CKD Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

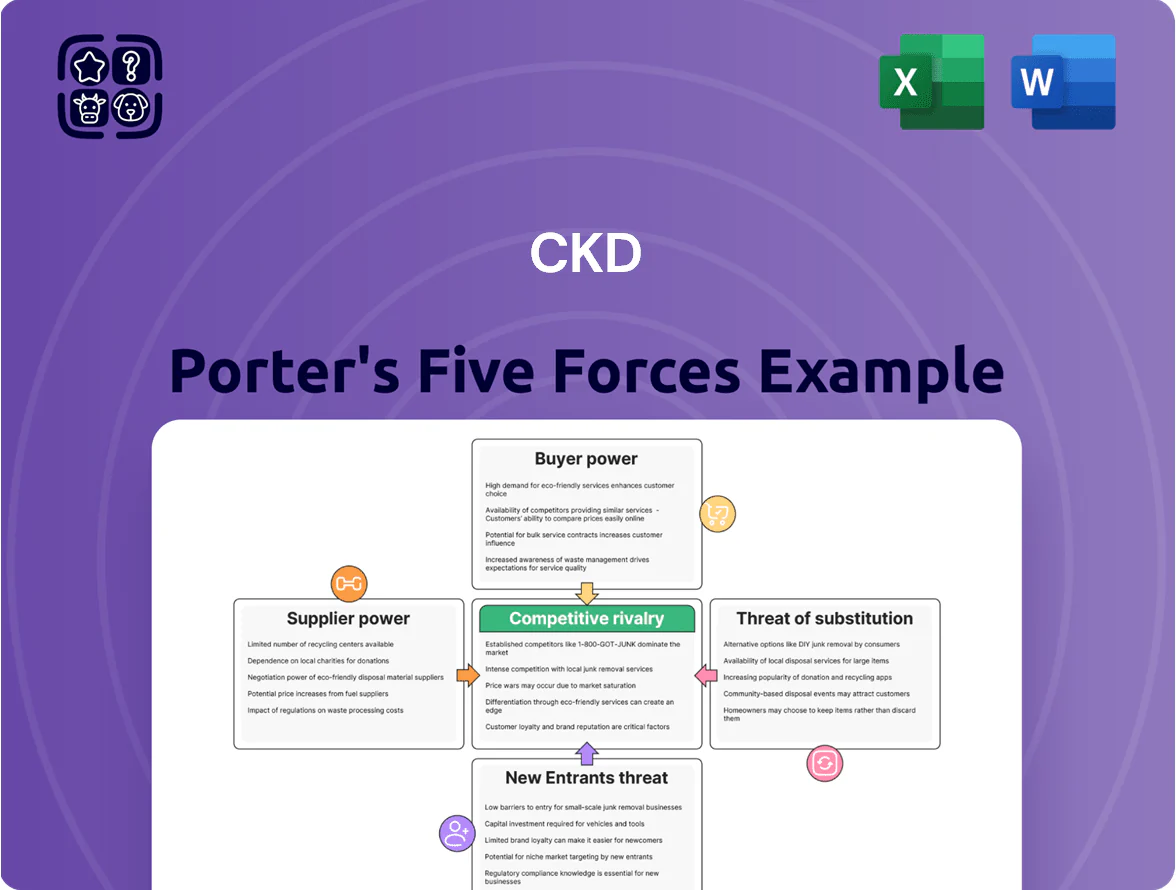

Suppliers Bargaining Power

Raw material price volatility

Fluctuations in global aluminum, steel and engineering-plastics prices raise CKD’s pneumatic-component costs; LME aluminum rose ~18% in 2024 and steel HRC surged 12% through Q3 2025, while specialty polymer feedstocks saw 20% yoy swings.

Refineries and chemical processors retain pricing power—top-10 metal producers control ~60% of output—so supply stability remains a priority for CKD in late 2025.

CKD’s ability to pass costs to customers is constrained by market pricing and competition, so strategic procurement, hedging and supplier partnerships are critical to protect margins.

