CITIC Telecom International Holdings Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

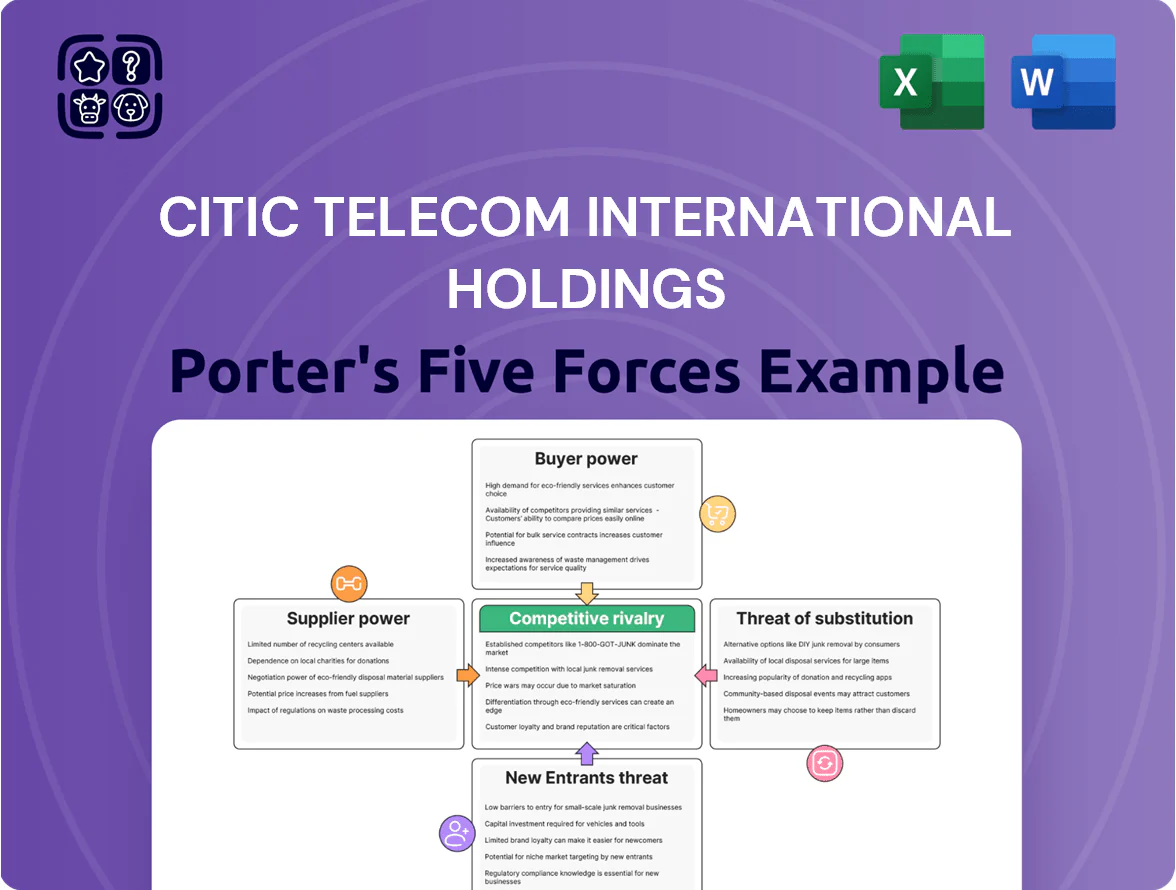

CITIC Telecom International operates in a capital-intensive, consolidation-prone telecom services market where buyer price sensitivity, regulatory oversight, and technological disruption shape competitive dynamics; supplier leverage for network equipment and skilled talent raises costs while moderate entry barriers limit newcomers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for smarter investment and planning.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

The company relies on a small set of global vendors for 5G and specialized networking hardware; by late 2025 Huawei, ZTE and Ericsson together held roughly 60–70% of core RAN market share, raising CITIC Telecom’s supplier dependency for critical maintenance and upgrades.

