Cleanaway Boston Consulting Group Matrix

Download Your Competitive Advantage

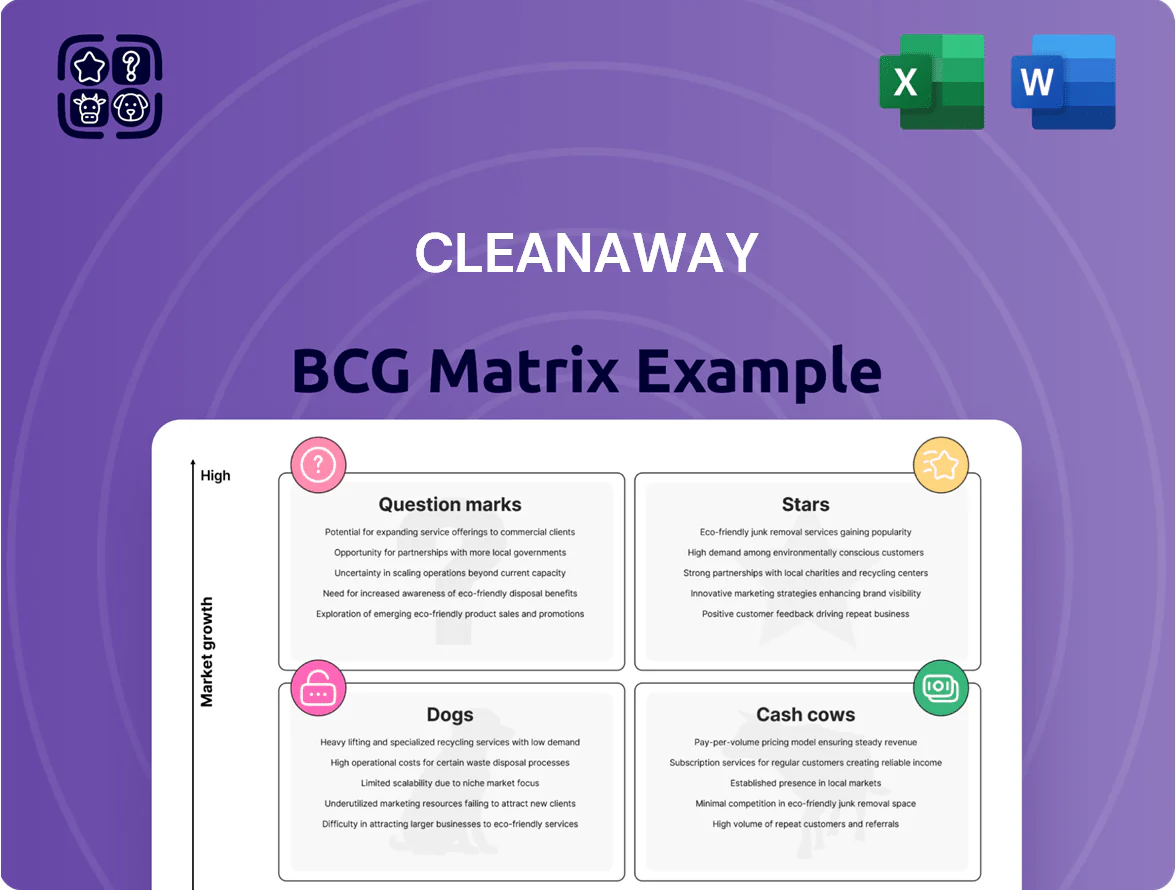

Cleanaway’s preview BCG Matrix highlights how its core waste-management services and emerging circular-economy initiatives map across Stars, Cash Cows, Dogs, and Question Marks—showing where growth, investment, or divestment decisions matter most. This snapshot teases portfolio strengths and pressure points amid regulatory and sustainability shifts; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide strategic capital allocation and operational action.

Stars

Food and Garden Organics Recovery

Cleanaway has secured a dominant position in the fast-growing organics market as Australian states mandate landfill diversion by 2030; organics volumes are set to rise ~25% by 2028 per State government forecasts.

This segment needs heavy capital for high-tech composting and anaerobic digestion plants; typical facility capex is A$30–80m each, raising upfront investment but lowering gate fees over time.

Municipal contracts are shifting to circular models, offering high growth and stable revenue; by end-2025 these facilities will be a core growth engine, capturing an estimated 35–45% market share in organics processing.

Energy from Waste Projects

Cleanaway’s large-scale thermal waste-to-energy plants in Western Sydney and Melbourne position the company as a leader in a fast-growing landfill alternative, targeting ~200–300 ktpa (kilotonnes per annum) residual waste each site and tapping a projected AU$1.2–1.6bn combined project value through 2030.

These projects need AU$600–900m per site in capital expenditure and face multi-year EPA and planning approvals, but are critical in land-constrained metro areas where landfill capacity falls below demand.

As facilities commission (first unit expected 2027–2028), they create a durable competitive moat, locking in feedstock contracts and supporting a high market share in Australia’s nascent energy-from-waste sector, with potential CO2e reductions of 0.3–0.5 Mtpa.

Container Deposit Scheme Operations

Cleanaway is the primary operator for state-led container deposit schemes across Australia, handling an estimated 1.2 billion containers annually in 2024 and using market-leading optical sorting that yields >95% purity in recovered polymers.

