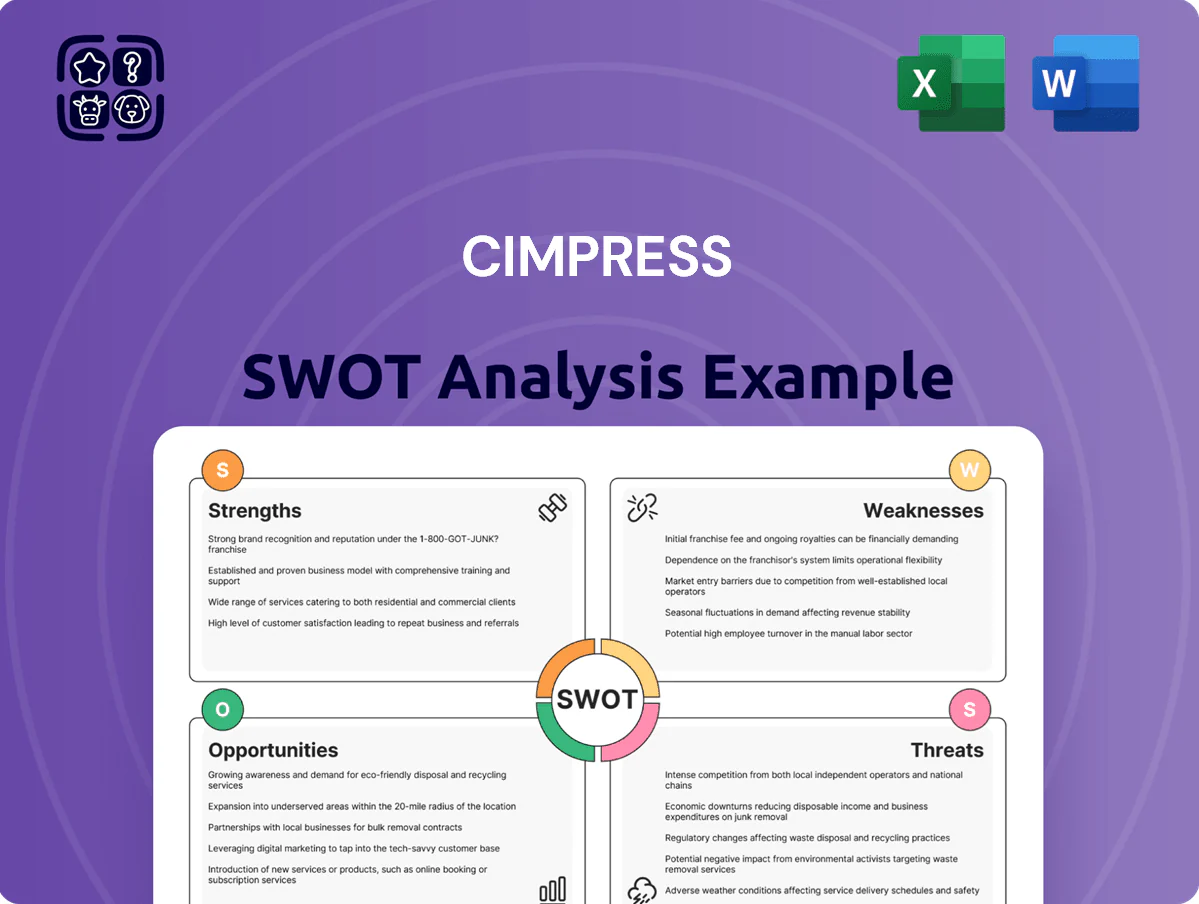

Cimpress SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Cimpress combines mass-customization scale with strong e-commerce tech, but faces margin pressure, competition, and execution complexity; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete SWOT analysis to get a professionally written, editable Word report plus an Excel matrix—built for investors, consultants, and executives to plan, pitch, and act with confidence.

Strengths

Dominant Market Presence

Cimpress, via Vistaprint, held roughly 35% share of the online small-business print market in key markets by end-2025, giving it clear scale advantages in customer acquisition and trust.

