Cineplex SWOT Analysis

Your Strategic Toolkit Starts Here

Cineplex’s strong brand, diversified entertainment offerings, and resilient market presence position it well amid shifting consumer behavior, but rising streaming competition, labour costs, and pandemic-era recovery risks demand strategic agility; uncover revenue levers, operational vulnerabilities, and growth pathways in our full SWOT. Purchase the complete analysis to receive a professionally formatted, editable Word report and Excel matrix—ready for investment decisions, strategic planning, or stakeholder presentations.

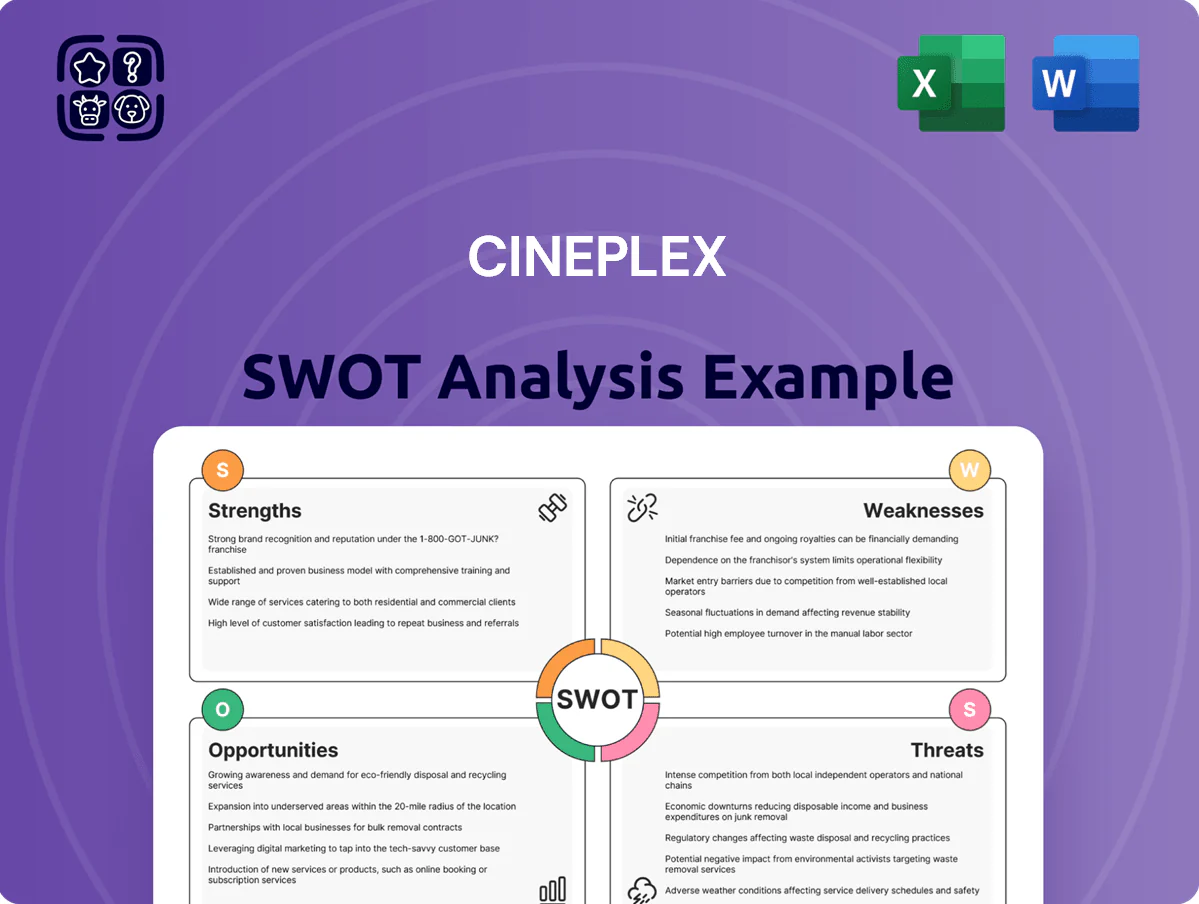

Strengths

Dominant Canadian Market Share

Cineplex controls about 75% of Canada’s box office, operating ~1,600 screens and generating CA$1.1B in 2023 revenue, giving it strong negotiating leverage with studios and suppliers.

