Canadian Imperial Bank Business Model Canvas

CIBC Decoded: A Concise Business Model Canvas Revealing How the Bank Wins

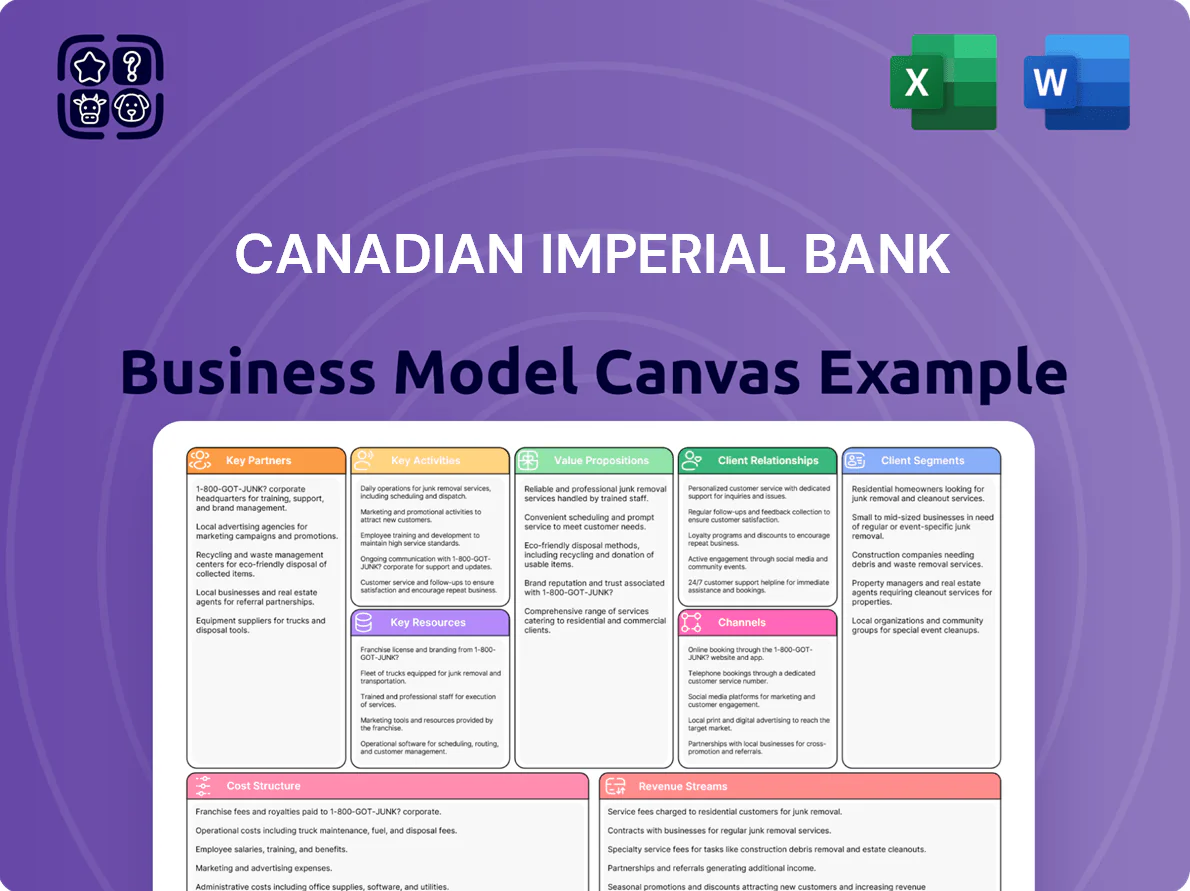

Unlock the full strategic blueprint behind Canadian Imperial Bank's business model—our in-depth Business Model Canvas dissects customer segments, value propositions, revenue streams and key partnerships to show exactly how CIBC wins and scales in banking.

Partnerships

Strategic Fintech Collaborations

CIBC partners with fintechs to embed digital payments, AI credit scoring, and biometric security into its infrastructure, cutting mobile app login times by 35% and speeding loan approvals by 40% in pilot programs; in 2025 these collaborations supported ~2.1 million active digital users and aimed to reduce fraud losses by an estimated CAD 45m annually.

