CJ Cheiljedang Boston Consulting Group Matrix

Actionable Strategy Starts Here

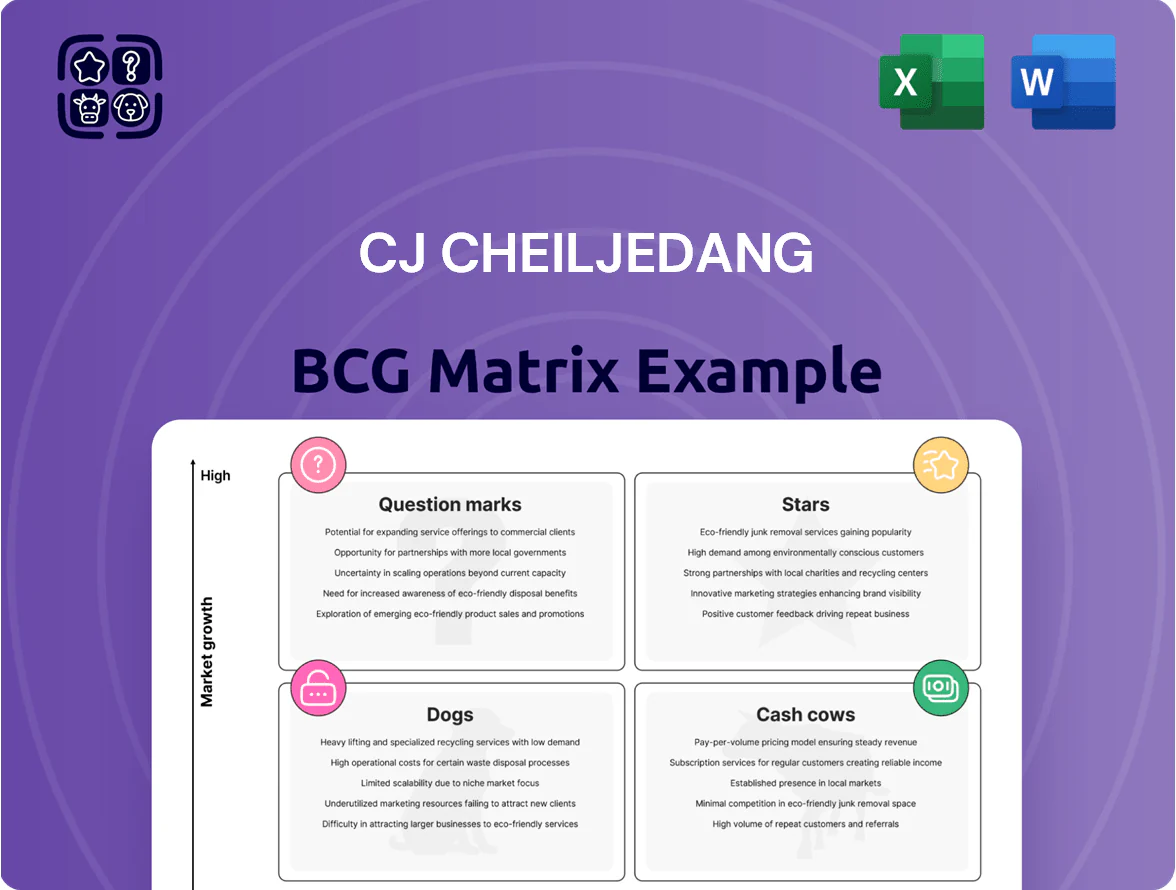

CJ CheilJedang’s product portfolio straddles high-growth food tech and stable staples—expect Stars in bio-based ingredients and Cash Cows in legacy food brands, with select Question Marks in emerging wellness segments that could become future Stars. This snapshot hints at resource allocation tensions between innovation and margin preservation; the full BCG Matrix maps each business unit’s quadrant, growth metrics, and suggested strategic moves. Purchase the complete report for quadrant-by-quadrant analysis, data-driven recommendations, and editable Word/Excel deliverables to act confidently.

Stars

Bibigo Global Expansion

As of late 2025 Bibigo is the global K-food leader, with overseas sales exceeding domestic revenue for the first time—over $1.2 billion abroad versus $1.0 billion at home in FY2025.

The brand holds a high share in North American frozen dumplings (estimated 32% market share in 2025) and is scaling quickly in Europe and Oceania, growing international retail distribution by 28% YoY.