That scale raises the cost for international entrants and secures preferable film windows and terms, supporting higher per-screen yields and concession margins.

The Cineplex brand is nearly synonymous with Canadian cinema, driving steady national foot traffic and repeat visits across its theatre network.

Diversified Revenue Streams

Cineplex has diversified beyond film exhibition into Location-Based Entertainment and media solutions, with venues like The Rec Room and Playdium contributing to non-box-office revenue; in FY2024 non-film revenues grew to ~39% of total revenue, up from 29% in FY2019. This reduces dependency on Hollywood release timing and cuts box-office volatility risk, while leveraging Cineplex’s hospitality and real-estate expertise across 160+ locations and ancillary sales (food, games, events) that raised per-visit spend by ~12% vs 2019.

Robust Scene Plus Loyalty Program

The Scene Plus loyalty program, run with Scotiabank and Empire Company, is among Canada’s largest with over 10 million members as of 2025 and drives meaningful cross-retail spend.

Its transaction and visit data give Cineplex granular insights into customer behaviour and spending patterns, enabling targeted marketing and personalized offers.

Scene Plus campaigns increased repeat visit rates and average ticket-plus-concession spend, contributing to double-digit growth in loyalty-derived revenue in recent quarters.

Premium Viewing Experience Portfolio

Cineplex has built a Premium Viewing Experience portfolio—IMAX, UltraAVX, VIP—that raised average ticket price by about 22% in 2024 vs standard screens, helping drive premium-attendee growth during FY2024 when premium admissions made up ~28% of box office revenue.

These formats attract higher-spend demographics willing to pay 30–60% more per ticket, letting Cineplex offset streaming competition by offering in-theatre tech and service that consumers can’t replicate at home.

- Premium formats: IMAX, UltraAVX, VIP

- Average premium price +22% (2024)

- Premium admissions ≈28% of box office (FY2024)

- Premium ticket uplift 30–60% vs standard

Integrated Media and Advertising Network

Cineplex Media runs a high-margin advertising network across 161 Canadian theatres and 14,000+ third-party digital out-of-home (DOOH) screens, giving advertisers captive reach in pre-show and venue environments.

The blend of cinema ads and digital signage delivers national-scale impressions and premium pricing; Cineplex reported media revenue of CAD 122.3 million in FY2024, up 8% year-over-year.

Unique value: targeted demographics, guaranteed view time, and cross-platform measurement for brands seeking broad Canadian reach.

- 161 theatres, 14,000+ third-party DOOH screens

- CAD 122.3M media revenue in FY2024 (+8% YoY)

- Captive pre-show audience with guaranteed view time

- Integrated measurement across cinema and DOOH

Cineplex: Canada’s 75% box-office titan — CA$1.1B rev, >10M Scene members

Cineplex dominates Canada’s box office (~75%), operates ~1,600 screens, CA$1.1B revenue (2023), and FY2024 non-film revenue ~39%; premium formats (IMAX/UltraAVX/VIP) drove +22% avg ticket and ~28% of box office; Scene Plus >10M members (2025) and Cineplex Media CAD122.3M (FY2024).

| Metric | Value |

|---|---|

| Box office share | ~75% |

| Screens | ~1,600 |

| Revenue (2023) | CA$1.1B |

| Non-film rev (FY2024) | ~39% |

| Premium ticket uplift (2024) | +22% |

| Premium share (FY2024) | ~28% |

| Scene Plus members (2025) | >10M |

| Media revenue (FY2024) | CAD122.3M |

What is included in the product

Provides a concise SWOT overview of Cineplex, highlighting its operational strengths, structural weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise Cineplex SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations.

