CHS Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

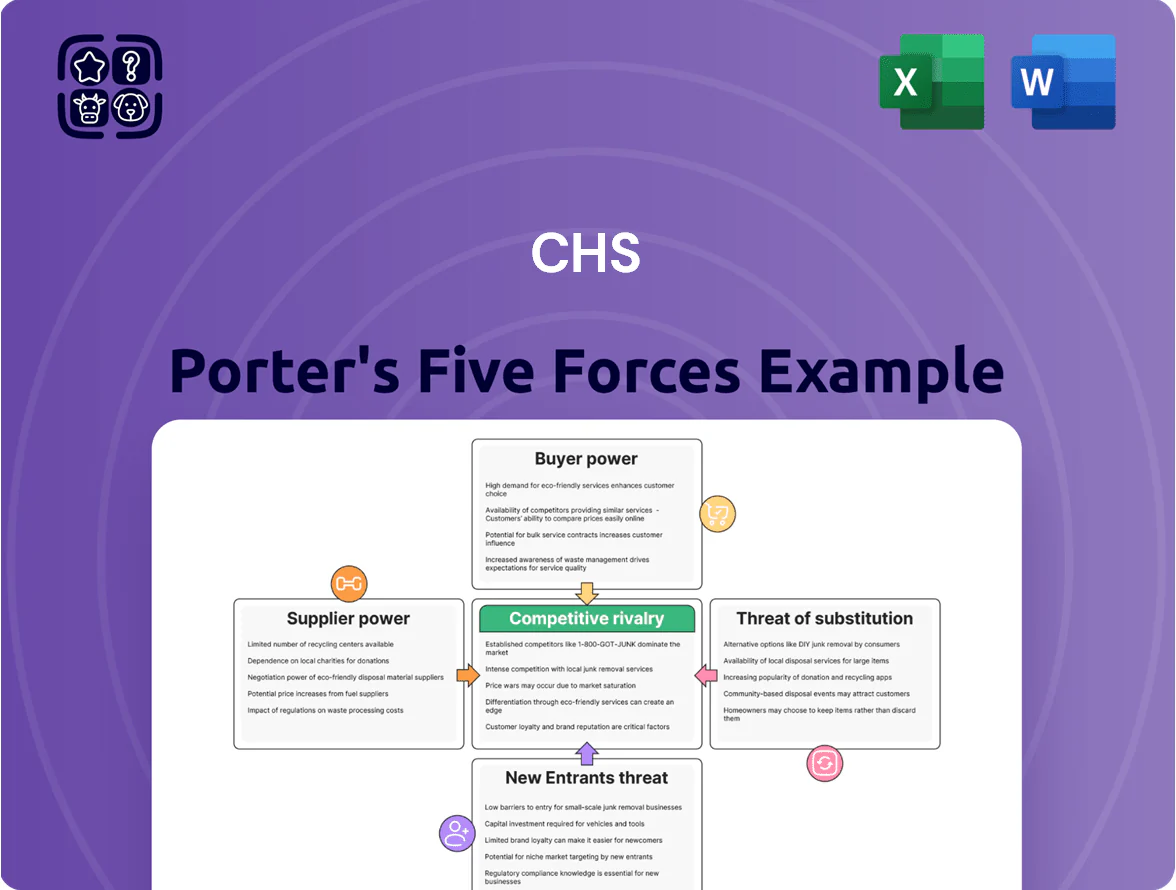

CHS faces mixed competitive pressure: strong buyer concentration and regulatory oversight elevate bargaining challenges, while supplier ties and high capital needs limit new entrants—yet scale and diversified services bolster CHS’s resilience. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CHS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Global Energy Feedstocks

CHS, as a major refiner/distributor, is highly exposed to crude oil and natural gas price swings; Brent averaged 84 USD/barrel in 2025 YTD and Henry Hub gas was ~3.5 USD/MMBtu, tightening CHS’s input costs.

Geopolitical tensions and OPEC+ cuts since late 2024 have constrained supply, limiting CHS’s ability to negotiate lower prices and keeping supplier leverage high.

Concentration of Fertilizer Raw Materials

Fertilizer production depends on potash, phosphate and nitrogen, markets dominated by a few players: Nutrien, Mosaic, and Yara hold roughly 55–65% of global potash/phosphate capacity as of 2024, so CHS faces suppliers that can set terms during demand spikes. In 2022–24, fertilizer prices surged 40–80% at peaks, showing how concentration forces CHS into price-taking behavior. This supplier power compresses CHS margins and increases procurement risk during planting seasons.

