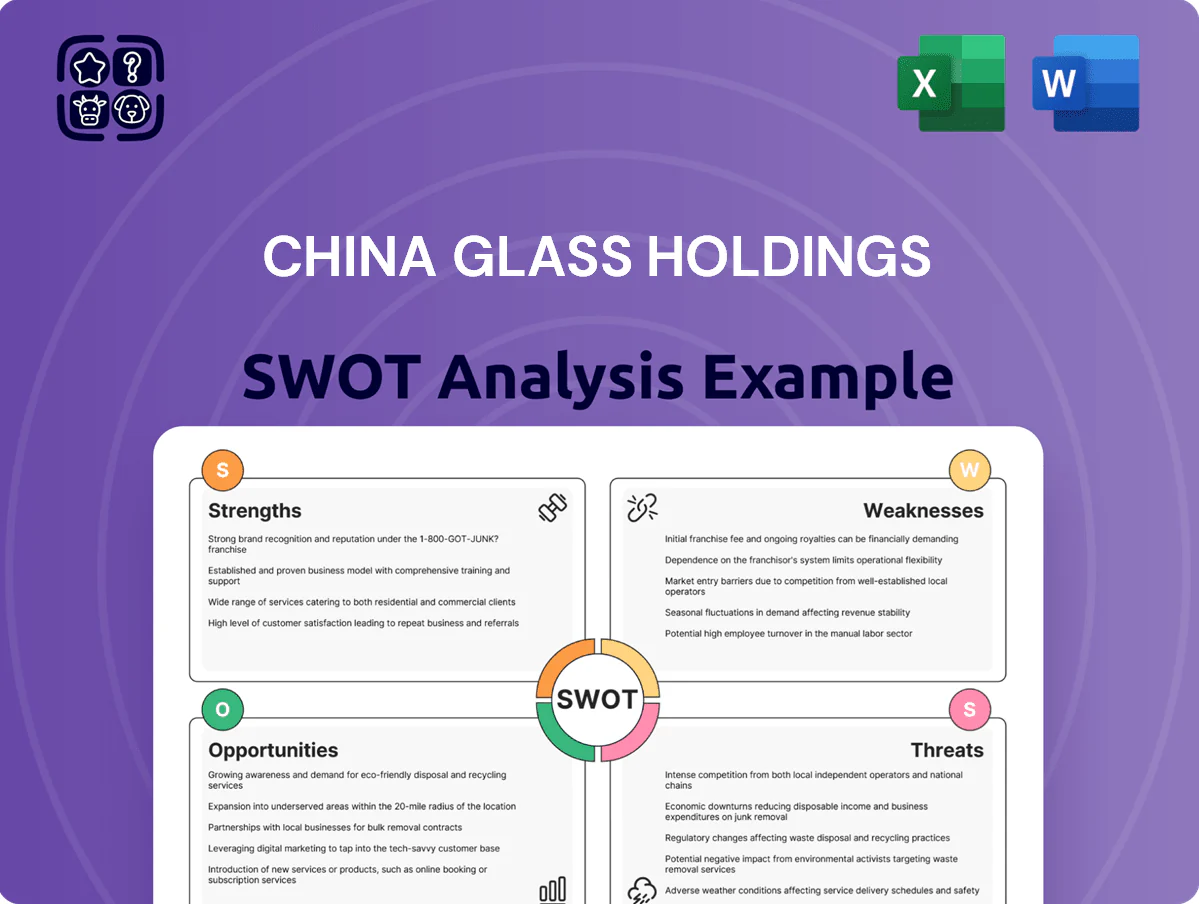

China Glass Holdings SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

China Glass Holdings shows resilient manufacturing scale and strong domestic demand exposure, yet faces margin pressure from raw material volatility and intensifying competition; its green-building credentials and export potential are notable growth levers. Discover the full picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to inform strategy, investment, or due diligence.

Strengths

Diversified Product Portfolio

China Glass Holdings offers float glass, energy-efficient low-emissivity (low-E) architectural glass, and specialized automotive glass, which in 2024 contributed roughly 42%, 35%, and 23% of segment revenue respectively according to company disclosures—spreading sales across construction, automotive, and decoration reduces single-market exposure.

