Clasquin Porter's Five Forces Analysis

Don't Miss the Bigger Picture

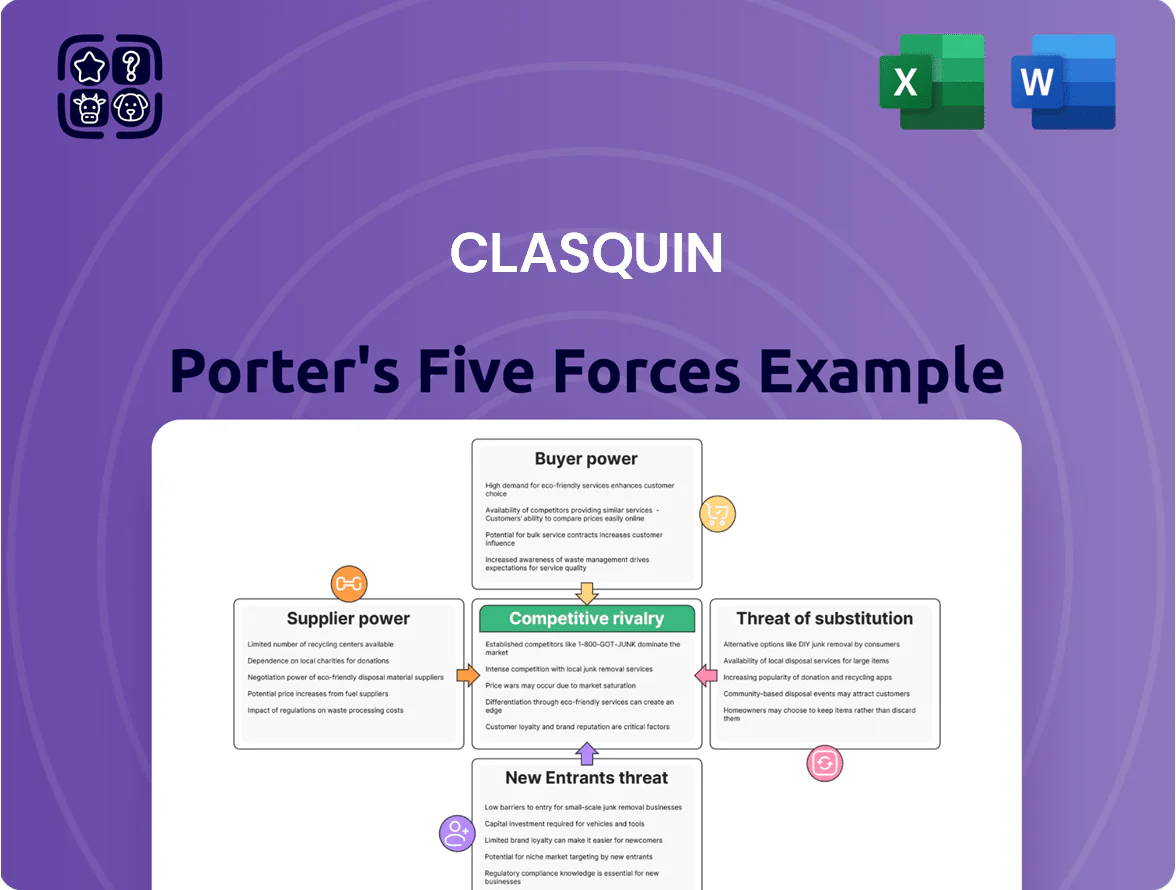

Clasquin faces mixed pressures: buyer demand for logistics flexibility raises negotiation power while specialized freight services and regulatory hurdles limit entrant threats; suppliers wield moderate influence, and substitutes like digital platforms pose growing risk to margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clasquin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Ocean Carrier Consolidation

The global containership sector is concentrated: three alliances and top 10 carriers controlled about 80% of capacity by TEU in 2024, letting carriers set freight rates and sailings during equipment shortages; record 2023 peak rate spikes saw Asia-Europe box rates jump over 300% year-on-year at times. For mid-sized forwarder Clasquin, this concentration cuts bargaining power versus the largest shippers, limiting long-term contract leverage and exposing margins to spot volatility.

