China International Capital Corporation Porter's Five Forces Analysis

From Overview to Strategy Blueprint

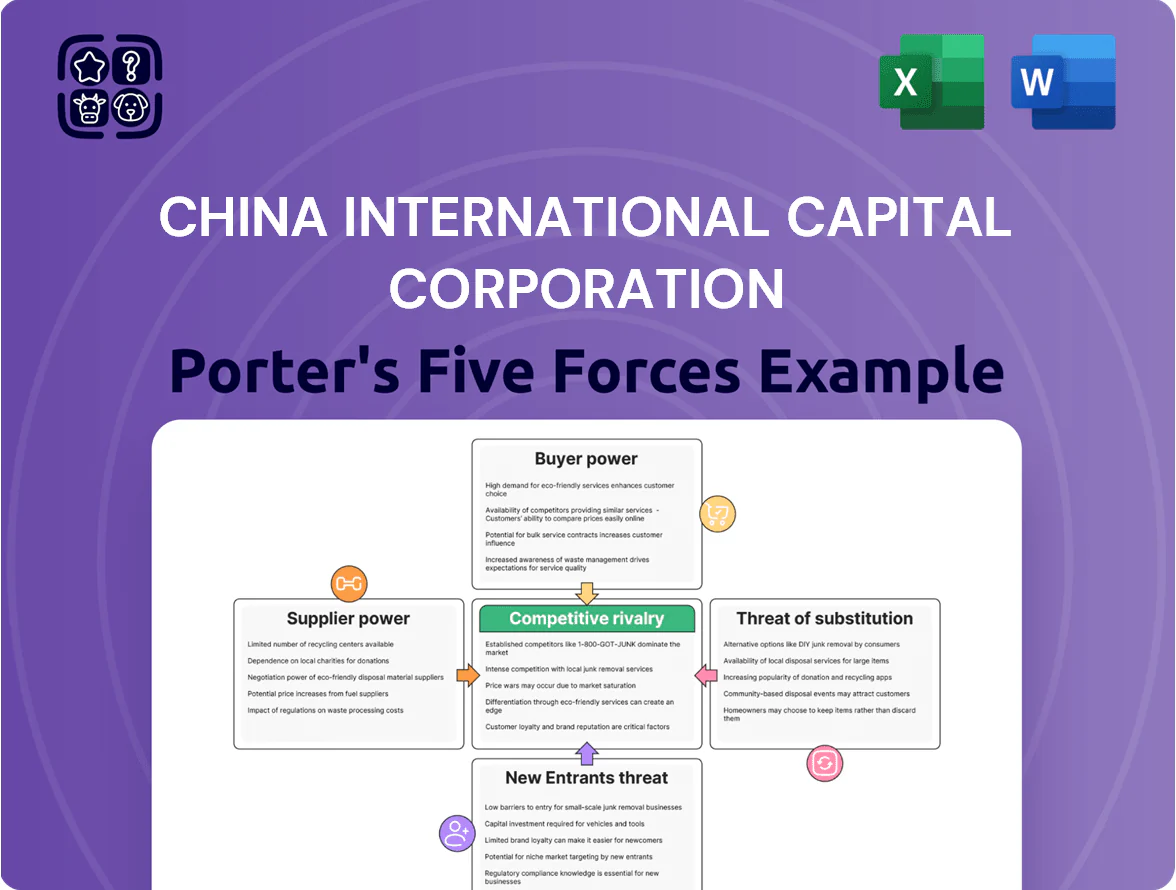

China International Capital Corporation (CICC) operates in a highly competitive investment banking landscape where client concentration, regulatory shifts, and fintech disruption shape bargaining power and margins.

This snapshot highlights key pressures—strong buyer sophistication, moderate supplier leverage, high rivalry, manageable threat of substitutes, and guarded entry barriers—affecting CICC’s strategic choices.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Access to Elite Human Capital

The primary suppliers for China International Capital Corporation (CICC) are its senior investment bankers, research analysts, and wealth managers, whose skillsets drive deal origination and AUM growth.

By end-2025 demand for talent with China-market expertise plus global finance fluency remains very high; headhunters report a 22% pay premium for such hires in mainland China in 2024–25.

Top performers hold leverage—CICC must match cash compensation, carry and prestige to avoid poaching by global banks or private equity, or risk higher attrition and lost mandates.

Financial Data and Infrastructure Providers

CICC depends on terminals and feeds from Bloomberg, Wind and Reuters and on HFT infrastructure; these vendors have moderate–high bargaining power because their data drives analysis, valuation and execution.

In 2024 CICC paid an estimated >USD 10–30m annually for terminal/licensing and millisecond-capable connectivity; the small global supplier pool and technical lock-in limit CICC’s leverage despite its scale.

