Classic Hospitals PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, and technological advances are reshaping Classic Hospitals’ strategic outlook—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Ideal for investors and strategists, the full, instantly downloadable PESTLE delivers deep-dive, editable insights you can act on now—purchase to get the complete analysis.

Political factors

Medical Visa Policy Accessibility

The UK medical visa regime shapes inbound patient volumes to Classic Hospitals; in 2024 international patient revenue for London private hospitals was estimated at £1.2bn, with non-EEA HNW patients representing ~35% of high-value cases. Streamlined visas for medical treatment and investor routes reduce friction, boosting admissions and average revenue per international patient (~£25k–£60k). More restrictive immigration policies could divert this demand to EU or Middle East hubs growing at 8–12% annually.

Diplomatic Relations with Key Source Markets

Strong UK ties with the GCC and East Asia support medical tourism; UK inbound patients from GCC rose ~8% in 2023 to ~22,000, while East Asian referrals grew 6% to ~15,500, underpinning Classic Hospitals’ revenue streams.

Bilateral healthcare agreements and political stability shape government-sponsored patient flows—UK-GCC health MOUs signed in 2022 facilitated an estimated £45m in cross-border treatment spending in 2024.

Classic Hospitals must manage referral networks amid geopolitics; a 2024 survey found 31% of international patient coordinators cite diplomatic disruptions as major operational risk, necessitating contingency partnerships.

NHS Capacity and Private Sector Integration

Post-Brexit Regulatory Frameworks

The post-Brexit UK regulatory landscape now operates under the Medicines and Healthcare products Regulatory Agency (MHRA); since 2021 over 1,200 devices have required UK-specific conformity assessment changes, affecting procurement timelines and compliance costs for Classic Hospitals.

Classic Hospitals must verify specialists comply with evolving UK clinical governance standards—NHS England reported a 7% rise in regulatory inspections in 2023—potentially increasing administrative burden and credentialing delays.

Political decisions on recognition of international medical qualifications reduced automatic EU mutual recognition; as of 2024, UK visas for health and care workers rose 4% year-on-year, tightening the international talent pipeline.

- MHRA-led device revalidation: >1,200 devices impacted since 2021

- Regulatory inspections up 7% in 2023 (NHS England)

- Health and care worker visas +4% YoY in 2024, but recognition barriers remain

Global Geopolitical Stability

Classic Hospitals depends on international patients and is vulnerable to regional conflicts; e.g., global medical travel flows fell 30% from MENA during 2022–23 after geopolitical unrest disrupted referrals.

Travel corridor closures or sanctions can stop arrivals overnight, and markets contributing >15% of revenue each pose concentration risk.

Strategic planning should diversify client geographies—targeting growth in Southeast Asia and Africa where outbound medical spend rose ~12% in 2024.

- 30% drop MENA referrals (2022–23)

- Single-market >15% revenue risk

- Seek SE Asia/Africa +12% outbound spend (2024)

Political shifts reshape Classic Hospitals: £1.2bn intl revenue, patient flows & compliance

Political drivers—visa regimes, NHS backlog procurement, MHRA reforms and geopolitical risk—directly affect Classic Hospitals’ international admissions, clinician supply and compliance costs; 2024–25 figures: £1.2bn international revenue (London privates), 7.3m NHS waiting list (Dec 2025), MHRA >1,200 device changes since 2021, GCC/East Asia referrals +8%/+6% (2023–24).

