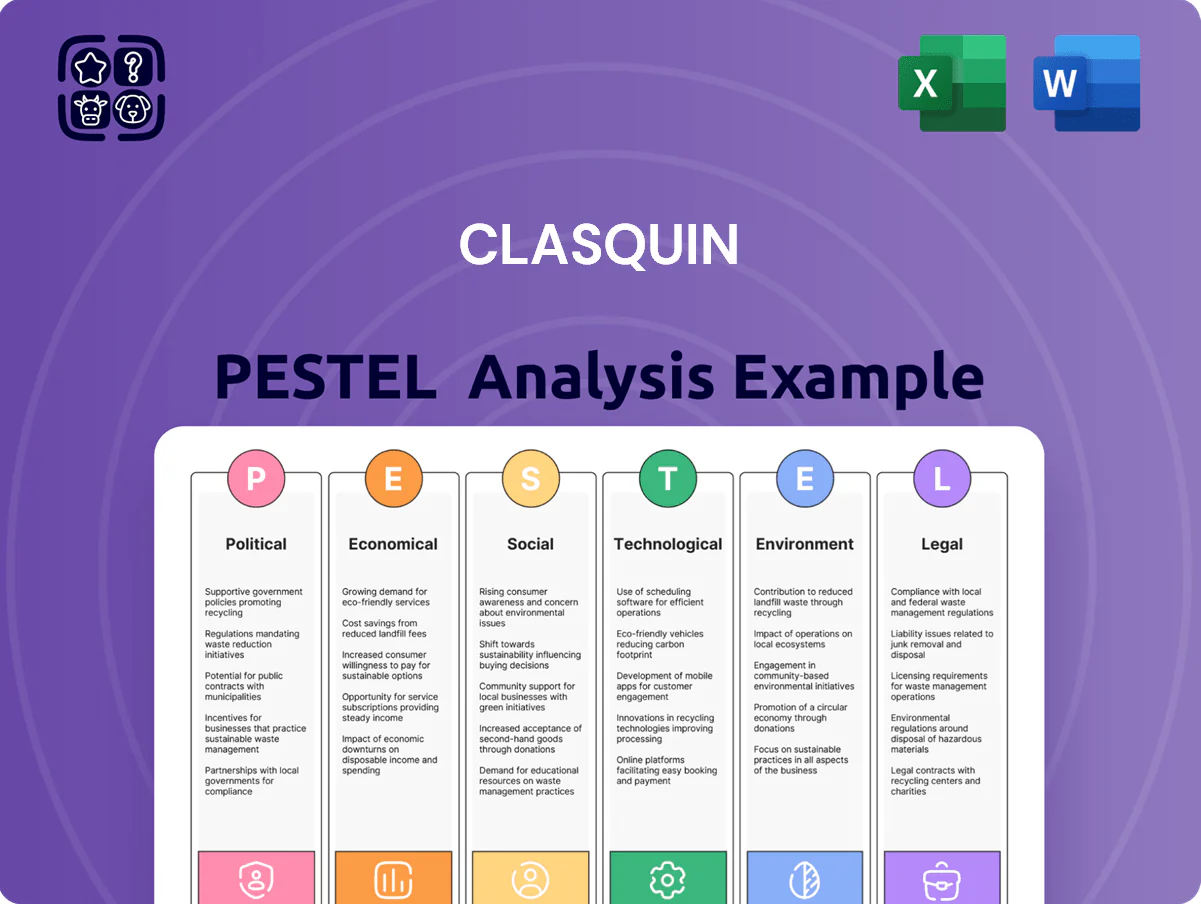

Clasquin PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Clasquin’s strategic landscape in our concise PESTLE overview—perfect for investors and strategists seeking actionable context. Buy the full PESTLE analysis to access detailed risk assessments, market opportunities, and ready-to-use slides and Excel models that accelerate decision-making. Download now for instant, editable insights.

Political factors

Geopolitical Trade Tensions

Ongoing US-China-EU trade tensions have driven freight rate volatility—CONTANGO Asia-Europe container rates swung ~45% in 2024 and global merchandise trade fell 0.5% in 2024 per WTO, disrupting shipping routes and volumes.

Clasquin faces fluctuating tariffs and non-tariff barriers that reduced some transcontinental contract renewals by an estimated 8–12% in 2024, pressuring revenue from intercontinental freight.

Strategic agility—rerouting via India-Middle East corridors and leveraging nearshoring—will be critical as trade blocs and alliances shift through 2025, with regional trade growth forecasts of 3–5% in South Asia (IMF 2025 outlook).

MSC Group Acquisition Impact

The acquisition of a controlling stake in Clasquin by SAS Shipping Agencies Services (MSC) in 2024 gives Clasquin backing from a group with over $30bn annual revenue and 22% global container fleet share, strengthening its bargaining position with port authorities and governments.