This concentration reduces CITIC Telecom’s bargaining leverage, limits price negotiation—vendor markup power can add 5–15% to capex—and slows shifts to alternative standards or suppliers when interoperability or regulatory issues arise.

Rising Energy Costs for Data Center Operations

Energy utilities hold strong leverage as CITIC Telecom expands data centers in Asia and Europe; power typically accounts for 30–40% of colocation OPEX and a 10% price rise in 2024 would cut margins materially.

High-performance compute and cooling drive peak loads: a 10 MW site can consume ~80 GWh/year, exposing CITIC to wholesale price swings seen in Europe (wholesale average €120/MWh in 2022–24 peaks).

Investing in on-site renewables and PPAs can lower exposure; PPA deals reduced buyer costs 15–25% in APAC pilots 2023–25, so renewables are strategic to curb utility pricing power.

Scarcity of International Submarine Cable Capacity

Suppliers of undersea cable bandwidth and maintenance hold strong leverage because global routes are physically limited: there were about 1.4 million km of active subsea cable in 2024, concentrated among a few consortiums, so CITIC Telecom must secure long-term leases or equity stakes in cables like APCN-2 or new Asia-Europe links to guarantee transit. New cable builds cost $200m–$500m for typical routes, keeping incumbents’ pricing power high and raising operating costs if capacity isn’t pre-booked.

Specialized Talent and Software Licensing

The move to software-defined networking and AI services raises CITIC Telecom’s dependence on niche software vendors and cloud platforms; Gartner reported 2024 enterprise software subscription price increases averaging 6.3% year-over-year, pressuring margins.

Subscription licensing permits periodic price hikes, and a 2023 ISC2 report found a 3.4 million global shortfall in cybersecurity roles, boosting wage demands for specialized AI/cyber talent and supplier leverage.

- 6.3% average software subscription price rise (Gartner 2024)

- 3.4M global cybersecurity workforce gap (ISC2 2023)

- Subscription models enable periodic price increases

- Specialized talent shortages push up compensation

Dependency on Local Access Providers

In markets where CITIC Telecom acts as a virtual operator, it must lease last-mile lines from local incumbents that often hold monopoly/duopoly control; those incumbents set wholesale rates, creating cost exposure that can reduce margins on enterprise services and mobile roaming.

For example, in 2024 average wholesale access premiums in Southeast Asia ranged 15–35% above competitive rates, and if CITIC Telecom faces a 20% higher access cost, its roaming gross margin can shrink by ~4–6 percentage points on average.

Suppliers dominate: concentrated RAN, costly power & subsea, rising software and security gaps

Suppliers (RAN vendors, power, subsea cables, software, last-mile incumbents) have high bargaining power: vendor concentration (Huawei/ZTE/Ericsson 60–70% RAN share by 2025), power = 30–40% colo OPEX, European wholesale peaks €120/MWh (2022–24), subsea build $200–$500m, software +6.3% YoY (Gartner 2024), cybersecurity gap 3.4M (ISC2 2023).

| Supplier | Metric |

|---|---|

| RAN vendors | 60–70% market share (2025) |

| Power | 30–40% colo OPEX; €120/MWh peak |

| Subsea | $200–$500m build cost |

| Software | +6.3% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for CITIC Telecom International Holdings uncovering key competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats shaping its telecom services and international carrier positioning.

A concise Porter's Five Forces snapshot for CITIC Telecom—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

High Volume Demands of Multinational Corporations

Large enterprise clients and multinational corporations (MNCs) account for roughly 55–65% of CITIC Telecom International Holdings’ revenue, giving them strong bargaining power through scale and contract value.

These buyers run competitive bids, pressuring CITIC to cut prices and improve SLAs; in 2024 several global tenders drove average contract margins down by about 120–180 basis points.

The option to consolidate global traffic with one provider amplifies leverage, since a single global contract can represent millions of dollars in annual recurring revenue for CITIC.

