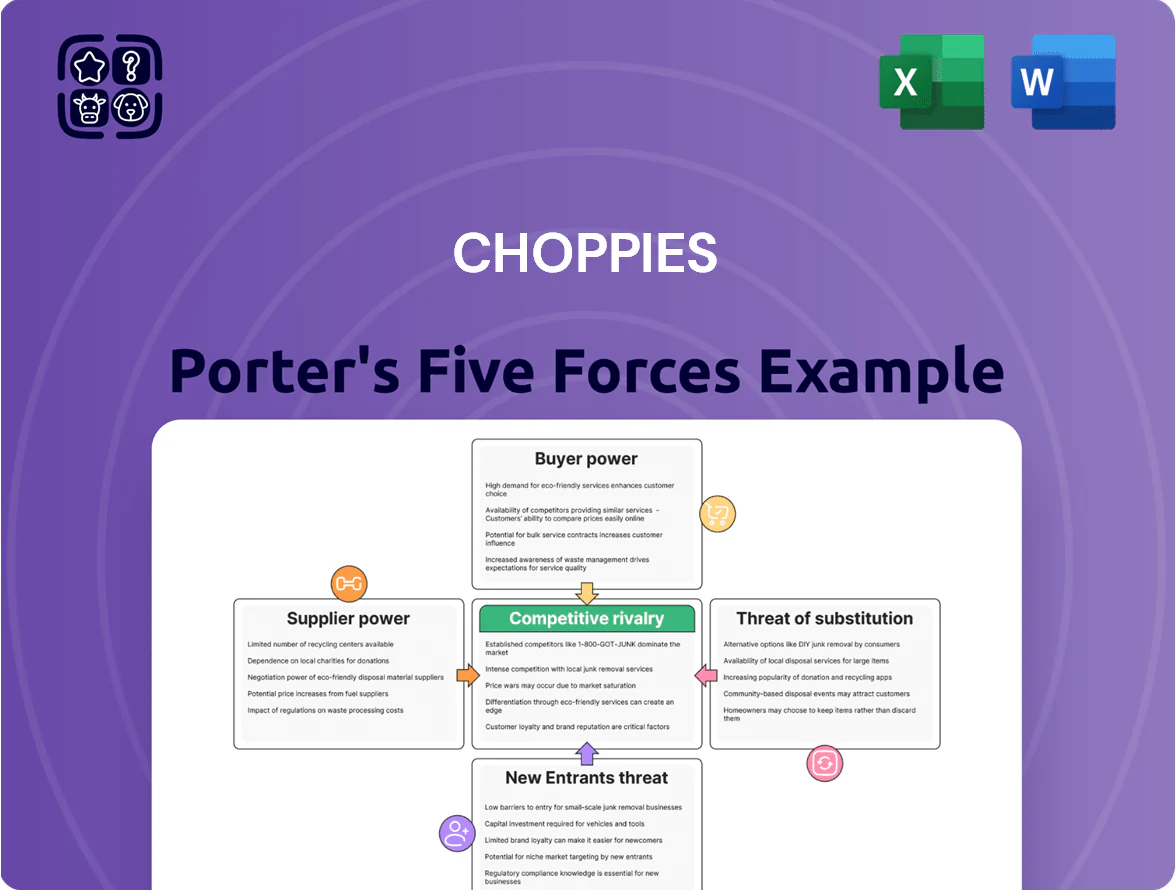

Choppies Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Choppies faces intense buyer pressure, thin margins, and regional supply-chain constraints that shape its competitive stance; this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Choppies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global FMCG Brands

Large multinationals like Nestlé, Unilever and P&G hold strong leverage through brands and must-have SKUs; Choppies sources ≈40–55% of top-selling grocery lines from such suppliers, which drive ~60% of weekly foot traffic. Consolidation continued into late 2025—top 10 FMCG global firms control ~48% of retail CPG revenue—keeping supplier bargaining power high versus regional chains.

Growth of Local Sourcing Initiatives

Choppies has boosted local sourcing in Botswana and Namibia, increasing local supplier spend to an estimated 18% of COGS by 2024, cutting reliance on a few international vendors and lowering freight exposure by ~12% year-over-year.

Partnering with dozens of small farmers improved price negotiation flexibility, reduced single-supplier volume concentration from ~40% to ~25%, and supported regional income—roughly 3,200 local jobs tied to its supply chain.

Volume-Driven Negotiating Leverage

Choppies uses its scale—over 250 stores across Botswana, South Africa, Zimbabwe, Zambia and other SADC markets as of 2025—to extract volume discounts and rebates, securing supplier price cuts often 3–7% per category to protect low margins; suppliers accept lower unit margins to access Choppies’ multi-country distribution and weekly orders exceeding millions of Pula, which blunts supplier power from medium-sized vendors.