Limited Air Cargo Capacity

Air freight suppliers—commercial airlines and cargo specialists—hold strong bargaining power because aircraft and belly-capacity are specialized assets; IATA reported global belly capacity at 78% of 2019 levels in 2024, keeping slots scarce on Asia–Europe/North America lanes. Peak-season yield surges reached 40–120% in 2021–23 on key routes, letting suppliers add surcharges and tight booking windows Clasquin must absorb or pass to clients.

Impact of MSC Ownership

After MSC Group’s 2023 acquisition of Clasquin via Shipping Agencies Services, supplier power shifted: Clasquin gains stable access to MSC’s 780+ vessels and ~23% share of global container capacity (2024), lowering price volatility from its parent, but rival carriers like Maersk and CMA CGM may curtail cooperation, raising external supplier leverage and spot-rate variability by an estimated 5–8% on routes where those lines dominate.

Labor and Port Authority Influence

Suppliers of infrastructure services like port authorities and terminal operators wield strong bargaining power by controlling essential gateways; in 2025 global container throughput at top 20 ports rose 3.1%, concentrating leverage and fee-setting power.

Labor unions at major ports caused notable disruptions in 2025—strikes in regions handling ~12% of global TEU capacity led to average berth delays of 36–48 hours, forcing forwarders to reroute or pay premiums.

These services are non-substitutable, so forwarders face fee hikes—terminal handling charges rose an average 6.4% in 2025—and operational delays with limited mitigation options.

Technological Platform Providers

- High switching costs from deep TMS integration

- TMS market $3.2bn in 2024, +9% YoY

- SaaS/integration ~6–10% of logistics OPEX

- Vendors hold steady pricing and renewal leverage

Shipping suppliers dominate: 80% TEU, MSC 23%, rising port charges & costly air capacity

Suppliers hold high bargaining power: top 10 carriers ~80% TEU (2024), MSC ~23% share (2024) improving Clasquin access but rivals keep leverage; air belly capacity 78% of 2019 (IATA 2024) keeping yields high; top-20 ports throughput +3.1% (2025) and terminal charges +6.4% (2025); TMS market $3.2bn (2024) with SaaS 6–10% logistics OPEX.

| Metric | Value |

|---|---|

| Top-10 carriers TEU share (2024) | ~80% |

| MSC global capacity (2024) | ~23% |

| Air belly capacity (IATA 2024) | 78% of 2019 |

| Top-20 ports throughput (2025) | +3.1% |

| Terminal charges (2025) | +6.4% |

| TMS market (2024) | $3.2bn |

What is included in the product

Tailored Porter's Five Forces for Clasquin: uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats with industry data and strategic commentary for investor and strategy use.

Quick, one-sheet Porter's Five Forces tailored to Clasquin—visualize supplier, buyer, entrant, substitute, and rivalry pressures at a glance to speed strategic decisions and highlight immediate relief points.

Customers Bargaining Power

Low Switching Costs for Shippers

Customers in freight forwarding face low switching costs, with industry surveys showing 62% of shippers used three or more forwarders in 2024 to secure rates and capacity; deep IT/warehouse integration can lock 18% of contracts into longer terms, but most accounts stay fluid. This bargaining power forces Clasquin to keep service levels high and pricing competitive—Clasquin reported 2024 revenue growth of 9% while trimming spot-rate losses to 1.6% of gross margin to limit churn.

High Demand for Digital Transparency

By end-2025, 78% of logistics buyers expect real-time tracking and analytics as standard; Clasquin faces buyers demanding free custom dashboards and integrated reports, especially large clients who control >40% of contract volume.

That demand shifts bargaining power to customers: tech is now entry-level, not a premium, squeezing margins as Clasquin must absorb digital costs to retain high-volume accounts.

Price Sensitivity in Commodity Markets

For standard shipments without special handling, 78% of shippers cite price as the top decision factor, so Clasquin faces strong price sensitivity on basic lanes.

Digital platforms let shippers compare rates from 30–50 forwarders in seconds, increasing transparency and driving commoditization of core freight services.

As a result, Clasquin’s margin compression is acute on high-volume, low-complexity lanes—industry data shows average gross margins drop to 6–8% versus 15–18% on specialized services.

Concentration of Large Account Volume

A significant share of Clasquin revenue—about 35% in 2024—came from roughly 10 global accounts, giving those shippers strong leverage to demand lower rates and 60–90 day payment terms that strain Clasquin’s working capital.

