Civista Bank Business Model Canvas

Civista Bank Business Model Canvas: Strategic Blueprint for Investors & Advisors

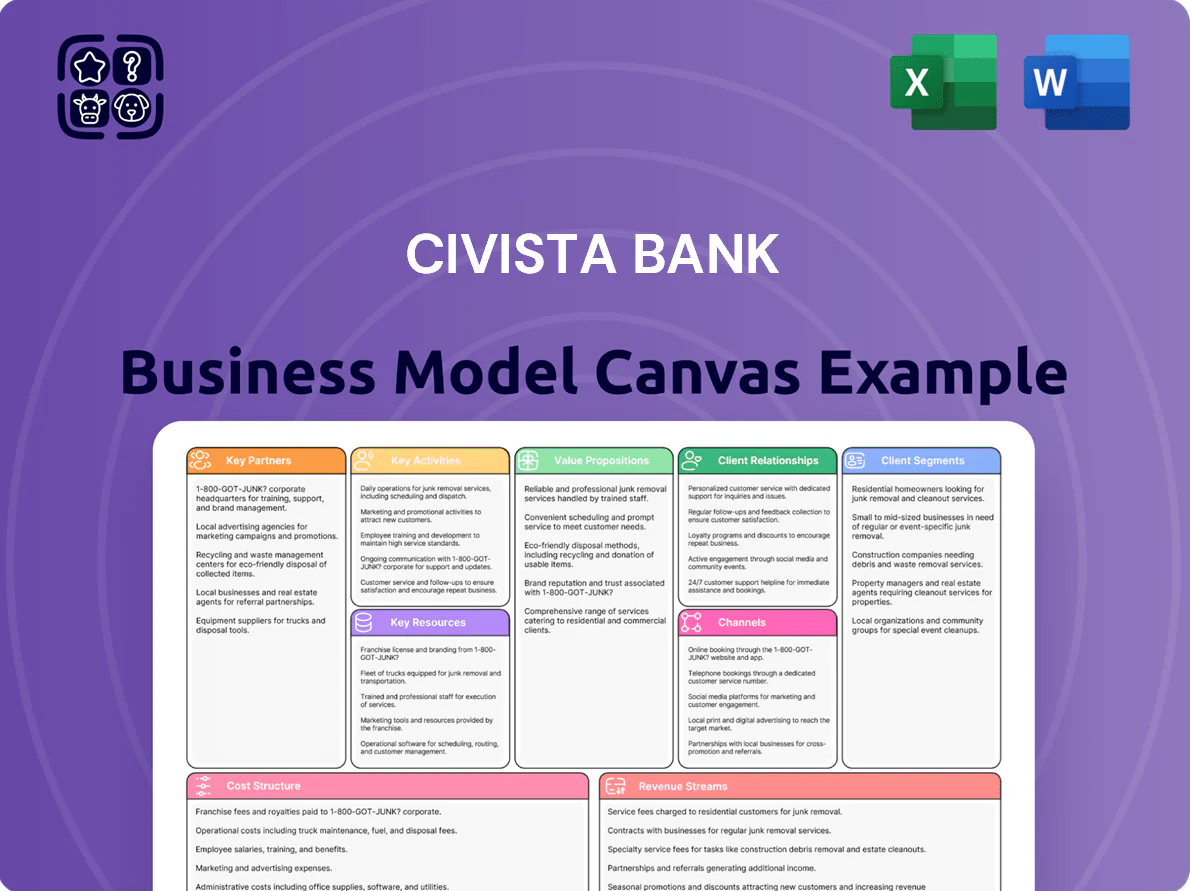

Unlock the full strategic blueprint behind Civista Bank’s business model—this concise Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains growth in regional markets. Ideal for investors, advisors, and entrepreneurs, the full version offers section-by-section detail on customer segments, revenue streams, key partners, and cost structure. Download the editable Word/Excel file to benchmark strategies, inform M&A or drive competitive analysis.

Partnerships

Fintech and Software Providers

Civista Bank partners with fintech and core-software providers to run its digital banking platform and core processing, enabling features like mobile check deposit, real-time ACH and Zelle transfers, and multi-factor security; in 2024 these integrations supported ~45% of customer transactions via digital channels. By outsourcing specialist tech, Civista keeps IT spend lean—estimated 0.8–1.2% of assets in 2024—while focusing on relationship banking and competing with national banks.