CJ CheilJedang is reinvesting heavily to sustain growth, opening a Chiba plant in Japan (2024 start) and expanding Hungary capacity, adding ~40,000 tons annual frozen-product output and capital expenditure of roughly $220 million through 2026.

Schwan’s Company Frozen Pizza

Acquired to anchor CJ CheilJedang’s US push, Schwan’s Company Frozen Pizza—led by Red Baron and Tony’s—holds a market-leading share in the US frozen pizza segment; in 2025 the unit grew ~6–8% organic sales, outpacing category peers in premium and single-serve lines and boosting EBITDA margins to roughly 14%. It remains a cash generator, but planned CAPEX of ~$120–150M through 2026 for automation and logistics integration is needed to sustain advantage.

Global Strategic Products (GSP)

Global Strategic Products (GSP) — shelf-stable rice, kimchi, seaweed snacks, and K-sauces — are CJ CheilJedang’s high-growth engine in international markets, posting double-digit revenue growth in 2025 (UK +18%, Germany +15%, Netherlands +22%).

These SKUs grew faster in European mainstream grocery channels than ethnic aisles, lifting total GSP export sales to KRW 420 billion in 2025, up 21% year-on-year.

CJ is funding aggressive marketing and in-store promotions—estimated KRW 35 billion incremental spend in 2025—to shift perception from niche ethnic to convenience staples; ROI targets aim for payback within 18 months.

Specialty Amino Acids

CJ CheilJedang’s bio-engineering unit holds a global-leading share (>40% in 2025) in high-value specialty amino acids like Tryptophan and Valine, classifying them as Stars in the BCG Matrix.

Despite broader bio market volatility in 2025, these high-margin functional ingredients grew ~8–12% YoY, driven by sustainable, health-focused feed additive demand.

The company is reallocating CAPEX and R&D away from commodity amino acids toward technology-intensive Star segments, leveraging a near-technical monopoly and higher EBITDA margins (mid-20s%).

- Global share >40% (2025)

- Growth 8–12% YoY (2025)

- EBITDA margin mid-20s%

- Strategic CAPEX/R&D pivot to Stars

European and Oceania Food Markets

European and Oceania Food Markets are Stars for CJ Cheiljedang, with Europe posting 2025 revenue growth above 13 percent and Oceania up ~9–11 percent, driven by rising K-food demand and low penetration versus the US.

The company sees a large runway for share gains via new distribution partnerships and is prioritizing infrastructure spend—€120–150 million planned across Europe and AUD 40–55 million in Oceania through 2026 to scale cold chain and retail reach.

- 2025 Europe growth >13%

- Oceania growth ~9–11%

- Low K-food penetration vs US

- Planned investment: €120–150M Europe, AUD40–55M Oceania

- Focus: distribution, cold chain, retail partnerships

CJ CheilJedang 2025: $1.2B overseas food, bio amino >40% share, Schwan’s EBITDA ~14%

Stars: Bibigo, Schwan’s frozen pizza, GSP, and specialty amino acids drive CJ CheilJedang’s high-growth portfolio—2025 highlights: overseas food sales $1.2B, GSP exports KRW420B (+21% YoY), bio amino acids global share >40% with 8–12% growth, Schwan’s EBITDA ~14% with CAPEX $120–150M, Europe growth >13% (CAPEX €120–150M), Oceania growth ~9–11% (CAPEX AUD40–55M).

| Unit | 2025 | Growth/CAPEX |

|---|---|---|

| Overseas food sales | $1.2B | — |

| GSP exports | KRW420B | +21% YoY |

| Bio amino acids | >40% share | 8–12% YoY |

| Schwan’s EBITDA | ~14% | CAPEX $120–150M |

| Europe | >13% growth | €120–150M CAPEX |

| Oceania | 9–11% growth | AUD40–55M CAPEX |

What is included in the product

Comprehensive BCG Matrix review of CJ CheilJedang's portfolio, guiding invest/hold/divest decisions with quadrant-specific risks and trends.

One-page BCG matrix mapping CJ CheilJedang units for quick strategic decisions and stakeholder-ready presentations.

