China Gas Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, energy pricing, and technological innovation are reshaping China Gas Holdings’ growth path—our concise PESTLE snapshot highlights opportunities and risks you can act on now; purchase the full analysis for a comprehensive, board-ready report with actionable recommendations.

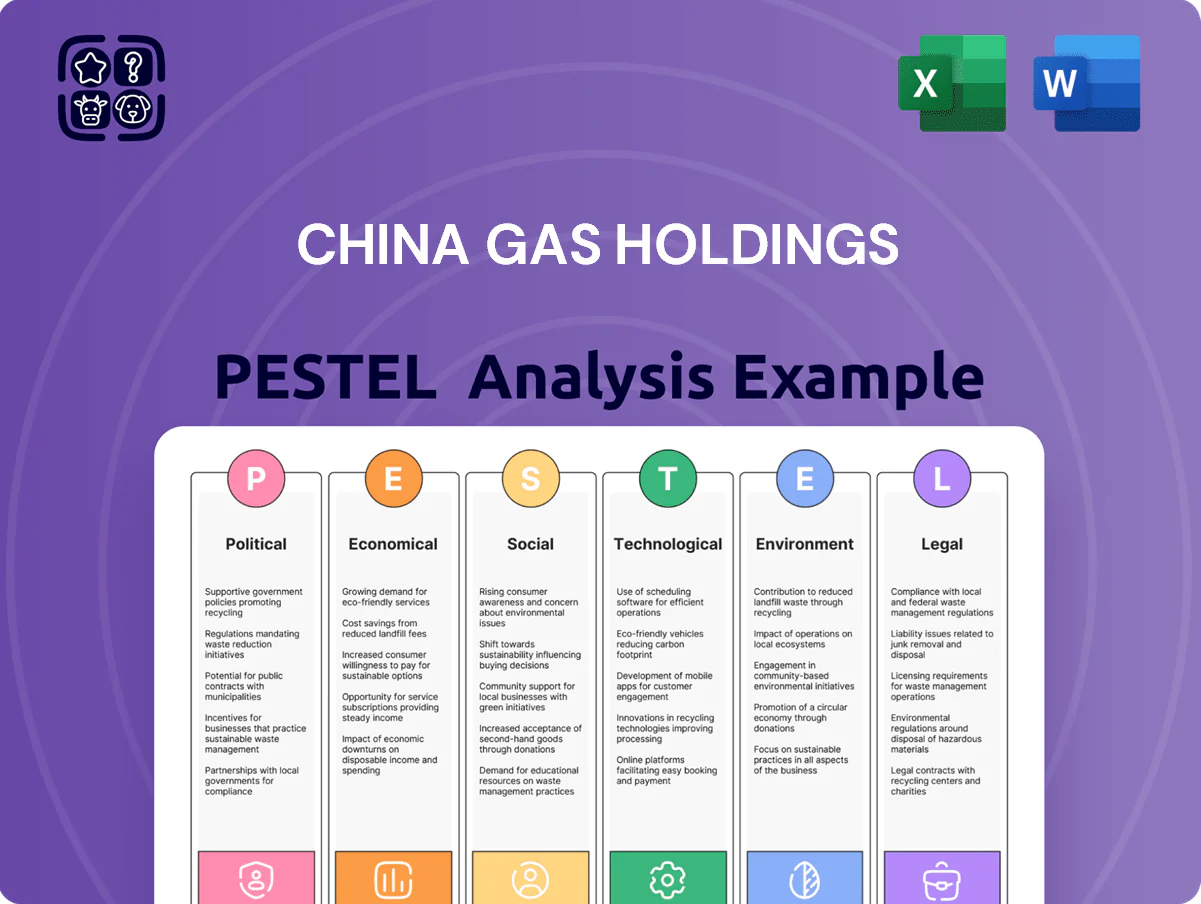

Political factors

Energy Security and State Policy Alignment

The Chinese government prioritizes energy security, targeting a 20% share for natural gas in primary energy consumption by 2025, reducing coal dependence; China Gas aligns expansion with the 14th Five-Year Plan, accelerating pipeline and LNG terminal projects to tap this shift.