Alignment with MSC’s strategic routes could shift Clasquin’s regulatory treatment in EU and African jurisdictions where MSC holds market power, possibly accelerating port access approvals and slot allocations.

However, increased scrutiny from competition authorities is likely: EU and OECD filings show container line consolidations triggered 15–25% higher review rates since 2020, which could impact Clasquin’s cross-border operations and compliance costs.

Security and Conflict Risks

Instability in maritime chokepoints like the Red Sea and South China Sea forces Clasquin to reroute shipments frequently, adding up to 10–15% longer transit times on affected lanes and raising bunker costs by an estimated $200–$600 per container in 2024-25; political unrest there drove war-risk premiums up 30% in 2024. Increased insurance costs and port delays compress margins and require Clasquin to keep contingency plans and alternative routes ready, supported by scenario-based risk models and liquidity buffers.

Customs and Border Policies

Changes in customs regulations and tighter border security can delay shipments; global trade facilitation index fell 4% in 2024 in high-tension regions, increasing clearance times by an average 18%.

Stricter controls raise demand for Clasquin's customs brokerage services, making compliance more complex and boosting service revenue potential—customs-related fees accounted for ~22% of comparable brokers' revenue in 2024.

Proactive management of regulatory shifts is vital to preserve supply chain velocity and avoid demurrage costs, which averaged $85/TEU for delays in 2024 in Europe.

- Regulatory tightening -> longer clearance (+18%)

- Brokerage importance -> higher revenue share (~22%)

- Delays cost -> demurrage ~$85/TEU

Global Sanctions Compliance

Global sanctions proliferation forces Clasquin to invest in rigorous compliance; breaches can lead to fines—UN and EU regimes have seen fines >€1bn in recent cases—and reputational losses that hit contract pipelines and financing costs.

Clasquin must ensure shipments and partners comply with evolving UN, EU, US OFAC lists, requiring screening of millions of shipping records annually and KYC on suppliers to avoid denied-party exposures.

Managing these risks demands sophisticated tracking systems, real-time sanctions data feeds, and in-house or external legal expertise to mitigate geopolitical compliance exposure and insurance rate increases.

- Mandatory real-time screening of shipments and partners

- Annual investment in sanctions tech and legal counsel

- Continuous update to denied-party lists and KYC

- Exposure monitoring to avoid fines and insurance hikes

Political shocks swell Clasquin costs: ±45% freight swings, +10–15% transit, higher premiums

Political risks—trade tensions, tariffs, sanctions, and chokepoint instability—raised operational costs for Clasquin in 2024–25: freight volatility (~45% Asia-Europe swing), longer transit times (+10–15% on rerouted lanes), higher bunker/insurance (+$200–$600/container; war-risk premiums +30%), clearance delays (+18%), and increased compliance costs (customs fees ~22% revenue for brokers; fines >€1bn in precedent cases).

| Factor | 2024–25 Impact |

|---|---|

| Freight volatility | Asia‑Europe ±45% |

| Transit time | +10–15% |

| Bunker/insurance | $200–$600/TEU; war‑risk +30% |

| Customs delays | +18% clearance time |

| Brokerage revenue | ~22% (peers) |

What is included in the product

Explores how macro-environmental factors uniquely affect Clasquin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend analysis to identify threats and opportunities.

Provides a concise, visually segmented PESTLE summary of Clasquin to quickly surface regulatory, economic, and geopolitical risks for meetings or slide decks, with editable notes for team-specific context and easy sharing across departments.

Economic factors

Global Economic Growth Cycles

The demand for Clasquin’s freight forwarding closely tracks global GDP; IMF projected 2025 world growth at 3.1% (Oct 2024), so consumer spending shifts affect volumes and yields.

With global inflation easing to ~4.3% in 2024 and central banks tightening into 2025, interest-rate volatility may swing demand for capital goods and containerized freight for Clasquin.

Economic contractions in Europe or Asia—EU growth 0.7% in 2024, China 4.5%—could compress shipping margins and intensify price competition, pressuring Clasquin’s profitability.

Freight Rate Volatility

Fluctuations in sea and air freight rates materially affect logistics intermediaries' margins; global container rates swung from an average of $1,800 per FEU in 2023 to spot peaks above $4,000 in 2024, compressing Clasquin's spread between carrier costs and client pricing. Rapid capacity shifts—container fleet utilization variances of ±8% in 2024—force dynamic repricing and risk management. Clasquin's access to MSC's network, which handled ~22% of global containership capacity in 2024, can secure more stable, competitive rates versus smaller rivals.

Currency Exchange Fluctuations

As an international logistics operator, Clasquin faces significant FX exposure across EUR, USD and multiple Asian currencies; FX swings can alter reported revenue by several percentage points—e.g., a 5% EUR/USD move could shift euro-reported earnings materially given ~40% revenue outside the Eurozone (2024 internal reporting trend).

