City Union Bank Business Model Canvas

City Union Bank Business Model Canvas: Profitable Blueprint for Investors & Strategists

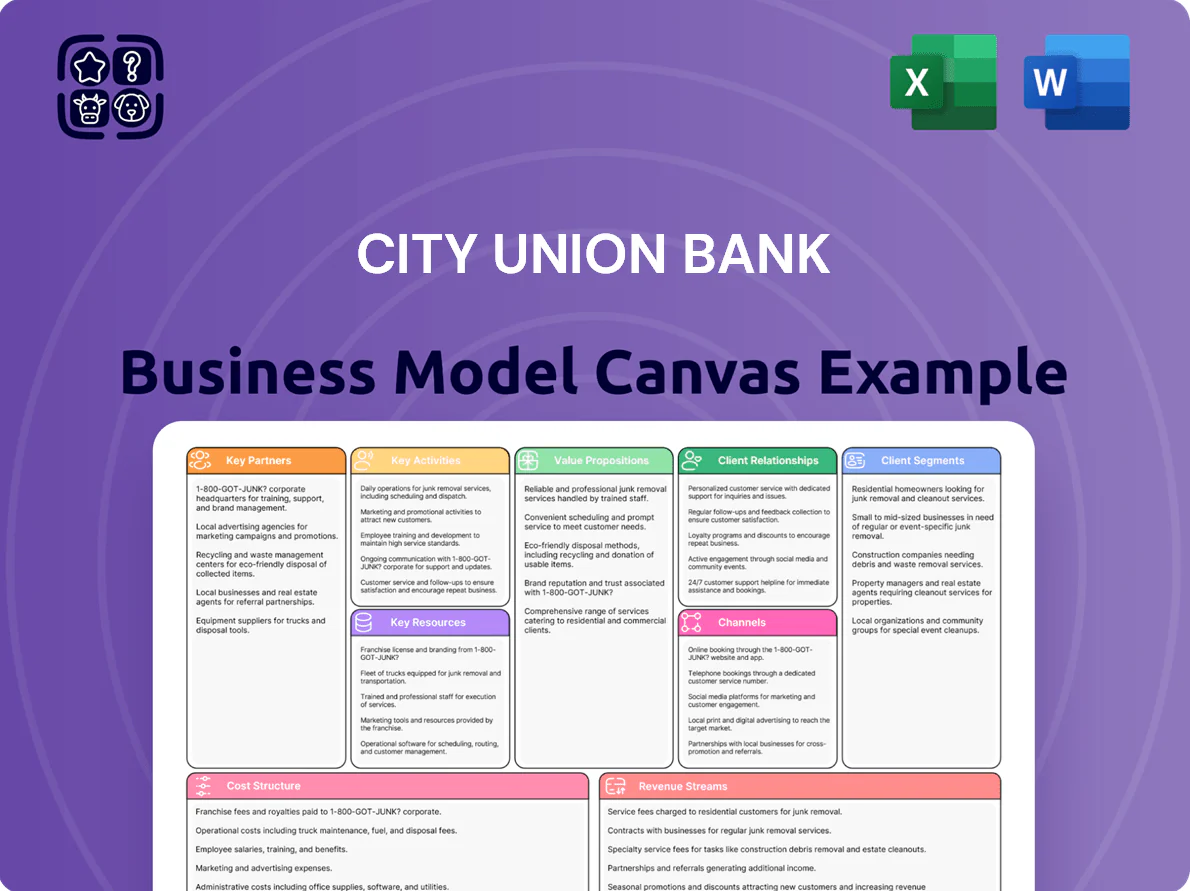

Unlock the full strategic blueprint behind City Union Bank’s business model — this concise Business Model Canvas reveals how the bank creates customer value, monetizes core services, and leverages partnerships to grow profitably; ideal for investors, consultants, and founders seeking actionable, bank-specific insights.

Partnerships

Strategic Fintech Collaborations

City Union Bank partners with fintechs to embed digital payments and alternative credit scoring, cutting MSME loan approval times from ~14 days to under 4 days in 2025 and lifting digital loan disbursals to 28% of retail book by Q3 2025.

Bancassurance and Third-Party Providers

City Union Bank partners with major insurers (HDFC Life, ICICI Prudential) and mutual fund houses (Nippon India, SBI Mutual) to distribute products, earning commission income; bancassurance and third-party fees helped lift non-interest income to about 22% of total revenue in FY2024, supporting one-stop financial solutions for customers.

Regulatory and Clearing House Alliances

City Union Bank partners with the Reserve Bank of India and the National Payments Corporation of India to keep transaction processing compliant and seamless; as of FY2024 the bank supported over 12 million UPI transactions monthly and processed 3.2 million Bharat BillPay transactions in 2024, ensuring its systems align with evolving RBI guidelines and the national digital payments stack.

