by GB rules | ~26M (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Zhejiang Tiancheng Controls across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities tailored for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Zhejiang Tiancheng Controls that simplifies regulatory, economic, social, technological, environmental, and legal risks for quick reference in meetings or presentations.

Economic factors

Raw Material Cost Fluctuations

The profitability of Zhejiang Tiancheng Controls is highly sensitive to steel, plastic resin and upholstery fabric prices; steel rose ~18% and resin spot prices averaged +12% YoY in 2024, pressuring COGS.

By end-2025, ongoing commodity volatility—IMF commodity index swings ±15% in 2024—necessitates advanced procurement, JIT contracts and hedging to stabilize input costs.

Sharp raw-material cost hikes not passed to OEMs could cut operating margin by an estimated 150–300 basis points based on 2024 cost structures.

Automotive Market Growth Trends

The global automotive market grew 6% in 2024 to ~94 million light vehicles, boosting demand for seat control systems; mature markets (NA, EU, JP) showed flat-to-low-single-digit growth while China, India and Southeast Asia together added ~7–9% YOY, driving higher volume needs for Zhejiang Tiancheng Controls.

Shift to shared mobility and AD/EVs alters product mix: EV penetration reached ~18% of global sales in 2024 and autonomous vehicle pilots expanded revenue opportunities for advanced seat actuators and sensors, with premium seating content per vehicle rising 12–18% in key markets.

Labor Cost Inflation

Rising wages in Zhejiang and other Chinese manufacturing hubs climbed about 6-8% annually in 2023–2024, squeezing margins for labor-intensive assembly at Zhejiang Tiancheng Controls; average manufacturing wages in Zhejiang reached roughly CNY 85,000–95,000 per annum by 2024. To stay competitive by 2025 the firm must offset ~10–15% higher labor costs via automation and process upgrades, accelerating capital-intensive shifts already reflected in planned CAPEX increases of ~12% year-on-year.

Currency Exchange Volatility

As an exporter-importer, Zhejiang Tiancheng faces Renminbi volatility versus USD/EUR; CNY moved ~3.5% vs USD in 2024 and FX swings trimmed manufacturing margins by an estimated 1.2–2.0 percentage points in FY2024.

RMB depreciation boosts export competitiveness but raised imported component costs—import bills rose ~6% YoY in 2024 for comparable inputs—pressuring gross margins.

Robust treasury and hedging needed: company-level FX hedges covering 40–60% of net exposure can stabilize earnings against sudden moves seen in 2022–2024.

- 2024 RMB vs USD volatility ~3.5%

- Imported input costs up ~6% YoY in 2024

- FX impact on margins ~1.2–2.0 ppt in FY2024

- Recommended hedging coverage 40–60% of exposure

Construction and Infrastructure Spending

Economic cycles in construction and infrastructure directly affect Tiancheng Controls’ heavy machinery seat sales; global construction output grew 3.6% in 2024 after a 2023 slowdown, lifting demand for operator cabins and seats.

Major stimulus: China’s 2024 infrastructure investment rose 5.2% YoY through Q3, and global construction equipment shipments increased ~8% in 2024, boosting market opportunities for specialized seating.

Tiancheng monitors PMI, government capex, and equipment OEM orders to forecast seat demand and adjust production.

- 2024 global construction output +3.6%

- China infra investment +5.2% YoY (2024 through Q3)

- Construction equipment shipments +~8% in 2024

Input costs surge, EVs climb: steel +18%, resin +12%, global LV +6% in 2024

Steel/resin up ~18%/12% in 2024; wage inflation 6–8% (Zhejiang avg CNY85–95k); RMB vs USD vol ~3.5% (FX hit margins 1.2–2.0ppt); global LV sales +6% to ~94m (2024); EV share ~18%; China infra +5.2% through Q3 2024.

| Metric | 2024 |

|---|---|

| Steel price | +18% |

| Resin | +12% |

| Wages (Zhejiang) | CNY85–95k (+6–8%) |

| RMB vs USD vol | ~3.5% |

| Global LV | 94m (+6%) |

Preview the Actual Deliverable

Zhejiang Tiancheng Controls PESTLE Analysis

The preview shown here is the exact Zhejiang Tiancheng Controls PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment—no placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Zhejiang Tiancheng Controls—pinpoint how political shifts, economic cycles, and tech trends affect growth and risk. Tailored for investors and strategists, this concise briefing reveals actionable insights you can apply immediately. Purchase the full report to access detailed implications, supporting data, and editable charts for quicker, smarter decisions.