Cash Cows

Domestic Processed Foods

CJ CheilJedang dominates South Korea’s processed-foods market with brands like Hetbahn and Spam, holding roughly 30–40% category share and delivering stable domestic FY2024 revenues of about KRW 2.1 trillion from food operations. The mature market—shrinking population (-0.4% YoY in 2024) and CPI-driven inflation near 4%—cuts growth but these SKUs yield high margins and low marketing spend, producing robust free cash flow (~KRW 400–600 billion annually). This cash generation funds CJ’s global expansion and biotech R&D, enabling 2024 capex and M&A outlays of roughly KRW 700 billion.

Sugar and Flour Business

As CJ CheilJedang’s foundational milling and sugar refining units hold dominant market shares in South Korea—estimated domestic market share ~40–60% in wheat milling and ~50% in refined sugar in 2024—they are classic cash cows in a low-growth, mature sector with high entry barriers.

These units need minimal promo spend, generate steady EBITDA margins around 8–12% (2024 pro forma), and supply predictable cash flow that services corporate debt and funds newer, higher-growth businesses like biotech and meal kits.

CJ Logistics Synergy

CJ Logistics Synergy: as CJ CheilJedang’s logistics subsidiary, it anchors the group with a dominant market share in Korea and steady cash generation; in 2025 it reported ~KRW 1.2 trillion revenue and operating profit up 6% YoY, driven by e-commerce fulfillment and contract logistics growth.

Traditional Seasonings and Sauces

Traditional seasonings like Dashida and fermented pastes (jang) hold ~30–40% value share in Korea’s retail condiment category and deliver gross margins around 35–40% for CJ CheilJedang as of FY2024, reflecting mature, low-growth demand but high profitability from scale and lean production.

These products act as cash cows—stable profit anchors—insulated from trend volatility; domestic seasoning volume growth was ~1–2% CAGR 2019–2024 while EBITDA contribution from condiments stayed >20% of CJ Food & Retail FY2024.

- Value share 30–40% in Korea

- Gross margins ~35–40% (FY2024)

- Volume CAGR ~1–2% (2019–2024)

- EBITDA >20% of CJ Food & Retail (FY2024)

Animal Feed and Care (Retained Segments)

Following the 2025 divestiture of underperforming feed assets, CJ CheilJedang’s retained specialized livestock feed operations stabilized into steady cash generators, contributing roughly KRW 120–150 billion in annual EBIT by 2025.

Management now prioritizes core efficiencies and premium feed in stable markets, cutting capital expenditures from KRW 90 billion (pre-2025) to ~KRW 25–35 billion yearly and lifting operating margins to about 12–14%.

Strategy shifted from growth to maximizing livestock spread and operational margins, with return on invested capital (ROIC) for the segment rising to ~11% in 2025.

- 2025 EBIT ~KRW 120–150B

- CapEx cut to KRW 25–35B/yr

- Operating margin ~12–14%

- Segment ROIC ~11% (2025)

CJ CheilJedang’s cash cows drive KRW 400–600B FCF, strong margins & market shares

CJ CheilJedang’s cash cows—processed foods, milling/sugar, seasonings, logistics, and premium feed—generated steady FY2024–2025 cash flows: food revenues ~KRW 2.1T, free cash flow ~KRW 400–600B, milling/sugar market shares ~40–60%/50%, seasonings gross margin 35–40% and EBITDA >20% of food, CJ Logistics revenue ~KRW 1.2T (2025), feed EBIT ~KRW 120–150B (2025).

| Segment | 2024–25 Key |

|---|---|

| Processed foods | Rev KRW 2.1T; FCF KRW 400–600B |

| Milling / sugar | Share 40–60% / ~50% |

| Seasonings | GM 35–40%; EBITDA >20% |

| Logistics | Rev KRW 1.2T (2025) |

| Feed | EBIT KRW 120–150B; ROIC ~11% |

Preview = Final Product

CJ Cheiljedang BCG Matrix

The file you're previewing is the exact CJ CheilJedang BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, strategy-ready document crafted for clarity and practical use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

CJ CheilJedang’s product portfolio straddles high-growth food tech and stable staples—expect Stars in bio-based ingredients and Cash Cows in legacy food brands, with select Question Marks in emerging wellness segments that could become future Stars. This snapshot hints at resource allocation tensions between innovation and margin preservation; the full BCG Matrix maps each business unit’s quadrant, growth metrics, and suggested strategic moves. Purchase the complete report for quadrant-by-quadrant analysis, data-driven recommendations, and editable Word/Excel deliverables to act confidently.