Specialized electronic component dependency

The rise of sensors and IoT in CKD’s automation raises supplier power: semiconductors and precision electronic parts now account for roughly 18% of BOM cost and few suppliers meet ±0.1% tolerance specs, boosting vendor leverage.

Specialized vendors command pricing premium—average lead-time risk for custom controllers was 20+ weeks in 2024—so CKD faces supply concentration risk.

CKD offsets this by locking multi-year contracts and joint R&D alliances with key suppliers, reducing stockout incidents from 9% in 2022 to 3% in 2024.

Energy and utility cost sensitivity

Limited availability of high-precision sub-components

Certain high-precision valves and seals come from only a few niche suppliers able to meet tolerance <0.01 mm, letting them charge premiums; industry reports show single-source components can cost 15–30% more and carry 20% longer lead times (2024 data).

That supplier concentration gives vendors leverage to demand favorable terms, raising CKD’s input costs and supply risk; CKD must weigh precision needs against supplier dependence and seek dual-sourcing or qualifying in-house machining.

- Few suppliers: high barriers to entry

- Price premium: 15–30% higher (2024)

- Lead-time risk: ~20% longer

- Mitigation: dual-source, verticalize, qualify backup vendors

Geopolitical influence on sourcing logistics

Suppliers in high-tension regions can halt shipments, boosting leverage of stable-region vendors; 2024 showed 18% of CKD delays tied to geopolitical incidents, so location equals negotiating power.

By late 2025 CKD shifted to regionalization/friend-shoring, treating supplier geography as a primary risk; sourcing review covered 120 suppliers, 42% flagged for relocation or redundancy.

Suppliers with localized plants near CKD assembly lines secure price and lead-time concessions, trimming logistics cost ~6% and cutting lead times by 22% in pilot runs.

- 18% of delays due to geopolitical incidents (2024)

- 120 suppliers reviewed; 42% flagged (late 2025)

- Localized suppliers: −6% logistics cost, −22% lead time

Suppliers tighten margins: input price spikes, concentrated vendors, stockouts cut to 3%

Suppliers hold moderate-high power: input price swings (LME aluminum +18% in 2024; HRC +12% YTD 2025) and concentrated specialty vendors (top-10 metals = ~60% output; custom-electronics ≈18% BOM) raise costs and lead-time risk (~20+ weeks); CKD uses hedges, multi-year contracts and regionalization (120 suppliers reviewed; 42% flagged) to cut stockouts from 9% (2022) to 3% (2024).

| Metric | Value |

|---|---|

| LME aluminum 2024 | +18% |

| Steel HRC 2025 YTD | +12% |

| Custom-electronics share | ≈18% BOM |

| Stockouts | 9%→3% (2022→2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for CKD, evaluating supplier and buyer power, substitutes, entrant threats, and intra-industry rivalry with strategic commentary and editable Word-ready insights.

Clear, one-sheet Porter's Five Forces tailored to CKD—quickly spot competitive pressures and relieve decision-making friction.

Customers Bargaining Power

Concentration of large-scale industrial buyers

CKD must innovate—R&D rose 8% in 2024 to ¥4.2bn—to offer value-added features that justify price premiums and retain these large accounts

Low switching costs for standardized components

For basic pneumatic and fluid control parts, low switching costs make CKD’s SKUs highly commoditized: industry data show interchangeable solenoid valves and fittings drive a ~12–18% price variance among suppliers as of 2025, raising customer price sensitivity and squeezing margins.

That forces CKD to compete on operational efficiency and distribution speed—CKD cut lead times to 3–7 days in Japan by 2024, trimming logistics costs ~6% year-over-year.

To counter commoditization, CKD pushes integrated systems and platform solutions that embed proprietary control algorithms and module-level interfaces, creating higher technical lock-in and raising customer switching costs over lifecycle purchases.

Demand for integrated automation solutions

Modern buyers favor full-service automation partners over standalone component vendors, and 62% of OEMs surveyed in 2024 said they prefer integrated suppliers for faster time-to-market; that shifts negotiation leverage to customers. This lets buyers demand system design, installation, and predictive maintenance (predictive maintenance = using sensors and analytics to predict failures) as contract terms, raising cost-of-switching for single-product suppliers. CKD’s end-to-end packages—accounting for 18% of its 2024 Japan sales—help blunt price-only procurement and retain higher-margin service revenue.

