CHS PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

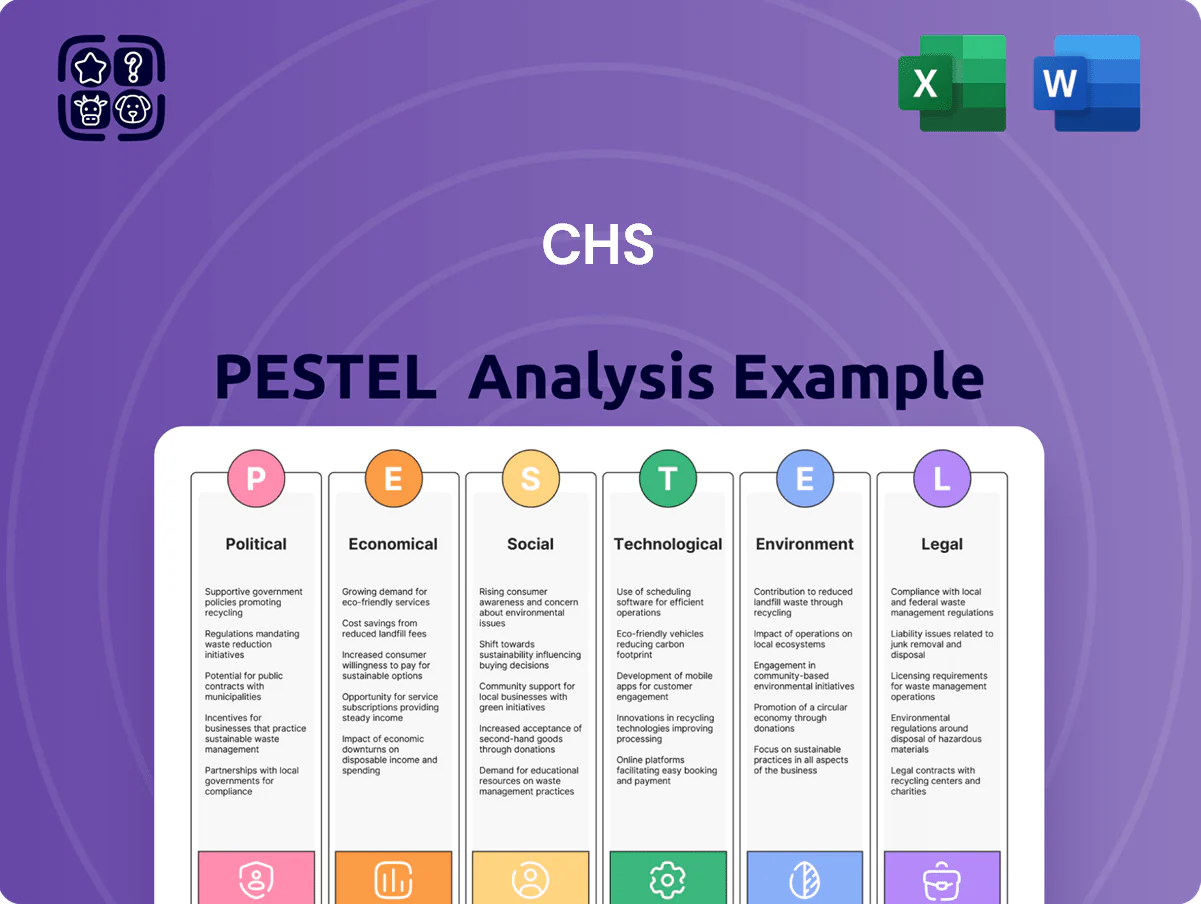

Unlock strategic clarity with our PESTLE Analysis of CHS—spot political, economic, and technological forces shaping its trajectory and turn those insights into competitive advantage; purchase the full report for a downloadable, ready-to-use deep dive that’s ideal for investors, consultants, and planners.

Political factors

Global Trade Policy and Tariffs

As of late 2025, U.S.-China agricultural trade remains pivotal for CHS; China imported about 37 million tonnes of U.S. soybeans in 2024-25, and any new tariffs could reduce export volumes by an estimated 10–20%, cutting exporter revenues materially.