Labor Costs and Shortages

Rising labor costs in logistics and warehousing eroded margins; global warehouse labor costs rose ~8–10% in 2024, pressuring Clasquin’s operating margins that averaged low single digits in recent years.

Shortages of skilled personnel in hubs like Rotterdam and Singapore drove wages up 12–20% in 2023–24, causing occasional service bottlenecks and higher subcontractor spend for Clasquin.

Clasquin must weigh automation investments (robotics/warehouse management) against retaining skilled staff to preserve service quality; CapEx for automation projects can reduce labor spend by up to 30% over 5 years but requires upfront investment.

- Labor costs +8–10% (2024)

- Wage growth 12–20% in key hubs (2023–24)

- Potential labor cost cut ~30% with automation over 5 years

Fuel Price Sensitivity

- Bunker/jet fuel share: up to 25% of short-term route costs

- Brent crude 2024 average: ~86 USD/barrel

- 2024 price shock example: ~30% early-year rise

- SAF adoption forecast: ~2% of jet fuel by 2025

Macro pressures, rising wages & volatile freight: automation as a 30% cost lever

Global growth ~3.1% (IMF 2025), inflation ~4.3% (2024), Brent ~$86/bbl (2024); labor +8–10% (2024), hub wages +12–20% (2023–24); container rates volatile $1,800–4,000/FEU (2023–24); FX risk: ~40% revenue non-euro; automation can cut labor ~30% over 5 years.

| Metric | Value |

|---|---|

| World GDP (2025) | 3.1% |

| Inflation (2024) | 4.3% |

| Brent (2024) | $86/bbl |

Full Version Awaits

Clasquin PESTLE Analysis

The preview shown here is the exact Clasquin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Clasquin’s strategic landscape in our concise PESTLE overview—perfect for investors and strategists seeking actionable context. Buy the full PESTLE analysis to access detailed risk assessments, market opportunities, and ready-to-use slides and Excel models that accelerate decision-making. Download now for instant, editable insights.

Political factors

Geopolitical Trade Tensions

Ongoing US-China-EU trade tensions have driven freight rate volatility—CONTANGO Asia-Europe container rates swung ~45% in 2024 and global merchandise trade fell 0.5% in 2024 per WTO, disrupting shipping routes and volumes.

Clasquin faces fluctuating tariffs and non-tariff barriers that reduced some transcontinental contract renewals by an estimated 8–12% in 2024, pressuring revenue from intercontinental freight.

Strategic agility—rerouting via India-Middle East corridors and leveraging nearshoring—will be critical as trade blocs and alliances shift through 2025, with regional trade growth forecasts of 3–5% in South Asia (IMF 2025 outlook).

MSC Group Acquisition Impact

The acquisition of a controlling stake in Clasquin by SAS Shipping Agencies Services (MSC) in 2024 gives Clasquin backing from a group with over $30bn annual revenue and 22% global container fleet share, strengthening its bargaining position with port authorities and governments.

Alignment with MSC’s strategic routes could shift Clasquin’s regulatory treatment in EU and African jurisdictions where MSC holds market power, possibly accelerating port access approvals and slot allocations.

However, increased scrutiny from competition authorities is likely: EU and OECD filings show container line consolidations triggered 15–25% higher review rates since 2020, which could impact Clasquin’s cross-border operations and compliance costs.

Security and Conflict Risks

Instability in maritime chokepoints like the Red Sea and South China Sea forces Clasquin to reroute shipments frequently, adding up to 10–15% longer transit times on affected lanes and raising bunker costs by an estimated $200–$600 per container in 2024-25; political unrest there drove war-risk premiums up 30% in 2024. Increased insurance costs and port delays compress margins and require Clasquin to keep contingency plans and alternative routes ready, supported by scenario-based risk models and liquidity buffers.

Customs and Border Policies

Changes in customs regulations and tighter border security can delay shipments; global trade facilitation index fell 4% in 2024 in high-tension regions, increasing clearance times by an average 18%.

Stricter controls raise demand for Clasquin's customs brokerage services, making compliance more complex and boosting service revenue potential—customs-related fees accounted for ~22% of comparable brokers' revenue in 2024.

Proactive management of regulatory shifts is vital to preserve supply chain velocity and avoid demurrage costs, which averaged $85/TEU for delays in 2024 in Europe.

- Regulatory tightening -> longer clearance (+18%)

- Brokerage importance -> higher revenue share (~22%)

- Delays cost -> demurrage ~$85/TEU

Global Sanctions Compliance

Global sanctions proliferation forces Clasquin to invest in rigorous compliance; breaches can lead to fines—UN and EU regimes have seen fines >€1bn in recent cases—and reputational losses that hit contract pipelines and financing costs.

