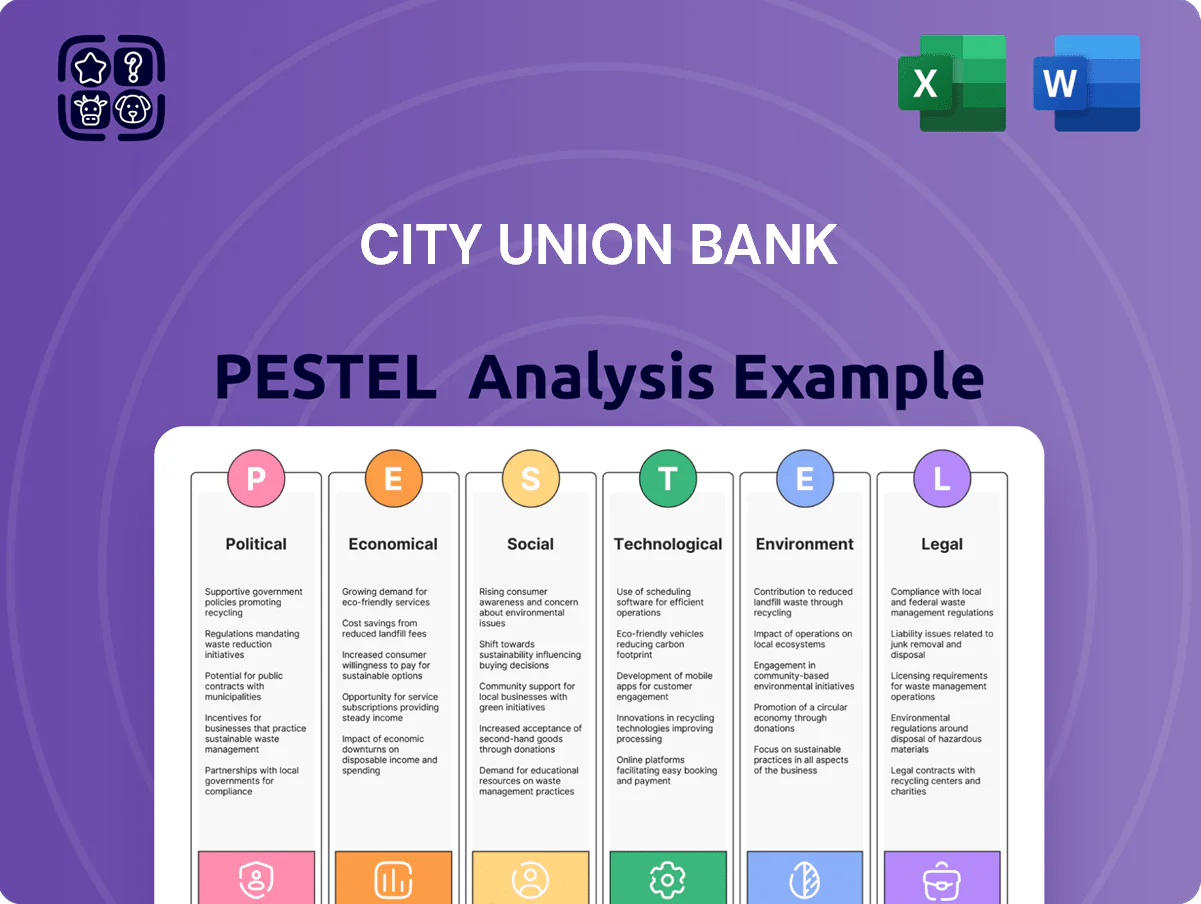

City Union Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of City Union Bank—identify how regulatory shifts, economic trends, and technological advances will shape future growth and risk; perfect for investors and strategists seeking concise, actionable insight. Purchase the full report to access the complete deep-dive, editable files, and ready-to-use intelligence for confident decision-making.

Political factors

Government Focus on MSME Growth

The Indian government continues prioritizing MSMEs via schemes like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and Production Linked Incentives, with MSME credit outstanding rising to about 17.4 lakh crore INR in FY2024 per RBI data. City Union Bank's significant MSME exposure—around 28% of its advances in FY2024—makes policy shifts on credit guarantees and subsidies critical to asset quality. Enhanced incentives have driven higher loan demand and improved repayment capacity among small-scale borrowers, supporting the bank's core lending franchise.