U.S. Farm Bill Legislation

The ongoing implementation of the 2023 Farm Bill, which authorized about $50 billion annually in commodity and conservation programs, directly shapes subsidies, crop insurance and conservation incentives for CHS member-owners; USDA data show federal crop insurance indemnities averaged $12.5 billion per year (2021–2023), providing a safety net that stabilizes farmer cash flows and CHS revenues. Legislative delays or funding shifts in Washington can quickly reduce planting intensity and input purchases, cutting cooperative sales and working capital needs.

Geopolitical Stability in Energy Corridors

CHS faces heightened risk from geopolitical instability in energy corridors given its 2024 refinery throughput exposure of ~180 kbpd and 2025 fuel distribution revenue of $6.2bn; conflicts or shipping disruptions can swing refined-product margins by ±$10–$25/barrel, amplifying earnings volatility. Government moves on strategic petroleum reserves and export licenses—e.g., U.S. SPR releases of 180m barrels since 2022—directly affect CHS midstream utilization and freight costs.

Biofuel Mandates and RFS Standards

Federal political support for the Renewable Fuel Standard (RFS) underpins demand for corn ethanol and soybean biodiesel; in 2024 RFS volumes targeted ~15.8 billion gallons of corn ethanol and 2.76 billion gallons of advanced biofuels, supporting CHS revenue exposure in biofuels and feed markets.

CHS depends on consistent blending mandates—about 13% of U.S. gasoline use was ethanol in 2023—so any rollback of RFS targets could reduce utilization of CHS-owned ethanol plants and biodiesel supply contracts, pressuring margins.

A political shift reducing mandates would materially hit profitability: the U.S. EPA estimated RIN market values averaged $0.70–$1.20/gal in 2023–2024, and lower mandates could compress those credits and CHS renewable returns.

- 2024 RFS: ~15.8B gal corn ethanol, 2.76B gal advanced

- Ethanol share ~13% of U.S. gasoline (2023)

- RIN prices averaged $0.70–$1.20/gal (2023–2024)

- Mandate reductions = lower plant utilization, compressed margins

International Regulatory Alignment

Operating across 70+ countries, CHS faces divergent political standards on food safety and chemical use, with the EU proposing restrictions that could cut certain pesticide markets by an estimated 10–15% of global volumes by 2025.

Political pressure to ban specific fertilizers and pesticides forces CHS to shift R&D and inventory, impacting FY2024 nutrient sales mix where specialty nutrients rose to 22% of product revenue.

Maintaining multi-jurisdiction compliance raises logistics costs and risk; regulatory-driven supply chain changes contributed to a 3.2% rise in FY2024 SG&A for compliance and traceability systems.

- Operates in 70+ countries; EU restrictions may reduce some pesticide markets 10–15% by 2025

- Specialty nutrients = 22% of product revenue in FY2024

- Regulatory compliance added ~3.2% to FY2024 SG&A

CHS: Soy, Farm Bill & RFS Stabilize Revenues; EU Rules Lift Costs, Biofuels Boost Margins

U.S.-China trade (37 Mt US soybeans 2024–25) and the 2023 Farm Bill (~$50bn/yr) stabilize CHS revenues; energy/geopolitics affect 2024 refinery throughput (~180 kbpd) and $6.2bn 2025 fuel revenue; RFS (15.8B gal corn ethanol, 2.76B gal advanced 2024) and RINs ($0.70–$1.20/gal) support biofuel margins; EU pesticide limits (‑10–15% market) and 22% specialty nutrient revenue raise compliance costs (~3.2% SG&A uptick).

| Factor | Key Data |

|---|---|

| China soy | 37 Mt (2024–25) |

| Farm Bill | $50bn/yr |

| Refinery | ~180 kbpd throughput |

| Fuel rev | $6.2bn (2025) |

| RFS | 15.8B gal corn; 2.76B advanced (2024) |

| RINs | $0.70–$1.20/gal (2023–24) |

| EU pesticide impact | ‑10–15% market by 2025 |

| Specialty nutrients | 22% revenue (FY2024) |

| Compliance cost | ~3.2% SG&A increase (FY2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect CHS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary for CHS that streamlines external risk discussions and can be dropped into presentations or planning decks for quick team alignment.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, the high U.S. Fed funds path—peaking near 5.25%–5.50% in 2024 and easing to ~4.75% by late 2025—keeps CHS and farmer-owners facing elevated borrowing costs; U.S. farm operating loan rates averaged ~6.5%–7.5% in 2024, raising financing costs for equipment and inputs.