To reduce that bargaining power, Clasquin is diversifying into niches—luxury goods and perishables—where specialization lets it charge 8–12% premium margins versus commodity lanes.

Sophistication of Procurement Departments

Modern procurement teams use TMS and spend-analytics tools to cut freight costs; 62% of European shippers reported using analytics in 2024, so Clasquin faces buyers who can benchmark rates to the euro.

Buyers track fuel surcharges, capacity and lead times, shrinking forwarder margin opacity; spot rates and surcharges are compared daily, forcing Clasquin to justify every fee.

This financial literacy means Clasquin must link costs to services—e.g., real-time visibility, PO finance, or network density—to retain contracts and price above pure commodity levels.

- 62% of EU shippers used analytics in 2024

- Buyers compare fuel and spot rates daily

- Clasquin must justify each cost via services

Concentrated buyers, thin margins & stretched working capital as real-time demand rises

Customers hold high bargaining power: 35% of Clasquin revenue came from 10 global accounts in 2024, 62% of EU shippers used analytics, and 78% expect real-time tracking by 2025—driving price sensitivity (standard-lane margins 6–8% vs 15–18% specialized) and requests for 60–90 day terms that stress working capital.

| Metric | Value |

|---|---|

| Top-10 revenue share (2024) | 35% |

| EU shippers using analytics (2024) | 62% |

| Buyers expecting real-time (by 2025) | 78% |

| Standard-lane gross margin | 6–8% |

| Specialized gross margin | 15–18% |

| Payment terms pushed by clients | 60–90 days |

Preview Before You Purchase

Clasquin Porter's Five Forces Analysis

This preview shows the exact Clasquin Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the full, professionally written file; once you complete your purchase you’ll get instant access to this same deliverable for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Clasquin faces mixed pressures: buyer demand for logistics flexibility raises negotiation power while specialized freight services and regulatory hurdles limit entrant threats; suppliers wield moderate influence, and substitutes like digital platforms pose growing risk to margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clasquin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Ocean Carrier Consolidation

The global containership sector is concentrated: three alliances and top 10 carriers controlled about 80% of capacity by TEU in 2024, letting carriers set freight rates and sailings during equipment shortages; record 2023 peak rate spikes saw Asia-Europe box rates jump over 300% year-on-year at times. For mid-sized forwarder Clasquin, this concentration cuts bargaining power versus the largest shippers, limiting long-term contract leverage and exposing margins to spot volatility.

Limited Air Cargo Capacity

Air freight suppliers—commercial airlines and cargo specialists—hold strong bargaining power because aircraft and belly-capacity are specialized assets; IATA reported global belly capacity at 78% of 2019 levels in 2024, keeping slots scarce on Asia–Europe/North America lanes. Peak-season yield surges reached 40–120% in 2021–23 on key routes, letting suppliers add surcharges and tight booking windows Clasquin must absorb or pass to clients.

Impact of MSC Ownership

After MSC Group’s 2023 acquisition of Clasquin via Shipping Agencies Services, supplier power shifted: Clasquin gains stable access to MSC’s 780+ vessels and ~23% share of global container capacity (2024), lowering price volatility from its parent, but rival carriers like Maersk and CMA CGM may curtail cooperation, raising external supplier leverage and spot-rate variability by an estimated 5–8% on routes where those lines dominate.

Labor and Port Authority Influence

Suppliers of infrastructure services like port authorities and terminal operators wield strong bargaining power by controlling essential gateways; in 2025 global container throughput at top 20 ports rose 3.1%, concentrating leverage and fee-setting power.

Labor unions at major ports caused notable disruptions in 2025—strikes in regions handling ~12% of global TEU capacity led to average berth delays of 36–48 hours, forcing forwarders to reroute or pay premiums.

These services are non-substitutable, so forwarders face fee hikes—terminal handling charges rose an average 6.4% in 2025—and operational delays with limited mitigation options.

