Clarus PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and technological advances are shaping Clarus’s strategic outlook with our concise PESTLE snapshot—crafted for investors and strategists who need actionable insight fast; buy the full analysis to access the complete, editable report and make smarter, faster decisions.

Political factors

Global Trade Policy and Tariffs

As of late 2025, shifting trade alliances and rising protectionist measures have increased supply-chain volatility for Clarus brands like Black Diamond, with Asian-origin raw material import duties rising by an average of 6.2% year-over-year and freight costs up 18% since 2023.

Changes in tariffs on finished goods entering North America have squeezed manufacturing margins, contributing to a reported 120–180 basis point decline in gross margin for comparable outdoor-equipment peers in 2024–25.

Management must navigate these geopolitical tensions, reoptimizing supplier footprints and passing limited cost increases to customers while targeting a 3–5% price-competitiveness buffer to protect market share.

Geopolitical Stability in Manufacturing Hubs

Government Outdoor Recreation Initiatives

Export Control and Defense Regulations

Certain Sierra-brand precision optics and match-grade components may fall under US export controls (ITAR/EAR); in 2024 the Commerce Dept. added multiple optics categories to stricter controls, raising compliance costs by an estimated 5–8% for affected manufacturers.

Maintaining alignment with evolving federal and allied-country mandates on sale and shipment is essential to avoid fines—recent penalties in 2023–24 exceeded $100m industry-wide—so Clarus must invest in licensing and supply-chain screening.

Political shifts on firearm accessories require a proactive regulatory strategy; tracking 50+ pending state/federal bills and updating export-classification procedures reduces operational disruption and market-access risks.

- ITAR/EAR exposure for precision optics; 5–8% added compliance cost

- Industry fines >$100m in 2023–24 signal enforcement risk

- Monitor 50+ pending firearm-related bills; update licensing and screening

Labor Laws and Minimum Wage Shifts

Political movements pushing minimum wages up to $15–$20/hour in several US states raise Clarus’s domestic labor costs; a 10–15% wage uplift could increase assembly/distribution OPEX materially versus 2024 payrolls of $120M.

Changes in labor relations laws reducing flexible scheduling can hurt peak-season capacity, potentially increasing temporary staffing costs by 8–12% during Q4 demand spikes.

Clarus must weigh social responsibility against rising mandated labor expenses under new administrations, which could compress gross margins by 50–150 bps if costs are passed through.

- Higher minimum wages: $15–$20/hr; 10–15% payroll impact

- Scheduling restrictions: +8–12% peak temporary costs

- Margin pressure: 50–150 basis points potential compression

Supply shocks, tariffs and compliance squeeze margins as federal funding boosts market

Geopolitical trade barriers and tariffs raised input costs ~6–18% (2023–25), cutting peers’ gross margins 120–180 bps; 27% of BOM sourced from Vietnam/Mexico exposes Clarus to 8.5% 2024 supply shortfall and 6–12 week supplier-switch timelines; ITAR/EAR optics controls add 5–8% compliance costs; federal outdoor funding ($1.5B+/yr) and $400M trail grants (2024) expand addressable market.