Geopolitical Tensions and Import Stability

Ongoing geopolitical shifts, notably Russia-Ukraine tensions and Central Asia pipeline politics, raise volatility in import volumes and prices; China imported about 16% of its pipeline gas from Central Asia and over 7 bcm LNG from Russia in 2024, exposing China Gas to supply-cost swings.

As a major distributor serving 22+ million customers, China Gas must manage trade barriers, sanctions risk and freight-cost changes that can raise LNG procurement costs by 10–25% in shock scenarios.

Diplomatic outcomes—e.g., 2024 China-Russia energy agreements worth estimated $30–40 billion—directly affect China Gas’s ability to secure long-term contracts and maintain steady industrial and residential supply.

Rural Revitalization and Gas-to-Coal Initiatives

The central government's rural revitalization drives expansion of gas infrastructure into 600,000+ village households; China Gas is a key implementer, targeting capacity additions aligned with 2024–25 plans to reach ~35 million piped customers nationwide.

State mandates to replace coal with natural gas in northern provinces underpin China Gas's role; nationwide coal-to-gas campaigns cut household coal use by ~20% (2023–24) and propel demand growth of 8–12% annually in targeted regions.

These politically driven programs create sizable revenue upside—China Gas reported FY2024 gas sales volume growth of ~9%—but require heavy capex, with industry pipeline and infrastructure spending estimated at RMB 30–50 billion annually to meet central deadlines.

Local Government Relations and Franchising

Operational success for China Gas hinges on municipal ties across 300+ city concessions; FY2024 revenue from city-gas operations accounted for about 78% of group revenue (HKD figure per annual report 2024).

Exclusive franchise rights are locally granted, so lobbying, permit compliance and RMB-denominated tariff approvals are critical to protect recurring cash flows and EBITDA margins.

Leadership changes or regional policy shifts may disrupt concession terms—historical renegotiations have affected project timelines, with some pipeline rollouts delayed by 6–18 months.

- 300+ city concessions

- 78% of FY2024 revenue from city-gas

- RMB tariffs and local approvals drive EBITDA stability

- Past renegotiations caused 6–18 month delays

State-Owned Enterprise Competition and Collaboration

While China Gas is privately listed, it competes and partners with SOEs such as PipeChina and PetroChina, which together control over 60% of China's midstream pipeline capacity as of 2024.

Political dynamics force China Gas to secure joint ventures or third-party access agreements to reach customers, with SOE-led pipeline tariffs and allocation rules materially affecting margins.

Regulatory leverage of SOEs is a persistent political risk to China Gas's market share and expansion plans.

- SOEs (PipeChina, PetroChina) control >60% midstream capacity (2024)

- Joint ventures and access agreements essential for supply routes

- SOE tariff/regulatory influence directly impacts China Gas margins

China city-gas boom: 300+ concessions, SOE midstream control and 8–12% demand uptick

Political support for gas (20% target by 2025) and coal-to-gas mandates drive ~8–12% regional demand growth; China Gas’s 300+ city concessions generated ~78% of FY2024 revenue, with FY2024 sales +9% and sector capex ~RMB30–50bn/year. SOEs control >60% midstream capacity (2024), making JV/access deals and local tariff approvals critical to margins.

| Metric | Value (2024) |

|---|---|

| City concessions | 300+ |

| Revenue from city-gas | 78% FY2024 |

| Sales volume growth | ~9% |

| Midstream SOE share | >60% |

| Sector capex | RMB30–50bn/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect China Gas Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of China Gas Holdings for quick reference in meetings, highlighting key political, economic, social, technological, legal and environmental factors that relieve prep time and support rapid decision-making.

