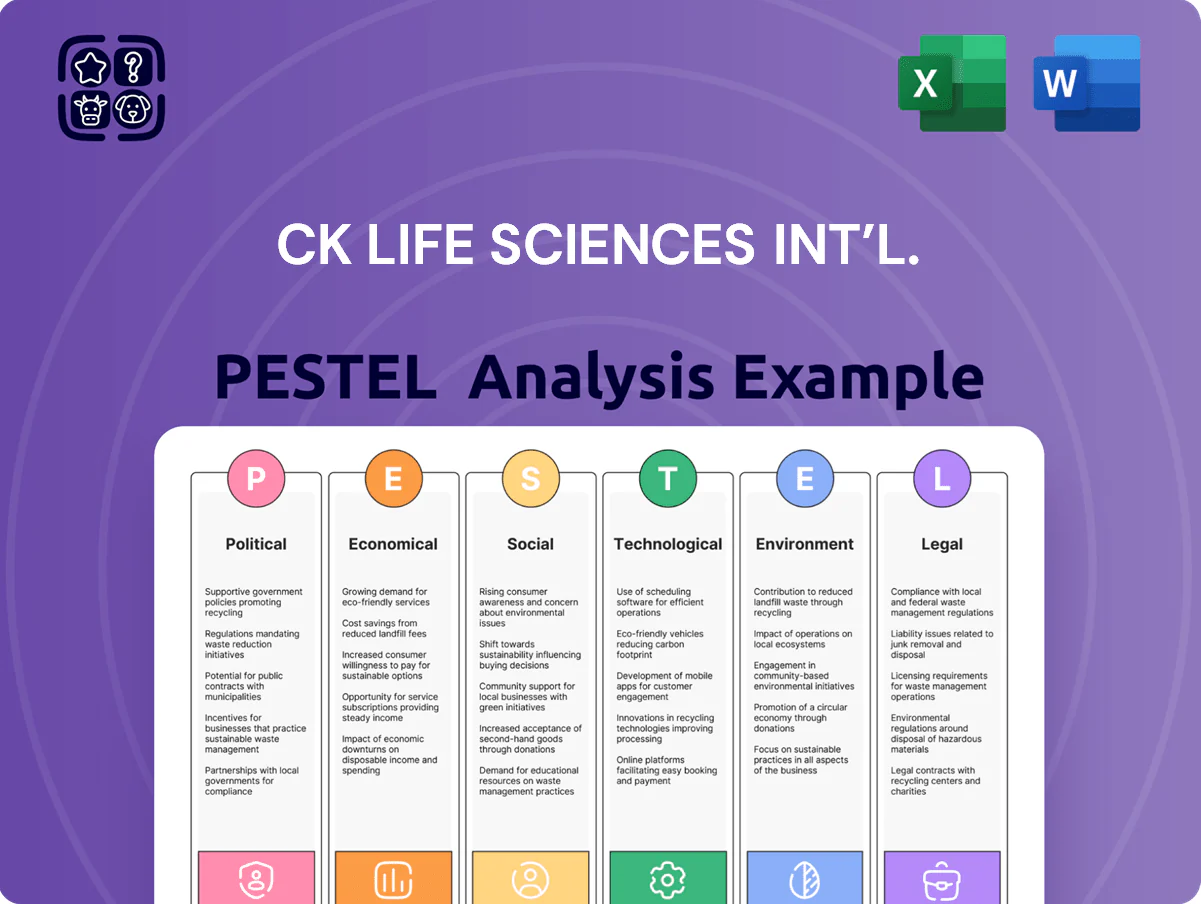

CK Life Sciences Int’l. PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic advantage with our focused PESTLE Analysis of CK Life Sciences Int’l.—uncover how political, economic, social, technological, legal, and environmental forces are shaping the company’s trajectory and use these insights to refine your investment or strategic plan; purchase the full report to access actionable, ready-to-use intelligence instantly.

Political factors

Geopolitical Trade Dynamics

The company’s operations across Australia, North America and Greater China expose it to shifting trade alliances; 2025 saw 18% of CK Life Sciences’ revenues tied to Greater China markets, amplifying risk from diplomatic shifts.