| Metric | Value |

|---|---|

| Tariff/freight rise | 6–18% |

| Peers’ margin hit | 120–180 bps |

| BOM from VN/MX | 27% |

| Supply drop (2024) | 8.5% |

| ITAR/EAR cost | 5–8% |

| Federal outdoor funding | $1.5B+/yr |

| Trail grants (2024) | $400M |

What is included in the product

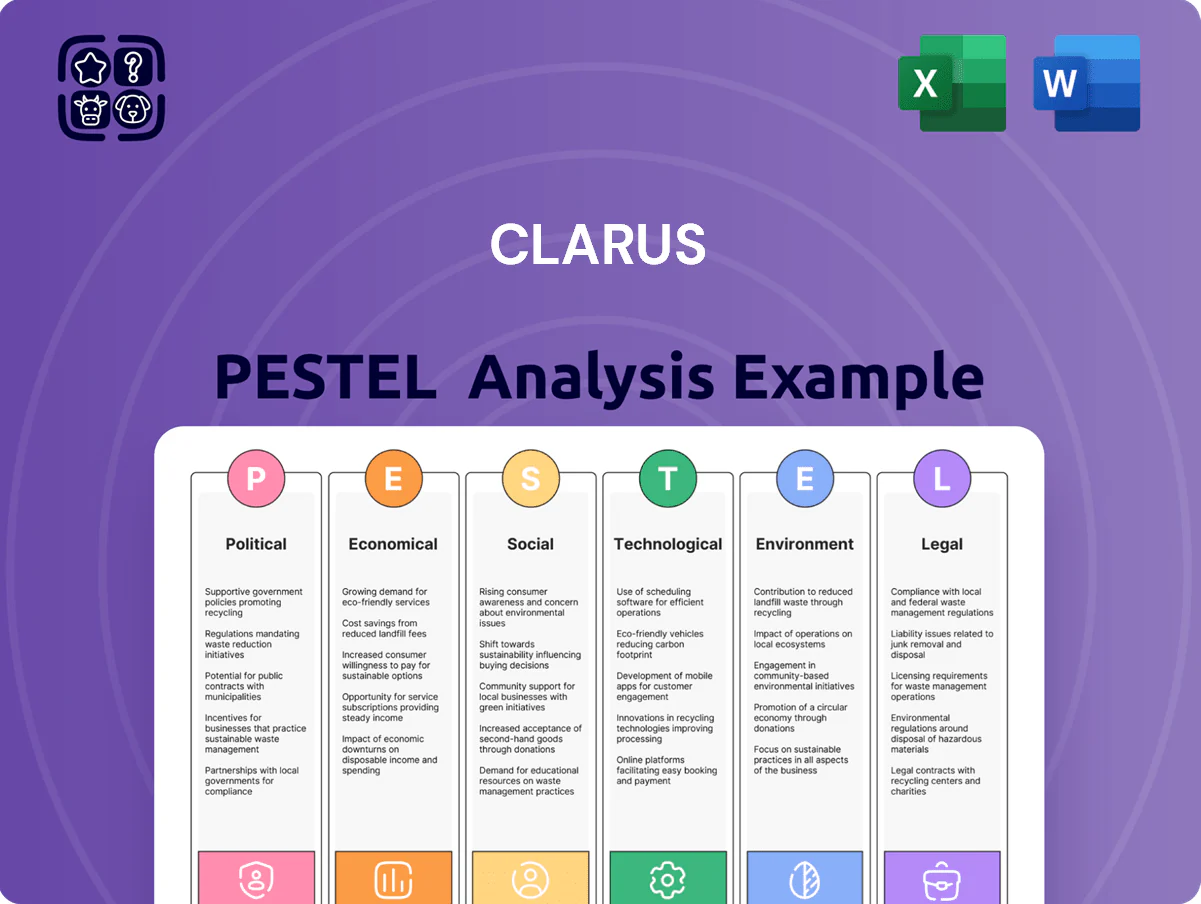

Explores how external macro-environmental factors uniquely affect the Clarus across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Provides a clean, summarized PESTLE snapshot that’s visually segmented for quick interpretation and easily dropped into presentations or shared for rapid team alignment.

Economic factors

Consumer Discretionary Spending Trends

Demand for premium outdoor gear is highly tied to disposable income; OECD data showed household real disposable income in major markets fell 0.8% y/y in H2 2025, increasing price sensitivity for high-ticket items like Rhino-Rack and pro skiing equipment.

Inflationary pressures (global CPI averaging 4.1% in 2025) and a 1.2% slowdown in US retail spending on sporting goods through Q3 2025 led many consumers to defer purchases.

Clarus monitors unemployment, consumer confidence (GfK indices down 6 points in 2025) and retail sales monthly to adjust production volumes and inventory, reducing output by targeted percentages during demand soft patches.

Fluctuations in Foreign Exchange Rates

As a global entity, Clarus faces currency volatility that impacted FY2024 reported revenue, with a 5% headwind from USD strength versus EUR and AUD, reducing translated sales by about $18m; a stronger dollar can make products ~10–15% costlier for European and Australian buyers, pressuring demand. Clarus uses FX hedges—forward contracts and options—covering roughly 60% of projected FX exposure to limit P&L volatility.

Interest Rate Environment and Capital Cost

As of end-2025, the US Federal Funds rate near 5.25%–5.50% raised Clarus’s weighted average cost of debt, pushing borrowing costs for acquisitions and R&D to roughly 200–300 basis points above pre-2022 levels and increasing annual interest expense by an estimated $8–12m on $400m of new debt.

Raw Material and Commodity Pricing

Raw material costs for Clarus brands Black Diamond and Rhino-Rack—notably aluminum, steel and specialty polymers—track volatile commodity cycles; LME aluminum rose ~12% in 2024 while US steel HRC averaged $780/ton in 2024, pressuring margins when costs can't be passed to customers.

Energy-driven input inflation and freight spikes in 2022–24 tightened gross margins; long-term sourcing and hedges plus supply-chain efficiency are critical to stabilise input cost exposure.