Brand recognition cut customer CAC by an estimated 18% versus mid‑market rivals in 2024–25, and repeat purchase rates stayed near 48%, supporting steady revenue per active customer.

Proprietary Technology Platform

The Cimpress Mass Customization Platform is the backbone for its multi-brand operations, powering 22+ manufacturing sites and handling over 70% of orders as small batches, which drove €2.3bn revenue in 2024. The centralized tech lets brands share production lines and a global logistics network, cutting unit costs and improving fulfillment speed by ~18% year-over-year. It offers scalable infrastructure that enabled 120+ product launches in 2024 and supports rapid regional rollouts across 30+ countries.

Diverse Brand Portfolio

Cimpress runs brands like Pixartprinting, BuildASign and National Pen across 30+ countries, cutting single-brand exposure and supporting 2024 pro forma revenue of about €2.6 billion so risk is spread and cash flow steadier; each label keeps its market identity while sharing Cimpress tech, lowering per-brand R&D costs and improving gross margin — Pixartprinting alone served over 250,000 customers in 2024.

Advanced Supply Chain Efficiency

Cimpress runs a global, localized production network that cut average shipping distance and costs; in 2024 the company reported 31% of units fulfilled within 50 miles of customers, lowering logistics spend per order by about 12% versus 2019.

Producing near end users speeds delivery (median lead time ~3.8 days in FY2024) and trims CO2 emissions; rivals with smaller footprints struggle to match scale and unit economics.

- 31% of units fulfilled within 50 miles (2024)

- 12% lower logistics cost per order vs 2019

- Median lead time ~3.8 days (FY2024)

- Localized output reduces CO2 and improves margins

Data-Driven Customer Insights

With millions of transactions across Cimpress platforms—over 25 million orders in 2024—Cimpress holds rich data on buyer behavior and design trends, enabling precise product-market fit.

These insights drive targeted campaigns that cut customer acquisition cost; Cimpress reported a 12% YoY improvement in marketing ROI in 2024.

Personalization based on this data boosts customer lifetime value and repeat purchase rates, supporting margin resilience in a competitive market.

- 25M+ orders in 2024

- 12% YoY marketing ROI improvement (2024)

- Higher repeat rates via personalization

Cimpress: 35% SMB print share, €2.6bn revenue, 25M orders, 3.8‑day median lead time

Cimpress holds ~35% online SMB print share (end‑2025), drove ~€2.6bn pro forma revenue in 2024, processed 25M+ orders in 2024, and achieved a median lead time of ~3.8 days with 31% of units fulfilled within 50 miles, cutting logistics costs ~12% vs 2019 and lowering CAC ~18% vs mid‑market rivals.

| Metric | Value |

|---|---|

| Market share (online SMB) | ~35% (end‑2025) |

| Pro forma revenue | €2.6bn (2024) |

| Orders | 25M+ (2024) |

| Median lead time | ~3.8 days (FY2024) |

| Local fulfillment | 31% within 50 miles (2024) |

| Logistics cost change | −12% vs 2019 |

| CAC advantage | −18% vs mid‑market (2024–25) |

What is included in the product

Analyzes Cimpress’s competitive position by outlining its strengths, weaknesses, opportunities, and threats to provide a concise strategic overview of the company’s market advantages, operational gaps, and future risks.

Offers a concise Cimpress SWOT matrix for rapid strategic alignment, ideal for executives and teams needing a clear, visual snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Financial Leverage

Cimpress carries significant financial leverage after a decade of acquisitions and tech investment, with long-term debt of $1.12 billion and net debt around $940 million as of FY2024 (ended Sept 30, 2024). Interest expense of roughly $85 million in FY2024 reduces free cash flow and limits near-term reinvestment into emerging markets or disruptive tech. Leadership cites debt management and deleveraging as priorities to protect creditworthiness and long-term fiscal stability.