Leading Market Position in China

China Glass Holdings ranks among China’s top glass makers with reported annual production capacity around 2.4 million tonnes as of 2025, giving scale advantages in raw material procurement and factory utilization.

That scale cuts unit costs and strengthens negotiating leverage with suppliers, helping the company maintain gross margins near industry peers (circa 15–18% in 2024 reporting periods).

Strong brand recognition supports winning large infrastructure and commercial contracts—projects often demand sustained high-volume supply, where China Glass’s distribution network across 20+ provinces provides a clear logistical edge.

Advanced Production Technology

Strategic Geographical Footprint

- ~15% lower transport cost

- 3–7 day response time

- Logistics ≈20–30% of delivered cost

- Facilities near Shenzhen, Beijing, Tianjin

Strong R&D for Energy Efficiency

- Focus: Low-E and energy-saving glass

- 2024 green-glass sales growth: 18%

- Gross-margin premium: ~240 bps (2024)

- Preferred supplier: government green projects

2.4Mt capacity lifts margins: R&D, logistics and green glass drive 14% ASP & +240bps

Large scale (2.4Mt capacity, 2025) lowers unit costs; diversified mix (float 42%, low-E 35%, auto 23% in 2024) reduces market risk; R&D spend RMB120m (2024) yields ±0.1mm control, >98% first-pass yield and 14% ASP premium; logistics across Guangdong, Hebei, Shandong cuts transport ~15% and enables 3–7 day response; green-glass sales +18% (2024), margin +240bps vs commodity.

| Metric | Value |

|---|---|

| Capacity 2025 | 2.4 Mt |

| Revenue mix 2024 | Float 42% / Low-E 35% / Auto 23% |

| R&D 2024 | RMB 120m |

| ASP premium 2024 | +14% |

| Transport saving | ~15% |

| Green sales growth 2024 | +18% |

| Margin premium | +240 bps |

What is included in the product

Provides a concise SWOT analysis of China Glass Holdings, highlighting its operational strengths and cost advantages, internal weaknesses and capacity constraints, external growth opportunities in construction and automotive glass demand, and threats from raw material price volatility and competitive pressures.

Provides a concise SWOT matrix for China Glass Holdings to quickly align strategy, highlight competitive glass manufacturing strengths, identify market and regulatory risks, and support fast stakeholder decision-making.

Weaknesses

High Sensitivity to Energy Prices

The glass manufacturing process is highly energy-intensive, so China Glass Holdings is exposed to natural gas and electricity price swings; for example, Chinese industrial power tariffs rose about 12% in 2024 in some provinces, which can cut gross margins by several percentage points if costs aren’t passed on. Rising energy costs compressed margins across the sector in 2023–2024, making this dependency a key operational risk during global or domestic market volatility.

Exposure to Real Estate Cycles

A substantial share of China Glass Holdings revenue comes from construction, tying earnings to a cyclical sector sensitive to interest rates and policy; China's new housing starts fell 23% year‑on‑year in 2024, cutting demand for architectural and float glass.

During the 2021–2024 property downturn, China Glass’s sales likely faced pressure as unit volumes dropped; any further policy tightening or rate hikes would quickly depress orders for new builds.

Significant Debt Obligations

Maintaining and expanding large-scale glass plants forces heavy capital spending, leaving China Glass Holdings with reported net debt of HKD 4.2 billion at FY2024 (Dec 31, 2024), raising leverage and interest costs; this reduces financial flexibility if rates rise. High debt means more cash must go to interest and principal, so consistent operating cash flow—2024 operating cash flow HKD 860 million—is essential to service debt while funding operations.

Raw Material Price Volatility

Raw material price volatility: China Glass Holdings depends on soda ash and silica sand; soda ash spot prices rose about 22% in 2024 to roughly $360/ton, squeezing margins for 2024 Q3–Q4 and beyond.

Supply shocks from mining curbs in Inner Mongolia and shipping delays in 2024 pushed input costs up 8–12%, forcing short-term margin compression and price pass-through limits in a crowded domestic market.

Managing these costs remains crucial to stay price-competitive; hedging and long-term contracts covered only ~30% of purchases in 2024, leaving exposure high.

