China Tower Corp. Porter's Five Forces Analysis

From Overview to Strategy Blueprint

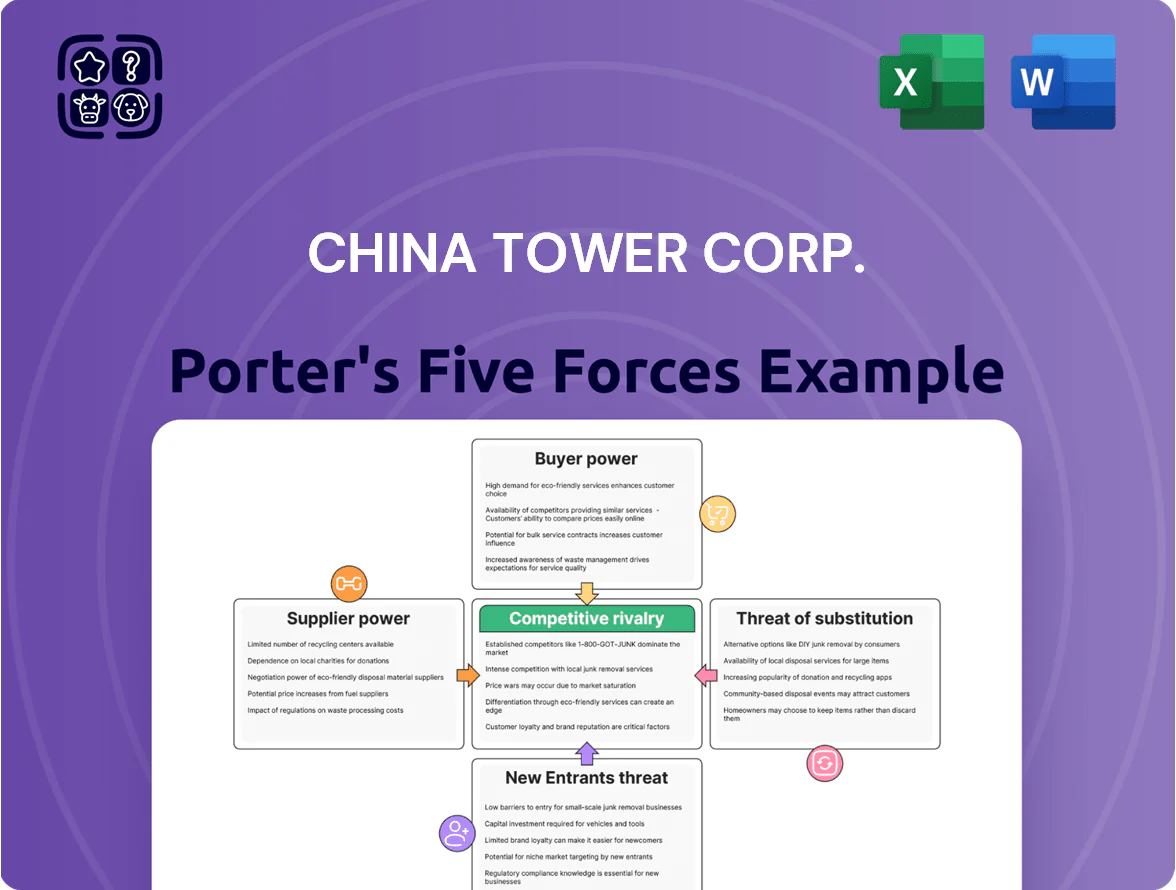

China Tower faces moderate supplier power and high regulatory/customer stickiness, while capital intensity and scale create significant barriers to entry but also limit pricing flexibility; rivalry is intense among infrastructure players vying for tower tenants and 5G rollout contracts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Tower Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Equipment Vendor Market

China Tower depends on a concentrated set of global and domestic vendors for specialized telecom and 5G/6G hardware; in 2024 its top suppliers supplied roughly 70% of equipment spend, creating supplier leverage despite China Tower’s bulk purchases.

Land Access and Leasing Constraints

Suppliers of land—local governments and private owners—exercise strong local bargaining power; in 2024 urban land premiums in top-tier Chinese cities rose ~9% YoY, pushing tower-site lease rates higher.