Reliance on Member-Owner Grain Supply

A unique strength for CHS is its member-owner grain origination, giving a loyal base; in 2024 CHS sourced roughly 25% of its grain from cooperative members, which stabilizes supply.

That loyalty depends on competitive payouts—if CHS lags local cash bids (farm-gate premiums averaged $0.05–$0.12/bushel in 2024), members can sell elsewhere.

When members shift to direct-to-consumer or local buyers, CHS faces internal supply pressure that can raise procurement costs and reduce throughput.

Logistical and Transportation Constraints

Suppliers of rail, barge, and trucking services strongly influence CHS’s commodity flow; in 2024 Class I railroads handled ~70% of U.S. rail freight, leaving CHS few alternatives when rates rise.

With just six Class I U.S. railroads and specialized inland barges, a 10–20% spike in freight rates or a week-long disruption can raise CHS’s logistics costs materially versus margins.

Disruptions in rail/river corridors in 2023–24 caused grain basis volatility up to $0.50–$1.00/bushel, costs hard to offset through commodity spreads.

- Six Class I railroads limit options

- Rail handles ~70% U.S. freight (2024)

- Freight shocks can raise costs 10–20%

- Basis swings $0.50–$1.00/bushel in 2023–24

Technological and Seed Patent Dominance

In crop sciences, biotech firms like Bayer and Corteva held over 60% of global patented seed traits by 2024, leaving CHS as a distributor with limited leverage over pricing and supply terms.

This IP concentration forces CHS to rely on a few vendors to offer hybrid and traited seeds, exposing farmer-owners to margin pressure and supply risk if patents or royalties shift.

- 60%+ patented trait share (2024)

- High vendor dependency for product portfolio

- Limited bargaining on price/royalties

- Supply risk affects farmer-owner margins

Supplier power & market concentration squeeze CHS margins despite member grain, fragile logistics

Suppliers exert high bargaining power: oil/gas price swings (Brent ~84 USD/bbl 2025 YTD; Henry Hub ~3.5 USD/MMBtu) and concentrated fertilizer/seed markets (Nutrien/Mosaic/Yara ~55–65% potash/phosphate; Bayer/Corteva >60% patented traits) compress CHS margins, while member-origin grain (≈25% in 2024) and limited logistics options (six Class I railroads; rail ~70% freight) partially mitigate but remain fragile.

| Metric | Value |

|---|---|

| Brent (2025 YTD) | 84 USD/bbl |

| Henry Hub (2025 YTD) | 3.5 USD/MMBtu |

| Fertilizer share (2024) | 55–65% |

| Seed trait share (2024) | >60% |

| Grain from members (2024) | ≈25% |

| US rail freight (2024) | ~70% |

What is included in the product

Tailored Porter's Five Forces for CHS, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market position, with strategic insights to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for CHS that highlights competitive threats and relief strategies—ideal for fast boardroom decisions and investor briefs.

Customers Bargaining Power

Consolidation of Global Food Processors

Price Sensitivity of Independent Farmers

Independent farmer-owners operate on thin margins—US farm cash receipts per operator averaged about $102,000 in 2024 while net farm income fell 6% year-over-year—so they are highly price sensitive to inputs like fuel and fertilizer.

If CHS fails to match local retailer prices, farmers will shift purchases to protect margins; in 2024, 23% of ag retailers reported lost volume to lower-priced competitors.

That pressure forces CHS to run at high efficiency—its 2024 retail gross margin target near 12% reflects this need to stay price-competitive.

Access to Real-Time Market Information

Modern digital platforms give CHS customers instant global commodity prices and supply-chain visibility; 2024 AgriTech reports show 68% of grain buyers use real-time pricing apps, shrinking information asymmetry and lifting buyer negotiating power. With spot data and competitor quotes, purchasers extract tighter margins—industry-wide farm-retail price spreads fell 12% from 2020–24—so CHS must bundle analytics, logistics and credit services to retain loyalty in an informed market.

Low Switching Costs for Energy Products

Low switching costs in refined fuels and propane mean customers often choose price and delivery over brand; CHS lost market share to regional suppliers in 2024 where spot diesel spreads hit as low as $0.05/gal, pushing margins down.