Impact of Logistics and Input Costs

Suppliers in Southern Africa faced fuel-led operational cost rises of ~24% between 2021–2024, and 2025 diesel averages near US$1.10/litre, pressuring margins and prompting frequent price pass-throughs to retailers like Choppies.

Choppies’ negotiating leverage is constrained because cutting supplier prices risks stockouts; suppliers owning distribution gain power given rural store density—over 40% of Choppies outlets are in hard-to-reach areas as of 2025.

- Fuel up ~24% rise 2021–24

- Diesel ~US$1.10/litre (2025)

- 40%+ stores remote (2025)

- Supplier-owned logistics = stronger leverage

Backward Vertical Integration

Choppies has moved into packaging and private-label production to reduce COGS; private-label sales rose to about 18% of group sales in FY2024, cutting supplier spend by an estimated 4–6%.

By offering house brands, Choppies credibly threatens external suppliers with lost shelf space, forcing tighter pricing or margins; this capped supplier price increases in groceries to single-digit rises in 2023–24.

- Private-label = 18% of sales FY2024

- Estimated supplier spend cut 4–6%

- Supplier price increases kept to single digits 2023–24

Supplier dominance pressures Choppies—local sourcing & private labels blunt the squeeze

Suppliers hold high power due to global FMCG consolidation (top 10 firms ~48% of CPG revenue, 2025) and must-have SKUs driving ~60% of Choppies footfall, though Choppies cuts exposure with local sourcing (~18% of COGS by 2024), private labels (18% of sales FY2024) and scale discounts (3–7% price cuts). Fuel-driven cost rises (~24% 2021–24; diesel ~US$1.10/litre 2025) force passthroughs, while 40%+ remote stores and supplier-owned logistics limit Choppies’ leverage.

| Metric | Value |

|---|---|

| Top-10 FMCG share (2025) | ~48% |

| Share of footfall from top SKUs | ~60% |

| Local sourcing (COGS, 2024) | ~18% |

| Private-label sales (FY2024) | 18% |

| Volume discount range | 3–7% |

| Fuel cost rise (2021–24) | ~24% |

| Diesel (2025) | ~US$1.10/litre |

| Remote stores (2025) | 40%+ |

What is included in the product

Tailored Porter's Five Forces for Choppies: examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlights disruptive trends and entry barriers shaping the retailer’s pricing, margins, and strategic positioning.

Clear, one-sheet Porter's Five Forces for Choppies—quickly pinpoint supplier, buyer, and competitive pressures to streamline strategy and investor decisions.

Customers Bargaining Power

High Sensitivity to Price Fluctuations

Choppies primary customers are low- to middle-income earners who faced average inflation of about 8.3% in late 2025, so small price moves prompt immediate switching to competitors or informal markets. Even a 3–5% rise on staples cuts volume as shoppers hunt cheaper options, forcing Choppies to keep gross margins near single digits to hold share. This price sensitivity raises churn and squeezes EBITDA, with stores relying on high turnover to offset tight margins.

Minimal Switching Costs for Shoppers

Customers face almost zero switching costs moving from Choppies to rivals like Shoprite or Spar; average urban shoppers in South Africa visit 2.6 supermarkets weekly (2024 NielsenIQ), so choice is easy.

High store density—Johannesburg has 1.2 supermarkets per 10,000 people (2023 StatsSA-linked retail data)—lets consumers cherry-pick deals across brands.

Choppies must run frequent promos; in 2024, grocery loyalty redemption rates averaged 22%, showing rewards help but don’t fully lock in shoppers.

Influence of Digital Price Comparison

In Southern Africa smartphone penetration rose to about 56% by 2025, letting shoppers use price-compare apps and WhatsApp groups to check Choppies against Shoprite and Pick n Pay in real time.

Digital flyers and social media became standard by end-2025, with 62% of grocery buyers citing them for deal discovery, amplifying price transparency.

That transparency shifts leverage: consumers can demand lower prices or switch retailers quickly, squeezing Choppies’ margin on price-sensitive SKUs.

Demand for Value-Added Services

Modern shoppers expect more than low prices; 2024 South African retail surveys show 62% value in-store services like banking and bill payments, pushing Choppies to add these to retain traffic.

Choppies must invest in POS banking, utility kiosks, and mobile integration—failure lets tech-savvy rivals with higher basket frequency capture customers; Choppies’ 2023-24 footprint saw exits cost stores up to 8% same-store sales.