- 2024 soda ash +22% (~$360/ton)

- 2024 input cost shock +8–12%

- Hedged volume ~30% in 2024

Lower Margins in Commodity Segments

China Glass earns higher returns from specialized glass, but roughly 60% of revenue comes from standard float glass, a commoditized product with low entry barriers and slim margins.

Intense competition fuels price wars; industry gross margins for float glass fell to about 12% in 2024, squeezing profitability despite high volumes.

The firm must balance scale—annual float output ~18 million tonnes—with margin recovery through product mix, cost control, and capacity discipline.

- ~60% revenue from float glass

- 2024 float gross margin ≈12%

- Annual float output ≈18 Mt

- Price wars → thin margins

High costs, weak housing demand and heavy leverage squeeze float glass margins

Energy‑intense production and 2024 industrial power tariff rises (~12%) plus soda ash +22% (~$360/ton) squeezed margins; hedging covered ~30% of purchases. Heavy reliance on cyclical construction (new housing starts -23% y/y 2024) makes revenue volatile. High leverage—net debt HKD 4.2bn, 2024 operating cash flow HKD 860m—limits flexibility. Commodity float glass (~60% revenue; ~18 Mt output) faces thin margins (~12% gross in 2024).

| Metric | 2024 |

|---|---|

| Industrial power tariff change | +~12% |

| Soda ash price | ~$360/ton (+22%) |

| Hedged purchases | ~30% |

| New housing starts | -23% y/y |

| Net debt | HKD 4.2bn |

| Operating cash flow | HKD 860m |

| Float revenue share | ~60% |

| Float output | ~18 Mt |

| Float gross margin | ~12% |

Preview Before You Purchase

China Glass Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report on China Glass Holdings, covering strengths, weaknesses, opportunities, and threats in a concise, actionable format. Buy to unlock the complete, editable version for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

China Glass Holdings shows resilient manufacturing scale and strong domestic demand exposure, yet faces margin pressure from raw material volatility and intensifying competition; its green-building credentials and export potential are notable growth levers. Discover the full picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to inform strategy, investment, or due diligence.

Strengths

Diversified Product Portfolio

China Glass Holdings offers float glass, energy-efficient low-emissivity (low-E) architectural glass, and specialized automotive glass, which in 2024 contributed roughly 42%, 35%, and 23% of segment revenue respectively according to company disclosures—spreading sales across construction, automotive, and decoration reduces single-market exposure.

Leading Market Position in China

China Glass Holdings ranks among China’s top glass makers with reported annual production capacity around 2.4 million tonnes as of 2025, giving scale advantages in raw material procurement and factory utilization.

That scale cuts unit costs and strengthens negotiating leverage with suppliers, helping the company maintain gross margins near industry peers (circa 15–18% in 2024 reporting periods).

Strong brand recognition supports winning large infrastructure and commercial contracts—projects often demand sustained high-volume supply, where China Glass’s distribution network across 20+ provinces provides a clear logistical edge.

Advanced Production Technology

Strategic Geographical Footprint

- ~15% lower transport cost

- 3–7 day response time

- Logistics ≈20–30% of delivered cost

- Facilities near Shenzhen, Beijing, Tianjin

Strong R&D for Energy Efficiency

- Focus: Low-E and energy-saving glass

- 2024 green-glass sales growth: 18%

- Gross-margin premium: ~240 bps (2024)

- Preferred supplier: government green projects

2.4Mt capacity lifts margins: R&D, logistics and green glass drive 14% ASP & +240bps

Large scale (2.4Mt capacity, 2025) lowers unit costs; diversified mix (float 42%, low-E 35%, auto 23% in 2024) reduces market risk; R&D spend RMB120m (2024) yields ±0.1mm control, >98% first-pass yield and 14% ASP premium; logistics across Guangdong, Hebei, Shandong cuts transport ~15% and enables 3–7 day response; green-glass sales +18% (2024), margin +240bps vs commodity.

| Metric | Value |

|---|---|

| Capacity 2025 | 2.4 Mt |

| Revenue mix 2024 | Float 42% / Low-E 35% / Auto 23% |

| R&D 2024 | RMB 120m |

| ASP premium 2024 | +14% |

| Transport saving | ~15% |

| Green sales growth 2024 | +18% |

| Margin premium | +240 bps |

What is included in the product

Provides a concise SWOT analysis of China Glass Holdings, highlighting its operational strengths and cost advantages, internal weaknesses and capacity constraints, external growth opportunities in construction and automotive glass demand, and threats from raw material price volatility and competitive pressures.