Rising urban density shrinks suitable siting options, so landowners demand higher rents and stricter terms, increasing site-acquisition costs by an estimated 5–12% per new tower in megacities.

China Tower offsets this via state-backed mandates and long-term leases; as of 2024 over 70% of its sites had multi-year agreements, stabilizing OPEX and capping rent volatility.

Energy and Utility Provider Dependence

Electricity is a major input for China Tower, with power and cooling costs accounting for about 12–15% of operating expenses in 2024; that gives suppliers clear leverage. State-owned utility monopolies in China limit China Tower’s bargaining power, so rate negotiation room is small and price exposure is high. The company has deployed solar, diesel-to-battery shifts, and ~1.4 GW of on-site capacity plus battery storage pilots to cut grid reliance and lower energy spend.

Standardized Procurement Processes

- Centralized procurement cut costs 6–8% (2024)

- RMB 18.3bn common-materials volume (2024)

- Transparent e-tenders reduce supplier leverage

- Specialized tech suppliers remain influential

Labor Market for Specialized Maintenance

Supplier power mixed: bulk buys & multi‑year leases mute telecom vendor leverage

Supplier power is mixed: concentrated telecom vendors and state utilities raise leverage, but centralized procurement, RMB 18.3bn bulk buys (2024) and 70% multi‑year site leases (2024) mute overall pressure; energy and certified-tech labour remain key cost risks (power 12–15% OPEX; wage growth ~7.2% 2025).

| Item | Key metric |

|---|---|

| Top suppliers share | ~70% equipment spend (2024) |

| Materials volume | RMB 18.3bn (2024) |

| Site leases | 70% multi‑year (2024) |

| Energy OPEX | 12–15% (2024) |

| Wage growth | ~7.2% (2025) |

What is included in the product

Tailored exclusively for China Tower Corp., this Porter's Five Forces overview uncovers competitive intensity, customer and supplier power, entry barriers and substitute threats, highlighting regulatory dynamics and infrastructure scale that shape pricing and profitability.

One-sheet Porter’s Five Forces for China Tower—instantly spot regulatory, supplier, and competitive pressures to simplify telecom infrastructure decisions for boards and investors.

Customers Bargaining Power

High Customer Concentration Among the Big Three

The customer base is nearly exclusively China Mobile, China Unicom, and China Telecom—also China Tower’s founding shareholders—giving them outsized bargaining power over pricing and contract terms.

These three carriers accounted for about 95% of China Tower’s 2024 revenue, forcing the towerco to accept low fees and long-term contracts that compress EBITDA margins (China Tower reported a 2024 EBITDA margin near 32%).

The carriers’ collective leverage aligns China Tower with national affordability goals, maintaining high utilization but capping pricing upside and capital return potential.

Commercial Pricing Agreement Influence

Service fees under multi-year Commercial Pricing Agreements (CPAs) are renegotiated periodically between China Tower and major operators, locking in revenue tiers tied to occupancy levels; sharing discounts cut per-operator fees by up to 30% when multiple operators co-locate, lowering average tower ARPU. As of 2025, CPAs favor operators to boost site sharing and cut operator CAPEX, with tower utilization rising—China Tower reporting >1.8 tenants per site and consolidated site rental growth slowing to mid-single digits in 2024. This buyer-friendly pricing keeps customer bargaining power high and limits China Tower’s margin expansion.

Ownership Structure and Strategic Alignment

Because China Tower’s three major customers—China Mobile, China Unicom, and China Telecom—hold about 38% combined equity (reported end-2024), their interests are tied to the towerco’s strategy, blending returns with service cost minimization.

This owner-customer overlap pushes China Tower to balance dividend policy versus capex: in 2024 it paid RMB 6.2bn dividends while capex was RMB 22.5bn, reflecting operators’ preference for lower rental costs.

Switching Costs and Infrastructure Lock-in

Customers exert pricing pressure, but switching is nearly impossible because China Tower controls ~2.3 million towers and site assets across China, creating heavy infrastructure lock-in.

Relocating radios or rebuilding sites would cost operators hundreds of millions RMB and cause service disruption, so they remain captive to long-term colocation contracts.

As a result, China Tower recorded stable tower rental revenue of RMB 63.5 billion in 2024, giving predictable cashflows despite client bargaining power.