Geopolitical tensions in late 2025 pressured biotech supply chains—global logistics delays rose 12% year-over-year—raising input costs and inventory carrying for the firm’s agri-health lines.

Cross-border capital movement tightened; foreign direct investment into biotech fell 9% in 2025, implying potential constraints on CK Life Sciences’ financing and M&A flexibility.

Strategic planning must model tariff scenarios: a 5–15% tariff on agricultural exports between regions could cut segment margins materially, necessitating rerouting, local sourcing, or price hedges.

Government Healthcare Subsidies

Public health policies and government-funded programs strongly shape demand for CK Life Sciences’ drugs and nutraceuticals; for example, China’s Basic Medical Insurance covers over 1.3 billion people, directly affecting uptake of oncology agents. Changes in reimbursement or subsidy levels for cancer treatments—South Korea cut some cancer drug reimbursements by 10–15% in 2024—can shift R&D ROI and go/no-go decisions. Preventative supplement subsidies or lack thereof in markets like Australia (private market ~AUD 2.5bn in 2024) alter commercial viability. Executives must track legislation favoring cost containment over premium biotech to anticipate margin and pipeline impacts.

Agricultural Land Ownership Regulations

As one of Australasia’s largest vineyard owners, CK Life Sciences faces political scrutiny over foreign ownership of agricultural land, with New Zealand and Australia reviewing ~15–25% of sensitive transactions annually; recent proposals could cut foreign acquisition approvals by up to 30%, raising compliance costs and transaction delays. Ongoing engagement with local authorities and legal counsel is essential to protect its ~10,000+ hectare real estate portfolio and cash-flow projections tied to land permits.

Research and Development Incentives

CK Life Sciences depends on government R&D tax credits and grants that covered an estimated HKD 120–150 million of R&D spending in 2024, reducing net pipeline investment significantly.

Policy moves to cut or expand incentives would alter capital allocation; a 10% reduction in credits could raise R&D net costs by ~HKD 12–15 million, slowing project starts.

Analysts monitor legislative changes and 2025 budget signals to forecast R&D cadence and related capex needs for biotech and sustainable-agro programs.

- 2024 R&D support ~HKD 120–150M

- 10% credit cut ≈ HKD 12–15M higher net R&D cost

- Policy shifts drive capex and project timing forecasts

Global Health Security Initiatives

The 2025 post-pandemic political focus on health and agri self-sufficiency boosts demand for local production; 62% of OECD nations reported new supply-security measures in 2024 that favor domestic manufacturers, creating market access risks for CK Life Sciences Int’l.

Governments are subsidizing local medicine and fertilizer production—EU and US incentives totaled over $45bn in 2024—so CK must localize manufacturing or partner with domestic firms to avoid preferential procurement barriers.

Aligning R&D and supply-chain investments with national security priorities—targeting markets where CK already has local facilities or JV presence—will protect revenue streams and sustain competitive positioning across 30+ countries.

- 62% of OECD countries enacted supply-security measures in 2024

- US/EU health/agri incentives > $45bn in 2024

- Exposure across 30+ countries; prioritize localization or JVs

Geopolitical headwinds: China 18% revenues, FDI -9%, R&D cuts, supply-security surge

Political risks: 2025 revenues: 18% Greater China; FDI into biotech -9% (2025); R&D tax credits ~HKD 120–150M (2024) — a 10% cut ≈ HKD 12–15M impact; 62% OECD supply-security measures (2024); US/EU health/agri incentives > $45bn (2024); land-review proposals could cut foreign approvals by up to 30%.

| Metric | 2024/25 |

|---|---|

| Greater China rev share | 18% |

| FDI biotech | -9% |

| R&D credits | HKD 120–150M |

| OECD measures | 62% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CK Life Sciences Int’l. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to identify actionable threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary for CK Life Sciences Int’l that’s easy to drop into presentations, share across teams, and annotate with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Global Interest Rate Fluctuations

CK Life Sciences’ large asset base and reliance on debt for R&D and acquisitions make it sensitive to global interest rate shifts; average corporate borrowing costs fell from ~5.2% in 2023 peak to ~4.1% by Q4 2025, easing financing pressures.