Retail and Brand Affiliates

CIBC partners with major retailers like Loblaw Companies Limited via PC Financial to issue co-branded credit cards and loyalty rewards, which helped drive $1.2 billion in retail card purchase volume in 2024 and supported a 3.1% rise in personal banking net new accounts that year. These retailer ties expand CIBC’s presence in everyday spending categories, increasing card activation rates by about 8 percentage points versus non-affiliate cards.

Global Payment Networks

Partnerships with Visa and Mastercard power CIBC’s credit and debit card operations, enabling global acceptance and settlement; in 2024 CIBC issued over 5 million cards and processed billions in transactions via these networks.

Mortgage and Insurance Brokers

CIBC partners with thousands of third-party mortgage brokers and insurance providers to distribute mortgages and protection products, reaching clients who skip branches; brokers originated roughly 45% of Canadian mortgage volume in 2024, helping CIBC defend share in a market where its Canadian banking revenue was C$19.8B in FY2024.

- Expands distribution beyond branches

- Accesses diverse customer segments

- Supports mortgage market share amid 2024 broker-led origination (~45%)

- Cost-efficient external sales channel

Government and Regulatory Bodies

The bank partners with agencies like Canada Mortgage and Housing Corporation (CMHC) and the Bank of Canada to manage a CAD 200+ billion insured mortgage book and align with monetary policy and liquidity operations.

These ties ensure compliance with federal regulations, stress-tested capital ratios (Tier 1 CET1 ~12.5% in 2024) and cross-border rules across the North American financial system.

- CMHC: insured-mortgage underwriting and guarantees

- Bank of Canada: policy rate, liquidity facilities

- OSFI/FINTRAC: prudential rules and AML/CFT compliance

- Cross-border regulators: US passthrough and reporting

CIBC partners power digital adoption, card growth & a C$200B+ mortgage franchise

CIBC’s key partners—fintechs, Loblaw/PC Financial, Visa/Mastercard, mortgage brokers, CMHC, Bank of Canada, OSFI—drive digital adoption (≈2.1M active digital users in 2025), retail card spend (C$1.2B in 2024), card issuance (5M+ cards in 2024), broker-originated mortgages (~45% of market 2024), and support a C$200B+ insured mortgage book and CET1 ≈12.5% (2024).

| Metric | Value |

|---|---|

| Digital users (2025) | ≈2.1M |

| Retail card volume (2024) | C$1.2B |

| Cards issued (2024) | 5M+ |

| Broker mortgage share (2024) | ≈45% |

| Insured mortgage book | >C$200B |

| CET1 ratio (2024) | ≈12.5% |

What is included in the product

A concise, ready-to-use Business Model Canvas for Canadian Imperial Bank of Commerce (CIBC) outlining customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams mapped to CIBC’s real-world retail, commercial, and wealth businesses.

High-level view of CIBC’s business model with editable cells to streamline strategy reviews and relieve the pain of building structured bank-centric canvases from scratch.

Activities

Retail and Business Lending

Retail and business lending at Canadian Imperial Bank of Commerce (CIBC) covers underwriting and management of personal loans, mortgages and commercial credit lines, with $207.5 billion in loans and acceptances on the balance sheet as of Q4 2025; credit loss provisions remained 0.35% in FY2024. CIBC uses rigorous risk assessment and, by late 2025, AI-driven credit-scoring models screen ~65% of new applications to speed decisions and protect capital.

Wealth and Asset Management

CIBC’s Wood Gundy and Private Wealth deliver investment advice, portfolio management, and estate planning for HNW clients, using active research and asset-allocation strategies to grow assets and secure recurring fee income; as of FY2024 CIBC Wealth reported CA$76.7 billion in assets under administration and contributed roughly CA$1.1 billion in revenue, driving stable fee-based margins for the bank.

Capital Markets Operations

Digital Infrastructure Maintenance

CIBC dedicates a large share of IT spend to keep digital banking live 24/7, strengthen cybersecurity, and enhance mobile UX; in 2024 CIBC reported CAD 2.2B in technology and operational expenses, with digital sessions up ~18% YoY and 99.98% uptime on core platforms.

- CAD 2.2B tech/ops spend (2024)

- 99.98% core uptime

- Digital sessions +18% YoY

- Continuous app releases, regular security audits

Compliance and Risk Management

Compliance and risk management at Canadian Imperial Bank of Commerce (CIBC) centers on real‑time transaction monitoring for fraud and strict Anti‑Money Laundering (AML) controls; in 2024 CIBC reported regulatory and compliance expenses of CAD 1.02 billion, reflecting heavy investment in these systems.