RBI Monetary Policy and Regulatory Oversight

The Reserve Bank of India kept the repo rate at 6.50% as of Dec 2025, tightly managing liquidity to curb inflation and support growth; this stance forces City Union Bank to recalibrate lending and deposit pricing to remain competitive.

As a private lender with a reported NIM of 3.65% in FY2024–25, City Union Bank’s margins are sensitive to RBI rate shifts; a 25 bp move can materially affect net interest income.

Any political tilt toward monetary easing or tightening—evident in RBI’s 2024–25 liquidity actions—directly influences the bank’s profitability and product strategies.

Digital India and Financial Inclusion Initiatives

Government programs like PMJDY (over 460 million accounts as of Dec 2025) and GST-driven cashless push have reshaped banking; City Union Bank (CUB) expanded UPI/CDR-enabled services, raising mobile transactions by ~38% YoY in FY2024–25 and widening reach in 2,000+ semi-urban/rural branches.

Geopolitical Stability and Trade Finance

India's expanding trade ties—merchandise exports rose 15% to $447bn in FY2023–24—boost City Union Bank's forex volumes as corporate clients increase import-export transactions handled by its foreign exchange desk.

Political stability supports steady cross-border trade vital to the bank's commercial book; disruptions can reduce transaction banking fees and working-capital flows.

Geopolitical tensions or protectionist measures spike currency volatility; forex non-interest income, which for many mid-sized Indian banks can vary 10–30% annually, faces downside risk.

- India merchandise exports $447bn FY2023–24; trade growth fuels forex volumes

- Political stability ensures predictable transaction banking and fee income

- Geopolitical tensions increase FX volatility, threatening 10–30% swing in forex NII

Regional Political Dynamics in South India

City Union Bank, with over 850 branches concentrated in Tamil Nadu and South India (around 70% of its network as of FY2024), is highly sensitive to state-level political shifts and fiscal policies that affect credit demand and deposits.

State infrastructure spends—Tamil Nadu capex ~INR 1.2 lakh crore in 2024–25—plus industrial policy incentives drive localized SME and lending opportunities, influencing branch-level portfolio growth.

Monitoring regional political climate is critical for optimizing branch expansion, risk exposure, and community relations to protect a loan book where ~60% of advances are South India-linked.

- ~70% branches in Tamil Nadu/South India (FY2024)

- Tamil Nadu capex ~INR 1.2 lakh crore (2024–25)

- ~60% of advances concentrated in South-linked sectors

CUB’s MSME-heavy southern footprint ties margins to RBI policy, Tamil Nadu capex and trade

Political stability, RBI policy (repo 6.50% Dec 2025) and MSME support (MSME credit ~INR 17.4 lakh crore FY2024) significantly shape City Union Bank’s margins and asset quality; ~28% advances to MSMEs and ~70% branches in South India make state fiscal moves (Tamil Nadu capex ~INR 1.2 lakh crore 2024–25) and trade flows (exports $447bn FY2023–24) key risk/drivers.

| Metric | Value |

|---|---|

| Repo rate (Dec 2025) | 6.50% |

| MSME credit (FY2024) | INR 17.4L cr |

| CUB MSME share | ~28% |

| Branches in South | ~70% |

| TN capex (2024–25) | INR 1.2L cr |

What is included in the product

Explores how external macro-environmental factors uniquely affect City Union Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategic responses tailored to the bank’s regional market and regulatory context.

Concise PESTLE summary tailored for City Union Bank to streamline strategy sessions and presentations, highlighting key external risks and opportunities for quick alignment across teams.

Economic factors

Interest Rate Volatility and Margin Management

The prevailing interest rate environment in India directly affects City Union Bank’s cost of funds and yield on advances; RBI rate hikes from 4% in 2021 to 6.5% by Dec 2023 raised systemic deposit costs and pressured margins. Fluctuations in market rates force the bank to actively rebalance its asset-liability mix to protect NIM, which was 4.1% in FY2023. Economic cycles with rate hikes increase deposit expenses, while cuts risk compressing lending spreads if repricing is not managed efficiently.