Political factors

Industrial Policy Support

The Chinese government continued prioritizing automotive and high-end equipment manufacturing through policies in 2025–2026, directing over CNY 120 billion in targeted incentives; Zhejiang Tiancheng Controls benefits as a domestic supplier of vehicle control components.

Geopolitical Trade Relations

Ongoing trade tensions between China and Western economies complicate exports of automotive seats and agricultural machinery components, with US-China tariffs affecting $650m in bilateral automotive parts trade in 2024 and EU anti-dumping probes rising 18% year-on-year. Tariff volatility from the US or EU can squeeze margins and alter international pricing, risking single-digit market share declines in vulnerable regions. Management should diversify production: increasing ASEAN output (Vietnam/Thailand share rose to 14% of Chinese parts exports in 2025) and deepening regional partnerships to hedge geopolitical risk.

New Energy Vehicle Subsidies

Government support for New Energy Vehicles remains pivotal through 2025, with China allocating about CNY 1.2 trillion (2024–25) to EV infrastructure and supply-chain incentives; direct consumer subsidies have declined by ~40% since 2020.

Policy emphasis now targets charging stations and battery supply chains—over 2.1 million public chargers nationwide by end-2024—benefiting component suppliers like Zhejiang Tiancheng Controls.

Tiancheng aligns R&D to EV mandates, positioning to win contracts from state-backed OEMs; BYD, SAIC, and Geely account for ~45% of EV output in 2024, representing key addressable demand.

Safety Regulation Mandates

Strict political oversight on vehicle safety compels Zhejiang Tiancheng Controls to invest continually in seat-control innovation and reinforced structures; China updated GB safety standards in 2024, tightening crashworthiness and seat anchorage rules that affect ~26 million new vehicle registrations in 2024.

Frequent government revisions aim to cut road/workplace fatalities—China reported 59,000 traffic deaths in 2023—forcing rapid product updates for passenger and industrial seats.

The company must sustain regulatory engagement; noncompliance risks recalls and revenue loss—automotive OEM recalls in China rose 18% in 2024—so close ties with agencies are essential.

- 2024 GB updates affect seat anchorage and airbag interlocks

- ~26M new vehicles in China (2024) enlarge compliance scope

- 59,000 traffic deaths (2023) drive stricter rules

- 18% rise in OEM recalls (2024) increases risk

Rural Development Initiatives

China's rural revitalization and agricultural modernization policies, including subsidies and mechanization targets, boost demand for specialized farming machinery seats; Ministry of Agriculture aims to raise farm mechanization above 70% by 2025, supporting Tiancheng's agricultural-seat segment.

Government procurement and subsidy programs (rural equipment investment grew ~8% YoY in 2024) provide a stable revenue base, cushioning Tiancheng against passenger-car cyclicality where auto sales fell ~3% in 2024.

- Mechanization target >70% by 2025

- Rural equipment investment +8% YoY (2024)

- Agricultural-seat demand stabilizes revenue vs auto downturns

Tiancheng primed by massive EV & rural equipment stimulus, but export rules raise risks

Strong state support for EVs and equipment manufacturing (CNY 1.2T EV incentives 2024–25; 2.1M public chargers by 2024) and rural mechanization (>70% target by 2025; rural equipment investment +8% YoY 2024) boosts Tiancheng; trade tensions (US tariffs impacting $650M parts trade 2024) and tighter GB safety rules (affecting ~26M new vehicles 2024) raise compliance and export risks.

| Metric | Value |

|---|---|

| EV incentives (2024–25) | CNY 1.2T |

| Public chargers (end-2024) | 2.1M |

| Rural mechanization target | >70% (2025) |

| Rural equipment invest 2024 | +8% YoY |

| US-China parts trade affected | $650M (2024) |

| New vehicles impacted by GB rules | ~26M (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Zhejiang Tiancheng Controls across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities tailored for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Zhejiang Tiancheng Controls that simplifies regulatory, economic, social, technological, environmental, and legal risks for quick reference in meetings or presentations.