Lower terminal rates have reduced discount rates used in long-term pharma DCFs from ~9–10% to ~7–8%, boosting NPV on late-stage projects.

Investors track US Fed and RBA moves—US policy rates eased to 4.25%–4.50% and Australia to 3.10% by end-2025—to reassess interest coverage ratios (currently near 4.0x) and revalue land holdings in Hong Kong and Australia.

Currency Exchange Volatility

With revenue in AUD, NZD, USD and HKD, CK Life Sciences faces significant translational and transactional currency risk; FY2024 reported ~28% of revenue from Australia/NZ, amplifying AUD/USD moves on consolidated results.

Between 2023–2025 AUD/USD swung ~0.60–0.73, materially affecting agricultural earnings and imported input costs; a 10% AUD depreciation increases USD-equivalent input costs ~10%.

Management uses hedging (forwards/options) and geographic diversification—~40% non-HKD revenue in 2024—to mitigate volatility as a core financial risk control.

Inflationary Pressure on Operating Costs

Persistent inflation through 2024–25 raised energy, labor and raw-material costs by roughly 6–9% annually, squeezing margins in fertilizer operations where input-linked commodity sensitivity limits pass-through.

CK Life Sciences retains pricing power in premium nutraceuticals, supporting 3–5% revenue uplifts, but agricultural segment gross margins fell about 120–180 bps in 2024.

Balancing rising input costs against consumer price elasticity and competitive pressure remains a key economic challenge for the executive team.

Agricultural Commodity Price Cycles

The agricultural division’s margins track cyclical crop, wine grape and salt prices; global wheat and corn futures fell ~8–12% in 2024, pressuring revenue, while premium wine grape prices rose ~5% in key regions.

Shifts in global demand—driven by dietary trends and industrial feed use—caused commodity revenue volatility of ±15% annually for similar firms in 2023–2024.

Diversification across crops, viticulture and salt reduced company-level commodity exposure, historically cutting annual revenue volatility by an estimated 6–9%.

- Revenue sensitivity: ±15% commodity-driven swings

- Diversification impact: ~6–9% lower volatility

- 2024 price moves: wheat/corn −8–12%, premium grapes +5%

Consumer Discretionary Spending Trends

The nutraceutical and supplement segment depends on consumer disposable income; global wellness market reached about $7.2 trillion in 2024, with supplements ~$220bn, and sales correlate with household discretionary spending trends.

When budgets tighten, premium product demand becomes more price-elastic; e.g., 2023–24 data showed mid/high-end supplement unit volumes fell ~6% in some APAC markets while value tiers grew.

CK Life Sciences should use targeted marketing and multi-tier product lines to capture demand across income segments and protect margins during slower GDP growth.

- Global wellness market $7.2T (2024); supplements ~$220B

- Premium supplement volumes down ~6% in parts of APAC (2023–24)

- Strategy: targeted marketing + product tiering to retain share

Lower rates boost NPVs; FX swings and input inflation squeeze ag margins

Interest-costs eased (corp borrowing ~4.1% by Q4 2025), lowering DCF discount rates to ~7–8% and boosting NPVs; FX exposure (28% revenue Australia/NZ in FY2024) and AUD/USD swings (0.60–0.73 2023–25) materially affect consolidated results; input inflation 2024–25 raised costs ~6–9%, squeezing agricultural margins ~120–180 bps while nutraceuticals saw 3–5% pricing power gains.

| Metric | Value |

|---|---|

| Corp borrowing (Q4 2025) | ~4.1% |

| DCF rates | ~7–8% |

| AUD/USD range (2023–25) | 0.60–0.73 |

| FY2024 AU/NZ revenue | ~28% |

| Input inflation (2024–25) | ~6–9% |

| Agric. margin decline 2024 | 120–180 bps |

Same Document Delivered

CK Life Sciences Int’l. PESTLE Analysis

The preview shown here is the exact CK Life Sciences Int’l. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic advantage with our focused PESTLE Analysis of CK Life Sciences Int’l.—uncover how political, economic, social, technological, legal, and environmental forces are shaping the company’s trajectory and use these insights to refine your investment or strategic plan; purchase the full report to access actionable, ready-to-use intelligence instantly.