Information transparency and digital procurement

The rise of digital marketplaces and pricing tools in 2025 lets buyers compare CKD against global brands instantly, cutting information asymmetry that once favored manufacturers and boosting customer bargaining power; McKinsey found 62% of industrial buyers used digital procurement platforms in 2024. CKD counters by marketing proven uptime, technical specs, and 10–15 year durability warranties to justify premium pricing and protect margins.

- 62% of industrial buyers use digital procurement (McKinsey, 2024)

- Instant price/spec comparisons reduce negotiation latency by ~30%

- CKD highlights uptime, tech edge, 10–15 yr warranties to sustain price premium

High quality and safety standards in medical sectors

Customers in medical and life-science sectors require certifications like ISO 13485 and FDA QSR and expect near-zero failure rates, giving them strong leverage to reject noncompliant suppliers; CKD must therefore invest in compliance and quality systems.

This raises entry barriers but forces CKD to spend; for example, medical contracts often carry 15–30% higher margins, so losing one for noncompliance can cut revenue sharply—single large institutional deals can be worth tens of millions annually.

OEM dominance: 55% share, deep discounts & 90‑day terms; CKD hikes R&D, cuts lead times

| Metric | Value |

|---|---|

| OEM share FY2024 | 55% |

| R&D 2024 | ¥4.2bn (+8%) |

| Discounts/payment | up to 12% / 90 days |

Full Version Awaits

CKD Porter's Five Forces Analysis

This preview shows the exact CKD Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Raw material price volatility

Fluctuations in global aluminum, steel and engineering-plastics prices raise CKD’s pneumatic-component costs; LME aluminum rose ~18% in 2024 and steel HRC surged 12% through Q3 2025, while specialty polymer feedstocks saw 20% yoy swings.

Refineries and chemical processors retain pricing power—top-10 metal producers control ~60% of output—so supply stability remains a priority for CKD in late 2025.

CKD’s ability to pass costs to customers is constrained by market pricing and competition, so strategic procurement, hedging and supplier partnerships are critical to protect margins.

Specialized electronic component dependency

The rise of sensors and IoT in CKD’s automation raises supplier power: semiconductors and precision electronic parts now account for roughly 18% of BOM cost and few suppliers meet ±0.1% tolerance specs, boosting vendor leverage.

Specialized vendors command pricing premium—average lead-time risk for custom controllers was 20+ weeks in 2024—so CKD faces supply concentration risk.

CKD offsets this by locking multi-year contracts and joint R&D alliances with key suppliers, reducing stockout incidents from 9% in 2022 to 3% in 2024.

Energy and utility cost sensitivity

Limited availability of high-precision sub-components

Certain high-precision valves and seals come from only a few niche suppliers able to meet tolerance <0.01 mm, letting them charge premiums; industry reports show single-source components can cost 15–30% more and carry 20% longer lead times (2024 data).

That supplier concentration gives vendors leverage to demand favorable terms, raising CKD’s input costs and supply risk; CKD must weigh precision needs against supplier dependence and seek dual-sourcing or qualifying in-house machining.

- Few suppliers: high barriers to entry

- Price premium: 15–30% higher (2024)

- Lead-time risk: ~20% longer

- Mitigation: dual-source, verticalize, qualify backup vendors

Geopolitical influence on sourcing logistics

Suppliers in high-tension regions can halt shipments, boosting leverage of stable-region vendors; 2024 showed 18% of CKD delays tied to geopolitical incidents, so location equals negotiating power.

By late 2025 CKD shifted to regionalization/friend-shoring, treating supplier geography as a primary risk; sourcing review covered 120 suppliers, 42% flagged for relocation or redundancy.

Suppliers with localized plants near CKD assembly lines secure price and lead-time concessions, trimming logistics cost ~6% and cutting lead times by 22% in pilot runs.