Federal and State Regulatory Agencies

The bank maintains vital ties with the Federal Reserve, the FDIC, and state banking divisions to ensure compliance and financial stability; FDIC insurance covers deposits up to $250,000 per depositor, and Civista reports a CET1 ratio of 12.1% (2024), reflecting regulatory capital adequacy. Continuous regulator engagement helps adapt to evolving rules and keeps the bank’s charter and depositor confidence in good standing.

Third-Party Investment and Trust Affiliates

Civista Bank partners with external asset managers and investment platform providers to offer a full wealth suite—mutual funds, annuities, and brokerage—without building each product in-house; as of 2025 these partnerships helped manage an estimated $1.2 billion in custody and advisory assets for high-net-worth clients. This model supplies sophisticated financial planning tools and diversified products while keeping fixed-costs lower and product breadth high.

Local Community and Economic Development Groups

Civista Bank partners with local chambers of commerce and non-profits to drive regional growth, sourcing community development loans and projects that match its mission; in 2024 Civista reported $1.2B in community lending and contributed $1.5M to local initiatives.

These partnerships boost brand presence and customer loyalty across its Ohio and Michigan footprint, helping identify small-business lending opportunities—about 18% of new commercial loans in 2024 originated via community referrals.

- 2024 community lending: $1.2B

- Cash/non-cash support: $1.5M (2024)

- Referral-sourced commercial loans: 18% (2024)

Credit Bureaus and Rating Agencies

Civista Bank partners with major credit bureaus and rating agencies to access consumer and commercial credit data, enabling precise risk assessment and loan underwriting; as of 2024 Civista used bureau scores and tradeline data to keep net charge-off rates near 0.45% (2024 YTD) and maintain NPLs under 0.7%.

These partnerships supply credit histories, scores, and alerts that are essential to evaluate applicant creditworthiness and manage the bank’s overall credit risk exposure, supporting portfolio health and regulatory compliance.

- Net charge-offs ~0.45% (2024 YTD)

- Nonperforming loans <0.7% (2024)

- Uses FICO and commercial scores, tradeline data

Civista: Digital-first banking with $1.2B custody, 45% digital txns, strong credit metrics

Civista leverages fintech/core processors, asset managers, regulators, credit bureaus, and community partners to run digital banking (45% transactions, 2024), manage $1.2B custody/advisory (2025), sustain CET1 12.1% (2024), keep NCO ~0.45% and NPLs <0.7% (2024), and deliver $1.2B community lending with $1.5M support (2024).

| Metric | Value |

|---|---|

| Digital txns | 45% (2024) |

| Custody/advisory | $1.2B (2025) |

| CET1 | 12.1% (2024) |

| NCO | ~0.45% (2024 YTD) |

| NPLs | <0.7% (2024) |

| Community lending | $1.2B (2024) |

| Community support | $1.5M (2024) |

What is included in the product

A concise Business Model Canvas for Civista Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting real-world community banking operations and strategic priorities for investor presentations and internal planning.

High-level, editable one-page snapshot of Civista Bank's business model that condenses strategy into a clean layout for fast review, team collaboration, and quick deliverables.

Activities

Lending and Credit Administration

Civista Bank’s lending and credit administration focuses on originating, underwriting, and servicing loans from mortgages to commercial lines, with $3.2 billion in loans outstanding as of Q4 2025 and net charge-offs under 0.30% in 2024. Staff rigorously evaluate credit to balance 8–10% annual loan growth targets with risk control, including monthly performance monitoring and collateral management to protect the bank’s assets.

Deposit and Liquidity Management

Civista Bank gathers deposits from individuals and businesses across checking, savings, and CDs—using these funds to support $4.2 billion in loans (2024 year-end) and to meet liquidity needs. The treasury team actively manages cash buffers and wholesale funding so the bank maintains regulatory liquidity ratios (LCR >100%) and meets daily withdrawal demands.

Financial Advisory and Wealth Management

Civista Bank offers personalized financial planning, trust services, and investment management—advisors run deep discovery sessions to set goals and risk profiles, then deploy tailored portfolios to grow and preserve wealth. In 2024 Civista reported ~$45 million in non‑interest income, with wealth management driving ~18% of fee revenue, a key source of loyalty and recurring fees.

Digital and Physical Channel Operations

Maintaining a seamless omnichannel experience, Civista Bank runs and secures 75 branch locations and 120 ATMs while supporting mobile and online platforms that handled $4.2B in digital payments in 2024; both channels are optimized for transactions, deposits, and advisory services to match customer preferences.