Compressed Profit Margins

The online printing sector’s intense price competition keeps gross margins under pressure; Cimpress reported a 2024 gross margin of ~36.5% (FY2024) versus peers at ~40%, forcing frequent aggressive discounting to defend market share, which squeezed adjusted EBITDA margin to 6.8% in FY2024. Balancing volume-led revenue growth with price integrity remains a key operational challenge in a crowded marketplace.

Operational Complexity

Managing Cimpress’ diverse portfolio—over 40 brands across 30+ countries—ties together legacy systems and cultures, creating integration hurdles that stretched SG&A to $1.1B in FY2024 and slowed group-wide initiatives; this complexity drove a 6% YoY increase in operating expenses in 2024 and longer decision cycles. Streamlining operations while keeping brand autonomy demands ongoing management focus and capital, risking slower scale benefits.

Dependence on Small Business Spending

- ~65% revenue from SMBs (2024)

- FY2023 revenue down 4.8% in key channels

- Enterprise shift = multi-year, capital-intensive

High Customer Acquisition Costs

Cimpress: High Debt, Thin Margins, Rising CACs and SMB Concentration

Cimpress carries high leverage (long-term debt $1.12B; net debt ~$940M FY2024), thin margins (gross ~36.5%; adj EBITDA 6.8% FY2024), heavy SMB exposure (~65% revenue FY2024) and rising customer acquisition costs (CPCs +15% YoY 2024; S&M $358M FY2024), plus integration complexity across 40+ brands slowing scale benefits.

| Metric | Value |

|---|---|

| Long-term debt | $1.12B |

| Net debt | $940M |

| Gross margin | 36.5% |

| Adj EBITDA | 6.8% |

| SMB revenue | ~65% |

| CPC change | +15% YoY 2024 |

| S&M | $358M FY2024 |

Preview the Actual Deliverable

Cimpress SWOT Analysis

This is the actual Cimpress SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Cimpress combines mass-customization scale with strong e-commerce tech, but faces margin pressure, competition, and execution complexity; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete SWOT analysis to get a professionally written, editable Word report plus an Excel matrix—built for investors, consultants, and executives to plan, pitch, and act with confidence.

Strengths

Dominant Market Presence

Cimpress, via Vistaprint, held roughly 35% share of the online small-business print market in key markets by end-2025, giving it clear scale advantages in customer acquisition and trust.

Brand recognition cut customer CAC by an estimated 18% versus mid‑market rivals in 2024–25, and repeat purchase rates stayed near 48%, supporting steady revenue per active customer.

Proprietary Technology Platform

The Cimpress Mass Customization Platform is the backbone for its multi-brand operations, powering 22+ manufacturing sites and handling over 70% of orders as small batches, which drove €2.3bn revenue in 2024. The centralized tech lets brands share production lines and a global logistics network, cutting unit costs and improving fulfillment speed by ~18% year-over-year. It offers scalable infrastructure that enabled 120+ product launches in 2024 and supports rapid regional rollouts across 30+ countries.

Diverse Brand Portfolio

Cimpress runs brands like Pixartprinting, BuildASign and National Pen across 30+ countries, cutting single-brand exposure and supporting 2024 pro forma revenue of about €2.6 billion so risk is spread and cash flow steadier; each label keeps its market identity while sharing Cimpress tech, lowering per-brand R&D costs and improving gross margin — Pixartprinting alone served over 250,000 customers in 2024.

Advanced Supply Chain Efficiency

Cimpress runs a global, localized production network that cut average shipping distance and costs; in 2024 the company reported 31% of units fulfilled within 50 miles of customers, lowering logistics spend per order by about 12% versus 2019.

Producing near end users speeds delivery (median lead time ~3.8 days in FY2024) and trims CO2 emissions; rivals with smaller footprints struggle to match scale and unit economics.

- 31% of units fulfilled within 50 miles (2024)

- 12% lower logistics cost per order vs 2019

- Median lead time ~3.8 days (FY2024)

- Localized output reduces CO2 and improves margins

Data-Driven Customer Insights

With millions of transactions across Cimpress platforms—over 25 million orders in 2024—Cimpress holds rich data on buyer behavior and design trends, enabling precise product-market fit.