Low Switching Costs in the Retail Mobile Segment

In Macau, CITIC Telecom’s CTM faces low switching costs due to regulatory mobile number portability introduced in 2012, enabling consumers to port numbers within 24 hours and fueling churn—Macau’s retail mobile churn averaged about 18% in 2024 per industry reports. This ease of switching forces CTM to spend on loyalty schemes and promotional bundles; CTM allocated roughly MOP 45–60 million to retail marketing in 2023–24 to defend market share. If network performance slips versus rivals, customers can defect quickly, so sustained capex and targeted offers remain critical.

Price Sensitivity in International Wholesale Carrier Services

Global carriers buying wholesale voice and data face a transparent, commoditized market where price discovery is near-instant; industry reports show interconnect rates can vary by micro-cents and 70–80% of traffic shifts toward the lowest-cost routes within weeks. This price sensitivity forces CITIC Telecom International Holdings to drive sub-0.5% margin improvements via automation, network optimization, and volume discounts to stay the preferred partner.

Customization Requirements for Smart City Solutions

Government and institutional buyers now demand highly customized smart-city and IoT solutions, forcing CITIC Telecom to absorb higher R&D and integration costs; public-sector projects in Asia-Pacific grew 12% y/y to about $48B in 2024, raising contract complexity.

These buyers have in-house technical teams to compare vendors and insist on bespoke features, increasing switching power and pressuring margins—CITIC Telecom may face 5–8% lower gross margins on such contracts.

Their policy influence and control over multi-year infrastructure plans give them strategic leverage, affecting vendor selection and long-term revenue visibility for carriers and integrators.

- 2024 APAC public smart-city spend ~$48B, +12% y/y

- Customization can cut provider gross margins 5–8%

- Buyers’ technical teams increase vendor switching power

- Policy control boosts buyers’ long-term leverage

Impact of Economic Volatility on Corporate Spending

During 2024–2025 regional economic uncertainty, many corporate clients cut digital transformation spend—APAC IT budgets fell ~3.2% in 2024 per IDC—so buyers press for flexible payment terms and downgraded service tiers.

CITIC Telecom must pivot to cost-saving propositions—highlight network consolidation, cloud-cost optimization, and managed services—to retain price-sensitive buyers and protect revenue.

- APAC IT spend down ~3.2% in 2024 (IDC)

- Buyers demand flexible terms, longer payment cycles

- Offerings: network consolidation, cloud cost ops, managed services

- Goal: preserve ARR and reduce churn among budget-conscious clients

Margin squeeze: Enterprise power, retail churn & custom APAC smart‑city costs bite profits

Large enterprise/MNCs (55–65% revenue) and wholesale buyers exert high bargaining power, forcing price cuts (avg margins -120–180bps in 2024) and rapid route-shifting (70–80% traffic to lowest-cost routes). Retail churn in Macau hit ~18% in 2024, driving CTM marketing spend MOP 45–60M. APAC public smart-city spend ~$48B (+12% y/y) increases customization pressure, cutting gross margins 5–8%.

| Metric | 2024 value |

|---|---|

| Enterprise revenue share | 55–65% |

| Contract margin impact | -120–180 bps |

| Macau retail churn | ~18% |

| CTM retail marketing | MOP 45–60M |

| Wholesale traffic shift | 70–80% |

| APAC smart-city spend | $48B (+12% y/y) |

| Customization margin hit | 5–8% |

Full Version Awaits

CITIC Telecom International Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for CITIC Telecom International Holdings that you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable: concise competitive threat assessment, bargaining power insights, and strategic implications tailored to CITIC Telecom. No mockups or samples—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CITIC Telecom International operates in a capital-intensive, consolidation-prone telecom services market where buyer price sensitivity, regulatory oversight, and technological disruption shape competitive dynamics; supplier leverage for network equipment and skilled talent raises costs while moderate entry barriers limit newcomers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for smarter investment and planning.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

The company relies on a small set of global vendors for 5G and specialized networking hardware; by late 2025 Huawei, ZTE and Ericsson together held roughly 60–70% of core RAN market share, raising CITIC Telecom’s supplier dependency for critical maintenance and upgrades.