Stars

Bibigo Global Expansion

As of late 2025 Bibigo is the global K-food leader, with overseas sales exceeding domestic revenue for the first time—over $1.2 billion abroad versus $1.0 billion at home in FY2025.

The brand holds a high share in North American frozen dumplings (estimated 32% market share in 2025) and is scaling quickly in Europe and Oceania, growing international retail distribution by 28% YoY.

CJ CheilJedang is reinvesting heavily to sustain growth, opening a Chiba plant in Japan (2024 start) and expanding Hungary capacity, adding ~40,000 tons annual frozen-product output and capital expenditure of roughly $220 million through 2026.

Schwan’s Company Frozen Pizza

Acquired to anchor CJ CheilJedang’s US push, Schwan’s Company Frozen Pizza—led by Red Baron and Tony’s—holds a market-leading share in the US frozen pizza segment; in 2025 the unit grew ~6–8% organic sales, outpacing category peers in premium and single-serve lines and boosting EBITDA margins to roughly 14%. It remains a cash generator, but planned CAPEX of ~$120–150M through 2026 for automation and logistics integration is needed to sustain advantage.

Global Strategic Products (GSP)

Global Strategic Products (GSP) — shelf-stable rice, kimchi, seaweed snacks, and K-sauces — are CJ CheilJedang’s high-growth engine in international markets, posting double-digit revenue growth in 2025 (UK +18%, Germany +15%, Netherlands +22%).

These SKUs grew faster in European mainstream grocery channels than ethnic aisles, lifting total GSP export sales to KRW 420 billion in 2025, up 21% year-on-year.

CJ is funding aggressive marketing and in-store promotions—estimated KRW 35 billion incremental spend in 2025—to shift perception from niche ethnic to convenience staples; ROI targets aim for payback within 18 months.

Specialty Amino Acids

CJ CheilJedang’s bio-engineering unit holds a global-leading share (>40% in 2025) in high-value specialty amino acids like Tryptophan and Valine, classifying them as Stars in the BCG Matrix.

Despite broader bio market volatility in 2025, these high-margin functional ingredients grew ~8–12% YoY, driven by sustainable, health-focused feed additive demand.

The company is reallocating CAPEX and R&D away from commodity amino acids toward technology-intensive Star segments, leveraging a near-technical monopoly and higher EBITDA margins (mid-20s%).

- Global share >40% (2025)

- Growth 8–12% YoY (2025)

- EBITDA margin mid-20s%

- Strategic CAPEX/R&D pivot to Stars

European and Oceania Food Markets

European and Oceania Food Markets are Stars for CJ Cheiljedang, with Europe posting 2025 revenue growth above 13 percent and Oceania up ~9–11 percent, driven by rising K-food demand and low penetration versus the US.

The company sees a large runway for share gains via new distribution partnerships and is prioritizing infrastructure spend—€120–150 million planned across Europe and AUD 40–55 million in Oceania through 2026 to scale cold chain and retail reach.

- 2025 Europe growth >13%

- Oceania growth ~9–11%

- Low K-food penetration vs US

- Planned investment: €120–150M Europe, AUD40–55M Oceania

- Focus: distribution, cold chain, retail partnerships

CJ CheilJedang 2025: $1.2B overseas food, bio amino >40% share, Schwan’s EBITDA ~14%

Stars: Bibigo, Schwan’s frozen pizza, GSP, and specialty amino acids drive CJ CheilJedang’s high-growth portfolio—2025 highlights: overseas food sales $1.2B, GSP exports KRW420B (+21% YoY), bio amino acids global share >40% with 8–12% growth, Schwan’s EBITDA ~14% with CAPEX $120–150M, Europe growth >13% (CAPEX €120–150M), Oceania growth ~9–11% (CAPEX AUD40–55M).

| Unit | 2025 | Growth/CAPEX |

|---|---|---|

| Overseas food sales | $1.2B | — |

| GSP exports | KRW420B | +21% YoY |

| Bio amino acids | >40% share | 8–12% YoY |

| Schwan’s EBITDA | ~14% | CAPEX $120–150M |

| Europe | >13% growth | €120–150M CAPEX |

| Oceania | 9–11% growth | AUD40–55M CAPEX |

What is included in the product

Comprehensive BCG Matrix review of CJ CheilJedang's portfolio, guiding invest/hold/divest decisions with quadrant-specific risks and trends.