Political factors

Geopolitical Trade Dynamics

The company’s operations across Australia, North America and Greater China expose it to shifting trade alliances; 2025 saw 18% of CK Life Sciences’ revenues tied to Greater China markets, amplifying risk from diplomatic shifts.

Geopolitical tensions in late 2025 pressured biotech supply chains—global logistics delays rose 12% year-over-year—raising input costs and inventory carrying for the firm’s agri-health lines.

Cross-border capital movement tightened; foreign direct investment into biotech fell 9% in 2025, implying potential constraints on CK Life Sciences’ financing and M&A flexibility.

Strategic planning must model tariff scenarios: a 5–15% tariff on agricultural exports between regions could cut segment margins materially, necessitating rerouting, local sourcing, or price hedges.

Government Healthcare Subsidies

Public health policies and government-funded programs strongly shape demand for CK Life Sciences’ drugs and nutraceuticals; for example, China’s Basic Medical Insurance covers over 1.3 billion people, directly affecting uptake of oncology agents. Changes in reimbursement or subsidy levels for cancer treatments—South Korea cut some cancer drug reimbursements by 10–15% in 2024—can shift R&D ROI and go/no-go decisions. Preventative supplement subsidies or lack thereof in markets like Australia (private market ~AUD 2.5bn in 2024) alter commercial viability. Executives must track legislation favoring cost containment over premium biotech to anticipate margin and pipeline impacts.

Agricultural Land Ownership Regulations

As one of Australasia’s largest vineyard owners, CK Life Sciences faces political scrutiny over foreign ownership of agricultural land, with New Zealand and Australia reviewing ~15–25% of sensitive transactions annually; recent proposals could cut foreign acquisition approvals by up to 30%, raising compliance costs and transaction delays. Ongoing engagement with local authorities and legal counsel is essential to protect its ~10,000+ hectare real estate portfolio and cash-flow projections tied to land permits.

Research and Development Incentives

CK Life Sciences depends on government R&D tax credits and grants that covered an estimated HKD 120–150 million of R&D spending in 2024, reducing net pipeline investment significantly.

Policy moves to cut or expand incentives would alter capital allocation; a 10% reduction in credits could raise R&D net costs by ~HKD 12–15 million, slowing project starts.

Analysts monitor legislative changes and 2025 budget signals to forecast R&D cadence and related capex needs for biotech and sustainable-agro programs.

- 2024 R&D support ~HKD 120–150M

- 10% credit cut ≈ HKD 12–15M higher net R&D cost

- Policy shifts drive capex and project timing forecasts

Global Health Security Initiatives

The 2025 post-pandemic political focus on health and agri self-sufficiency boosts demand for local production; 62% of OECD nations reported new supply-security measures in 2024 that favor domestic manufacturers, creating market access risks for CK Life Sciences Int’l.

Governments are subsidizing local medicine and fertilizer production—EU and US incentives totaled over $45bn in 2024—so CK must localize manufacturing or partner with domestic firms to avoid preferential procurement barriers.

Aligning R&D and supply-chain investments with national security priorities—targeting markets where CK already has local facilities or JV presence—will protect revenue streams and sustain competitive positioning across 30+ countries.

- 62% of OECD countries enacted supply-security measures in 2024

- US/EU health/agri incentives > $45bn in 2024

- Exposure across 30+ countries; prioritize localization or JVs

Geopolitical headwinds: China 18% revenues, FDI -9%, R&D cuts, supply-security surge

Political risks: 2025 revenues: 18% Greater China; FDI into biotech -9% (2025); R&D tax credits ~HKD 120–150M (2024) — a 10% cut ≈ HKD 12–15M impact; 62% OECD supply-security measures (2024); US/EU health/agri incentives > $45bn (2024); land-review proposals could cut foreign approvals by up to 30%.

| Metric | 2024/25 |

|---|---|

| Greater China rev share | 18% |

| FDI biotech | -9% |

| R&D credits | HKD 120–150M |

| OECD measures | 62% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CK Life Sciences Int’l. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to identify actionable threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary for CK Life Sciences Int’l that’s easy to drop into presentations, share across teams, and annotate with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Global Interest Rate Fluctuations

CK Life Sciences’ large asset base and reliance on debt for R&D and acquisitions make it sensitive to global interest rate shifts; average corporate borrowing costs fell from ~5.2% in 2023 peak to ~4.1% by Q4 2025, easing financing pressures.