If rates stabilize or fall toward 4.5%–5.0% in 2025, modeled capex uptake could rise 8%–12% across cooperatives as lower rates cut weighted average cost of capital and support expansion of storage, processing, and precision-ag equipment.

Volatility in Commodity Pricing

Fluctuations in corn, soybean, wheat and crude oil prices directly impact CHS revenue—U.S. corn fell ~18% in 2024 while Brent averaged $86/bbl in 2024, widening input cost swings for agribulk margins.

Global supply-demand imbalances from 2023–25 weather shocks and rising feed demand in Asia created sharper price variance, compressing CHS feed and grain margins in FY2024.

CHS’s hedging and risk-management services, which supported $7.5 billion in merchandising volume in 2024, are critical to stabilizing cashflows amid these cyclical swings.

Inflationary Pressure on Input Costs

Persistent inflation raised US PPI for fertilizers and chemical inputs by about 9.8% year-over-year in 2024, increasing CHS procurement costs for fertilizers, crop nutrients and energy products and pressuring gross margins. While farmgate prices for major crops rose roughly 6–12% in 2023–24, higher output prices only partially offset input inflation, squeezing cooperative net margins. CHS must monitor monthly PPI data and the October 2024 3.2% core PPI trend to recalibrate pricing, hedging and supply agreements to remain competitive while protecting profitability.

Currency Exchange Rate Fluctuations

As a major exporter, CHS faces competitiveness pressure when the U.S. dollar strengthens; a 10% USD rise in 2024 correlated with a roughly 4–6% drop in U.S. grain export volumes versus 2023, raising FOB prices for buyers. Economic shifts in competitor currencies—Brazil’s real depreciating ~8% in 2024 and Russia’s ruble volatility—further shift market share toward lower-cost origins.

- USD up 10% in 2024 → US grain exports down ~4–6%

- BRL -8% 2024 → Brazil gains price competitiveness

- Ruble volatility → uncertain Russian export volumes

Labor Market Dynamics in Rural Areas

Labor shortages in rural U.S. areas raise recruitment costs for CHS; rural unemployment fell to 3.1% in 2024 while agricultural skilled-worker vacancies rose 12% year-over-year, pressuring processing plants and distribution centers.

Wage inflation in logistics/manufacturing—average hourly pay up ~5.6% in 2024—adds to overhead, increasing unit costs across CHS supply chains.

CHS needs targeted retention/recruitment investments; a 2024 industry benchmark shows training and retention programs can cut turnover by ~18%, preserving complex operations.

- Rural unemployment 3.1% (2024)

- Skilled-worker vacancies +12% YoY (agriculture, 2024)

- Wage inflation +5.6% avg hourly (logistics/manufacturing, 2024)

- Retention programs can lower turnover ~18% (industry 2024)

Higher rates, weaker crops and stronger USD squeeze CHS margins in 2024

Rising rates (Fed peak ~5.25%–5.50% in 2024; ~4.75% by end-2025) and 2024 farm loan rates ~6.5%–7.5% raised financing costs; crop price swings (corn -18% 2024; Brent ~$86/bbl 2024) compressed agribulk margins; USD +10% 2024 cut US grain exports ~4–6%; rural unemployment 3.1% and skilled vacancies +12% drove wage inflation ~+5.6% (2024), pressuring CHS margins.

| Metric | 2024 |

|---|---|

| Fed peak | 5.25%–5.50% |

| Farm loan rates | 6.5%–7.5% |

| Corn price change | -18% |

| Brent | $86/bbl |

| USD change | +10% |

| Rural unemployment | 3.1% |

| Wage inflation | +5.6% |

Preview the Actual Deliverable

CHS PESTLE Analysis

The preview shown here is the exact CHS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of CHS—spot political, economic, and technological forces shaping its trajectory and turn those insights into competitive advantage; purchase the full report for a downloadable, ready-to-use deep dive that’s ideal for investors, consultants, and planners.