Economic factors

Raw Material Cost Fluctuations

The profitability of Zhejiang Tiancheng Controls is highly sensitive to steel, plastic resin and upholstery fabric prices; steel rose ~18% and resin spot prices averaged +12% YoY in 2024, pressuring COGS.

By end-2025, ongoing commodity volatility—IMF commodity index swings ±15% in 2024—necessitates advanced procurement, JIT contracts and hedging to stabilize input costs.

Sharp raw-material cost hikes not passed to OEMs could cut operating margin by an estimated 150–300 basis points based on 2024 cost structures.

Automotive Market Growth Trends

The global automotive market grew 6% in 2024 to ~94 million light vehicles, boosting demand for seat control systems; mature markets (NA, EU, JP) showed flat-to-low-single-digit growth while China, India and Southeast Asia together added ~7–9% YOY, driving higher volume needs for Zhejiang Tiancheng Controls.

Shift to shared mobility and AD/EVs alters product mix: EV penetration reached ~18% of global sales in 2024 and autonomous vehicle pilots expanded revenue opportunities for advanced seat actuators and sensors, with premium seating content per vehicle rising 12–18% in key markets.

Labor Cost Inflation

Rising wages in Zhejiang and other Chinese manufacturing hubs climbed about 6-8% annually in 2023–2024, squeezing margins for labor-intensive assembly at Zhejiang Tiancheng Controls; average manufacturing wages in Zhejiang reached roughly CNY 85,000–95,000 per annum by 2024. To stay competitive by 2025 the firm must offset ~10–15% higher labor costs via automation and process upgrades, accelerating capital-intensive shifts already reflected in planned CAPEX increases of ~12% year-on-year.

Currency Exchange Volatility

As an exporter-importer, Zhejiang Tiancheng faces Renminbi volatility versus USD/EUR; CNY moved ~3.5% vs USD in 2024 and FX swings trimmed manufacturing margins by an estimated 1.2–2.0 percentage points in FY2024.

RMB depreciation boosts export competitiveness but raised imported component costs—import bills rose ~6% YoY in 2024 for comparable inputs—pressuring gross margins.

Robust treasury and hedging needed: company-level FX hedges covering 40–60% of net exposure can stabilize earnings against sudden moves seen in 2022–2024.

- 2024 RMB vs USD volatility ~3.5%

- Imported input costs up ~6% YoY in 2024

- FX impact on margins ~1.2–2.0 ppt in FY2024

- Recommended hedging coverage 40–60% of exposure

Construction and Infrastructure Spending

Economic cycles in construction and infrastructure directly affect Tiancheng Controls’ heavy machinery seat sales; global construction output grew 3.6% in 2024 after a 2023 slowdown, lifting demand for operator cabins and seats.

Major stimulus: China’s 2024 infrastructure investment rose 5.2% YoY through Q3, and global construction equipment shipments increased ~8% in 2024, boosting market opportunities for specialized seating.

Tiancheng monitors PMI, government capex, and equipment OEM orders to forecast seat demand and adjust production.

- 2024 global construction output +3.6%

- China infra investment +5.2% YoY (2024 through Q3)

- Construction equipment shipments +~8% in 2024

Input costs surge, EVs climb: steel +18%, resin +12%, global LV +6% in 2024

Steel/resin up ~18%/12% in 2024; wage inflation 6–8% (Zhejiang avg CNY85–95k); RMB vs USD vol ~3.5% (FX hit margins 1.2–2.0ppt); global LV sales +6% to ~94m (2024); EV share ~18%; China infra +5.2% through Q3 2024.

| Metric | 2024 |

|---|---|

| Steel price | +18% |

| Resin | +12% |

| Wages (Zhejiang) | CNY85–95k (+6–8%) |

| RMB vs USD vol | ~3.5% |

| Global LV | 94m (+6%) |

Preview the Actual Deliverable

Zhejiang Tiancheng Controls PESTLE Analysis

The preview shown here is the exact Zhejiang Tiancheng Controls PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment—no placeholders, no surprises.