Capital and Liquidity Sources

As an intermediary, CICC relies on interbank funding and bond markets; large Chinese banks and institutional bondholders supply liquidity and can tighten terms when policy rates rise.

By late 2025, global policy tightening pushed benchmark yields—China 1Y LPR ~3.55% and US 10Y ~4.6%—raising CICC’s funding costs and squeezing trading and underwriting margins.

Higher cost of capital gives these liquidity suppliers bargaining power over pricing, tenor, and covenant demands, increasing CICC’s refinancing and balance-sheet risk.

Technological and AI Software Vendors

The shift to AI analytics and cloud wealth platforms makes tech vendors critical; global fintech AI spending hit $55bn in 2024, raising vendor leverage over CICC.

CICC depends on advanced cybersecurity and proprietary trading software to protect client assets and alpha; breaches cost firms ~$4.45m on average in 2023.

High switching costs and bespoke integration give vendors substantial bargaining power at renewals, often locking multi-year, high-margin contracts.

- 2024 fintech AI spend $55bn

- Avg breach cost $4.45m (2023)

- Large switching costs, multi-year contracts

Regulatory Compliance and Legal Services

External legal counsel and compliance consultants are critical for China International Capital Corporation’s cross-border deals and IPOs; top-tier law firms earned average China-Hong Kong-New York cross-border deal fees of ~3–5% of transaction value in 2024–2025, reflecting their bargaining leverage.

Regulatory changes in China, Hong Kong, and the US through 2025 raise compliance complexity, so these firms command high fees and limited supplier substitution, increasing supplier power and cost risk for CICC.

- Top-tier firms: 3–5% avg deal fees (2024–2025)

- Multi-jurisdiction complexity: China, HK, US rule changes in 2023–2025

- Low substitution: niche expertise, high switching costs

Suppliers wield strong pricing power: premiums, high terminal costs & rising fintech/cyber/legal bills

Suppliers (senior bankers, data vendors, tech vendors, liquidity providers, law firms) hold moderate–high bargaining power: 22% pay premium for China-skilled hires (2024–25); terminal/licenses >USD10–30m pa; fintech AI spend $55bn (2024); avg breach cost $4.45m (2023); top-tier legal fees ~3–5% (2024–25); funding pressures: China 1Y LPR ~3.55%, US 10Y ~4.6% (late 2025).

| Supplier | Key metric |

|---|---|

| Talent | 22% pay premium |

| Data/terminals | >USD10–30m pa |

| Fintech | $55bn (2024) |

| Cyber cost | $4.45m (2023) |

| Legal | 3–5% fees |

What is included in the product

Tailored Porter's Five Forces analysis for China International Capital Corporation that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market position—ideal for investor decks and strategic planning.

A concise Porter's Five Forces snapshot for China International Capital Corporation—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

Sophisticated Institutional Investors

Institutional clients—pension funds, sovereign wealth funds—account for roughly 60–70% of CICC’s AUM and a similar share of brokerage flow, giving them strong leverage; a single sovereign or pension reallocation can shift hundreds of millions of dollars in fees away. They press for lower commissions and bespoke research, so CICC must offer tailored macro/sector reports and execution packages to retain mandates. In 2024 CICC reported institutional revenue growth of ~12%, showing the cost of meeting those demands.

Corporate Clients for Investment Banking

Major corporate IPO and M&A clients wield strong leverage because single transactions often exceed $500m and generate fees >1% of deal value, so by end-2025 many solicit pitches from 3–6 top banks, compressing underwriting fees by an estimated 10–25%. CICC’s international execution record (e.g., 2024 led global IPOs in China with $7.2bn arranged) cushions fee pressure, but rivals like CITIC, CSC, and international banks leave clients ample alternatives. Large SOEs and tech firms drive most mandate competition, raising client bargaining power despite CICC’s brand.

High-Net-Worth Individuals in Wealth Management

The wealth management arm of China International Capital Corporation serves high-net-worth individuals (HNWI) who are more mobile and financially literate; China had about 2.7 million HNWIs in 2024, up 8% year-on-year per Capgemini. These clients hold high bargaining power since they can shift assets to boutique firms or international private banks; average Chinese HNWI allocates roughly 30% to offshore or alternative investments. To retain them, CICC must deliver superior risk-adjusted returns and tailored service, because individual switching costs—often under 1% of AUM in fees and paperwork—are relatively low.

Government and State-Owned Enterprises

As a firm rooted in China, CICC regularly advises government bodies and SOEs that control large mandates — SOEs held ~34% of China’s nonfinancial corporate assets in 2023, so their deals can reshape markets.

These clients wield strategic power: negotiations often prioritize national policy over price, forcing CICC to tailor offerings to state economic goals, for example underwriting sovereign-linked bonds and state M&A.