- 62% of consumers want in-store services

- Invest in POS banking, utility kiosks, mobile pay

- Missing services can cut SSS by ~8%

Growth of Private Label Acceptance

- Private-label share: 17% global, ~22% Africa (2024)

- 34% of buyers switch if quality poor

- 2% quality drop → 0.5–1.0 pp EBITDA loss

Price-sensitive shoppers, loyalty fragile: 3–5% price hikes slash volumes, hurt EBITDA

Customers have high price sensitivity and near-zero switching costs, amplified by 56% smartphone penetration and real-time price checks; a 3–5% staple price rise cuts volume and squeezes EBITDA. Frequent promotions and 22% loyalty redemption limit stickiness; missing in-store services can cut same-store sales ~8%. Private labels (17% global, ~22% Africa) pressure margins—34% switchback if quality falls, a 2% quality drop can cost 0.5–1.0 pp EBITDA.

| Metric | Value |

|---|---|

| Smartphone penetration (2025) | 56% |

| Staple price sensitivity | 3–5% → volume drop |

| Loyalty redemption (2024) | 22% |

| Store density (Joburg, 2023) | 1.2/10,000 |

| Private-label share (Africa, 2024) | ~22% |

| Switchback if quality poor | 34% |

| SSS loss if services missing | ~8% |

| EBITDA impact (2% quality drop) | 0.5–1.0 pp |

What You See Is What You Get

Choppies Porter's Five Forces Analysis

This preview shows the exact Choppies Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is part of the full version and is identical to the file available for instant download once you complete your purchase.

You’re viewing the final, professionally written deliverable; after payment you’ll get immediate access to this same complete analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Choppies faces intense buyer pressure, thin margins, and regional supply-chain constraints that shape its competitive stance; this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Choppies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global FMCG Brands

Large multinationals like Nestlé, Unilever and P&G hold strong leverage through brands and must-have SKUs; Choppies sources ≈40–55% of top-selling grocery lines from such suppliers, which drive ~60% of weekly foot traffic. Consolidation continued into late 2025—top 10 FMCG global firms control ~48% of retail CPG revenue—keeping supplier bargaining power high versus regional chains.

Growth of Local Sourcing Initiatives

Choppies has boosted local sourcing in Botswana and Namibia, increasing local supplier spend to an estimated 18% of COGS by 2024, cutting reliance on a few international vendors and lowering freight exposure by ~12% year-over-year.

Partnering with dozens of small farmers improved price negotiation flexibility, reduced single-supplier volume concentration from ~40% to ~25%, and supported regional income—roughly 3,200 local jobs tied to its supply chain.

Volume-Driven Negotiating Leverage

Choppies uses its scale—over 250 stores across Botswana, South Africa, Zimbabwe, Zambia and other SADC markets as of 2025—to extract volume discounts and rebates, securing supplier price cuts often 3–7% per category to protect low margins; suppliers accept lower unit margins to access Choppies’ multi-country distribution and weekly orders exceeding millions of Pula, which blunts supplier power from medium-sized vendors.

Impact of Logistics and Input Costs

Suppliers in Southern Africa faced fuel-led operational cost rises of ~24% between 2021–2024, and 2025 diesel averages near US$1.10/litre, pressuring margins and prompting frequent price pass-throughs to retailers like Choppies.

Choppies’ negotiating leverage is constrained because cutting supplier prices risks stockouts; suppliers owning distribution gain power given rural store density—over 40% of Choppies outlets are in hard-to-reach areas as of 2025.

- Fuel up ~24% rise 2021–24

- Diesel ~US$1.10/litre (2025)

- 40%+ stores remote (2025)

- Supplier-owned logistics = stronger leverage

Backward Vertical Integration

Choppies has moved into packaging and private-label production to reduce COGS; private-label sales rose to about 18% of group sales in FY2024, cutting supplier spend by an estimated 4–6%.

By offering house brands, Choppies credibly threatens external suppliers with lost shelf space, forcing tighter pricing or margins; this capped supplier price increases in groceries to single-digit rises in 2023–24.