| Metric | 2023–25 value |

|---|---|

| Intl patient revenue (London) | £1.2bn (2024) |

| NHS elective waiting list | 7.3m (Dec 2025) |

| MHRA device changes | >1,200 since 2021 |

| GCC referrals growth | +8% (2023) |

| East Asia referrals growth | +6% (2023) |

What is included in the product

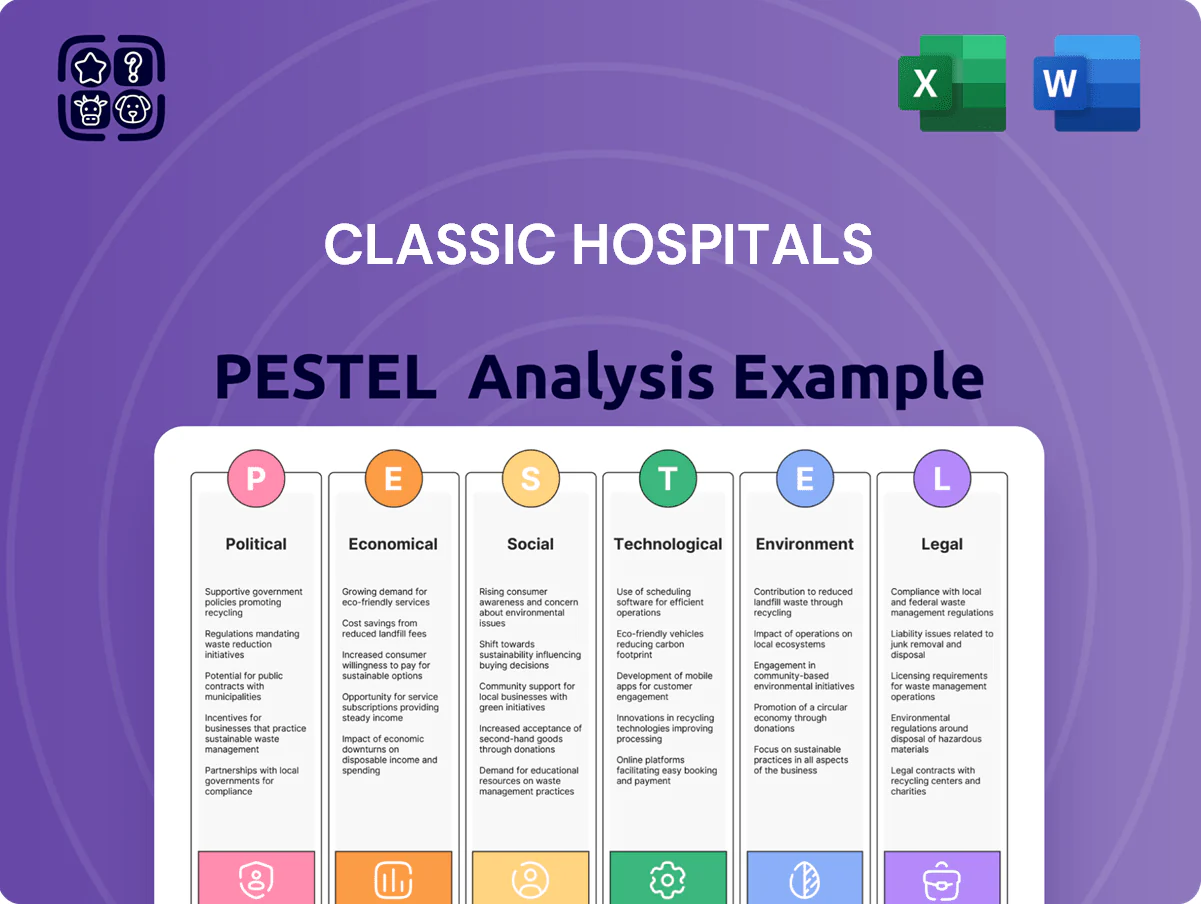

Explores how macro-environmental forces uniquely impact Classic Hospitals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and scenario-based insights tailored for executives, consultants, and investors to identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Classic Hospitals that’s visually segmented for quick meeting use, easy to drop into presentations, and editable so teams can adapt risks and opportunities to their region or service line.

Economic factors

Exchange Rate Volatility

The pound fell about 5% against the dollar in 2023 and traded near 1.28 USD in Jan 2025, boosting international patients’ purchasing power for London treatments by roughly the same margin and making UK care relatively cheaper versus home markets.

A 10% pound appreciation historically shifts some cost-sensitive medical tourists to Turkey or India where procedures can be 40–70% cheaper, posing revenue risk to Classic Hospitals if sterling strengthens sharply.

Global Wealth Distribution Trends

Rising middle/upper classes in emerging markets—Asia-Pacific household wealth up 8.3% in 2024 to $80 trillion—expand demand for premium international healthcare coordination, benefiting Classic Hospitals’ patient acquisition in regions lacking advanced care.

Classic Hospitals depends on private wealth accumulation in markets like India and Brazil, where high-net-worth individuals grew 6–7% in 2024, to fund cross-border treatment and concierge services.

Economic downturns can sharply reduce discretionary spend: during 2023–24 regional slowdowns elective medical travel bookings fell ~12–18%, risking revenue volatility for high-end medical travel and elective procedures.

Inflation in Medical Operational Costs

Competitive Pricing in Global Medical Hubs

London competes with Rochester, Singapore and Dubai as premier medical destinations; global medical tourism market was valued at about $96.2bn in 2024, with the UK capturing roughly 6% of international patient flows.

Alternative hubs offer economic advantages—Singapore and Dubai benefit from government subsidies and Rochester leverages lower operating costs—pressuring UK market share, which slipped an estimated 0.5–1% in 2023–24.

Classic Hospitals must justify London’s premium pricing (average private inpatient tariff ~£7,800 in 2024) by emphasizing clinical outcomes, specialist expertise and integrated research links.