- 2024 LME aluminum +12% year; US HRC ~$780/ton 2024

- Energy/freight inflation 2022–24 amplified input costs

- Long-term contracts, hedging, logistics efficiency mitigate margin risk

Global Logistics and Freight Costs

Global logistics costs, driven by fuel surcharges and container availability, directly raise Clarus’s landed cost; average global sea freight rates fell ~35% from 2022 peaks to about 1,200 USD/FEU in 2024, easing pressure but not eliminating costs.

By 2025 volatility has stabilized, yet route shifts (nearshoring, Arctic lane interest) add structural transit-time and capacity risks that can raise unit costs 3–7% versus pre-2020 norms.

Efficient logistics—warehousing, modal mix, demand forecasting—remains crucial for Clarus to preserve gross margins and sustain competitive retail pricing; improving logistics could trim COGS by 1–2%.

- 2024 avg sea freight ~1,200 USD/FEU

- Route-induced cost premium 3–7%

- Potential COGS reduction via logistics 1–2%

Macro squeeze: falling incomes, higher CPI & costs; $18M FX hit, rates up, inflationary inputs

Disposable income decline (OECD H2 2025 -0.8%), global CPI 2025 4.1%, US retail sporting goods -1.2% YTD 2025; FX headwind ~5% vs EUR/AUD (~$18m revenue impact FY2024), USD rates 5.25–5.50% raise borrowing costs +200–300bps; LME Al +12% (2024), US HRC ~$780/ton (2024); sea freight ~$1,200/FEU (2024).

| Metric | Value |

|---|---|

| OECD disposable income | -0.8% H2 2025 |

| Global CPI 2025 | 4.1% |

| FX headwind | ~5% (~$18m) |

What You See Is What You Get

Clarus PESTLE Analysis

The preview shown here is the exact Clarus PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible in the preview are the final product with no placeholders or teasers. After checkout you’ll instantly download this exact file, professionally structured for immediate application. What you see is what you’ll own and work with.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and technological advances are shaping Clarus’s strategic outlook with our concise PESTLE snapshot—crafted for investors and strategists who need actionable insight fast; buy the full analysis to access the complete, editable report and make smarter, faster decisions.

Political factors

Global Trade Policy and Tariffs

As of late 2025, shifting trade alliances and rising protectionist measures have increased supply-chain volatility for Clarus brands like Black Diamond, with Asian-origin raw material import duties rising by an average of 6.2% year-over-year and freight costs up 18% since 2023.

Changes in tariffs on finished goods entering North America have squeezed manufacturing margins, contributing to a reported 120–180 basis point decline in gross margin for comparable outdoor-equipment peers in 2024–25.

Management must navigate these geopolitical tensions, reoptimizing supplier footprints and passing limited cost increases to customers while targeting a 3–5% price-competitiveness buffer to protect market share.

Geopolitical Stability in Manufacturing Hubs

Government Outdoor Recreation Initiatives

Export Control and Defense Regulations

Certain Sierra-brand precision optics and match-grade components may fall under US export controls (ITAR/EAR); in 2024 the Commerce Dept. added multiple optics categories to stricter controls, raising compliance costs by an estimated 5–8% for affected manufacturers.

Maintaining alignment with evolving federal and allied-country mandates on sale and shipment is essential to avoid fines—recent penalties in 2023–24 exceeded $100m industry-wide—so Clarus must invest in licensing and supply-chain screening.

Political shifts on firearm accessories require a proactive regulatory strategy; tracking 50+ pending state/federal bills and updating export-classification procedures reduces operational disruption and market-access risks.

- ITAR/EAR exposure for precision optics; 5–8% added compliance cost

- Industry fines >$100m in 2023–24 signal enforcement risk

- Monitor 50+ pending firearm-related bills; update licensing and screening

Labor Laws and Minimum Wage Shifts

Political movements pushing minimum wages up to $15–$20/hour in several US states raise Clarus’s domestic labor costs; a 10–15% wage uplift could increase assembly/distribution OPEX materially versus 2024 payrolls of $120M.

Changes in labor relations laws reducing flexible scheduling can hurt peak-season capacity, potentially increasing temporary staffing costs by 8–12% during Q4 demand spikes.

Clarus must weigh social responsibility against rising mandated labor expenses under new administrations, which could compress gross margins by 50–150 bps if costs are passed through.