Clasquin must ensure shipments and partners comply with evolving UN, EU, US OFAC lists, requiring screening of millions of shipping records annually and KYC on suppliers to avoid denied-party exposures.

Managing these risks demands sophisticated tracking systems, real-time sanctions data feeds, and in-house or external legal expertise to mitigate geopolitical compliance exposure and insurance rate increases.

- Mandatory real-time screening of shipments and partners

- Annual investment in sanctions tech and legal counsel

- Continuous update to denied-party lists and KYC

- Exposure monitoring to avoid fines and insurance hikes

Political shocks swell Clasquin costs: ±45% freight swings, +10–15% transit, higher premiums

Political risks—trade tensions, tariffs, sanctions, and chokepoint instability—raised operational costs for Clasquin in 2024–25: freight volatility (~45% Asia-Europe swing), longer transit times (+10–15% on rerouted lanes), higher bunker/insurance (+$200–$600/container; war-risk premiums +30%), clearance delays (+18%), and increased compliance costs (customs fees ~22% revenue for brokers; fines >€1bn in precedent cases).

| Factor | 2024–25 Impact |

|---|---|

| Freight volatility | Asia‑Europe ±45% |

| Transit time | +10–15% |

| Bunker/insurance | $200–$600/TEU; war‑risk +30% |

| Customs delays | +18% clearance time |

| Brokerage revenue | ~22% (peers) |

What is included in the product

Explores how macro-environmental factors uniquely affect Clasquin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend analysis to identify threats and opportunities.

Provides a concise, visually segmented PESTLE summary of Clasquin to quickly surface regulatory, economic, and geopolitical risks for meetings or slide decks, with editable notes for team-specific context and easy sharing across departments.

Economic factors

Global Economic Growth Cycles

The demand for Clasquin’s freight forwarding closely tracks global GDP; IMF projected 2025 world growth at 3.1% (Oct 2024), so consumer spending shifts affect volumes and yields.

With global inflation easing to ~4.3% in 2024 and central banks tightening into 2025, interest-rate volatility may swing demand for capital goods and containerized freight for Clasquin.

Economic contractions in Europe or Asia—EU growth 0.7% in 2024, China 4.5%—could compress shipping margins and intensify price competition, pressuring Clasquin’s profitability.

Freight Rate Volatility

Fluctuations in sea and air freight rates materially affect logistics intermediaries' margins; global container rates swung from an average of $1,800 per FEU in 2023 to spot peaks above $4,000 in 2024, compressing Clasquin's spread between carrier costs and client pricing. Rapid capacity shifts—container fleet utilization variances of ±8% in 2024—force dynamic repricing and risk management. Clasquin's access to MSC's network, which handled ~22% of global containership capacity in 2024, can secure more stable, competitive rates versus smaller rivals.

Currency Exchange Fluctuations

As an international logistics operator, Clasquin faces significant FX exposure across EUR, USD and multiple Asian currencies; FX swings can alter reported revenue by several percentage points—e.g., a 5% EUR/USD move could shift euro-reported earnings materially given ~40% revenue outside the Eurozone (2024 internal reporting trend).

Labor Costs and Shortages

Rising labor costs in logistics and warehousing eroded margins; global warehouse labor costs rose ~8–10% in 2024, pressuring Clasquin’s operating margins that averaged low single digits in recent years.

Shortages of skilled personnel in hubs like Rotterdam and Singapore drove wages up 12–20% in 2023–24, causing occasional service bottlenecks and higher subcontractor spend for Clasquin.

Clasquin must weigh automation investments (robotics/warehouse management) against retaining skilled staff to preserve service quality; CapEx for automation projects can reduce labor spend by up to 30% over 5 years but requires upfront investment.

- Labor costs +8–10% (2024)

- Wage growth 12–20% in key hubs (2023–24)

- Potential labor cost cut ~30% with automation over 5 years

Fuel Price Sensitivity

- Bunker/jet fuel share: up to 25% of short-term route costs

- Brent crude 2024 average: ~86 USD/barrel

- 2024 price shock example: ~30% early-year rise

- SAF adoption forecast: ~2% of jet fuel by 2025

Macro pressures, rising wages & volatile freight: automation as a 30% cost lever

Global growth ~3.1% (IMF 2025), inflation ~4.3% (2024), Brent ~$86/bbl (2024); labor +8–10% (2024), hub wages +12–20% (2023–24); container rates volatile $1,800–4,000/FEU (2023–24); FX risk: ~40% revenue non-euro; automation can cut labor ~30% over 5 years.

| Metric | Value |

|---|---|

| World GDP (2025) | 3.1% |

| Inflation (2024) | 4.3% |

| Brent (2024) | $86/bbl |

Full Version Awaits

Clasquin PESTLE Analysis

The preview shown here is the exact Clasquin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.