- 75 branches; 120 ATMs (2024)

- $4.2B digital payments processed (2024)

- 24/7 app and portal uptime target; multi-factor authentication

- Face-to-face service for complex needs; digital for daily convenience

Risk Management and Regulatory Compliance

Civista Bank allocates substantial resources to monitor internal controls, prevent fraud, and comply with anti-money laundering (AML) laws, running quarterly audits, monthly AML transaction reviews, and mandatory annual staff training that covered 100% of frontline staff in 2025.

They deploy advanced monitoring software that flagged a 22% increase in suspicious activity reports in 2024, avoiding regulatory fines and protecting the bank’s reputation through timely remediation.

- Quarterly audits and monthly AML reviews

- 100% frontline staff trained in 2025

- Advanced monitoring software in use

- 22% rise in SARs flagged in 2024

Civista: $3.2B Loans, $4.2B Digital Payments, Strong LCR & Full AML Training

Civista’s key activities: loan origination & servicing ($3.2B loans Q4 2025; net charge-offs <0.30% 2024), deposit gathering funding $4.2B loans (2024) and LCR >100%, wealth management (~$45M non‑interest income; 18% fee share 2024), branch/digital ops (75 branches;120 ATMs; $4.2B digital payments 2024), AML/compliance (100% frontline trained 2025; 22% SAR rise 2024).

| Metric | Value |

|---|---|

| Loans outstanding | $3.2B (Q4 2025) |

| Digital payments | $4.2B (2024) |

| Branches / ATMs | 75 / 120 (2024) |

| Wealth income | $45M; 18% fees (2024) |

| AML training | 100% frontline (2025) |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Civista Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample; upon ordering you’ll get this exact, fully editable file (Word and Excel) with all sections and formatting intact, ready for presentation, editing, and sharing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Civista Bank Business Model Canvas: Strategic Blueprint for Investors & Advisors

Unlock the full strategic blueprint behind Civista Bank’s business model—this concise Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains growth in regional markets. Ideal for investors, advisors, and entrepreneurs, the full version offers section-by-section detail on customer segments, revenue streams, key partners, and cost structure. Download the editable Word/Excel file to benchmark strategies, inform M&A or drive competitive analysis.

Partnerships

Fintech and Software Providers

Civista Bank partners with fintech and core-software providers to run its digital banking platform and core processing, enabling features like mobile check deposit, real-time ACH and Zelle transfers, and multi-factor security; in 2024 these integrations supported ~45% of customer transactions via digital channels. By outsourcing specialist tech, Civista keeps IT spend lean—estimated 0.8–1.2% of assets in 2024—while focusing on relationship banking and competing with national banks.

Federal and State Regulatory Agencies

The bank maintains vital ties with the Federal Reserve, the FDIC, and state banking divisions to ensure compliance and financial stability; FDIC insurance covers deposits up to $250,000 per depositor, and Civista reports a CET1 ratio of 12.1% (2024), reflecting regulatory capital adequacy. Continuous regulator engagement helps adapt to evolving rules and keeps the bank’s charter and depositor confidence in good standing.

Third-Party Investment and Trust Affiliates

Civista Bank partners with external asset managers and investment platform providers to offer a full wealth suite—mutual funds, annuities, and brokerage—without building each product in-house; as of 2025 these partnerships helped manage an estimated $1.2 billion in custody and advisory assets for high-net-worth clients. This model supplies sophisticated financial planning tools and diversified products while keeping fixed-costs lower and product breadth high.

Local Community and Economic Development Groups

Civista Bank partners with local chambers of commerce and non-profits to drive regional growth, sourcing community development loans and projects that match its mission; in 2024 Civista reported $1.2B in community lending and contributed $1.5M to local initiatives.

These partnerships boost brand presence and customer loyalty across its Ohio and Michigan footprint, helping identify small-business lending opportunities—about 18% of new commercial loans in 2024 originated via community referrals.

- 2024 community lending: $1.2B

- Cash/non-cash support: $1.5M (2024)

- Referral-sourced commercial loans: 18% (2024)

Credit Bureaus and Rating Agencies

Civista Bank partners with major credit bureaus and rating agencies to access consumer and commercial credit data, enabling precise risk assessment and loan underwriting; as of 2024 Civista used bureau scores and tradeline data to keep net charge-off rates near 0.45% (2024 YTD) and maintain NPLs under 0.7%.

These partnerships supply credit histories, scores, and alerts that are essential to evaluate applicant creditworthiness and manage the bank’s overall credit risk exposure, supporting portfolio health and regulatory compliance.