Weaknesses

High Operational Fixed Costs

The Cineplex model carries heavy fixed costs from long-term leases and large-site maintenance; in 2024 rent and facility expenses represented about 28% of operating costs, so low attendance quickly hits margins. A 2023–24 slump in box office—Canadian admissions down ~9% year-over-year—showed EBITDA fell sharply during slow quarters, straining cash and credit lines. The chain needs high occupancy and steady per-guest spend (concessions up to 40% of ticket-era gross) to stay viable.

Heavy Dependency on Studio Output

Despite diversification into gaming and food services, Cineplex Inc. (TSE:CGX) still derives about 60% of box office-linked revenue from major Hollywood releases; that concentration makes quarterly EBITDA swing—Cineplex reported a 32% year-over-year box office drop in Q3 2024 when tentpole releases delayed.

Significant Debt Obligations

Cineplex holds significant debt—about CAD 650 million net debt as of Q3 2025—carried over from pre-pandemic expansion and recovery, and although net debt fell ~18% year-over-year, interest expense of CAD ~38 million YTD 2025 still eats into free cash flow.

Higher Canadian interest rates (Bank of Canada policy rate 5.00% in Dec 2025) raise servicing costs and tighten headroom, constraining capex like theatre retrofits and limiting agility for M&A or tech investments.

Geographic Concentration Risk

The company's operations are almost entirely concentrated in Canada, exposing Cineplex to domestic downturns and regulatory shifts; in 2024 roughly 95% of revenue came from Canada, so a national recession or provincial labor-law change would hit results hard.

Without international markets to offset weakness, Cineplex cannot diversify regionally, raising sensitivity to Canadian consumer debt (household credit-to-GDP ~175% in 2024) and provincial wage pressures.

This geographic concentration amplifies volatility: a 1% drop in Canadian box office (C$1.2bn market in 2024) would meaningfully cut Cineplex’s top line.

- ~95% revenue from Canada (2024)

- Canadian box office ≈ C$1.2bn (2024)

- Household credit-to-GDP ~175% (2024)

- No international operations to hedge regional shocks

Exposure to Rising Labor Costs

Cineplex faces rising labor-cost exposure: provincial minimum wages in Canada rose to $16.55–$17.50/hour in 2024 in key provinces, and labor is ~30–40% of theater operating costs, squeezing concession margins and EBITDA.

Automation (self-service kiosks, mobile ordering) cuts cashier hours, but VIP dining and event venues still require skilled staff, keeping a hard labor-cost floor and limiting full offset.

- 2024 min wages up to $17.50/hr

- Labor ~30–40% of operating costs

- Automation reduces but doesn’t eliminate labor

- VIP services sustain baseline staffing

High rent, heavy debt and Canada concentration make margins hostage to box‑office swings

Heavy fixed costs and lease burden (rent ~28% of ops in 2024) make margins highly attendance-sensitive; Q3 2024 box-office slump cut EBITDA sharply. Revenue concentration—~95% Canada, ~60% box-office-linked—amplifies quarter-to-quarter swings when tentpoles delay. Net debt ~CAD 650M (Q3 2025) and interest ~CAD 38M YTD 2025 limit capex; rising wages (up to CAD 17.50/hr in 2024) keep labor at ~30–40% of ops.

| Metric | Value |

|---|---|

| Canada revenue share (2024) | ~95% |

| Net debt (Q3 2025) | CAD 650M |

| Interest expense YTD 2025 | CAD 38M |

| Rent & facility (2024) | ~28% ops |

| Labor cost share | ~30–40% |

| Min wage (key provinces, 2024) | CAD 16.55–17.50/hr |

Same Document Delivered

Cineplex SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content you’ll download after payment. Buy now to unlock the complete, detailed Cineplex SWOT analysis ready for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Cineplex’s strong brand, diversified entertainment offerings, and resilient market presence position it well amid shifting consumer behavior, but rising streaming competition, labour costs, and pandemic-era recovery risks demand strategic agility; uncover revenue levers, operational vulnerabilities, and growth pathways in our full SWOT. Purchase the complete analysis to receive a professionally formatted, editable Word report and Excel matrix—ready for investment decisions, strategic planning, or stakeholder presentations.