Technology and Infrastructure Vendors

City Union Bank partners with global and domestic IT vendors for core banking hardware/software and cybersecurity, with vendors supporting 99.95%+ uptime targets and handling peak loads from 5–7x transaction spikes during festivals (FY2024 peak traffic data).

These ties run on multi-year SLAs—commonly 3–5 years—covering incident MTTR targets (under 1 hour), regular patching, and compliance audits to protect customer data and ensure continuous operations.

- 99.95% uptime target

- 3–5 year SLAs

- MTTR ≤ 1 hour

- 5–7x peak traffic handling

Correspondent Banking Networks

City Union Bank runs correspondent banking ties with foreign banks in London, Dubai, Singapore, and New York to process remittances and trade flows; in FY2024 the bank handled about 18,500 outward remittances and supported export-import credit lines totaling ~INR 2.1 billion.

This network enables FX services and trade finance for corporates and NRI clients, shortening settlement times and widening currency corridors.

- Coverage: London, Dubai, Singapore, New York

- Remittances FY2024: ~18,500 outward

- Trade credit supported: ~INR 2.1 billion

- Services: FX, letters of credit, collection

City Union Bank: <4-day MSME approvals, 28% digital loans, 12M UPI/mo, 99.95% uptime

City Union Bank’s partners—fintechs, insurers, AMCs, RBI/NPCI, IT vendors, correspondent banks—cut MSME loan approval to <4 days (2025), lifted digital disbursals to 28% (Q3 2025), ran 12M UPI txns/mo (FY2024), 3.2M Bharat BillPay txns (2024), 99.95% uptime, MTTR ≤1h, 3–5yr SLAs, ~18,500 outward remittances and ~INR 2.1bn trade credit (FY2024).

| Metric | Value |

|---|---|

| MSME approval time | <4 days (2025) |

| Digital loan disbursal | 28% retail book (Q3 2025) |

| UPI txns/month | 12M (FY2024) |

| Bharat BillPay txns | 3.2M (2024) |

| Uptime | 99.95% |

| SLAs | 3–5 years |

| MTTR | ≤1 hour |

| Outward remittances | ~18,500 (FY2024) |

| Trade credit supported | ~INR 2.1bn (FY2024) |

What is included in the product

A concise, investor-ready Business Model Canvas for City Union Bank detailing customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure, and risk factors, reflecting its retail and SME-focused operations and competitive strengths for presentations and strategic analysis.

Condenses City Union Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready insights.

Activities

Credit Disbursement and Risk Management

City Union Bank focuses on assessing creditworthiness and disbursing loans to retail, agriculture, and MSME clients, with gross advances of ₹91,200 crore as of FY2024‑25 supporting this mix. The bank combines traditional underwriting with AI-driven analytics to keep GNPA at 1.05% (FY2024‑25) and conducts continuous portfolio monitoring to maintain CRAR above 15% under 2025 market conditions.

Deposit Mobilization and Management

City Union Bank prioritizes low-cost CASA (current and savings) to keep cost of funds low, reporting a CASA ratio of 37.8% and CASA deposits of ₹32,400 crore as of FY2024; it targets retail segments with age-tailored savings and institutional term deposits to widen this base.

The bank uses active liquidity management—maintaining LCR (liquidity coverage ratio) above regulatory levels and optimizing an investment book of ~₹48,000 crore in FY2024—to meet withdrawals while maximizing yield.

Digital Transformation and IT Maintenance

City Union Bank prioritizes continuous upgrades to its mobile app and internet banking portal—supporting 8.2 million digital customers as of FY2024 and targeting a 15% YoY increase in active digital users—while automating back‑end processes (RPA and straight‑through processing) to cut manual errors and reduce processing costs by an estimated 12%. Daily cybersecurity operations protect customer assets against rising fraud: the bank reported a 28% year‑on‑year increase in attempted digital fraud blocks in 2024, prompting sustained investment in SOC and threat intelligence.

Customer Service and Relationship Building

City Union Bank delivers personalized service via 730+ branches and digital helpdesks; staff handle complex queries and advisory work for SMEs, supporting ~18% of loan book to micro/small enterprises as of FY2024–25.

Customer-service focus drives high loyalty—CASA ratio 36.8% and 2025 NPS ~58 in regional surveys, aiding stable retail deposit growth of 9% YoY.

- 730+ branches + digital helpdesks

- 18% loan book to micro/small firms

- CASA 36.8% (FY2024–25)

- NPS ~58 (2025 regional survey)

- Retail deposit growth 9% YoY

Compliance and Regulatory Reporting

City Union Bank must follow KYC, Anti-Money Laundering (AML), and Basel III capital and liquidity norms, filing regular reports and statutory returns to the Reserve Bank of India; in 2025 the bank allocates ~12% of compliance budget to AML tech after a 28% rise in SAR filings in 2024.