Political factors

Global Trade Policy and Tariffs

As of late 2025, U.S.-China agricultural trade remains pivotal for CHS; China imported about 37 million tonnes of U.S. soybeans in 2024-25, and any new tariffs could reduce export volumes by an estimated 10–20%, cutting exporter revenues materially.

U.S. Farm Bill Legislation

The ongoing implementation of the 2023 Farm Bill, which authorized about $50 billion annually in commodity and conservation programs, directly shapes subsidies, crop insurance and conservation incentives for CHS member-owners; USDA data show federal crop insurance indemnities averaged $12.5 billion per year (2021–2023), providing a safety net that stabilizes farmer cash flows and CHS revenues. Legislative delays or funding shifts in Washington can quickly reduce planting intensity and input purchases, cutting cooperative sales and working capital needs.

Geopolitical Stability in Energy Corridors

CHS faces heightened risk from geopolitical instability in energy corridors given its 2024 refinery throughput exposure of ~180 kbpd and 2025 fuel distribution revenue of $6.2bn; conflicts or shipping disruptions can swing refined-product margins by ±$10–$25/barrel, amplifying earnings volatility. Government moves on strategic petroleum reserves and export licenses—e.g., U.S. SPR releases of 180m barrels since 2022—directly affect CHS midstream utilization and freight costs.

Biofuel Mandates and RFS Standards

Federal political support for the Renewable Fuel Standard (RFS) underpins demand for corn ethanol and soybean biodiesel; in 2024 RFS volumes targeted ~15.8 billion gallons of corn ethanol and 2.76 billion gallons of advanced biofuels, supporting CHS revenue exposure in biofuels and feed markets.

CHS depends on consistent blending mandates—about 13% of U.S. gasoline use was ethanol in 2023—so any rollback of RFS targets could reduce utilization of CHS-owned ethanol plants and biodiesel supply contracts, pressuring margins.

A political shift reducing mandates would materially hit profitability: the U.S. EPA estimated RIN market values averaged $0.70–$1.20/gal in 2023–2024, and lower mandates could compress those credits and CHS renewable returns.

- 2024 RFS: ~15.8B gal corn ethanol, 2.76B gal advanced

- Ethanol share ~13% of U.S. gasoline (2023)

- RIN prices averaged $0.70–$1.20/gal (2023–2024)

- Mandate reductions = lower plant utilization, compressed margins

International Regulatory Alignment

Operating across 70+ countries, CHS faces divergent political standards on food safety and chemical use, with the EU proposing restrictions that could cut certain pesticide markets by an estimated 10–15% of global volumes by 2025.

Political pressure to ban specific fertilizers and pesticides forces CHS to shift R&D and inventory, impacting FY2024 nutrient sales mix where specialty nutrients rose to 22% of product revenue.

Maintaining multi-jurisdiction compliance raises logistics costs and risk; regulatory-driven supply chain changes contributed to a 3.2% rise in FY2024 SG&A for compliance and traceability systems.

- Operates in 70+ countries; EU restrictions may reduce some pesticide markets 10–15% by 2025

- Specialty nutrients = 22% of product revenue in FY2024

- Regulatory compliance added ~3.2% to FY2024 SG&A

CHS: Soy, Farm Bill & RFS Stabilize Revenues; EU Rules Lift Costs, Biofuels Boost Margins

U.S.-China trade (37 Mt US soybeans 2024–25) and the 2023 Farm Bill (~$50bn/yr) stabilize CHS revenues; energy/geopolitics affect 2024 refinery throughput (~180 kbpd) and $6.2bn 2025 fuel revenue; RFS (15.8B gal corn ethanol, 2.76B gal advanced 2024) and RINs ($0.70–$1.20/gal) support biofuel margins; EU pesticide limits (‑10–15% market) and 22% specialty nutrient revenue raise compliance costs (~3.2% SG&A uptick).

| Factor | Key Data |

|---|---|

| China soy | 37 Mt (2024–25) |

| Farm Bill | $50bn/yr |

| Refinery | ~180 kbpd throughput |

| Fuel rev | $6.2bn (2025) |

| RFS | 15.8B gal corn; 2.76B advanced (2024) |

| RINs | $0.70–$1.20/gal (2023–24) |

| EU pesticide impact | ‑10–15% market by 2025 |

| Specialty nutrients | 22% revenue (FY2024) |

| Compliance cost | ~3.2% SG&A increase (FY2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect CHS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary for CHS that streamlines external risk discussions and can be dropped into presentations or planning decks for quick team alignment.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, the high U.S. Fed funds path—peaking near 5.25%–5.50% in 2024 and easing to ~4.75% by late 2025—keeps CHS and farmer-owners facing elevated borrowing costs; U.S. farm operating loan rates averaged ~6.5%–7.5% in 2024, raising financing costs for equipment and inputs.