Commoditization makes loyalty weak—energy volumes are price-sensitive and 70% of regional commercial accounts cited delivery reliability as top factor in a 2023 survey, so CHS must match local coop and private-firm pricing.

- Price-driven buying: spot spreads ≈ $0.05/gal (2024)

- Reliability key: 70% of accounts prioritize delivery (2023)

- Competition: regional coops/private firms erode share

Growth of Direct-to-Consumer Grain Sales

Advancements in logistics and digital marketplaces let large growers bypass aggregators like CHS, raising producer-customer bargaining power as sellers access more buyers; in 2024 digital grain bids grew ~18% in North America, shifting volume away from traditional channels.

CHS must boost origination incentives and expand global reach—adding price risk tools and freight contracts—to retain large accounts; failure risks lower margins and lost volumes (CHS procured 18.4M tonnes in 2023).

- Digital bids +18% (2024)

- CHS procured 18.4M tonnes (2023)

- Need: stronger origination incentives

- Need: expanded freight/global access

CHS must boost origination, freight access & services as buyers tighten spreads

| Metric | Value |

|---|---|

| Top-10 buyer share | ≈40% (end-2025) |

| CHS procured | 18.4M tonnes (2023) |

| Digital bids growth | +18% (2024) |

| Real-time pricing users | 68% (2024) |

| Compliance cost impact | ~1–2% gross margin |

Preview the Actual Deliverable

CHS Porter's Five Forces Analysis

This preview shows the exact CHS Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for use with no placeholders or mockups.

The document displayed here is the same professionally written file you'll be able to download instantly after payment, containing the full Five Forces assessment, key implications, and strategic insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

CHS faces mixed competitive pressure: strong buyer concentration and regulatory oversight elevate bargaining challenges, while supplier ties and high capital needs limit new entrants—yet scale and diversified services bolster CHS’s resilience. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CHS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Global Energy Feedstocks

CHS, as a major refiner/distributor, is highly exposed to crude oil and natural gas price swings; Brent averaged 84 USD/barrel in 2025 YTD and Henry Hub gas was ~3.5 USD/MMBtu, tightening CHS’s input costs.

Geopolitical tensions and OPEC+ cuts since late 2024 have constrained supply, limiting CHS’s ability to negotiate lower prices and keeping supplier leverage high.

Concentration of Fertilizer Raw Materials

Fertilizer production depends on potash, phosphate and nitrogen, markets dominated by a few players: Nutrien, Mosaic, and Yara hold roughly 55–65% of global potash/phosphate capacity as of 2024, so CHS faces suppliers that can set terms during demand spikes. In 2022–24, fertilizer prices surged 40–80% at peaks, showing how concentration forces CHS into price-taking behavior. This supplier power compresses CHS margins and increases procurement risk during planting seasons.

Reliance on Member-Owner Grain Supply

A unique strength for CHS is its member-owner grain origination, giving a loyal base; in 2024 CHS sourced roughly 25% of its grain from cooperative members, which stabilizes supply.

That loyalty depends on competitive payouts—if CHS lags local cash bids (farm-gate premiums averaged $0.05–$0.12/bushel in 2024), members can sell elsewhere.

When members shift to direct-to-consumer or local buyers, CHS faces internal supply pressure that can raise procurement costs and reduce throughput.

Logistical and Transportation Constraints

Suppliers of rail, barge, and trucking services strongly influence CHS’s commodity flow; in 2024 Class I railroads handled ~70% of U.S. rail freight, leaving CHS few alternatives when rates rise.

With just six Class I U.S. railroads and specialized inland barges, a 10–20% spike in freight rates or a week-long disruption can raise CHS’s logistics costs materially versus margins.

Disruptions in rail/river corridors in 2023–24 caused grain basis volatility up to $0.50–$1.00/bushel, costs hard to offset through commodity spreads.

- Six Class I railroads limit options

- Rail handles ~70% U.S. freight (2024)

- Freight shocks can raise costs 10–20%

- Basis swings $0.50–$1.00/bushel in 2023–24

Technological and Seed Patent Dominance

In crop sciences, biotech firms like Bayer and Corteva held over 60% of global patented seed traits by 2024, leaving CHS as a distributor with limited leverage over pricing and supply terms.