The bank runs frequent internal audits and submits detailed regulatory reports to reduce operational and legal risk, protecting reputation and solvency in a sector where fines can reach hundreds of millions.

- Real‑time transaction monitoring

- AML program enforcement

- Internal audits (ongoing)

- Regulatory reporting (CAD 1.02B in 2024)

- Reputation and capital protection

Bank drives CA$207.5B loans, CA$76.7B AUA; AI scores ~65% of new apps

Core activities: retail/commercial lending (CA$207.5B loans, Q4 2025), wealth management (CA$76.7B AUA, FY2024), capital markets (≈CA$1.2B revenue, 2024), tech/ops (CA$2.2B spend, 2024; 99.98% uptime), compliance (CA$1.02B reg spend, 2024); AI credit scoring covers ~65% of new apps by late 2025.

| Metric | Value |

|---|---|

| Loans | CA$207.5B Q4 2025 |

| Wealth AUA | CA$76.7B FY2024 |

| Cap Mkts Rev | CA$1.2B 2024 |

| Tech/ops | CA$2.2B 2024 |

| Compliance | CA$1.02B 2024 |

| AI credit | ~65% apps late 2025 |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Canadian Imperial Bank Business Model Canvas—not a mockup or sample—and reflects the exact file you’ll receive after purchase.

When you complete your order, you’ll get full access to this same professionally formatted document, ready to edit, present, or share in the provided formats.

No surprises or filler pages—this preview is a direct snapshot of the final deliverable, and the complete version will be instantly downloadable upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

CIBC Decoded: A Concise Business Model Canvas Revealing How the Bank Wins

Unlock the full strategic blueprint behind Canadian Imperial Bank's business model—our in-depth Business Model Canvas dissects customer segments, value propositions, revenue streams and key partnerships to show exactly how CIBC wins and scales in banking.

Partnerships

Strategic Fintech Collaborations

CIBC partners with fintechs to embed digital payments, AI credit scoring, and biometric security into its infrastructure, cutting mobile app login times by 35% and speeding loan approvals by 40% in pilot programs; in 2025 these collaborations supported ~2.1 million active digital users and aimed to reduce fraud losses by an estimated CAD 45m annually.

Retail and Brand Affiliates

CIBC partners with major retailers like Loblaw Companies Limited via PC Financial to issue co-branded credit cards and loyalty rewards, which helped drive $1.2 billion in retail card purchase volume in 2024 and supported a 3.1% rise in personal banking net new accounts that year. These retailer ties expand CIBC’s presence in everyday spending categories, increasing card activation rates by about 8 percentage points versus non-affiliate cards.

Global Payment Networks

Partnerships with Visa and Mastercard power CIBC’s credit and debit card operations, enabling global acceptance and settlement; in 2024 CIBC issued over 5 million cards and processed billions in transactions via these networks.

Mortgage and Insurance Brokers

CIBC partners with thousands of third-party mortgage brokers and insurance providers to distribute mortgages and protection products, reaching clients who skip branches; brokers originated roughly 45% of Canadian mortgage volume in 2024, helping CIBC defend share in a market where its Canadian banking revenue was C$19.8B in FY2024.

- Expands distribution beyond branches

- Accesses diverse customer segments

- Supports mortgage market share amid 2024 broker-led origination (~45%)

- Cost-efficient external sales channel

Government and Regulatory Bodies

The bank partners with agencies like Canada Mortgage and Housing Corporation (CMHC) and the Bank of Canada to manage a CAD 200+ billion insured mortgage book and align with monetary policy and liquidity operations.

These ties ensure compliance with federal regulations, stress-tested capital ratios (Tier 1 CET1 ~12.5% in 2024) and cross-border rules across the North American financial system.