Regular internal and external audits ensure transparency and trust; compliance teams produce quarterly returns, with RBI-directed reporting frequency up to weekly for select risk metrics, driving significant administrative workload to track evolving 2025 rules.

- KYC/AML adherence

- Basel III capital & liquidity reporting

- Quarterly/weekly RBI returns

- 12% budget to AML tech (2025)

- 28% rise in SARs (2024)

Strong CASA-led lending (₹91,200cr) with low GNPA (1.05%) and 8.2M digital users

Key activities: underwriting and disbursing ₹91,200 crore gross advances (FY2024‑25) across retail, agri, MSME; CASA-led funding (CASA 37.8%, ₹32,400 crore FY2024) and liquidity/investment management (LCR above regulatory, investment book ~₹48,000 crore FY2024); digital upgrades supporting 8.2m users and 730+ branches; compliance/AML (12% compliance budget 2025) keeping GNPA 1.05%.

| Metric | Value |

|---|---|

| Gross advances | ₹91,200 cr (FY2024‑25) |

| CASA | 37.8%, ₹32,400 cr (FY2024) |

| Investment book | ~₹48,000 cr (FY2024) |

| Digital users | 8.2M (FY2024) |

| Branches | 730+ |

| GNPA | 1.05% (FY2024‑25) |

| AML budget | 12% (2025) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual City Union Bank Business Model Canvas—not a mockup or sample—and reflects the exact content and structure included in the final deliverable.

When you complete your purchase, you’ll receive this same professional, ready-to-use file in editable formats, with all sections, layouts, and content preserved as shown here.

No placeholders or hidden pages—what you see is what you’ll download and use immediately for analysis, presentation, or customization.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

City Union Bank Business Model Canvas: Profitable Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind City Union Bank’s business model — this concise Business Model Canvas reveals how the bank creates customer value, monetizes core services, and leverages partnerships to grow profitably; ideal for investors, consultants, and founders seeking actionable, bank-specific insights.

Partnerships

Strategic Fintech Collaborations

City Union Bank partners with fintechs to embed digital payments and alternative credit scoring, cutting MSME loan approval times from ~14 days to under 4 days in 2025 and lifting digital loan disbursals to 28% of retail book by Q3 2025.

Bancassurance and Third-Party Providers

City Union Bank partners with major insurers (HDFC Life, ICICI Prudential) and mutual fund houses (Nippon India, SBI Mutual) to distribute products, earning commission income; bancassurance and third-party fees helped lift non-interest income to about 22% of total revenue in FY2024, supporting one-stop financial solutions for customers.

Regulatory and Clearing House Alliances

City Union Bank partners with the Reserve Bank of India and the National Payments Corporation of India to keep transaction processing compliant and seamless; as of FY2024 the bank supported over 12 million UPI transactions monthly and processed 3.2 million Bharat BillPay transactions in 2024, ensuring its systems align with evolving RBI guidelines and the national digital payments stack.

Technology and Infrastructure Vendors

City Union Bank partners with global and domestic IT vendors for core banking hardware/software and cybersecurity, with vendors supporting 99.95%+ uptime targets and handling peak loads from 5–7x transaction spikes during festivals (FY2024 peak traffic data).

These ties run on multi-year SLAs—commonly 3–5 years—covering incident MTTR targets (under 1 hour), regular patching, and compliance audits to protect customer data and ensure continuous operations.

- 99.95% uptime target

- 3–5 year SLAs

- MTTR ≤ 1 hour

- 5–7x peak traffic handling

Correspondent Banking Networks

City Union Bank runs correspondent banking ties with foreign banks in London, Dubai, Singapore, and New York to process remittances and trade flows; in FY2024 the bank handled about 18,500 outward remittances and supported export-import credit lines totaling ~INR 2.1 billion.

This network enables FX services and trade finance for corporates and NRI clients, shortening settlement times and widening currency corridors.

- Coverage: London, Dubai, Singapore, New York

- Remittances FY2024: ~18,500 outward

- Trade credit supported: ~INR 2.1 billion

- Services: FX, letters of credit, collection

City Union Bank: <4-day MSME approvals, 28% digital loans, 12M UPI/mo, 99.95% uptime

City Union Bank’s partners—fintechs, insurers, AMCs, RBI/NPCI, IT vendors, correspondent banks—cut MSME loan approval to <4 days (2025), lifted digital disbursals to 28% (Q3 2025), ran 12M UPI txns/mo (FY2024), 3.2M Bharat BillPay txns (2024), 99.95% uptime, MTTR ≤1h, 3–5yr SLAs, ~18,500 outward remittances and ~INR 2.1bn trade credit (FY2024).

| Metric | Value |

|---|---|

| MSME approval time | <4 days (2025) |

| Digital loan disbursal | 28% retail book (Q3 2025) |

| UPI txns/month | 12M (FY2024) |

| Bharat BillPay txns | 3.2M (2024) |

| Uptime | 99.95% |

| SLAs | 3–5 years |

| MTTR | ≤1 hour |

| Outward remittances | ~18,500 (FY2024) |

| Trade credit supported | ~INR 2.1bn (FY2024) |

What is included in the product

A concise, investor-ready Business Model Canvas for City Union Bank detailing customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure, and risk factors, reflecting its retail and SME-focused operations and competitive strengths for presentations and strategic analysis.