If rates stabilize or fall toward 4.5%–5.0% in 2025, modeled capex uptake could rise 8%–12% across cooperatives as lower rates cut weighted average cost of capital and support expansion of storage, processing, and precision-ag equipment.

Volatility in Commodity Pricing

Fluctuations in corn, soybean, wheat and crude oil prices directly impact CHS revenue—U.S. corn fell ~18% in 2024 while Brent averaged $86/bbl in 2024, widening input cost swings for agribulk margins.

Global supply-demand imbalances from 2023–25 weather shocks and rising feed demand in Asia created sharper price variance, compressing CHS feed and grain margins in FY2024.

CHS’s hedging and risk-management services, which supported $7.5 billion in merchandising volume in 2024, are critical to stabilizing cashflows amid these cyclical swings.

Inflationary Pressure on Input Costs

Persistent inflation raised US PPI for fertilizers and chemical inputs by about 9.8% year-over-year in 2024, increasing CHS procurement costs for fertilizers, crop nutrients and energy products and pressuring gross margins. While farmgate prices for major crops rose roughly 6–12% in 2023–24, higher output prices only partially offset input inflation, squeezing cooperative net margins. CHS must monitor monthly PPI data and the October 2024 3.2% core PPI trend to recalibrate pricing, hedging and supply agreements to remain competitive while protecting profitability.

Currency Exchange Rate Fluctuations

As a major exporter, CHS faces competitiveness pressure when the U.S. dollar strengthens; a 10% USD rise in 2024 correlated with a roughly 4–6% drop in U.S. grain export volumes versus 2023, raising FOB prices for buyers. Economic shifts in competitor currencies—Brazil’s real depreciating ~8% in 2024 and Russia’s ruble volatility—further shift market share toward lower-cost origins.

- USD up 10% in 2024 → US grain exports down ~4–6%

- BRL -8% 2024 → Brazil gains price competitiveness

- Ruble volatility → uncertain Russian export volumes

Labor Market Dynamics in Rural Areas

Labor shortages in rural U.S. areas raise recruitment costs for CHS; rural unemployment fell to 3.1% in 2024 while agricultural skilled-worker vacancies rose 12% year-over-year, pressuring processing plants and distribution centers.

Wage inflation in logistics/manufacturing—average hourly pay up ~5.6% in 2024—adds to overhead, increasing unit costs across CHS supply chains.

CHS needs targeted retention/recruitment investments; a 2024 industry benchmark shows training and retention programs can cut turnover by ~18%, preserving complex operations.

- Rural unemployment 3.1% (2024)

- Skilled-worker vacancies +12% YoY (agriculture, 2024)

- Wage inflation +5.6% avg hourly (logistics/manufacturing, 2024)

- Retention programs can lower turnover ~18% (industry 2024)

Higher rates, weaker crops and stronger USD squeeze CHS margins in 2024

Rising rates (Fed peak ~5.25%–5.50% in 2024; ~4.75% by end-2025) and 2024 farm loan rates ~6.5%–7.5% raised financing costs; crop price swings (corn -18% 2024; Brent ~$86/bbl 2024) compressed agribulk margins; USD +10% 2024 cut US grain exports ~4–6%; rural unemployment 3.1% and skilled vacancies +12% drove wage inflation ~+5.6% (2024), pressuring CHS margins.

| Metric | 2024 |

|---|---|

| Fed peak | 5.25%–5.50% |

| Farm loan rates | 6.5%–7.5% |

| Corn price change | -18% |

| Brent | $86/bbl |

| USD change | +10% |

| Rural unemployment | 3.1% |

| Wage inflation | +5.6% |

Preview the Actual Deliverable

CHS PESTLE Analysis

The preview shown here is the exact CHS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.