CHS SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

CHS shows resilient market reach and diversified operations but faces margin pressure from commodity volatility and regulatory shifts; its strategic partnerships and scale are strengths, while supply-chain risks and ESG expectations are key vulnerabilities. Want the full picture? Purchase the complete SWOT analysis for a research-backed, editable report and Excel tools to support investment, planning, and presentations.

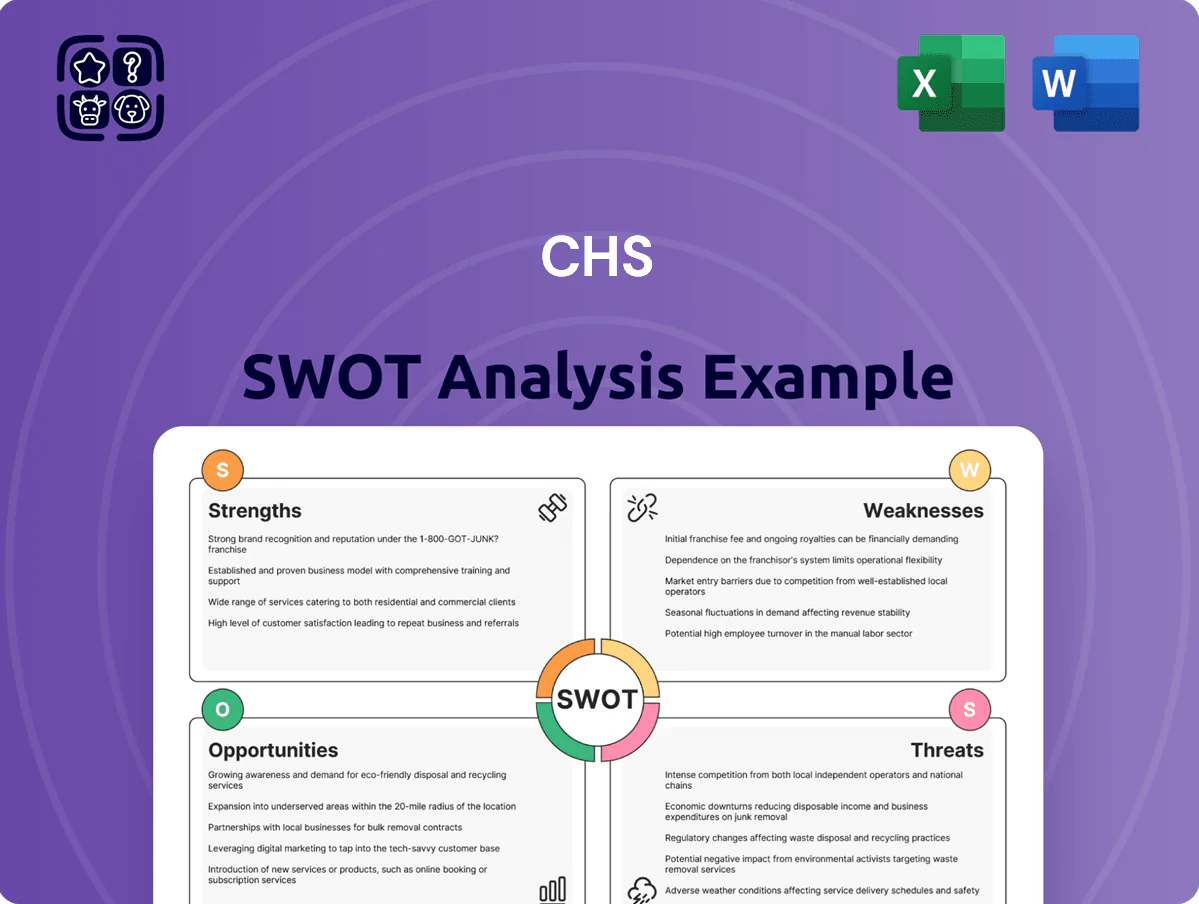

Strengths

Dominant Cooperative Market Position

Integrated Supply Chain Infrastructure

Owning the Cenex brand gives CHS a dominant rural fuel network—roughly 2,000 retail sites—strengthening fuel margins and cross-selling between energy and ag customers.