- Global market $96.2bn (2024)

- UK ~6% share; −0.5–1% 2023–24

- London private inpatient avg ~£7,800 (2024)

- Competitors boosted by subsidies/lower labor costs

Labor Market Dynamics for Healthcare Professionals

The cost and availability of world-class medical specialists and support staff in London are key economic drivers for Classic Hospitals; consultant salaries average £120k–£180k and agency nurse rates can exceed £45/hour, inflating operating expenses.

Nursing shortages—NHS vacancy rate ~10.6% (2024) and rising private-sector competition—push up recruitment and retention costs, risking service delays and patient satisfaction.

Immigration policy changes affect inflows of skilled healthcare workers; the Health and Care Visa introduced faster routes in 2022, with 2024 visa admissions for healthcare up ~8%, supporting staffing for international-patient services.

- Consultant pay £120k–£180k; agency nurses >£45/hr

- NHS vacancy rate ~10.6% (2024), raising costs

- Health and Care Visa increased healthcare admissions ~8% (2024)

UK MedTourism Faces Cost Pressures: Inflation, FX & Rising OPEX Squeeze Margins

Exchange swings (GBP ~1.28 USD Jan 2025) and 4.5% UK inflation (2024) affect pricing power; global medical tourism $96.2bn (2024), UK ~6% share. Equipment costs +8–12% YoY and indemnity +15% raise OPEX; consultant pay £120k–£180k, agency nurses >£45/hr, NHS vacancy ~10.6% (2024).

| Metric | Value |

|---|---|

| Global market | $96.2bn (2024) |

| UK share | ~6% |

| GBP/USD | ~1.28 (Jan 2025) |

| Inflation | 4.5% (2024) |

| Consultant pay | £120k–£180k |

What You See Is What You Get

Classic Hospitals PESTLE Analysis

The preview shown here is the exact Classic Hospitals PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, and technological advances are reshaping Classic Hospitals’ strategic outlook—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Ideal for investors and strategists, the full, instantly downloadable PESTLE delivers deep-dive, editable insights you can act on now—purchase to get the complete analysis.

Political factors

Medical Visa Policy Accessibility

The UK medical visa regime shapes inbound patient volumes to Classic Hospitals; in 2024 international patient revenue for London private hospitals was estimated at £1.2bn, with non-EEA HNW patients representing ~35% of high-value cases. Streamlined visas for medical treatment and investor routes reduce friction, boosting admissions and average revenue per international patient (~£25k–£60k). More restrictive immigration policies could divert this demand to EU or Middle East hubs growing at 8–12% annually.

Diplomatic Relations with Key Source Markets

Strong UK ties with the GCC and East Asia support medical tourism; UK inbound patients from GCC rose ~8% in 2023 to ~22,000, while East Asian referrals grew 6% to ~15,500, underpinning Classic Hospitals’ revenue streams.

Bilateral healthcare agreements and political stability shape government-sponsored patient flows—UK-GCC health MOUs signed in 2022 facilitated an estimated £45m in cross-border treatment spending in 2024.

Classic Hospitals must manage referral networks amid geopolitics; a 2024 survey found 31% of international patient coordinators cite diplomatic disruptions as major operational risk, necessitating contingency partnerships.

NHS Capacity and Private Sector Integration

Post-Brexit Regulatory Frameworks

The post-Brexit UK regulatory landscape now operates under the Medicines and Healthcare products Regulatory Agency (MHRA); since 2021 over 1,200 devices have required UK-specific conformity assessment changes, affecting procurement timelines and compliance costs for Classic Hospitals.

Classic Hospitals must verify specialists comply with evolving UK clinical governance standards—NHS England reported a 7% rise in regulatory inspections in 2023—potentially increasing administrative burden and credentialing delays.

Political decisions on recognition of international medical qualifications reduced automatic EU mutual recognition; as of 2024, UK visas for health and care workers rose 4% year-on-year, tightening the international talent pipeline.

- MHRA-led device revalidation: >1,200 devices impacted since 2021

- Regulatory inspections up 7% in 2023 (NHS England)

- Health and care worker visas +4% YoY in 2024, but recognition barriers remain

Global Geopolitical Stability

Classic Hospitals depends on international patients and is vulnerable to regional conflicts; e.g., global medical travel flows fell 30% from MENA during 2022–23 after geopolitical unrest disrupted referrals.

Travel corridor closures or sanctions can stop arrivals overnight, and markets contributing >15% of revenue each pose concentration risk.

Strategic planning should diversify client geographies—targeting growth in Southeast Asia and Africa where outbound medical spend rose ~12% in 2024.