One-page BCG matrix mapping CJ CheilJedang units for quick strategic decisions and stakeholder-ready presentations.

Cash Cows

Domestic Processed Foods

CJ CheilJedang dominates South Korea’s processed-foods market with brands like Hetbahn and Spam, holding roughly 30–40% category share and delivering stable domestic FY2024 revenues of about KRW 2.1 trillion from food operations. The mature market—shrinking population (-0.4% YoY in 2024) and CPI-driven inflation near 4%—cuts growth but these SKUs yield high margins and low marketing spend, producing robust free cash flow (~KRW 400–600 billion annually). This cash generation funds CJ’s global expansion and biotech R&D, enabling 2024 capex and M&A outlays of roughly KRW 700 billion.

Sugar and Flour Business

As CJ CheilJedang’s foundational milling and sugar refining units hold dominant market shares in South Korea—estimated domestic market share ~40–60% in wheat milling and ~50% in refined sugar in 2024—they are classic cash cows in a low-growth, mature sector with high entry barriers.

These units need minimal promo spend, generate steady EBITDA margins around 8–12% (2024 pro forma), and supply predictable cash flow that services corporate debt and funds newer, higher-growth businesses like biotech and meal kits.

CJ Logistics Synergy

CJ Logistics Synergy: as CJ CheilJedang’s logistics subsidiary, it anchors the group with a dominant market share in Korea and steady cash generation; in 2025 it reported ~KRW 1.2 trillion revenue and operating profit up 6% YoY, driven by e-commerce fulfillment and contract logistics growth.

Traditional Seasonings and Sauces

Traditional seasonings like Dashida and fermented pastes (jang) hold ~30–40% value share in Korea’s retail condiment category and deliver gross margins around 35–40% for CJ CheilJedang as of FY2024, reflecting mature, low-growth demand but high profitability from scale and lean production.

These products act as cash cows—stable profit anchors—insulated from trend volatility; domestic seasoning volume growth was ~1–2% CAGR 2019–2024 while EBITDA contribution from condiments stayed >20% of CJ Food & Retail FY2024.

- Value share 30–40% in Korea

- Gross margins ~35–40% (FY2024)

- Volume CAGR ~1–2% (2019–2024)

- EBITDA >20% of CJ Food & Retail (FY2024)

Animal Feed and Care (Retained Segments)

Following the 2025 divestiture of underperforming feed assets, CJ CheilJedang’s retained specialized livestock feed operations stabilized into steady cash generators, contributing roughly KRW 120–150 billion in annual EBIT by 2025.

Management now prioritizes core efficiencies and premium feed in stable markets, cutting capital expenditures from KRW 90 billion (pre-2025) to ~KRW 25–35 billion yearly and lifting operating margins to about 12–14%.

Strategy shifted from growth to maximizing livestock spread and operational margins, with return on invested capital (ROIC) for the segment rising to ~11% in 2025.

- 2025 EBIT ~KRW 120–150B

- CapEx cut to KRW 25–35B/yr

- Operating margin ~12–14%

- Segment ROIC ~11% (2025)

CJ CheilJedang’s cash cows drive KRW 400–600B FCF, strong margins & market shares

CJ CheilJedang’s cash cows—processed foods, milling/sugar, seasonings, logistics, and premium feed—generated steady FY2024–2025 cash flows: food revenues ~KRW 2.1T, free cash flow ~KRW 400–600B, milling/sugar market shares ~40–60%/50%, seasonings gross margin 35–40% and EBITDA >20% of food, CJ Logistics revenue ~KRW 1.2T (2025), feed EBIT ~KRW 120–150B (2025).

| Segment | 2024–25 Key |

|---|---|

| Processed foods | Rev KRW 2.1T; FCF KRW 400–600B |

| Milling / sugar | Share 40–60% / ~50% |

| Seasonings | GM 35–40%; EBITDA >20% |

| Logistics | Rev KRW 1.2T (2025) |

| Feed | EBIT KRW 120–150B; ROIC ~11% |

Preview = Final Product

CJ Cheiljedang BCG Matrix

The file you're previewing is the exact CJ CheilJedang BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, strategy-ready document crafted for clarity and practical use.