Strengths

Dominant Canadian Market Share

Cineplex controls about 75% of Canada’s box office, operating ~1,600 screens and generating CA$1.1B in 2023 revenue, giving it strong negotiating leverage with studios and suppliers.

That scale raises the cost for international entrants and secures preferable film windows and terms, supporting higher per-screen yields and concession margins.

The Cineplex brand is nearly synonymous with Canadian cinema, driving steady national foot traffic and repeat visits across its theatre network.

Diversified Revenue Streams

Cineplex has diversified beyond film exhibition into Location-Based Entertainment and media solutions, with venues like The Rec Room and Playdium contributing to non-box-office revenue; in FY2024 non-film revenues grew to ~39% of total revenue, up from 29% in FY2019. This reduces dependency on Hollywood release timing and cuts box-office volatility risk, while leveraging Cineplex’s hospitality and real-estate expertise across 160+ locations and ancillary sales (food, games, events) that raised per-visit spend by ~12% vs 2019.

Robust Scene Plus Loyalty Program

The Scene Plus loyalty program, run with Scotiabank and Empire Company, is among Canada’s largest with over 10 million members as of 2025 and drives meaningful cross-retail spend.

Its transaction and visit data give Cineplex granular insights into customer behaviour and spending patterns, enabling targeted marketing and personalized offers.

Scene Plus campaigns increased repeat visit rates and average ticket-plus-concession spend, contributing to double-digit growth in loyalty-derived revenue in recent quarters.

Premium Viewing Experience Portfolio

Cineplex has built a Premium Viewing Experience portfolio—IMAX, UltraAVX, VIP—that raised average ticket price by about 22% in 2024 vs standard screens, helping drive premium-attendee growth during FY2024 when premium admissions made up ~28% of box office revenue.

These formats attract higher-spend demographics willing to pay 30–60% more per ticket, letting Cineplex offset streaming competition by offering in-theatre tech and service that consumers can’t replicate at home.

- Premium formats: IMAX, UltraAVX, VIP

- Average premium price +22% (2024)

- Premium admissions ≈28% of box office (FY2024)

- Premium ticket uplift 30–60% vs standard

Integrated Media and Advertising Network

Cineplex Media runs a high-margin advertising network across 161 Canadian theatres and 14,000+ third-party digital out-of-home (DOOH) screens, giving advertisers captive reach in pre-show and venue environments.

The blend of cinema ads and digital signage delivers national-scale impressions and premium pricing; Cineplex reported media revenue of CAD 122.3 million in FY2024, up 8% year-over-year.

Unique value: targeted demographics, guaranteed view time, and cross-platform measurement for brands seeking broad Canadian reach.

- 161 theatres, 14,000+ third-party DOOH screens

- CAD 122.3M media revenue in FY2024 (+8% YoY)

- Captive pre-show audience with guaranteed view time

- Integrated measurement across cinema and DOOH

Cineplex: Canada’s 75% box-office titan — CA$1.1B rev, >10M Scene members

Cineplex dominates Canada’s box office (~75%), operates ~1,600 screens, CA$1.1B revenue (2023), and FY2024 non-film revenue ~39%; premium formats (IMAX/UltraAVX/VIP) drove +22% avg ticket and ~28% of box office; Scene Plus >10M members (2025) and Cineplex Media CAD122.3M (FY2024).

| Metric | Value |

|---|---|

| Box office share | ~75% |

| Screens | ~1,600 |

| Revenue (2023) | CA$1.1B |

| Non-film rev (FY2024) | ~39% |

| Premium ticket uplift (2024) | +22% |

| Premium share (FY2024) | ~28% |

| Scene Plus members (2025) | >10M |

| Media revenue (FY2024) | CAD122.3M |

What is included in the product

Provides a concise SWOT overview of Cineplex, highlighting its operational strengths, structural weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise Cineplex SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations.