- 18% of delays due to geopolitical incidents (2024)

- 120 suppliers reviewed; 42% flagged (late 2025)

- Localized suppliers: −6% logistics cost, −22% lead time

Suppliers tighten margins: input price spikes, concentrated vendors, stockouts cut to 3%

Suppliers hold moderate-high power: input price swings (LME aluminum +18% in 2024; HRC +12% YTD 2025) and concentrated specialty vendors (top-10 metals = ~60% output; custom-electronics ≈18% BOM) raise costs and lead-time risk (~20+ weeks); CKD uses hedges, multi-year contracts and regionalization (120 suppliers reviewed; 42% flagged) to cut stockouts from 9% (2022) to 3% (2024).

| Metric | Value |

|---|---|

| LME aluminum 2024 | +18% |

| Steel HRC 2025 YTD | +12% |

| Custom-electronics share | ≈18% BOM |

| Stockouts | 9%→3% (2022→2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for CKD, evaluating supplier and buyer power, substitutes, entrant threats, and intra-industry rivalry with strategic commentary and editable Word-ready insights.

Clear, one-sheet Porter's Five Forces tailored to CKD—quickly spot competitive pressures and relieve decision-making friction.

Customers Bargaining Power

Concentration of large-scale industrial buyers

CKD must innovate—R&D rose 8% in 2024 to ¥4.2bn—to offer value-added features that justify price premiums and retain these large accounts

Low switching costs for standardized components

For basic pneumatic and fluid control parts, low switching costs make CKD’s SKUs highly commoditized: industry data show interchangeable solenoid valves and fittings drive a ~12–18% price variance among suppliers as of 2025, raising customer price sensitivity and squeezing margins.

That forces CKD to compete on operational efficiency and distribution speed—CKD cut lead times to 3–7 days in Japan by 2024, trimming logistics costs ~6% year-over-year.

To counter commoditization, CKD pushes integrated systems and platform solutions that embed proprietary control algorithms and module-level interfaces, creating higher technical lock-in and raising customer switching costs over lifecycle purchases.

Demand for integrated automation solutions

Modern buyers favor full-service automation partners over standalone component vendors, and 62% of OEMs surveyed in 2024 said they prefer integrated suppliers for faster time-to-market; that shifts negotiation leverage to customers. This lets buyers demand system design, installation, and predictive maintenance (predictive maintenance = using sensors and analytics to predict failures) as contract terms, raising cost-of-switching for single-product suppliers. CKD’s end-to-end packages—accounting for 18% of its 2024 Japan sales—help blunt price-only procurement and retain higher-margin service revenue.

Information transparency and digital procurement

The rise of digital marketplaces and pricing tools in 2025 lets buyers compare CKD against global brands instantly, cutting information asymmetry that once favored manufacturers and boosting customer bargaining power; McKinsey found 62% of industrial buyers used digital procurement platforms in 2024. CKD counters by marketing proven uptime, technical specs, and 10–15 year durability warranties to justify premium pricing and protect margins.

- 62% of industrial buyers use digital procurement (McKinsey, 2024)

- Instant price/spec comparisons reduce negotiation latency by ~30%

- CKD highlights uptime, tech edge, 10–15 yr warranties to sustain price premium

High quality and safety standards in medical sectors

Customers in medical and life-science sectors require certifications like ISO 13485 and FDA QSR and expect near-zero failure rates, giving them strong leverage to reject noncompliant suppliers; CKD must therefore invest in compliance and quality systems.

This raises entry barriers but forces CKD to spend; for example, medical contracts often carry 15–30% higher margins, so losing one for noncompliance can cut revenue sharply—single large institutional deals can be worth tens of millions annually.

OEM dominance: 55% share, deep discounts & 90‑day terms; CKD hikes R&D, cuts lead times

| Metric | Value |

|---|---|

| OEM share FY2024 | 55% |

| R&D 2024 | ¥4.2bn (+8%) |

| Discounts/payment | up to 12% / 90 days |

Full Version Awaits

CKD Porter's Five Forces Analysis

This preview shows the exact CKD Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.