- Higher minimum wages: $15–$20/hr; 10–15% payroll impact

- Scheduling restrictions: +8–12% peak temporary costs

- Margin pressure: 50–150 basis points potential compression

Supply shocks, tariffs and compliance squeeze margins as federal funding boosts market

Geopolitical trade barriers and tariffs raised input costs ~6–18% (2023–25), cutting peers’ gross margins 120–180 bps; 27% of BOM sourced from Vietnam/Mexico exposes Clarus to 8.5% 2024 supply shortfall and 6–12 week supplier-switch timelines; ITAR/EAR optics controls add 5–8% compliance costs; federal outdoor funding ($1.5B+/yr) and $400M trail grants (2024) expand addressable market.

| Metric | Value |

|---|---|

| Tariff/freight rise | 6–18% |

| Peers’ margin hit | 120–180 bps |

| BOM from VN/MX | 27% |

| Supply drop (2024) | 8.5% |

| ITAR/EAR cost | 5–8% |

| Federal outdoor funding | $1.5B+/yr |

| Trail grants (2024) | $400M |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Clarus across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Provides a clean, summarized PESTLE snapshot that’s visually segmented for quick interpretation and easily dropped into presentations or shared for rapid team alignment.

Economic factors

Consumer Discretionary Spending Trends

Demand for premium outdoor gear is highly tied to disposable income; OECD data showed household real disposable income in major markets fell 0.8% y/y in H2 2025, increasing price sensitivity for high-ticket items like Rhino-Rack and pro skiing equipment.

Inflationary pressures (global CPI averaging 4.1% in 2025) and a 1.2% slowdown in US retail spending on sporting goods through Q3 2025 led many consumers to defer purchases.

Clarus monitors unemployment, consumer confidence (GfK indices down 6 points in 2025) and retail sales monthly to adjust production volumes and inventory, reducing output by targeted percentages during demand soft patches.

Fluctuations in Foreign Exchange Rates

As a global entity, Clarus faces currency volatility that impacted FY2024 reported revenue, with a 5% headwind from USD strength versus EUR and AUD, reducing translated sales by about $18m; a stronger dollar can make products ~10–15% costlier for European and Australian buyers, pressuring demand. Clarus uses FX hedges—forward contracts and options—covering roughly 60% of projected FX exposure to limit P&L volatility.

Interest Rate Environment and Capital Cost

As of end-2025, the US Federal Funds rate near 5.25%–5.50% raised Clarus’s weighted average cost of debt, pushing borrowing costs for acquisitions and R&D to roughly 200–300 basis points above pre-2022 levels and increasing annual interest expense by an estimated $8–12m on $400m of new debt.

Raw Material and Commodity Pricing

Raw material costs for Clarus brands Black Diamond and Rhino-Rack—notably aluminum, steel and specialty polymers—track volatile commodity cycles; LME aluminum rose ~12% in 2024 while US steel HRC averaged $780/ton in 2024, pressuring margins when costs can't be passed to customers.

Energy-driven input inflation and freight spikes in 2022–24 tightened gross margins; long-term sourcing and hedges plus supply-chain efficiency are critical to stabilise input cost exposure.

- 2024 LME aluminum +12% year; US HRC ~$780/ton 2024

- Energy/freight inflation 2022–24 amplified input costs

- Long-term contracts, hedging, logistics efficiency mitigate margin risk

Global Logistics and Freight Costs

Global logistics costs, driven by fuel surcharges and container availability, directly raise Clarus’s landed cost; average global sea freight rates fell ~35% from 2022 peaks to about 1,200 USD/FEU in 2024, easing pressure but not eliminating costs.

By 2025 volatility has stabilized, yet route shifts (nearshoring, Arctic lane interest) add structural transit-time and capacity risks that can raise unit costs 3–7% versus pre-2020 norms.

Efficient logistics—warehousing, modal mix, demand forecasting—remains crucial for Clarus to preserve gross margins and sustain competitive retail pricing; improving logistics could trim COGS by 1–2%.

- 2024 avg sea freight ~1,200 USD/FEU

- Route-induced cost premium 3–7%

- Potential COGS reduction via logistics 1–2%

Macro squeeze: falling incomes, higher CPI & costs; $18M FX hit, rates up, inflationary inputs

Disposable income decline (OECD H2 2025 -0.8%), global CPI 2025 4.1%, US retail sporting goods -1.2% YTD 2025; FX headwind ~5% vs EUR/AUD (~$18m revenue impact FY2024), USD rates 5.25–5.50% raise borrowing costs +200–300bps; LME Al +12% (2024), US HRC ~$780/ton (2024); sea freight ~$1,200/FEU (2024).

| Metric | Value |

|---|---|

| OECD disposable income | -0.8% H2 2025 |

| Global CPI 2025 | 4.1% |

| FX headwind | ~5% (~$18m) |

What You See Is What You Get

Clarus PESTLE Analysis

The preview shown here is the exact Clarus PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible in the preview are the final product with no placeholders or teasers. After checkout you’ll instantly download this exact file, professionally structured for immediate application. What you see is what you’ll own and work with.