Indian GDP Growth and Credit Demand

India's GDP grew 7.2% in FY2023–24 and IMF projects ~6.8% for 2024, sustaining strong credit demand across retail and corporate segments, a key earnings driver for City Union Bank.

Higher industrial production and rising consumer spending boost loan offtake; bank growth closely tracks these macro trends given its focus on SME, retail and gold loans.

Robust growth typically reduces delinquencies and raises utilization; CUB reported GNPA of 2.05% in FY2023–24, reflecting resilience amid increased credit uptake.

Inflationary Pressures and Operating Costs

Persistent inflation in India, with CPI easing from 7.4% in Aug 2023 to 5.1% by Dec 2024, still raises City Union Bank operating costs via salary hikes and admin expenses, squeezing FY2024-25 margins where employee costs grew ~9-11% industrywide. While higher nominal loan growth (bank credit rose 14.2% YoY by Dec 2024) can lift NII, inflation reduces retail borrowers disposable income, raising default risk in unsecured segments. To manage, the bank must accelerate automation and cost-control—digital transactions rose to ~60% of volumes in 2024—cutting branch costs and improving efficiency ratios.

Performance of the MSME and Agricultural Sectors

The health of MSME and agriculture heavily influences City Union Bank’s asset quality; MSMEs accounted for about 30% of its gross advances in FY2024, so sector stress raises NPA risk.

Supply-chain shocks or monsoon shortfalls can spike defaults—India’s agri-GDP grew 3.3% in 2024, yet localized shocks elevated MSME stress ratios to ~6–8% in 2024.

Recovery and modernization (digitisation, cold chains) open avenues for high-yield loans and tailored products—targeted MSME/agri lending grew ~12% YoY in 2024.

- MSME share ≈30% of advances (FY2024)

- Agri GDP growth 3.3% (2024)

- MSME stress ratios ~6–8% (2024)

- Targeted lending growth ~12% YoY (2024)

Liquidity Conditions in the Banking System

Systemic liquidity managed by the RBI affects City Union Bank's ability to mobilize deposits and fund lending; as of Dec 2025 reserve ratios and OMO operations tightened overnight rates to ~6.8%, raising funding costs.

Tight liquidity forces competition for deposits, increasing interest expenses and pressuring net interest margin; Indian banks saw deposit growth slow to ~8.5% YoY in FY2024–25, intensifying competition.

City Union Bank monitors indicators to maintain an optimal Liquidity Coverage Ratio—reported LCR ~140% in FY2024—balancing liquidity safety with return on assets around 1.2%.

- RBI liquidity stance → higher overnight rates (~6.8%)

- Deposit growth slowed to ~8.5% YoY FY2024–25

- City Union Bank LCR ~140% and RoA ~1.2%

Tightening rates squeeze margins despite strong GDP and credit-led loan growth

Interest rates and RBI liquidity tightened margins—RBI policy rate rose to 6.5% by Dec 2023 and overnight rates ~6.8% by Dec 2024, pressuring NIM (CUB NIM 4.1% FY2023; RoA ~1.2% FY2024). Strong GDP (~7.2% FY2023–24) and credit growth (+14.2% YoY Dec 2024) boosted loan demand, with MSME ~30% of advances and GNPA 2.05% FY2023–24; inflation eased to 5.1% Dec 2024, but cost pressures persisted.

| Metric | Value |

|---|---|

| Policy rate (Dec 2023) | 6.5% |

| Overnight rate (Dec 2024) | ~6.8% |

| NIM (FY2023) | 4.1% |

| RoA (FY2024) | ~1.2% |

| GDP growth (FY2023–24) | 7.2% |

| Credit growth (Dec 2024) | 14.2% YoY |

| MSME share (FY2024) | ~30% |

| GNPA (FY2023–24) | 2.05% |

| Inflation (Dec 2024 CPI) | 5.1% |

What You See Is What You Get

City Union Bank PESTLE Analysis

The preview shown here is the exact City Union Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of City Union Bank—identify how regulatory shifts, economic trends, and technological advances will shape future growth and risk; perfect for investors and strategists seeking concise, actionable insight. Purchase the full report to access the complete deep-dive, editable files, and ready-to-use intelligence for confident decision-making.