These insights drive targeted campaigns that cut customer acquisition cost; Cimpress reported a 12% YoY improvement in marketing ROI in 2024.

Personalization based on this data boosts customer lifetime value and repeat purchase rates, supporting margin resilience in a competitive market.

- 25M+ orders in 2024

- 12% YoY marketing ROI improvement (2024)

- Higher repeat rates via personalization

Cimpress: 35% SMB print share, €2.6bn revenue, 25M orders, 3.8‑day median lead time

Cimpress holds ~35% online SMB print share (end‑2025), drove ~€2.6bn pro forma revenue in 2024, processed 25M+ orders in 2024, and achieved a median lead time of ~3.8 days with 31% of units fulfilled within 50 miles, cutting logistics costs ~12% vs 2019 and lowering CAC ~18% vs mid‑market rivals.

| Metric | Value |

|---|---|

| Market share (online SMB) | ~35% (end‑2025) |

| Pro forma revenue | €2.6bn (2024) |

| Orders | 25M+ (2024) |

| Median lead time | ~3.8 days (FY2024) |

| Local fulfillment | 31% within 50 miles (2024) |

| Logistics cost change | −12% vs 2019 |

| CAC advantage | −18% vs mid‑market (2024–25) |

What is included in the product

Analyzes Cimpress’s competitive position by outlining its strengths, weaknesses, opportunities, and threats to provide a concise strategic overview of the company’s market advantages, operational gaps, and future risks.

Offers a concise Cimpress SWOT matrix for rapid strategic alignment, ideal for executives and teams needing a clear, visual snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Financial Leverage

Cimpress carries significant financial leverage after a decade of acquisitions and tech investment, with long-term debt of $1.12 billion and net debt around $940 million as of FY2024 (ended Sept 30, 2024). Interest expense of roughly $85 million in FY2024 reduces free cash flow and limits near-term reinvestment into emerging markets or disruptive tech. Leadership cites debt management and deleveraging as priorities to protect creditworthiness and long-term fiscal stability.

Compressed Profit Margins

The online printing sector’s intense price competition keeps gross margins under pressure; Cimpress reported a 2024 gross margin of ~36.5% (FY2024) versus peers at ~40%, forcing frequent aggressive discounting to defend market share, which squeezed adjusted EBITDA margin to 6.8% in FY2024. Balancing volume-led revenue growth with price integrity remains a key operational challenge in a crowded marketplace.

Operational Complexity

Managing Cimpress’ diverse portfolio—over 40 brands across 30+ countries—ties together legacy systems and cultures, creating integration hurdles that stretched SG&A to $1.1B in FY2024 and slowed group-wide initiatives; this complexity drove a 6% YoY increase in operating expenses in 2024 and longer decision cycles. Streamlining operations while keeping brand autonomy demands ongoing management focus and capital, risking slower scale benefits.

Dependence on Small Business Spending

- ~65% revenue from SMBs (2024)

- FY2023 revenue down 4.8% in key channels

- Enterprise shift = multi-year, capital-intensive

High Customer Acquisition Costs

Cimpress: High Debt, Thin Margins, Rising CACs and SMB Concentration

Cimpress carries high leverage (long-term debt $1.12B; net debt ~$940M FY2024), thin margins (gross ~36.5%; adj EBITDA 6.8% FY2024), heavy SMB exposure (~65% revenue FY2024) and rising customer acquisition costs (CPCs +15% YoY 2024; S&M $358M FY2024), plus integration complexity across 40+ brands slowing scale benefits.

| Metric | Value |

|---|---|

| Long-term debt | $1.12B |

| Net debt | $940M |

| Gross margin | 36.5% |

| Adj EBITDA | 6.8% |

| SMB revenue | ~65% |

| CPC change | +15% YoY 2024 |

| S&M | $358M FY2024 |

Preview the Actual Deliverable

Cimpress SWOT Analysis

This is the actual Cimpress SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.