Technological Platform Providers

- High switching costs from deep TMS integration

- TMS market $3.2bn in 2024, +9% YoY

- SaaS/integration ~6–10% of logistics OPEX

- Vendors hold steady pricing and renewal leverage

Shipping suppliers dominate: 80% TEU, MSC 23%, rising port charges & costly air capacity

Suppliers hold high bargaining power: top 10 carriers ~80% TEU (2024), MSC ~23% share (2024) improving Clasquin access but rivals keep leverage; air belly capacity 78% of 2019 (IATA 2024) keeping yields high; top-20 ports throughput +3.1% (2025) and terminal charges +6.4% (2025); TMS market $3.2bn (2024) with SaaS 6–10% logistics OPEX.

| Metric | Value |

|---|---|

| Top-10 carriers TEU share (2024) | ~80% |

| MSC global capacity (2024) | ~23% |

| Air belly capacity (IATA 2024) | 78% of 2019 |

| Top-20 ports throughput (2025) | +3.1% |

| Terminal charges (2025) | +6.4% |

| TMS market (2024) | $3.2bn |

What is included in the product

Tailored Porter's Five Forces for Clasquin: uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats with industry data and strategic commentary for investor and strategy use.

Quick, one-sheet Porter's Five Forces tailored to Clasquin—visualize supplier, buyer, entrant, substitute, and rivalry pressures at a glance to speed strategic decisions and highlight immediate relief points.

Customers Bargaining Power

Low Switching Costs for Shippers

Customers in freight forwarding face low switching costs, with industry surveys showing 62% of shippers used three or more forwarders in 2024 to secure rates and capacity; deep IT/warehouse integration can lock 18% of contracts into longer terms, but most accounts stay fluid. This bargaining power forces Clasquin to keep service levels high and pricing competitive—Clasquin reported 2024 revenue growth of 9% while trimming spot-rate losses to 1.6% of gross margin to limit churn.

High Demand for Digital Transparency

By end-2025, 78% of logistics buyers expect real-time tracking and analytics as standard; Clasquin faces buyers demanding free custom dashboards and integrated reports, especially large clients who control >40% of contract volume.

That demand shifts bargaining power to customers: tech is now entry-level, not a premium, squeezing margins as Clasquin must absorb digital costs to retain high-volume accounts.

Price Sensitivity in Commodity Markets

For standard shipments without special handling, 78% of shippers cite price as the top decision factor, so Clasquin faces strong price sensitivity on basic lanes.

Digital platforms let shippers compare rates from 30–50 forwarders in seconds, increasing transparency and driving commoditization of core freight services.

As a result, Clasquin’s margin compression is acute on high-volume, low-complexity lanes—industry data shows average gross margins drop to 6–8% versus 15–18% on specialized services.

Concentration of Large Account Volume

A significant share of Clasquin revenue—about 35% in 2024—came from roughly 10 global accounts, giving those shippers strong leverage to demand lower rates and 60–90 day payment terms that strain Clasquin’s working capital.

To reduce that bargaining power, Clasquin is diversifying into niches—luxury goods and perishables—where specialization lets it charge 8–12% premium margins versus commodity lanes.

Sophistication of Procurement Departments

Modern procurement teams use TMS and spend-analytics tools to cut freight costs; 62% of European shippers reported using analytics in 2024, so Clasquin faces buyers who can benchmark rates to the euro.

Buyers track fuel surcharges, capacity and lead times, shrinking forwarder margin opacity; spot rates and surcharges are compared daily, forcing Clasquin to justify every fee.

This financial literacy means Clasquin must link costs to services—e.g., real-time visibility, PO finance, or network density—to retain contracts and price above pure commodity levels.

- 62% of EU shippers used analytics in 2024

- Buyers compare fuel and spot rates daily

- Clasquin must justify each cost via services

Concentrated buyers, thin margins & stretched working capital as real-time demand rises

Customers hold high bargaining power: 35% of Clasquin revenue came from 10 global accounts in 2024, 62% of EU shippers used analytics, and 78% expect real-time tracking by 2025—driving price sensitivity (standard-lane margins 6–8% vs 15–18% specialized) and requests for 60–90 day terms that stress working capital.

| Metric | Value |

|---|---|

| Top-10 revenue share (2024) | 35% |

| EU shippers using analytics (2024) | 62% |

| Buyers expecting real-time (by 2025) | 78% |

| Standard-lane gross margin | 6–8% |

| Specialized gross margin | 15–18% |

| Payment terms pushed by clients | 60–90 days |

Preview Before You Purchase

Clasquin Porter's Five Forces Analysis

This preview shows the exact Clasquin Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the full, professionally written file; once you complete your purchase you’ll get instant access to this same deliverable for download and application.