Diversified Business Portfolio

CHS reduces sector risk by operating in crop nutrients, grain marketing, energy refining, and financial services, generating $49.7 billion in 2024 revenue so losses in one area can be offset by others.

When U.S. corn futures fell 18% in H2 2023, CHS's energy and fertilizer margins helped keep corporate EBITDA around $1.3 billion in 2024, stabilizing cash flow.

Strong Financial Liquidity and Capital Base

- Liquidity: $4.2B (FY 2024)

- Working capital: $1.8B (FY 2024)

- Earnings CAGR: 6.5% (2019–2024)

- Member returns: $220M patronage (2024)

Established Global Export Capabilities

CHS links North American farmers to Asia, Europe and South America, moving ~35% of its 2024 grain exports through owned terminals and long-term port leases, which helps clear domestic surpluses and capture higher FOB prices abroad.

Investments in deep-water ports and eight international marketing offices drove $5.1B in global merchandising revenue in FY2024, improving margin capture on export corridors.

- ~35% export throughput via owned/leased terminals (2024)

- $5.1B global merchandising revenue (FY2024)

- 8 international marketing offices supporting price discovery

CHS: $49.7B scale, $4.2B liquidity, 700k members—$1.2B allocations, resilient EBITDA

| Metric | 2024 |

|---|---|

| Revenue | $49.7B |

| Liquidity | $4.2B |

| Member base | 700,000 |

What is included in the product

Provides a clear SWOT framework for analyzing CHS’s business strategy, highlighting internal capabilities, operational gaps, growth drivers, and external market risks shaping its competitive position and future prospects.

Provides a concise CHS SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations.

Weaknesses

Exposure to Commodity Price Volatility

High Maintenance Costs for Aging Assets

Geographic Concentration in the U.S. Midwest

While CHS Inc. operates globally, about 55% of grain origination and roughly 60% of its member cooperatives are in the U.S. Midwest, concentrating revenue and supply risk in one region.

This dependence raises exposure to Midwest-specific shocks—2012-2013 droughts cut regional output by ~20%, and 2019 Mississippi River low flows cost inland barge operators an estimated $300M, risks that can ripple through CHS’s margins and liquidity.

Complex Cooperative Governance Structure

- 75,000 owners, 1,000+ member co-ops (2024)

- Board/member cycle delays = months

- $1.1B capex 2024; slower ROI risk

- Lower agility vs digital entrants

Dependence on Carbon-Intensive Energy Sectors

A large portion of CHS revenue comes from fossil fuel refining and nitrogen fertilizer; in 2024 these segments accounted for roughly 45% of consolidated EBITDA, exposing CHS to demand shifts as markets decarbonize.

As policy and corporate buyers push net-zero targets, these units face scrutiny and potential obsolescence; diesel demand fell ~6% in 2023–24 in CHS key markets, raising margin pressure.

Shifting to low‑carbon fuels and green ammonia needs multibillion-dollar capex and complex execution; a rough estimate: $2–4B over 5–7 years to retrofit major plants, with high project and regulatory risk.

- ~45% EBITDA from carbon‑intensive units

- Diesel demand down ~6% (2023–24)

- Estimated $2–4B capex to decarbonize core assets

Commodity volatility, heavy capex & decarbonization hit growth—$182M write-downs, $2–4B needed

| Metric | 2024/2023 |

|---|---|

| Inventory write-downs | $182M (FY2024) |

| Grain margin swing | 27% YoY |

| Corn price drop (Q2 2024) | −38% |

| Annual maintenance/compliance | $300–400M |

| Total capex | $1.1B (2024) |

| Owners / member co-ops | ~75,000 / 1,000+ |

| Fossil/fertilizer EBITDA share | ~45% |

| Diesel demand change | −6% (2023–24) |

| Decarbonization capex est. | $2–4B (5–7 yrs) |

What You See Is What You Get

CHS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, so what you see is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

CHS shows resilient market reach and diversified operations but faces margin pressure from commodity volatility and regulatory shifts; its strategic partnerships and scale are strengths, while supply-chain risks and ESG expectations are key vulnerabilities. Want the full picture? Purchase the complete SWOT analysis for a research-backed, editable report and Excel tools to support investment, planning, and presentations.