Provides a concise SWOT matrix for China Glass Holdings to quickly align strategy, highlight competitive glass manufacturing strengths, identify market and regulatory risks, and support fast stakeholder decision-making.

Weaknesses

High Sensitivity to Energy Prices

The glass manufacturing process is highly energy-intensive, so China Glass Holdings is exposed to natural gas and electricity price swings; for example, Chinese industrial power tariffs rose about 12% in 2024 in some provinces, which can cut gross margins by several percentage points if costs aren’t passed on. Rising energy costs compressed margins across the sector in 2023–2024, making this dependency a key operational risk during global or domestic market volatility.

Exposure to Real Estate Cycles

A substantial share of China Glass Holdings revenue comes from construction, tying earnings to a cyclical sector sensitive to interest rates and policy; China's new housing starts fell 23% year‑on‑year in 2024, cutting demand for architectural and float glass.

During the 2021–2024 property downturn, China Glass’s sales likely faced pressure as unit volumes dropped; any further policy tightening or rate hikes would quickly depress orders for new builds.

Significant Debt Obligations

Maintaining and expanding large-scale glass plants forces heavy capital spending, leaving China Glass Holdings with reported net debt of HKD 4.2 billion at FY2024 (Dec 31, 2024), raising leverage and interest costs; this reduces financial flexibility if rates rise. High debt means more cash must go to interest and principal, so consistent operating cash flow—2024 operating cash flow HKD 860 million—is essential to service debt while funding operations.

Raw Material Price Volatility

Raw material price volatility: China Glass Holdings depends on soda ash and silica sand; soda ash spot prices rose about 22% in 2024 to roughly $360/ton, squeezing margins for 2024 Q3–Q4 and beyond.

Supply shocks from mining curbs in Inner Mongolia and shipping delays in 2024 pushed input costs up 8–12%, forcing short-term margin compression and price pass-through limits in a crowded domestic market.

Managing these costs remains crucial to stay price-competitive; hedging and long-term contracts covered only ~30% of purchases in 2024, leaving exposure high.

- 2024 soda ash +22% (~$360/ton)

- 2024 input cost shock +8–12%

- Hedged volume ~30% in 2024

Lower Margins in Commodity Segments

China Glass earns higher returns from specialized glass, but roughly 60% of revenue comes from standard float glass, a commoditized product with low entry barriers and slim margins.

Intense competition fuels price wars; industry gross margins for float glass fell to about 12% in 2024, squeezing profitability despite high volumes.

The firm must balance scale—annual float output ~18 million tonnes—with margin recovery through product mix, cost control, and capacity discipline.

- ~60% revenue from float glass

- 2024 float gross margin ≈12%

- Annual float output ≈18 Mt

- Price wars → thin margins

High costs, weak housing demand and heavy leverage squeeze float glass margins

Energy‑intense production and 2024 industrial power tariff rises (~12%) plus soda ash +22% (~$360/ton) squeezed margins; hedging covered ~30% of purchases. Heavy reliance on cyclical construction (new housing starts -23% y/y 2024) makes revenue volatile. High leverage—net debt HKD 4.2bn, 2024 operating cash flow HKD 860m—limits flexibility. Commodity float glass (~60% revenue; ~18 Mt output) faces thin margins (~12% gross in 2024).

| Metric | 2024 |

|---|---|

| Industrial power tariff change | +~12% |

| Soda ash price | ~$360/ton (+22%) |

| Hedged purchases | ~30% |

| New housing starts | -23% y/y |

| Net debt | HKD 4.2bn |

| Operating cash flow | HKD 860m |

| Float revenue share | ~60% |

| Float output | ~18 Mt |

| Float gross margin | ~12% |

Preview Before You Purchase

China Glass Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report on China Glass Holdings, covering strengths, weaknesses, opportunities, and threats in a concise, actionable format. Buy to unlock the complete, editable version for immediate download and use.