- ~2.3M towers nationwide

- RMB 63.5B tower revenue (2024)

- High capex to relocate equipment

Demand for Integrated Information Services

As carriers shift to integrated services like edge computing and environmental monitoring, China Tower can sell value-added offerings that diversify revenue and slightly reduce customers' bargaining power; in 2024 China Tower reported 6.2% growth in value-added service revenue year-on-year, showing early traction.

Still, large operators set technical standards and price ceilings, keeping strong leverage—major carriers account for over 70% of site tenancy, so pricing power remains with them.

- 2024 value-added revenue +6.2%

- Top carriers >70% tenancy

- Operators define standards & price caps

- Integrated services only modestly lower bargaining power

China Tower: Carrier Dominance Drives 95% Revenue, Limits Pricing Power

Major customers (China Mobile, China Unicom, China Telecom) drove ~95% of 2024 revenue, hold ~38% equity, and force low fees via CPAs; China Tower had RMB63.5B revenue, ~32% EBITDA margin, >2.3M towers, >1.8 tenants/site, site rental growth mid-single digits (2024), and value-added revenue +6.2% (2024), so customer bargaining power remains high despite some service diversification.

| Metric | 2024/End‑2024 |

|---|---|

| Revenue (tower) | RMB63.5B |

| EBITDA margin | ~32% |

| Towers | ~2.3M |

| Tenants per site | >1.8 |

| Top carriers revenue share | ~95% |

| Value‑added growth | +6.2% |

Same Document Delivered

China Tower Corp. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of China Tower Corp. you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

The document covers supplier power, buyer power, competitive rivalry, threat of new entrants, and threat of substitutes with sector-specific insights and actionable implications for strategy and valuation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

China Tower faces moderate supplier power and high regulatory/customer stickiness, while capital intensity and scale create significant barriers to entry but also limit pricing flexibility; rivalry is intense among infrastructure players vying for tower tenants and 5G rollout contracts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Tower Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Equipment Vendor Market

China Tower depends on a concentrated set of global and domestic vendors for specialized telecom and 5G/6G hardware; in 2024 its top suppliers supplied roughly 70% of equipment spend, creating supplier leverage despite China Tower’s bulk purchases.

Land Access and Leasing Constraints

Suppliers of land—local governments and private owners—exercise strong local bargaining power; in 2024 urban land premiums in top-tier Chinese cities rose ~9% YoY, pushing tower-site lease rates higher.

Rising urban density shrinks suitable siting options, so landowners demand higher rents and stricter terms, increasing site-acquisition costs by an estimated 5–12% per new tower in megacities.

China Tower offsets this via state-backed mandates and long-term leases; as of 2024 over 70% of its sites had multi-year agreements, stabilizing OPEX and capping rent volatility.

Energy and Utility Provider Dependence

Electricity is a major input for China Tower, with power and cooling costs accounting for about 12–15% of operating expenses in 2024; that gives suppliers clear leverage. State-owned utility monopolies in China limit China Tower’s bargaining power, so rate negotiation room is small and price exposure is high. The company has deployed solar, diesel-to-battery shifts, and ~1.4 GW of on-site capacity plus battery storage pilots to cut grid reliance and lower energy spend.

Standardized Procurement Processes

- Centralized procurement cut costs 6–8% (2024)

- RMB 18.3bn common-materials volume (2024)

- Transparent e-tenders reduce supplier leverage

- Specialized tech suppliers remain influential

Labor Market for Specialized Maintenance

Supplier power mixed: bulk buys & multi‑year leases mute telecom vendor leverage

Supplier power is mixed: concentrated telecom vendors and state utilities raise leverage, but centralized procurement, RMB 18.3bn bulk buys (2024) and 70% multi‑year site leases (2024) mute overall pressure; energy and certified-tech labour remain key cost risks (power 12–15% OPEX; wage growth ~7.2% 2025).

| Item | Key metric |

|---|---|

| Top suppliers share | ~70% equipment spend (2024) |

| Materials volume | RMB 18.3bn (2024) |

| Site leases | 70% multi‑year (2024) |

| Energy OPEX | 12–15% (2024) |

| Wage growth | ~7.2% (2025) |

What is included in the product

Tailored exclusively for China Tower Corp., this Porter's Five Forces overview uncovers competitive intensity, customer and supplier power, entry barriers and substitute threats, highlighting regulatory dynamics and infrastructure scale that shape pricing and profitability.