Retail Investors and Digital Users

CICC targets high-net-worth clients but its digital brokerage faces price-sensitive retail users; by 2025 zero-commission models and platforms with >200 million Chinese retail accounts have pushed fee compression across the industry.

Retail traders, skewing younger, prefer fintech rivals; CICC must offer competitive digital pricing while protecting premium advisory margins to avoid losing market share.

- Zero-commission trend: widespread by 2025

- Industry retail accounts: ~200m+ in China

- Risk: younger users shift to fintech

- Need: competitive digital fees + premium services

CICC faces fee squeeze: institutional/SOE mandates vs. zero‑commission retail surge

Institutional and SOE clients hold high leverage—60–70% of CICC AUM from institutions (2024); SOEs owned ~34% of nonfinancial corporate assets (2023)—driving fee demands and policy-led mandates; large deals (> $500m) compress underwriting fees ~10–25%; HNWIs (2.7m in China, 2024) and 200m+ retail accounts force zero‑commission/fintech pressure by 2025.

| Client Type | Key Stat | Impact on CICC |

|---|---|---|

| Institutions | 60–70% AUM (2024) | High fee leverage |

| SOEs | 34% assets (2023) | Policy-driven mandates |

| Large deals | >$500m; fees down 10–25% | Fee compression |

| HNWIs | 2.7m (2024) | Mobile; demand bespoke service |

| Retail | 200m+ accounts (2025) | Zero‑commission pressure |

Same Document Delivered

China International Capital Corporation Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China International Capital Corporation you'll receive immediately after purchase—no placeholders or samples.

The document displayed is fully formatted and ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threats of entry and substitution.

No mockups or excerpts—this is the final deliverable you’ll get instantly after payment, prepared for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

China International Capital Corporation (CICC) operates in a highly competitive investment banking landscape where client concentration, regulatory shifts, and fintech disruption shape bargaining power and margins.

This snapshot highlights key pressures—strong buyer sophistication, moderate supplier leverage, high rivalry, manageable threat of substitutes, and guarded entry barriers—affecting CICC’s strategic choices.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Access to Elite Human Capital

The primary suppliers for China International Capital Corporation (CICC) are its senior investment bankers, research analysts, and wealth managers, whose skillsets drive deal origination and AUM growth.

By end-2025 demand for talent with China-market expertise plus global finance fluency remains very high; headhunters report a 22% pay premium for such hires in mainland China in 2024–25.

Top performers hold leverage—CICC must match cash compensation, carry and prestige to avoid poaching by global banks or private equity, or risk higher attrition and lost mandates.

Financial Data and Infrastructure Providers

CICC depends on terminals and feeds from Bloomberg, Wind and Reuters and on HFT infrastructure; these vendors have moderate–high bargaining power because their data drives analysis, valuation and execution.

In 2024 CICC paid an estimated >USD 10–30m annually for terminal/licensing and millisecond-capable connectivity; the small global supplier pool and technical lock-in limit CICC’s leverage despite its scale.

Capital and Liquidity Sources

As an intermediary, CICC relies on interbank funding and bond markets; large Chinese banks and institutional bondholders supply liquidity and can tighten terms when policy rates rise.

By late 2025, global policy tightening pushed benchmark yields—China 1Y LPR ~3.55% and US 10Y ~4.6%—raising CICC’s funding costs and squeezing trading and underwriting margins.

Higher cost of capital gives these liquidity suppliers bargaining power over pricing, tenor, and covenant demands, increasing CICC’s refinancing and balance-sheet risk.

Technological and AI Software Vendors

The shift to AI analytics and cloud wealth platforms makes tech vendors critical; global fintech AI spending hit $55bn in 2024, raising vendor leverage over CICC.

CICC depends on advanced cybersecurity and proprietary trading software to protect client assets and alpha; breaches cost firms ~$4.45m on average in 2023.

High switching costs and bespoke integration give vendors substantial bargaining power at renewals, often locking multi-year, high-margin contracts.

- 2024 fintech AI spend $55bn

- Avg breach cost $4.45m (2023)

- Large switching costs, multi-year contracts

Regulatory Compliance and Legal Services

External legal counsel and compliance consultants are critical for China International Capital Corporation’s cross-border deals and IPOs; top-tier law firms earned average China-Hong Kong-New York cross-border deal fees of ~3–5% of transaction value in 2024–2025, reflecting their bargaining leverage.

Regulatory changes in China, Hong Kong, and the US through 2025 raise compliance complexity, so these firms command high fees and limited supplier substitution, increasing supplier power and cost risk for CICC.