Political factors

Government Focus on MSME Growth

The Indian government continues prioritizing MSMEs via schemes like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and Production Linked Incentives, with MSME credit outstanding rising to about 17.4 lakh crore INR in FY2024 per RBI data. City Union Bank's significant MSME exposure—around 28% of its advances in FY2024—makes policy shifts on credit guarantees and subsidies critical to asset quality. Enhanced incentives have driven higher loan demand and improved repayment capacity among small-scale borrowers, supporting the bank's core lending franchise.

RBI Monetary Policy and Regulatory Oversight

The Reserve Bank of India kept the repo rate at 6.50% as of Dec 2025, tightly managing liquidity to curb inflation and support growth; this stance forces City Union Bank to recalibrate lending and deposit pricing to remain competitive.

As a private lender with a reported NIM of 3.65% in FY2024–25, City Union Bank’s margins are sensitive to RBI rate shifts; a 25 bp move can materially affect net interest income.

Any political tilt toward monetary easing or tightening—evident in RBI’s 2024–25 liquidity actions—directly influences the bank’s profitability and product strategies.

Digital India and Financial Inclusion Initiatives

Government programs like PMJDY (over 460 million accounts as of Dec 2025) and GST-driven cashless push have reshaped banking; City Union Bank (CUB) expanded UPI/CDR-enabled services, raising mobile transactions by ~38% YoY in FY2024–25 and widening reach in 2,000+ semi-urban/rural branches.

Geopolitical Stability and Trade Finance

India's expanding trade ties—merchandise exports rose 15% to $447bn in FY2023–24—boost City Union Bank's forex volumes as corporate clients increase import-export transactions handled by its foreign exchange desk.

Political stability supports steady cross-border trade vital to the bank's commercial book; disruptions can reduce transaction banking fees and working-capital flows.

Geopolitical tensions or protectionist measures spike currency volatility; forex non-interest income, which for many mid-sized Indian banks can vary 10–30% annually, faces downside risk.

- India merchandise exports $447bn FY2023–24; trade growth fuels forex volumes

- Political stability ensures predictable transaction banking and fee income

- Geopolitical tensions increase FX volatility, threatening 10–30% swing in forex NII

Regional Political Dynamics in South India

City Union Bank, with over 850 branches concentrated in Tamil Nadu and South India (around 70% of its network as of FY2024), is highly sensitive to state-level political shifts and fiscal policies that affect credit demand and deposits.

State infrastructure spends—Tamil Nadu capex ~INR 1.2 lakh crore in 2024–25—plus industrial policy incentives drive localized SME and lending opportunities, influencing branch-level portfolio growth.

Monitoring regional political climate is critical for optimizing branch expansion, risk exposure, and community relations to protect a loan book where ~60% of advances are South India-linked.

- ~70% branches in Tamil Nadu/South India (FY2024)

- Tamil Nadu capex ~INR 1.2 lakh crore (2024–25)

- ~60% of advances concentrated in South-linked sectors

CUB’s MSME-heavy southern footprint ties margins to RBI policy, Tamil Nadu capex and trade

Political stability, RBI policy (repo 6.50% Dec 2025) and MSME support (MSME credit ~INR 17.4 lakh crore FY2024) significantly shape City Union Bank’s margins and asset quality; ~28% advances to MSMEs and ~70% branches in South India make state fiscal moves (Tamil Nadu capex ~INR 1.2 lakh crore 2024–25) and trade flows (exports $447bn FY2023–24) key risk/drivers.

| Metric | Value |

|---|---|

| Repo rate (Dec 2025) | 6.50% |

| MSME credit (FY2024) | INR 17.4L cr |

| CUB MSME share | ~28% |

| Branches in South | ~70% |

| TN capex (2024–25) | INR 1.2L cr |

What is included in the product

Explores how external macro-environmental factors uniquely affect City Union Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategic responses tailored to the bank’s regional market and regulatory context.

Concise PESTLE summary tailored for City Union Bank to streamline strategy sessions and presentations, highlighting key external risks and opportunities for quick alignment across teams.