Economic factors

Natural Gas Pricing Reform and Cost Pass-Through

The Chinese government is shifting to market-oriented natural gas pricing, with spot-linked import prices rising 18% year-on-year in 2024, pressuring distributors like China Gas Holdings. The company faces a procurement-to-retail pass-through lag averaging 2–6 months, squeezing margins when LNG FOB import costs jumped to about $12–14/MMBtu in 2024. Profitability is highly sensitive to NDRC price-smoothing policies; a 1% delay in tariff adjustment can reduce EBITDA margin by an estimated 0.3–0.6 percentage points. Continued liberalization could widen volatility but also allow faster cost recovery when regulatory alignment improves.

Macroeconomic Growth and Industrial Demand

China Gas Holdings faces demand tied to China's GDP: 2024 GDP growth slowed to about 5.2%, and industrial production rose 3.5% year-on-year in 2024, constraining industrial gas volumes and pressuring distribution revenue.

Manufacturing downturns cut commercial gas use, while targeted 2024–25 stimulus for heavy-industry provinces and a CNY 1.2 trillion infrastructure push could lift pipeline utilization and gas sales.

Interest Rate Environment and Debt Management

As an infrastructure-heavy business, China Gas carried net debt of HKD 42.3 billion as of 2024 year-end, financing capital-intensive pipeline and LNG projects; rising domestic Hibor and global policy rates pushed blended borrowing costs toward ~4.5% in 2024, tightening cash flow. Fluctuations in domestic and international rates affect cost of capital and debt-servicing capacity, forcing management to use interest rate swaps and FX forwards. Strategic hedging is critical to protect margins and sustain investment-grade ratings.

Inflationary Pressures on Operational Costs

Rising inflation in China—CPI up 0.7% year-on-year in Jan 2026 and PPI at 1.6% in 2025—raises costs for steel, compressors and skilled labor, increasing capex for pipeline and terminal projects by an estimated 5–8% versus pre-inflation forecasts.

Such cost escalation can compress China Gas Holdings’ margins unless offset by efficiency gains or higher regulated tariffs; the company’s FY2025 gross margin of 18.2% leaves limited buffer.

Regular tracking of the Producer Price Index is critical to forecast capital needs for upcoming gas storage and terminal projects and to time procurement hedges.

- Inflation-driven capex rise: +5–8%

- PPI 2025: 1.6%

- CPI Jan 2026: 0.7%

- FY2025 gross margin: 18.2%

Urbanization Rates and Residential Consumption

Urbanization in China reached 64.7% in 2023 and was 65.2% in 2024, expanding addressable households and boosting demand for residential gas connections and gas appliances.

Pro-homeownership and urban development policies, including 2024 local housing incentives, directly increase China Gas’s potential customer base and recurring connection fee income.

The company has raised household penetration in targeted cities by ~3–5 percentage points annually, translating into higher recurring revenues.

- 2024 urbanization 65.2%

- Household penetration up 3–5 pp/year

- Rising recurring connection fees

Rising LNG costs, squeezed margins and higher capex amid steady GDP and HKD 42.3bn debt

Economic factors: gas price liberalization raised LNG FOB to ~$12–14/MMBtu in 2024, squeezing margins due to 2–6 month pass-through lag; 2024 GDP ~5.2% and industrial production +3.5% limited industrial demand; net debt HKD 42.3bn with blended borrowing cost ~4.5% in 2024; CPI Jan 2026 0.7%, PPI 2025 1.6% pushing capex +5–8%.

| Metric | Value |

|---|---|

| LNG FOB 2024 | $12–14/MMBtu |

| GDP 2024 | 5.2% |

| Net debt | HKD 42.3bn |

| Borrowing cost 2024 | ~4.5% |

Full Version Awaits

China Gas Holdings PESTLE Analysis

The preview shown here is the exact China Gas Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, energy pricing, and technological innovation are reshaping China Gas Holdings’ growth path—our concise PESTLE snapshot highlights opportunities and risks you can act on now; purchase the full analysis for a comprehensive, board-ready report with actionable recommendations.