This concentration reduces CITIC Telecom’s bargaining leverage, limits price negotiation—vendor markup power can add 5–15% to capex—and slows shifts to alternative standards or suppliers when interoperability or regulatory issues arise.

Rising Energy Costs for Data Center Operations

Energy utilities hold strong leverage as CITIC Telecom expands data centers in Asia and Europe; power typically accounts for 30–40% of colocation OPEX and a 10% price rise in 2024 would cut margins materially.

High-performance compute and cooling drive peak loads: a 10 MW site can consume ~80 GWh/year, exposing CITIC to wholesale price swings seen in Europe (wholesale average €120/MWh in 2022–24 peaks).

Investing in on-site renewables and PPAs can lower exposure; PPA deals reduced buyer costs 15–25% in APAC pilots 2023–25, so renewables are strategic to curb utility pricing power.

Scarcity of International Submarine Cable Capacity

Suppliers of undersea cable bandwidth and maintenance hold strong leverage because global routes are physically limited: there were about 1.4 million km of active subsea cable in 2024, concentrated among a few consortiums, so CITIC Telecom must secure long-term leases or equity stakes in cables like APCN-2 or new Asia-Europe links to guarantee transit. New cable builds cost $200m–$500m for typical routes, keeping incumbents’ pricing power high and raising operating costs if capacity isn’t pre-booked.

Specialized Talent and Software Licensing

The move to software-defined networking and AI services raises CITIC Telecom’s dependence on niche software vendors and cloud platforms; Gartner reported 2024 enterprise software subscription price increases averaging 6.3% year-over-year, pressuring margins.

Subscription licensing permits periodic price hikes, and a 2023 ISC2 report found a 3.4 million global shortfall in cybersecurity roles, boosting wage demands for specialized AI/cyber talent and supplier leverage.

- 6.3% average software subscription price rise (Gartner 2024)

- 3.4M global cybersecurity workforce gap (ISC2 2023)

- Subscription models enable periodic price increases

- Specialized talent shortages push up compensation

Dependency on Local Access Providers

In markets where CITIC Telecom acts as a virtual operator, it must lease last-mile lines from local incumbents that often hold monopoly/duopoly control; those incumbents set wholesale rates, creating cost exposure that can reduce margins on enterprise services and mobile roaming.

For example, in 2024 average wholesale access premiums in Southeast Asia ranged 15–35% above competitive rates, and if CITIC Telecom faces a 20% higher access cost, its roaming gross margin can shrink by ~4–6 percentage points on average.

Suppliers dominate: concentrated RAN, costly power & subsea, rising software and security gaps

Suppliers (RAN vendors, power, subsea cables, software, last-mile incumbents) have high bargaining power: vendor concentration (Huawei/ZTE/Ericsson 60–70% RAN share by 2025), power = 30–40% colo OPEX, European wholesale peaks €120/MWh (2022–24), subsea build $200–$500m, software +6.3% YoY (Gartner 2024), cybersecurity gap 3.4M (ISC2 2023).

| Supplier | Metric |

|---|---|

| RAN vendors | 60–70% market share (2025) |

| Power | 30–40% colo OPEX; €120/MWh peak |

| Subsea | $200–$500m build cost |

| Software | +6.3% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for CITIC Telecom International Holdings uncovering key competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats shaping its telecom services and international carrier positioning.

A concise Porter's Five Forces snapshot for CITIC Telecom—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

High Volume Demands of Multinational Corporations

Large enterprise clients and multinational corporations (MNCs) account for roughly 55–65% of CITIC Telecom International Holdings’ revenue, giving them strong bargaining power through scale and contract value.