Economic factors

Interest Rate Volatility and Margin Management

The prevailing interest rate environment in India directly affects City Union Bank’s cost of funds and yield on advances; RBI rate hikes from 4% in 2021 to 6.5% by Dec 2023 raised systemic deposit costs and pressured margins. Fluctuations in market rates force the bank to actively rebalance its asset-liability mix to protect NIM, which was 4.1% in FY2023. Economic cycles with rate hikes increase deposit expenses, while cuts risk compressing lending spreads if repricing is not managed efficiently.

Indian GDP Growth and Credit Demand

India's GDP grew 7.2% in FY2023–24 and IMF projects ~6.8% for 2024, sustaining strong credit demand across retail and corporate segments, a key earnings driver for City Union Bank.

Higher industrial production and rising consumer spending boost loan offtake; bank growth closely tracks these macro trends given its focus on SME, retail and gold loans.

Robust growth typically reduces delinquencies and raises utilization; CUB reported GNPA of 2.05% in FY2023–24, reflecting resilience amid increased credit uptake.

Inflationary Pressures and Operating Costs

Persistent inflation in India, with CPI easing from 7.4% in Aug 2023 to 5.1% by Dec 2024, still raises City Union Bank operating costs via salary hikes and admin expenses, squeezing FY2024-25 margins where employee costs grew ~9-11% industrywide. While higher nominal loan growth (bank credit rose 14.2% YoY by Dec 2024) can lift NII, inflation reduces retail borrowers disposable income, raising default risk in unsecured segments. To manage, the bank must accelerate automation and cost-control—digital transactions rose to ~60% of volumes in 2024—cutting branch costs and improving efficiency ratios.

Performance of the MSME and Agricultural Sectors

The health of MSME and agriculture heavily influences City Union Bank’s asset quality; MSMEs accounted for about 30% of its gross advances in FY2024, so sector stress raises NPA risk.

Supply-chain shocks or monsoon shortfalls can spike defaults—India’s agri-GDP grew 3.3% in 2024, yet localized shocks elevated MSME stress ratios to ~6–8% in 2024.

Recovery and modernization (digitisation, cold chains) open avenues for high-yield loans and tailored products—targeted MSME/agri lending grew ~12% YoY in 2024.

- MSME share ≈30% of advances (FY2024)

- Agri GDP growth 3.3% (2024)

- MSME stress ratios ~6–8% (2024)

- Targeted lending growth ~12% YoY (2024)

Liquidity Conditions in the Banking System

Systemic liquidity managed by the RBI affects City Union Bank's ability to mobilize deposits and fund lending; as of Dec 2025 reserve ratios and OMO operations tightened overnight rates to ~6.8%, raising funding costs.

Tight liquidity forces competition for deposits, increasing interest expenses and pressuring net interest margin; Indian banks saw deposit growth slow to ~8.5% YoY in FY2024–25, intensifying competition.

City Union Bank monitors indicators to maintain an optimal Liquidity Coverage Ratio—reported LCR ~140% in FY2024—balancing liquidity safety with return on assets around 1.2%.

- RBI liquidity stance → higher overnight rates (~6.8%)

- Deposit growth slowed to ~8.5% YoY FY2024–25

- City Union Bank LCR ~140% and RoA ~1.2%

Tightening rates squeeze margins despite strong GDP and credit-led loan growth

Interest rates and RBI liquidity tightened margins—RBI policy rate rose to 6.5% by Dec 2023 and overnight rates ~6.8% by Dec 2024, pressuring NIM (CUB NIM 4.1% FY2023; RoA ~1.2% FY2024). Strong GDP (~7.2% FY2023–24) and credit growth (+14.2% YoY Dec 2024) boosted loan demand, with MSME ~30% of advances and GNPA 2.05% FY2023–24; inflation eased to 5.1% Dec 2024, but cost pressures persisted.

| Metric | Value |

|---|---|

| Policy rate (Dec 2023) | 6.5% |

| Overnight rate (Dec 2024) | ~6.8% |

| NIM (FY2023) | 4.1% |

| RoA (FY2024) | ~1.2% |

| GDP growth (FY2023–24) | 7.2% |

| Credit growth (Dec 2024) | 14.2% YoY |

| MSME share (FY2024) | ~30% |

| GNPA (FY2023–24) | 2.05% |

| Inflation (Dec 2024 CPI) | 5.1% |

What You See Is What You Get

City Union Bank PESTLE Analysis

The preview shown here is the exact City Union Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.