- Net charge-offs ~0.45% (2024 YTD)

- Nonperforming loans <0.7% (2024)

- Uses FICO and commercial scores, tradeline data

Civista: Digital-first banking with $1.2B custody, 45% digital txns, strong credit metrics

Civista leverages fintech/core processors, asset managers, regulators, credit bureaus, and community partners to run digital banking (45% transactions, 2024), manage $1.2B custody/advisory (2025), sustain CET1 12.1% (2024), keep NCO ~0.45% and NPLs <0.7% (2024), and deliver $1.2B community lending with $1.5M support (2024).

| Metric | Value |

|---|---|

| Digital txns | 45% (2024) |

| Custody/advisory | $1.2B (2025) |

| CET1 | 12.1% (2024) |

| NCO | ~0.45% (2024 YTD) |

| NPLs | <0.7% (2024) |

| Community lending | $1.2B (2024) |

| Community support | $1.5M (2024) |

What is included in the product

A concise Business Model Canvas for Civista Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting real-world community banking operations and strategic priorities for investor presentations and internal planning.

High-level, editable one-page snapshot of Civista Bank's business model that condenses strategy into a clean layout for fast review, team collaboration, and quick deliverables.

Activities

Lending and Credit Administration

Civista Bank’s lending and credit administration focuses on originating, underwriting, and servicing loans from mortgages to commercial lines, with $3.2 billion in loans outstanding as of Q4 2025 and net charge-offs under 0.30% in 2024. Staff rigorously evaluate credit to balance 8–10% annual loan growth targets with risk control, including monthly performance monitoring and collateral management to protect the bank’s assets.

Deposit and Liquidity Management

Civista Bank gathers deposits from individuals and businesses across checking, savings, and CDs—using these funds to support $4.2 billion in loans (2024 year-end) and to meet liquidity needs. The treasury team actively manages cash buffers and wholesale funding so the bank maintains regulatory liquidity ratios (LCR >100%) and meets daily withdrawal demands.

Financial Advisory and Wealth Management

Civista Bank offers personalized financial planning, trust services, and investment management—advisors run deep discovery sessions to set goals and risk profiles, then deploy tailored portfolios to grow and preserve wealth. In 2024 Civista reported ~$45 million in non‑interest income, with wealth management driving ~18% of fee revenue, a key source of loyalty and recurring fees.

Digital and Physical Channel Operations

Maintaining a seamless omnichannel experience, Civista Bank runs and secures 75 branch locations and 120 ATMs while supporting mobile and online platforms that handled $4.2B in digital payments in 2024; both channels are optimized for transactions, deposits, and advisory services to match customer preferences.

- 75 branches; 120 ATMs (2024)

- $4.2B digital payments processed (2024)

- 24/7 app and portal uptime target; multi-factor authentication

- Face-to-face service for complex needs; digital for daily convenience

Risk Management and Regulatory Compliance

Civista Bank allocates substantial resources to monitor internal controls, prevent fraud, and comply with anti-money laundering (AML) laws, running quarterly audits, monthly AML transaction reviews, and mandatory annual staff training that covered 100% of frontline staff in 2025.

They deploy advanced monitoring software that flagged a 22% increase in suspicious activity reports in 2024, avoiding regulatory fines and protecting the bank’s reputation through timely remediation.

- Quarterly audits and monthly AML reviews

- 100% frontline staff trained in 2025

- Advanced monitoring software in use

- 22% rise in SARs flagged in 2024

Civista: $3.2B Loans, $4.2B Digital Payments, Strong LCR & Full AML Training

Civista’s key activities: loan origination & servicing ($3.2B loans Q4 2025; net charge-offs <0.30% 2024), deposit gathering funding $4.2B loans (2024) and LCR >100%, wealth management (~$45M non‑interest income; 18% fee share 2024), branch/digital ops (75 branches;120 ATMs; $4.2B digital payments 2024), AML/compliance (100% frontline trained 2025; 22% SAR rise 2024).

| Metric | Value |

|---|---|

| Loans outstanding | $3.2B (Q4 2025) |

| Digital payments | $4.2B (2024) |

| Branches / ATMs | 75 / 120 (2024) |

| Wealth income | $45M; 18% fees (2024) |

| AML training | 100% frontline (2025) |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Civista Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample; upon ordering you’ll get this exact, fully editable file (Word and Excel) with all sections and formatting intact, ready for presentation, editing, and sharing.