- 30% drop MENA referrals (2022–23)

- Single-market >15% revenue risk

- Seek SE Asia/Africa +12% outbound spend (2024)

Political shifts reshape Classic Hospitals: £1.2bn intl revenue, patient flows & compliance

Political drivers—visa regimes, NHS backlog procurement, MHRA reforms and geopolitical risk—directly affect Classic Hospitals’ international admissions, clinician supply and compliance costs; 2024–25 figures: £1.2bn international revenue (London privates), 7.3m NHS waiting list (Dec 2025), MHRA >1,200 device changes since 2021, GCC/East Asia referrals +8%/+6% (2023–24).

| Metric | 2023–25 value |

|---|---|

| Intl patient revenue (London) | £1.2bn (2024) |

| NHS elective waiting list | 7.3m (Dec 2025) |

| MHRA device changes | >1,200 since 2021 |

| GCC referrals growth | +8% (2023) |

| East Asia referrals growth | +6% (2023) |

What is included in the product

Explores how macro-environmental forces uniquely impact Classic Hospitals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and scenario-based insights tailored for executives, consultants, and investors to identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Classic Hospitals that’s visually segmented for quick meeting use, easy to drop into presentations, and editable so teams can adapt risks and opportunities to their region or service line.

Economic factors

Exchange Rate Volatility

The pound fell about 5% against the dollar in 2023 and traded near 1.28 USD in Jan 2025, boosting international patients’ purchasing power for London treatments by roughly the same margin and making UK care relatively cheaper versus home markets.

A 10% pound appreciation historically shifts some cost-sensitive medical tourists to Turkey or India where procedures can be 40–70% cheaper, posing revenue risk to Classic Hospitals if sterling strengthens sharply.

Global Wealth Distribution Trends

Rising middle/upper classes in emerging markets—Asia-Pacific household wealth up 8.3% in 2024 to $80 trillion—expand demand for premium international healthcare coordination, benefiting Classic Hospitals’ patient acquisition in regions lacking advanced care.

Classic Hospitals depends on private wealth accumulation in markets like India and Brazil, where high-net-worth individuals grew 6–7% in 2024, to fund cross-border treatment and concierge services.

Economic downturns can sharply reduce discretionary spend: during 2023–24 regional slowdowns elective medical travel bookings fell ~12–18%, risking revenue volatility for high-end medical travel and elective procedures.

Inflation in Medical Operational Costs

Competitive Pricing in Global Medical Hubs

London competes with Rochester, Singapore and Dubai as premier medical destinations; global medical tourism market was valued at about $96.2bn in 2024, with the UK capturing roughly 6% of international patient flows.

Alternative hubs offer economic advantages—Singapore and Dubai benefit from government subsidies and Rochester leverages lower operating costs—pressuring UK market share, which slipped an estimated 0.5–1% in 2023–24.

Classic Hospitals must justify London’s premium pricing (average private inpatient tariff ~£7,800 in 2024) by emphasizing clinical outcomes, specialist expertise and integrated research links.

- Global market $96.2bn (2024)

- UK ~6% share; −0.5–1% 2023–24

- London private inpatient avg ~£7,800 (2024)

- Competitors boosted by subsidies/lower labor costs

Labor Market Dynamics for Healthcare Professionals

The cost and availability of world-class medical specialists and support staff in London are key economic drivers for Classic Hospitals; consultant salaries average £120k–£180k and agency nurse rates can exceed £45/hour, inflating operating expenses.

Nursing shortages—NHS vacancy rate ~10.6% (2024) and rising private-sector competition—push up recruitment and retention costs, risking service delays and patient satisfaction.

Immigration policy changes affect inflows of skilled healthcare workers; the Health and Care Visa introduced faster routes in 2022, with 2024 visa admissions for healthcare up ~8%, supporting staffing for international-patient services.

- Consultant pay £120k–£180k; agency nurses >£45/hr

- NHS vacancy rate ~10.6% (2024), raising costs

- Health and Care Visa increased healthcare admissions ~8% (2024)

UK MedTourism Faces Cost Pressures: Inflation, FX & Rising OPEX Squeeze Margins

Exchange swings (GBP ~1.28 USD Jan 2025) and 4.5% UK inflation (2024) affect pricing power; global medical tourism $96.2bn (2024), UK ~6% share. Equipment costs +8–12% YoY and indemnity +15% raise OPEX; consultant pay £120k–£180k, agency nurses >£45/hr, NHS vacancy ~10.6% (2024).

| Metric | Value |

|---|---|

| Global market | $96.2bn (2024) |

| UK share | ~6% |

| GBP/USD | ~1.28 (Jan 2025) |

| Inflation | 4.5% (2024) |

| Consultant pay | £120k–£180k |

What You See Is What You Get

Classic Hospitals PESTLE Analysis

The preview shown here is the exact Classic Hospitals PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.