- CMHC: insured-mortgage underwriting and guarantees

- Bank of Canada: policy rate, liquidity facilities

- OSFI/FINTRAC: prudential rules and AML/CFT compliance

- Cross-border regulators: US passthrough and reporting

CIBC partners power digital adoption, card growth & a C$200B+ mortgage franchise

CIBC’s key partners—fintechs, Loblaw/PC Financial, Visa/Mastercard, mortgage brokers, CMHC, Bank of Canada, OSFI—drive digital adoption (≈2.1M active digital users in 2025), retail card spend (C$1.2B in 2024), card issuance (5M+ cards in 2024), broker-originated mortgages (~45% of market 2024), and support a C$200B+ insured mortgage book and CET1 ≈12.5% (2024).

| Metric | Value |

|---|---|

| Digital users (2025) | ≈2.1M |

| Retail card volume (2024) | C$1.2B |

| Cards issued (2024) | 5M+ |

| Broker mortgage share (2024) | ≈45% |

| Insured mortgage book | >C$200B |

| CET1 ratio (2024) | ≈12.5% |

What is included in the product

A concise, ready-to-use Business Model Canvas for Canadian Imperial Bank of Commerce (CIBC) outlining customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams mapped to CIBC’s real-world retail, commercial, and wealth businesses.

High-level view of CIBC’s business model with editable cells to streamline strategy reviews and relieve the pain of building structured bank-centric canvases from scratch.

Activities

Retail and Business Lending

Retail and business lending at Canadian Imperial Bank of Commerce (CIBC) covers underwriting and management of personal loans, mortgages and commercial credit lines, with $207.5 billion in loans and acceptances on the balance sheet as of Q4 2025; credit loss provisions remained 0.35% in FY2024. CIBC uses rigorous risk assessment and, by late 2025, AI-driven credit-scoring models screen ~65% of new applications to speed decisions and protect capital.

Wealth and Asset Management

CIBC’s Wood Gundy and Private Wealth deliver investment advice, portfolio management, and estate planning for HNW clients, using active research and asset-allocation strategies to grow assets and secure recurring fee income; as of FY2024 CIBC Wealth reported CA$76.7 billion in assets under administration and contributed roughly CA$1.1 billion in revenue, driving stable fee-based margins for the bank.

Capital Markets Operations

Digital Infrastructure Maintenance

CIBC dedicates a large share of IT spend to keep digital banking live 24/7, strengthen cybersecurity, and enhance mobile UX; in 2024 CIBC reported CAD 2.2B in technology and operational expenses, with digital sessions up ~18% YoY and 99.98% uptime on core platforms.

- CAD 2.2B tech/ops spend (2024)

- 99.98% core uptime

- Digital sessions +18% YoY

- Continuous app releases, regular security audits

Compliance and Risk Management

Compliance and risk management at Canadian Imperial Bank of Commerce (CIBC) centers on real‑time transaction monitoring for fraud and strict Anti‑Money Laundering (AML) controls; in 2024 CIBC reported regulatory and compliance expenses of CAD 1.02 billion, reflecting heavy investment in these systems.

The bank runs frequent internal audits and submits detailed regulatory reports to reduce operational and legal risk, protecting reputation and solvency in a sector where fines can reach hundreds of millions.

- Real‑time transaction monitoring

- AML program enforcement

- Internal audits (ongoing)

- Regulatory reporting (CAD 1.02B in 2024)

- Reputation and capital protection

Bank drives CA$207.5B loans, CA$76.7B AUA; AI scores ~65% of new apps

Core activities: retail/commercial lending (CA$207.5B loans, Q4 2025), wealth management (CA$76.7B AUA, FY2024), capital markets (≈CA$1.2B revenue, 2024), tech/ops (CA$2.2B spend, 2024; 99.98% uptime), compliance (CA$1.02B reg spend, 2024); AI credit scoring covers ~65% of new apps by late 2025.

| Metric | Value |

|---|---|

| Loans | CA$207.5B Q4 2025 |

| Wealth AUA | CA$76.7B FY2024 |

| Cap Mkts Rev | CA$1.2B 2024 |

| Tech/ops | CA$2.2B 2024 |

| Compliance | CA$1.02B 2024 |

| AI credit | ~65% apps late 2025 |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Canadian Imperial Bank Business Model Canvas—not a mockup or sample—and reflects the exact file you’ll receive after purchase.

When you complete your order, you’ll get full access to this same professionally formatted document, ready to edit, present, or share in the provided formats.

No surprises or filler pages—this preview is a direct snapshot of the final deliverable, and the complete version will be instantly downloadable upon purchase.