These buyers run competitive bids, pressuring CITIC to cut prices and improve SLAs; in 2024 several global tenders drove average contract margins down by about 120–180 basis points.

The option to consolidate global traffic with one provider amplifies leverage, since a single global contract can represent millions of dollars in annual recurring revenue for CITIC.

Low Switching Costs in the Retail Mobile Segment

In Macau, CITIC Telecom’s CTM faces low switching costs due to regulatory mobile number portability introduced in 2012, enabling consumers to port numbers within 24 hours and fueling churn—Macau’s retail mobile churn averaged about 18% in 2024 per industry reports. This ease of switching forces CTM to spend on loyalty schemes and promotional bundles; CTM allocated roughly MOP 45–60 million to retail marketing in 2023–24 to defend market share. If network performance slips versus rivals, customers can defect quickly, so sustained capex and targeted offers remain critical.

Price Sensitivity in International Wholesale Carrier Services

Global carriers buying wholesale voice and data face a transparent, commoditized market where price discovery is near-instant; industry reports show interconnect rates can vary by micro-cents and 70–80% of traffic shifts toward the lowest-cost routes within weeks. This price sensitivity forces CITIC Telecom International Holdings to drive sub-0.5% margin improvements via automation, network optimization, and volume discounts to stay the preferred partner.

Customization Requirements for Smart City Solutions

Government and institutional buyers now demand highly customized smart-city and IoT solutions, forcing CITIC Telecom to absorb higher R&D and integration costs; public-sector projects in Asia-Pacific grew 12% y/y to about $48B in 2024, raising contract complexity.

These buyers have in-house technical teams to compare vendors and insist on bespoke features, increasing switching power and pressuring margins—CITIC Telecom may face 5–8% lower gross margins on such contracts.

Their policy influence and control over multi-year infrastructure plans give them strategic leverage, affecting vendor selection and long-term revenue visibility for carriers and integrators.

- 2024 APAC public smart-city spend ~$48B, +12% y/y

- Customization can cut provider gross margins 5–8%

- Buyers’ technical teams increase vendor switching power

- Policy control boosts buyers’ long-term leverage

Impact of Economic Volatility on Corporate Spending

During 2024–2025 regional economic uncertainty, many corporate clients cut digital transformation spend—APAC IT budgets fell ~3.2% in 2024 per IDC—so buyers press for flexible payment terms and downgraded service tiers.

CITIC Telecom must pivot to cost-saving propositions—highlight network consolidation, cloud-cost optimization, and managed services—to retain price-sensitive buyers and protect revenue.

- APAC IT spend down ~3.2% in 2024 (IDC)

- Buyers demand flexible terms, longer payment cycles

- Offerings: network consolidation, cloud cost ops, managed services

- Goal: preserve ARR and reduce churn among budget-conscious clients

Margin squeeze: Enterprise power, retail churn & custom APAC smart‑city costs bite profits

Large enterprise/MNCs (55–65% revenue) and wholesale buyers exert high bargaining power, forcing price cuts (avg margins -120–180bps in 2024) and rapid route-shifting (70–80% traffic to lowest-cost routes). Retail churn in Macau hit ~18% in 2024, driving CTM marketing spend MOP 45–60M. APAC public smart-city spend ~$48B (+12% y/y) increases customization pressure, cutting gross margins 5–8%.

| Metric | 2024 value |

|---|---|

| Enterprise revenue share | 55–65% |

| Contract margin impact | -120–180 bps |

| Macau retail churn | ~18% |

| CTM retail marketing | MOP 45–60M |

| Wholesale traffic shift | 70–80% |

| APAC smart-city spend | $48B (+12% y/y) |

| Customization margin hit | 5–8% |

Full Version Awaits

CITIC Telecom International Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for CITIC Telecom International Holdings that you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable: concise competitive threat assessment, bargaining power insights, and strategic implications tailored to CITIC Telecom. No mockups or samples—what you see is what you get.