Strengths

Dominant Cooperative Market Position

Integrated Supply Chain Infrastructure

Owning the Cenex brand gives CHS a dominant rural fuel network—roughly 2,000 retail sites—strengthening fuel margins and cross-selling between energy and ag customers.

Diversified Business Portfolio

CHS reduces sector risk by operating in crop nutrients, grain marketing, energy refining, and financial services, generating $49.7 billion in 2024 revenue so losses in one area can be offset by others.

When U.S. corn futures fell 18% in H2 2023, CHS's energy and fertilizer margins helped keep corporate EBITDA around $1.3 billion in 2024, stabilizing cash flow.

Strong Financial Liquidity and Capital Base

- Liquidity: $4.2B (FY 2024)

- Working capital: $1.8B (FY 2024)

- Earnings CAGR: 6.5% (2019–2024)

- Member returns: $220M patronage (2024)

Established Global Export Capabilities

CHS links North American farmers to Asia, Europe and South America, moving ~35% of its 2024 grain exports through owned terminals and long-term port leases, which helps clear domestic surpluses and capture higher FOB prices abroad.

Investments in deep-water ports and eight international marketing offices drove $5.1B in global merchandising revenue in FY2024, improving margin capture on export corridors.

- ~35% export throughput via owned/leased terminals (2024)

- $5.1B global merchandising revenue (FY2024)

- 8 international marketing offices supporting price discovery

CHS: $49.7B scale, $4.2B liquidity, 700k members—$1.2B allocations, resilient EBITDA

| Metric | 2024 |

|---|---|

| Revenue | $49.7B |

| Liquidity | $4.2B |

| Member base | 700,000 |

What is included in the product

Provides a clear SWOT framework for analyzing CHS’s business strategy, highlighting internal capabilities, operational gaps, growth drivers, and external market risks shaping its competitive position and future prospects.

Provides a concise CHS SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations.

Weaknesses

Exposure to Commodity Price Volatility

High Maintenance Costs for Aging Assets

Geographic Concentration in the U.S. Midwest

While CHS Inc. operates globally, about 55% of grain origination and roughly 60% of its member cooperatives are in the U.S. Midwest, concentrating revenue and supply risk in one region.

This dependence raises exposure to Midwest-specific shocks—2012-2013 droughts cut regional output by ~20%, and 2019 Mississippi River low flows cost inland barge operators an estimated $300M, risks that can ripple through CHS’s margins and liquidity.

Complex Cooperative Governance Structure

- 75,000 owners, 1,000+ member co-ops (2024)

- Board/member cycle delays = months

- $1.1B capex 2024; slower ROI risk

- Lower agility vs digital entrants

Dependence on Carbon-Intensive Energy Sectors

A large portion of CHS revenue comes from fossil fuel refining and nitrogen fertilizer; in 2024 these segments accounted for roughly 45% of consolidated EBITDA, exposing CHS to demand shifts as markets decarbonize.

As policy and corporate buyers push net-zero targets, these units face scrutiny and potential obsolescence; diesel demand fell ~6% in 2023–24 in CHS key markets, raising margin pressure.

Shifting to low‑carbon fuels and green ammonia needs multibillion-dollar capex and complex execution; a rough estimate: $2–4B over 5–7 years to retrofit major plants, with high project and regulatory risk.

- ~45% EBITDA from carbon‑intensive units

- Diesel demand down ~6% (2023–24)

- Estimated $2–4B capex to decarbonize core assets

Commodity volatility, heavy capex & decarbonization hit growth—$182M write-downs, $2–4B needed

| Metric | 2024/2023 |

|---|---|

| Inventory write-downs | $182M (FY2024) |

| Grain margin swing | 27% YoY |

| Corn price drop (Q2 2024) | −38% |

| Annual maintenance/compliance | $300–400M |

| Total capex | $1.1B (2024) |

| Owners / member co-ops | ~75,000 / 1,000+ |

| Fossil/fertilizer EBITDA share | ~45% |

| Diesel demand change | −6% (2023–24) |

| Decarbonization capex est. | $2–4B (5–7 yrs) |

What You See Is What You Get

CHS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, so what you see is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.