- Private-label = 18% of sales FY2024

- Estimated supplier spend cut 4–6%

- Supplier price increases kept to single digits 2023–24

Supplier dominance pressures Choppies—local sourcing & private labels blunt the squeeze

Suppliers hold high power due to global FMCG consolidation (top 10 firms ~48% of CPG revenue, 2025) and must-have SKUs driving ~60% of Choppies footfall, though Choppies cuts exposure with local sourcing (~18% of COGS by 2024), private labels (18% of sales FY2024) and scale discounts (3–7% price cuts). Fuel-driven cost rises (~24% 2021–24; diesel ~US$1.10/litre 2025) force passthroughs, while 40%+ remote stores and supplier-owned logistics limit Choppies’ leverage.

| Metric | Value |

|---|---|

| Top-10 FMCG share (2025) | ~48% |

| Share of footfall from top SKUs | ~60% |

| Local sourcing (COGS, 2024) | ~18% |

| Private-label sales (FY2024) | 18% |

| Volume discount range | 3–7% |

| Fuel cost rise (2021–24) | ~24% |

| Diesel (2025) | ~US$1.10/litre |

| Remote stores (2025) | 40%+ |

What is included in the product

Tailored Porter's Five Forces for Choppies: examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlights disruptive trends and entry barriers shaping the retailer’s pricing, margins, and strategic positioning.

Clear, one-sheet Porter's Five Forces for Choppies—quickly pinpoint supplier, buyer, and competitive pressures to streamline strategy and investor decisions.

Customers Bargaining Power

High Sensitivity to Price Fluctuations

Choppies primary customers are low- to middle-income earners who faced average inflation of about 8.3% in late 2025, so small price moves prompt immediate switching to competitors or informal markets. Even a 3–5% rise on staples cuts volume as shoppers hunt cheaper options, forcing Choppies to keep gross margins near single digits to hold share. This price sensitivity raises churn and squeezes EBITDA, with stores relying on high turnover to offset tight margins.

Minimal Switching Costs for Shoppers

Customers face almost zero switching costs moving from Choppies to rivals like Shoprite or Spar; average urban shoppers in South Africa visit 2.6 supermarkets weekly (2024 NielsenIQ), so choice is easy.

High store density—Johannesburg has 1.2 supermarkets per 10,000 people (2023 StatsSA-linked retail data)—lets consumers cherry-pick deals across brands.

Choppies must run frequent promos; in 2024, grocery loyalty redemption rates averaged 22%, showing rewards help but don’t fully lock in shoppers.

Influence of Digital Price Comparison

In Southern Africa smartphone penetration rose to about 56% by 2025, letting shoppers use price-compare apps and WhatsApp groups to check Choppies against Shoprite and Pick n Pay in real time.

Digital flyers and social media became standard by end-2025, with 62% of grocery buyers citing them for deal discovery, amplifying price transparency.

That transparency shifts leverage: consumers can demand lower prices or switch retailers quickly, squeezing Choppies’ margin on price-sensitive SKUs.

Demand for Value-Added Services

Modern shoppers expect more than low prices; 2024 South African retail surveys show 62% value in-store services like banking and bill payments, pushing Choppies to add these to retain traffic.

Choppies must invest in POS banking, utility kiosks, and mobile integration—failure lets tech-savvy rivals with higher basket frequency capture customers; Choppies’ 2023-24 footprint saw exits cost stores up to 8% same-store sales.

- 62% of consumers want in-store services

- Invest in POS banking, utility kiosks, mobile pay

- Missing services can cut SSS by ~8%

Growth of Private Label Acceptance

- Private-label share: 17% global, ~22% Africa (2024)

- 34% of buyers switch if quality poor

- 2% quality drop → 0.5–1.0 pp EBITDA loss

Price-sensitive shoppers, loyalty fragile: 3–5% price hikes slash volumes, hurt EBITDA

Customers have high price sensitivity and near-zero switching costs, amplified by 56% smartphone penetration and real-time price checks; a 3–5% staple price rise cuts volume and squeezes EBITDA. Frequent promotions and 22% loyalty redemption limit stickiness; missing in-store services can cut same-store sales ~8%. Private labels (17% global, ~22% Africa) pressure margins—34% switchback if quality falls, a 2% quality drop can cost 0.5–1.0 pp EBITDA.

| Metric | Value |

|---|---|

| Smartphone penetration (2025) | 56% |

| Staple price sensitivity | 3–5% → volume drop |

| Loyalty redemption (2024) | 22% |

| Store density (Joburg, 2023) | 1.2/10,000 |

| Private-label share (Africa, 2024) | ~22% |

| Switchback if quality poor | 34% |

| SSS loss if services missing | ~8% |

| EBITDA impact (2% quality drop) | 0.5–1.0 pp |

What You See Is What You Get

Choppies Porter's Five Forces Analysis

This preview shows the exact Choppies Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is part of the full version and is identical to the file available for instant download once you complete your purchase.

You’re viewing the final, professionally written deliverable; after payment you’ll get immediate access to this same complete analysis.