Weaknesses

High Operational Fixed Costs

The Cineplex model carries heavy fixed costs from long-term leases and large-site maintenance; in 2024 rent and facility expenses represented about 28% of operating costs, so low attendance quickly hits margins. A 2023–24 slump in box office—Canadian admissions down ~9% year-over-year—showed EBITDA fell sharply during slow quarters, straining cash and credit lines. The chain needs high occupancy and steady per-guest spend (concessions up to 40% of ticket-era gross) to stay viable.

Heavy Dependency on Studio Output

Despite diversification into gaming and food services, Cineplex Inc. (TSE:CGX) still derives about 60% of box office-linked revenue from major Hollywood releases; that concentration makes quarterly EBITDA swing—Cineplex reported a 32% year-over-year box office drop in Q3 2024 when tentpole releases delayed.

Significant Debt Obligations

Cineplex holds significant debt—about CAD 650 million net debt as of Q3 2025—carried over from pre-pandemic expansion and recovery, and although net debt fell ~18% year-over-year, interest expense of CAD ~38 million YTD 2025 still eats into free cash flow.

Higher Canadian interest rates (Bank of Canada policy rate 5.00% in Dec 2025) raise servicing costs and tighten headroom, constraining capex like theatre retrofits and limiting agility for M&A or tech investments.

Geographic Concentration Risk

The company's operations are almost entirely concentrated in Canada, exposing Cineplex to domestic downturns and regulatory shifts; in 2024 roughly 95% of revenue came from Canada, so a national recession or provincial labor-law change would hit results hard.

Without international markets to offset weakness, Cineplex cannot diversify regionally, raising sensitivity to Canadian consumer debt (household credit-to-GDP ~175% in 2024) and provincial wage pressures.

This geographic concentration amplifies volatility: a 1% drop in Canadian box office (C$1.2bn market in 2024) would meaningfully cut Cineplex’s top line.

- ~95% revenue from Canada (2024)

- Canadian box office ≈ C$1.2bn (2024)

- Household credit-to-GDP ~175% (2024)

- No international operations to hedge regional shocks

Exposure to Rising Labor Costs

Cineplex faces rising labor-cost exposure: provincial minimum wages in Canada rose to $16.55–$17.50/hour in 2024 in key provinces, and labor is ~30–40% of theater operating costs, squeezing concession margins and EBITDA.

Automation (self-service kiosks, mobile ordering) cuts cashier hours, but VIP dining and event venues still require skilled staff, keeping a hard labor-cost floor and limiting full offset.

- 2024 min wages up to $17.50/hr

- Labor ~30–40% of operating costs

- Automation reduces but doesn’t eliminate labor

- VIP services sustain baseline staffing

High rent, heavy debt and Canada concentration make margins hostage to box‑office swings

Heavy fixed costs and lease burden (rent ~28% of ops in 2024) make margins highly attendance-sensitive; Q3 2024 box-office slump cut EBITDA sharply. Revenue concentration—~95% Canada, ~60% box-office-linked—amplifies quarter-to-quarter swings when tentpoles delay. Net debt ~CAD 650M (Q3 2025) and interest ~CAD 38M YTD 2025 limit capex; rising wages (up to CAD 17.50/hr in 2024) keep labor at ~30–40% of ops.

| Metric | Value |

|---|---|

| Canada revenue share (2024) | ~95% |

| Net debt (Q3 2025) | CAD 650M |

| Interest expense YTD 2025 | CAD 38M |

| Rent & facility (2024) | ~28% ops |

| Labor cost share | ~30–40% |

| Min wage (key provinces, 2024) | CAD 16.55–17.50/hr |

Same Document Delivered

Cineplex SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content you’ll download after payment. Buy now to unlock the complete, detailed Cineplex SWOT analysis ready for immediate use.