Lower terminal rates have reduced discount rates used in long-term pharma DCFs from ~9–10% to ~7–8%, boosting NPV on late-stage projects.

Investors track US Fed and RBA moves—US policy rates eased to 4.25%–4.50% and Australia to 3.10% by end-2025—to reassess interest coverage ratios (currently near 4.0x) and revalue land holdings in Hong Kong and Australia.

Currency Exchange Volatility

With revenue in AUD, NZD, USD and HKD, CK Life Sciences faces significant translational and transactional currency risk; FY2024 reported ~28% of revenue from Australia/NZ, amplifying AUD/USD moves on consolidated results.

Between 2023–2025 AUD/USD swung ~0.60–0.73, materially affecting agricultural earnings and imported input costs; a 10% AUD depreciation increases USD-equivalent input costs ~10%.

Management uses hedging (forwards/options) and geographic diversification—~40% non-HKD revenue in 2024—to mitigate volatility as a core financial risk control.

Inflationary Pressure on Operating Costs

Persistent inflation through 2024–25 raised energy, labor and raw-material costs by roughly 6–9% annually, squeezing margins in fertilizer operations where input-linked commodity sensitivity limits pass-through.

CK Life Sciences retains pricing power in premium nutraceuticals, supporting 3–5% revenue uplifts, but agricultural segment gross margins fell about 120–180 bps in 2024.

Balancing rising input costs against consumer price elasticity and competitive pressure remains a key economic challenge for the executive team.

Agricultural Commodity Price Cycles

The agricultural division’s margins track cyclical crop, wine grape and salt prices; global wheat and corn futures fell ~8–12% in 2024, pressuring revenue, while premium wine grape prices rose ~5% in key regions.

Shifts in global demand—driven by dietary trends and industrial feed use—caused commodity revenue volatility of ±15% annually for similar firms in 2023–2024.

Diversification across crops, viticulture and salt reduced company-level commodity exposure, historically cutting annual revenue volatility by an estimated 6–9%.

- Revenue sensitivity: ±15% commodity-driven swings

- Diversification impact: ~6–9% lower volatility

- 2024 price moves: wheat/corn −8–12%, premium grapes +5%

Consumer Discretionary Spending Trends

The nutraceutical and supplement segment depends on consumer disposable income; global wellness market reached about $7.2 trillion in 2024, with supplements ~$220bn, and sales correlate with household discretionary spending trends.

When budgets tighten, premium product demand becomes more price-elastic; e.g., 2023–24 data showed mid/high-end supplement unit volumes fell ~6% in some APAC markets while value tiers grew.

CK Life Sciences should use targeted marketing and multi-tier product lines to capture demand across income segments and protect margins during slower GDP growth.

- Global wellness market $7.2T (2024); supplements ~$220B

- Premium supplement volumes down ~6% in parts of APAC (2023–24)

- Strategy: targeted marketing + product tiering to retain share

Lower rates boost NPVs; FX swings and input inflation squeeze ag margins

Interest-costs eased (corp borrowing ~4.1% by Q4 2025), lowering DCF discount rates to ~7–8% and boosting NPVs; FX exposure (28% revenue Australia/NZ in FY2024) and AUD/USD swings (0.60–0.73 2023–25) materially affect consolidated results; input inflation 2024–25 raised costs ~6–9%, squeezing agricultural margins ~120–180 bps while nutraceuticals saw 3–5% pricing power gains.

| Metric | Value |

|---|---|

| Corp borrowing (Q4 2025) | ~4.1% |

| DCF rates | ~7–8% |

| AUD/USD range (2023–25) | 0.60–0.73 |

| FY2024 AU/NZ revenue | ~28% |

| Input inflation (2024–25) | ~6–9% |

| Agric. margin decline 2024 | 120–180 bps |

Same Document Delivered

CK Life Sciences Int’l. PESTLE Analysis

The preview shown here is the exact CK Life Sciences Int’l. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.