Political factors

Energy Security and State Policy Alignment

The Chinese government prioritizes energy security, targeting a 20% share for natural gas in primary energy consumption by 2025, reducing coal dependence; China Gas aligns expansion with the 14th Five-Year Plan, accelerating pipeline and LNG terminal projects to tap this shift.

Geopolitical Tensions and Import Stability

Ongoing geopolitical shifts, notably Russia-Ukraine tensions and Central Asia pipeline politics, raise volatility in import volumes and prices; China imported about 16% of its pipeline gas from Central Asia and over 7 bcm LNG from Russia in 2024, exposing China Gas to supply-cost swings.

As a major distributor serving 22+ million customers, China Gas must manage trade barriers, sanctions risk and freight-cost changes that can raise LNG procurement costs by 10–25% in shock scenarios.

Diplomatic outcomes—e.g., 2024 China-Russia energy agreements worth estimated $30–40 billion—directly affect China Gas’s ability to secure long-term contracts and maintain steady industrial and residential supply.

Rural Revitalization and Gas-to-Coal Initiatives

The central government's rural revitalization drives expansion of gas infrastructure into 600,000+ village households; China Gas is a key implementer, targeting capacity additions aligned with 2024–25 plans to reach ~35 million piped customers nationwide.

State mandates to replace coal with natural gas in northern provinces underpin China Gas's role; nationwide coal-to-gas campaigns cut household coal use by ~20% (2023–24) and propel demand growth of 8–12% annually in targeted regions.

These politically driven programs create sizable revenue upside—China Gas reported FY2024 gas sales volume growth of ~9%—but require heavy capex, with industry pipeline and infrastructure spending estimated at RMB 30–50 billion annually to meet central deadlines.

Local Government Relations and Franchising

Operational success for China Gas hinges on municipal ties across 300+ city concessions; FY2024 revenue from city-gas operations accounted for about 78% of group revenue (HKD figure per annual report 2024).

Exclusive franchise rights are locally granted, so lobbying, permit compliance and RMB-denominated tariff approvals are critical to protect recurring cash flows and EBITDA margins.

Leadership changes or regional policy shifts may disrupt concession terms—historical renegotiations have affected project timelines, with some pipeline rollouts delayed by 6–18 months.

- 300+ city concessions

- 78% of FY2024 revenue from city-gas

- RMB tariffs and local approvals drive EBITDA stability

- Past renegotiations caused 6–18 month delays

State-Owned Enterprise Competition and Collaboration

While China Gas is privately listed, it competes and partners with SOEs such as PipeChina and PetroChina, which together control over 60% of China's midstream pipeline capacity as of 2024.

Political dynamics force China Gas to secure joint ventures or third-party access agreements to reach customers, with SOE-led pipeline tariffs and allocation rules materially affecting margins.

Regulatory leverage of SOEs is a persistent political risk to China Gas's market share and expansion plans.

- SOEs (PipeChina, PetroChina) control >60% midstream capacity (2024)

- Joint ventures and access agreements essential for supply routes

- SOE tariff/regulatory influence directly impacts China Gas margins

China city-gas boom: 300+ concessions, SOE midstream control and 8–12% demand uptick

Political support for gas (20% target by 2025) and coal-to-gas mandates drive ~8–12% regional demand growth; China Gas’s 300+ city concessions generated ~78% of FY2024 revenue, with FY2024 sales +9% and sector capex ~RMB30–50bn/year. SOEs control >60% midstream capacity (2024), making JV/access deals and local tariff approvals critical to margins.

| Metric | Value (2024) |

|---|---|

| City concessions | 300+ |

| Revenue from city-gas | 78% FY2024 |

| Sales volume growth | ~9% |

| Midstream SOE share | >60% |

| Sector capex | RMB30–50bn/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect China Gas Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of China Gas Holdings for quick reference in meetings, highlighting key political, economic, social, technological, legal and environmental factors that relieve prep time and support rapid decision-making.