This IP concentration forces CHS to rely on a few vendors to offer hybrid and traited seeds, exposing farmer-owners to margin pressure and supply risk if patents or royalties shift.

- 60%+ patented trait share (2024)

- High vendor dependency for product portfolio

- Limited bargaining on price/royalties

- Supply risk affects farmer-owner margins

Supplier power & market concentration squeeze CHS margins despite member grain, fragile logistics

Suppliers exert high bargaining power: oil/gas price swings (Brent ~84 USD/bbl 2025 YTD; Henry Hub ~3.5 USD/MMBtu) and concentrated fertilizer/seed markets (Nutrien/Mosaic/Yara ~55–65% potash/phosphate; Bayer/Corteva >60% patented traits) compress CHS margins, while member-origin grain (≈25% in 2024) and limited logistics options (six Class I railroads; rail ~70% freight) partially mitigate but remain fragile.

| Metric | Value |

|---|---|

| Brent (2025 YTD) | 84 USD/bbl |

| Henry Hub (2025 YTD) | 3.5 USD/MMBtu |

| Fertilizer share (2024) | 55–65% |

| Seed trait share (2024) | >60% |

| Grain from members (2024) | ≈25% |

| US rail freight (2024) | ~70% |

What is included in the product

Tailored Porter's Five Forces for CHS, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market position, with strategic insights to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for CHS that highlights competitive threats and relief strategies—ideal for fast boardroom decisions and investor briefs.

Customers Bargaining Power

Consolidation of Global Food Processors

Price Sensitivity of Independent Farmers

Independent farmer-owners operate on thin margins—US farm cash receipts per operator averaged about $102,000 in 2024 while net farm income fell 6% year-over-year—so they are highly price sensitive to inputs like fuel and fertilizer.

If CHS fails to match local retailer prices, farmers will shift purchases to protect margins; in 2024, 23% of ag retailers reported lost volume to lower-priced competitors.

That pressure forces CHS to run at high efficiency—its 2024 retail gross margin target near 12% reflects this need to stay price-competitive.

Access to Real-Time Market Information

Modern digital platforms give CHS customers instant global commodity prices and supply-chain visibility; 2024 AgriTech reports show 68% of grain buyers use real-time pricing apps, shrinking information asymmetry and lifting buyer negotiating power. With spot data and competitor quotes, purchasers extract tighter margins—industry-wide farm-retail price spreads fell 12% from 2020–24—so CHS must bundle analytics, logistics and credit services to retain loyalty in an informed market.

Low Switching Costs for Energy Products

Low switching costs in refined fuels and propane mean customers often choose price and delivery over brand; CHS lost market share to regional suppliers in 2024 where spot diesel spreads hit as low as $0.05/gal, pushing margins down.

Commoditization makes loyalty weak—energy volumes are price-sensitive and 70% of regional commercial accounts cited delivery reliability as top factor in a 2023 survey, so CHS must match local coop and private-firm pricing.

- Price-driven buying: spot spreads ≈ $0.05/gal (2024)

- Reliability key: 70% of accounts prioritize delivery (2023)

- Competition: regional coops/private firms erode share

Growth of Direct-to-Consumer Grain Sales

Advancements in logistics and digital marketplaces let large growers bypass aggregators like CHS, raising producer-customer bargaining power as sellers access more buyers; in 2024 digital grain bids grew ~18% in North America, shifting volume away from traditional channels.

CHS must boost origination incentives and expand global reach—adding price risk tools and freight contracts—to retain large accounts; failure risks lower margins and lost volumes (CHS procured 18.4M tonnes in 2023).

- Digital bids +18% (2024)

- CHS procured 18.4M tonnes (2023)

- Need: stronger origination incentives

- Need: expanded freight/global access

CHS must boost origination, freight access & services as buyers tighten spreads

| Metric | Value |

|---|---|

| Top-10 buyer share | ≈40% (end-2025) |

| CHS procured | 18.4M tonnes (2023) |

| Digital bids growth | +18% (2024) |

| Real-time pricing users | 68% (2024) |

| Compliance cost impact | ~1–2% gross margin |

Preview the Actual Deliverable

CHS Porter's Five Forces Analysis

This preview shows the exact CHS Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for use with no placeholders or mockups.

The document displayed here is the same professionally written file you'll be able to download instantly after payment, containing the full Five Forces assessment, key implications, and strategic insights.