- Top-tier firms: 3–5% avg deal fees (2024–2025)

- Multi-jurisdiction complexity: China, HK, US rule changes in 2023–2025

- Low substitution: niche expertise, high switching costs

Suppliers wield strong pricing power: premiums, high terminal costs & rising fintech/cyber/legal bills

Suppliers (senior bankers, data vendors, tech vendors, liquidity providers, law firms) hold moderate–high bargaining power: 22% pay premium for China-skilled hires (2024–25); terminal/licenses >USD10–30m pa; fintech AI spend $55bn (2024); avg breach cost $4.45m (2023); top-tier legal fees ~3–5% (2024–25); funding pressures: China 1Y LPR ~3.55%, US 10Y ~4.6% (late 2025).

| Supplier | Key metric |

|---|---|

| Talent | 22% pay premium |

| Data/terminals | >USD10–30m pa |

| Fintech | $55bn (2024) |

| Cyber cost | $4.45m (2023) |

| Legal | 3–5% fees |

What is included in the product

Tailored Porter's Five Forces analysis for China International Capital Corporation that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market position—ideal for investor decks and strategic planning.

A concise Porter's Five Forces snapshot for China International Capital Corporation—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

Sophisticated Institutional Investors

Institutional clients—pension funds, sovereign wealth funds—account for roughly 60–70% of CICC’s AUM and a similar share of brokerage flow, giving them strong leverage; a single sovereign or pension reallocation can shift hundreds of millions of dollars in fees away. They press for lower commissions and bespoke research, so CICC must offer tailored macro/sector reports and execution packages to retain mandates. In 2024 CICC reported institutional revenue growth of ~12%, showing the cost of meeting those demands.

Corporate Clients for Investment Banking

Major corporate IPO and M&A clients wield strong leverage because single transactions often exceed $500m and generate fees >1% of deal value, so by end-2025 many solicit pitches from 3–6 top banks, compressing underwriting fees by an estimated 10–25%. CICC’s international execution record (e.g., 2024 led global IPOs in China with $7.2bn arranged) cushions fee pressure, but rivals like CITIC, CSC, and international banks leave clients ample alternatives. Large SOEs and tech firms drive most mandate competition, raising client bargaining power despite CICC’s brand.

High-Net-Worth Individuals in Wealth Management

The wealth management arm of China International Capital Corporation serves high-net-worth individuals (HNWI) who are more mobile and financially literate; China had about 2.7 million HNWIs in 2024, up 8% year-on-year per Capgemini. These clients hold high bargaining power since they can shift assets to boutique firms or international private banks; average Chinese HNWI allocates roughly 30% to offshore or alternative investments. To retain them, CICC must deliver superior risk-adjusted returns and tailored service, because individual switching costs—often under 1% of AUM in fees and paperwork—are relatively low.

Government and State-Owned Enterprises

As a firm rooted in China, CICC regularly advises government bodies and SOEs that control large mandates — SOEs held ~34% of China’s nonfinancial corporate assets in 2023, so their deals can reshape markets.

These clients wield strategic power: negotiations often prioritize national policy over price, forcing CICC to tailor offerings to state economic goals, for example underwriting sovereign-linked bonds and state M&A.

Retail Investors and Digital Users

CICC targets high-net-worth clients but its digital brokerage faces price-sensitive retail users; by 2025 zero-commission models and platforms with >200 million Chinese retail accounts have pushed fee compression across the industry.

Retail traders, skewing younger, prefer fintech rivals; CICC must offer competitive digital pricing while protecting premium advisory margins to avoid losing market share.

- Zero-commission trend: widespread by 2025

- Industry retail accounts: ~200m+ in China

- Risk: younger users shift to fintech

- Need: competitive digital fees + premium services

CICC faces fee squeeze: institutional/SOE mandates vs. zero‑commission retail surge

Institutional and SOE clients hold high leverage—60–70% of CICC AUM from institutions (2024); SOEs owned ~34% of nonfinancial corporate assets (2023)—driving fee demands and policy-led mandates; large deals (> $500m) compress underwriting fees ~10–25%; HNWIs (2.7m in China, 2024) and 200m+ retail accounts force zero‑commission/fintech pressure by 2025.

| Client Type | Key Stat | Impact on CICC |

|---|---|---|

| Institutions | 60–70% AUM (2024) | High fee leverage |

| SOEs | 34% assets (2023) | Policy-driven mandates |

| Large deals | >$500m; fees down 10–25% | Fee compression |

| HNWIs | 2.7m (2024) | Mobile; demand bespoke service |

| Retail | 200m+ accounts (2025) | Zero‑commission pressure |

Same Document Delivered

China International Capital Corporation Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China International Capital Corporation you'll receive immediately after purchase—no placeholders or samples.

The document displayed is fully formatted and ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threats of entry and substitution.

No mockups or excerpts—this is the final deliverable you’ll get instantly after payment, prepared for immediate application.