Economic factors

Natural Gas Pricing Reform and Cost Pass-Through

The Chinese government is shifting to market-oriented natural gas pricing, with spot-linked import prices rising 18% year-on-year in 2024, pressuring distributors like China Gas Holdings. The company faces a procurement-to-retail pass-through lag averaging 2–6 months, squeezing margins when LNG FOB import costs jumped to about $12–14/MMBtu in 2024. Profitability is highly sensitive to NDRC price-smoothing policies; a 1% delay in tariff adjustment can reduce EBITDA margin by an estimated 0.3–0.6 percentage points. Continued liberalization could widen volatility but also allow faster cost recovery when regulatory alignment improves.

Macroeconomic Growth and Industrial Demand

China Gas Holdings faces demand tied to China's GDP: 2024 GDP growth slowed to about 5.2%, and industrial production rose 3.5% year-on-year in 2024, constraining industrial gas volumes and pressuring distribution revenue.

Manufacturing downturns cut commercial gas use, while targeted 2024–25 stimulus for heavy-industry provinces and a CNY 1.2 trillion infrastructure push could lift pipeline utilization and gas sales.

Interest Rate Environment and Debt Management

As an infrastructure-heavy business, China Gas carried net debt of HKD 42.3 billion as of 2024 year-end, financing capital-intensive pipeline and LNG projects; rising domestic Hibor and global policy rates pushed blended borrowing costs toward ~4.5% in 2024, tightening cash flow. Fluctuations in domestic and international rates affect cost of capital and debt-servicing capacity, forcing management to use interest rate swaps and FX forwards. Strategic hedging is critical to protect margins and sustain investment-grade ratings.

Inflationary Pressures on Operational Costs

Rising inflation in China—CPI up 0.7% year-on-year in Jan 2026 and PPI at 1.6% in 2025—raises costs for steel, compressors and skilled labor, increasing capex for pipeline and terminal projects by an estimated 5–8% versus pre-inflation forecasts.

Such cost escalation can compress China Gas Holdings’ margins unless offset by efficiency gains or higher regulated tariffs; the company’s FY2025 gross margin of 18.2% leaves limited buffer.

Regular tracking of the Producer Price Index is critical to forecast capital needs for upcoming gas storage and terminal projects and to time procurement hedges.

- Inflation-driven capex rise: +5–8%

- PPI 2025: 1.6%

- CPI Jan 2026: 0.7%

- FY2025 gross margin: 18.2%

Urbanization Rates and Residential Consumption

Urbanization in China reached 64.7% in 2023 and was 65.2% in 2024, expanding addressable households and boosting demand for residential gas connections and gas appliances.

Pro-homeownership and urban development policies, including 2024 local housing incentives, directly increase China Gas’s potential customer base and recurring connection fee income.

The company has raised household penetration in targeted cities by ~3–5 percentage points annually, translating into higher recurring revenues.

- 2024 urbanization 65.2%

- Household penetration up 3–5 pp/year

- Rising recurring connection fees

Rising LNG costs, squeezed margins and higher capex amid steady GDP and HKD 42.3bn debt

Economic factors: gas price liberalization raised LNG FOB to ~$12–14/MMBtu in 2024, squeezing margins due to 2–6 month pass-through lag; 2024 GDP ~5.2% and industrial production +3.5% limited industrial demand; net debt HKD 42.3bn with blended borrowing cost ~4.5% in 2024; CPI Jan 2026 0.7%, PPI 2025 1.6% pushing capex +5–8%.

| Metric | Value |

|---|---|

| LNG FOB 2024 | $12–14/MMBtu |

| GDP 2024 | 5.2% |

| Net debt | HKD 42.3bn |

| Borrowing cost 2024 | ~4.5% |

Full Version Awaits

China Gas Holdings PESTLE Analysis

The preview shown here is the exact China Gas Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.