One-sheet Porter’s Five Forces for China Tower—instantly spot regulatory, supplier, and competitive pressures to simplify telecom infrastructure decisions for boards and investors.

Customers Bargaining Power

High Customer Concentration Among the Big Three

The customer base is nearly exclusively China Mobile, China Unicom, and China Telecom—also China Tower’s founding shareholders—giving them outsized bargaining power over pricing and contract terms.

These three carriers accounted for about 95% of China Tower’s 2024 revenue, forcing the towerco to accept low fees and long-term contracts that compress EBITDA margins (China Tower reported a 2024 EBITDA margin near 32%).

The carriers’ collective leverage aligns China Tower with national affordability goals, maintaining high utilization but capping pricing upside and capital return potential.

Commercial Pricing Agreement Influence

Service fees under multi-year Commercial Pricing Agreements (CPAs) are renegotiated periodically between China Tower and major operators, locking in revenue tiers tied to occupancy levels; sharing discounts cut per-operator fees by up to 30% when multiple operators co-locate, lowering average tower ARPU. As of 2025, CPAs favor operators to boost site sharing and cut operator CAPEX, with tower utilization rising—China Tower reporting >1.8 tenants per site and consolidated site rental growth slowing to mid-single digits in 2024. This buyer-friendly pricing keeps customer bargaining power high and limits China Tower’s margin expansion.

Ownership Structure and Strategic Alignment

Because China Tower’s three major customers—China Mobile, China Unicom, and China Telecom—hold about 38% combined equity (reported end-2024), their interests are tied to the towerco’s strategy, blending returns with service cost minimization.

This owner-customer overlap pushes China Tower to balance dividend policy versus capex: in 2024 it paid RMB 6.2bn dividends while capex was RMB 22.5bn, reflecting operators’ preference for lower rental costs.

Switching Costs and Infrastructure Lock-in

Customers exert pricing pressure, but switching is nearly impossible because China Tower controls ~2.3 million towers and site assets across China, creating heavy infrastructure lock-in.

Relocating radios or rebuilding sites would cost operators hundreds of millions RMB and cause service disruption, so they remain captive to long-term colocation contracts.

As a result, China Tower recorded stable tower rental revenue of RMB 63.5 billion in 2024, giving predictable cashflows despite client bargaining power.

- ~2.3M towers nationwide

- RMB 63.5B tower revenue (2024)

- High capex to relocate equipment

Demand for Integrated Information Services

As carriers shift to integrated services like edge computing and environmental monitoring, China Tower can sell value-added offerings that diversify revenue and slightly reduce customers' bargaining power; in 2024 China Tower reported 6.2% growth in value-added service revenue year-on-year, showing early traction.

Still, large operators set technical standards and price ceilings, keeping strong leverage—major carriers account for over 70% of site tenancy, so pricing power remains with them.

- 2024 value-added revenue +6.2%

- Top carriers >70% tenancy

- Operators define standards & price caps

- Integrated services only modestly lower bargaining power

China Tower: Carrier Dominance Drives 95% Revenue, Limits Pricing Power

Major customers (China Mobile, China Unicom, China Telecom) drove ~95% of 2024 revenue, hold ~38% equity, and force low fees via CPAs; China Tower had RMB63.5B revenue, ~32% EBITDA margin, >2.3M towers, >1.8 tenants/site, site rental growth mid-single digits (2024), and value-added revenue +6.2% (2024), so customer bargaining power remains high despite some service diversification.

| Metric | 2024/End‑2024 |

|---|---|

| Revenue (tower) | RMB63.5B |

| EBITDA margin | ~32% |

| Towers | ~2.3M |

| Tenants per site | >1.8 |

| Top carriers revenue share | ~95% |

| Value‑added growth | +6.2% |

Same Document Delivered

China Tower Corp. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of China Tower Corp. you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

The document covers supplier power, buyer power, competitive rivalry, threat of new entrants, and threat of substitutes with sector-specific insights and actionable implications for strategy and valuation.