Condenses City Union Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready insights.

Activities

Credit Disbursement and Risk Management

City Union Bank focuses on assessing creditworthiness and disbursing loans to retail, agriculture, and MSME clients, with gross advances of ₹91,200 crore as of FY2024‑25 supporting this mix. The bank combines traditional underwriting with AI-driven analytics to keep GNPA at 1.05% (FY2024‑25) and conducts continuous portfolio monitoring to maintain CRAR above 15% under 2025 market conditions.

Deposit Mobilization and Management

City Union Bank prioritizes low-cost CASA (current and savings) to keep cost of funds low, reporting a CASA ratio of 37.8% and CASA deposits of ₹32,400 crore as of FY2024; it targets retail segments with age-tailored savings and institutional term deposits to widen this base.

The bank uses active liquidity management—maintaining LCR (liquidity coverage ratio) above regulatory levels and optimizing an investment book of ~₹48,000 crore in FY2024—to meet withdrawals while maximizing yield.

Digital Transformation and IT Maintenance

City Union Bank prioritizes continuous upgrades to its mobile app and internet banking portal—supporting 8.2 million digital customers as of FY2024 and targeting a 15% YoY increase in active digital users—while automating back‑end processes (RPA and straight‑through processing) to cut manual errors and reduce processing costs by an estimated 12%. Daily cybersecurity operations protect customer assets against rising fraud: the bank reported a 28% year‑on‑year increase in attempted digital fraud blocks in 2024, prompting sustained investment in SOC and threat intelligence.

Customer Service and Relationship Building

City Union Bank delivers personalized service via 730+ branches and digital helpdesks; staff handle complex queries and advisory work for SMEs, supporting ~18% of loan book to micro/small enterprises as of FY2024–25.

Customer-service focus drives high loyalty—CASA ratio 36.8% and 2025 NPS ~58 in regional surveys, aiding stable retail deposit growth of 9% YoY.

- 730+ branches + digital helpdesks

- 18% loan book to micro/small firms

- CASA 36.8% (FY2024–25)

- NPS ~58 (2025 regional survey)

- Retail deposit growth 9% YoY

Compliance and Regulatory Reporting

City Union Bank must follow KYC, Anti-Money Laundering (AML), and Basel III capital and liquidity norms, filing regular reports and statutory returns to the Reserve Bank of India; in 2025 the bank allocates ~12% of compliance budget to AML tech after a 28% rise in SAR filings in 2024.

Regular internal and external audits ensure transparency and trust; compliance teams produce quarterly returns, with RBI-directed reporting frequency up to weekly for select risk metrics, driving significant administrative workload to track evolving 2025 rules.

- KYC/AML adherence

- Basel III capital & liquidity reporting

- Quarterly/weekly RBI returns

- 12% budget to AML tech (2025)

- 28% rise in SARs (2024)

Strong CASA-led lending (₹91,200cr) with low GNPA (1.05%) and 8.2M digital users

Key activities: underwriting and disbursing ₹91,200 crore gross advances (FY2024‑25) across retail, agri, MSME; CASA-led funding (CASA 37.8%, ₹32,400 crore FY2024) and liquidity/investment management (LCR above regulatory, investment book ~₹48,000 crore FY2024); digital upgrades supporting 8.2m users and 730+ branches; compliance/AML (12% compliance budget 2025) keeping GNPA 1.05%.

| Metric | Value |

|---|---|

| Gross advances | ₹91,200 cr (FY2024‑25) |

| CASA | 37.8%, ₹32,400 cr (FY2024) |

| Investment book | ~₹48,000 cr (FY2024) |

| Digital users | 8.2M (FY2024) |

| Branches | 730+ |

| GNPA | 1.05% (FY2024‑25) |

| AML budget | 12% (2025) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual City Union Bank Business Model Canvas—not a mockup or sample—and reflects the exact content and structure included in the final deliverable.

When you complete your purchase, you’ll receive this same professional, ready-to-use file in editable formats, with all sections, layouts, and content preserved as shown here.

No placeholders or hidden pages—what you see is what you’ll download and use immediately for analysis, presentation, or customization.