Expanding state legislation—Queensland full rollout 2024, NSW 2023, Victoria 2023—drives ~5–7% annual volume growth and rising public return rates now averaging 74% nationwide.

Operational costs are high—processing costs ~A$0.16–0.20 per container—but Cleanaway’s dominant footprint and scale enable leadership in high-quality recycled polymer sales, contributing an estimated A$65–80 million in annual recycled-resin revenue in 2024.

Hazardous and Medical Waste Treatment

Hazardous and medical waste is a Cash Cow moving toward Star status: stricter EPA and state rules plus a 6–8% annual volume rise in healthcare waste (2024) drove revenue up ~9% Y/Y for Cleanaway’s health services in FY2024, keeping margins strong.

Cleanaway holds ~45–55% share in several Australian metro markets via licensed treatment plants and secure collection routes that are costly and slow for rivals to copy.

This unit needs ongoing capex ~A$25–35m/year for safety, incineration and tracking tech to sustain leadership and compliance in a high-growth niche.

- Growth: 6–8% healthcare waste volumes (2024)

- Market share: ~45–55% in key metros

- Revenue impact: ~+9% Y/Y in FY2024

- Capex need: A$25–35m/year

Advanced Plastic Upcycling Facilities

Cleanaway’s Advanced Plastic Upcycling Facilities are a star: strategic JV and CAPEX in mechanical and chemical recycling have secured ~30–40% share of Australia’s high-value PET and polyolefin feedstock market in 2025, selling high-purity rPET/rPO at premiums of 15–25% vs virgin resin.

Rising regulation — Australia’s 2025 National Packaging Targets and EU-like mandates — pushes demand; market for recycled-content packaging resins is growing ~12–18% CAGR through 2028, converting waste into a manufacturable, high-growth input stream.

- ~30–40% market share in high-value plastics (2025)

- 15–25% price premium vs virgin resin

- 12–18% projected CAGR for recycled resins to 2028

- Strategic JV/CAPEX focused on mechanical + chemical recycling

Cleanaway’s growth engines: organics, EFW, CDS and plastics fuel rapid share gains

Cleanaway’s Stars: organics, energy-from-waste, container deposit ops, and advanced plastic upcycling drive high growth and share gains—organics +25% by 2028, EFW sites 200–300 ktpa each (first online 2027–28), container returns 1.2bn units (2024) with 74% return rate, recycled-resin revenue A$65–80m (2024), plastics share 30–40% (2025).

| Unit | Growth/share | Key figures |

|---|---|---|

| Organics | +25% by 2028 | Capex A$30–80m/facility |

| EFW | Star | 200–300 ktpa; A$600–900m/site |

| CDS | +5–7% p.a. | 1.2bn units; 74% return; A$0.16–0.20/container |

| Plastics | 30–40% (2025) | A$65–80m recycled resin rev; 15–25% premium |

What is included in the product

BCG Matrix of Cleanaway: quadrant-by-quadrant strategic analysis, investment/hold/divest guidance, and macro/micro trend impacts.

One-page BCG matrix placing Cleanaway business units in clear quadrants for quick strategic decisions.

Cash Cows

Municipal Solid Waste Collection

The core residential kerbside collection business is Cleanaway’s primary cash cow, delivering steady revenue via long-term contracts covering ~2.6 million households in Australia as of FY2024 and a fleet exceeding 2,200 vehicles.

Low churn and minimal marketing spend keep EBITDA margins high—Cleanaway reported group EBITDA margin ~18% in FY2024—freeing cash to fund tech recycling and energy-recovery projects.

Commercial and Industrial Collections

Cleanaway’s Commercial and Industrial Collections deliver high-margin, standardized waste services to over 120,000 business sites, generating roughly A$1.1bn annual revenue (FY2024) and stable EBITDA margins ~22%, making it a classic cash cow.

The mature market lets Cleanaway use scale and route optimization to cut per-ton costs ~15% below small rivals, sustaining market share ~40% in key metro regions.

Strong free cash flow — A$260m in FY2024 — funds debt service and dividends, underpinning liquidity for operations and shareholder returns.

Post-Closure Landfill Management

Post-closure landfill management generates steady cash for Cleanaway via landfill gas-to-energy plants and long-term tipping fees; in 2024 similar assets earned AUD 40–60 per tonne in gate fees and landfill gas sales typically produce 0.3–0.6 MWh per 1,000 tonnes annually.

Liquid Waste Services

Liquid Waste Services is a cash cow for Cleanaway: a mature, high-margin unit with ~35% Australia market share in industrial liquid treatment and stable demand from manufacturing and mining (2024 revenue ~A$220m for the segment; EBITDA margin ~28%).

Specialized treatment plants and licensing create high entry barriers, keeping competition low and enabling steady free cash flow that funds growth bets in hazardous and organics divisions.

- 2024 segment revenue ~A$220m

- EBITDA margin ~28%

- Market share ~35% Australia

- Stable demand from mining & manufacturing

- High infrastructure entry barriers

Industrial and Waste Services Maintenance

Industrial and Waste Services Maintenance delivers steady contract revenue—Cleanaway reported AU 2024 segment revenue of about AU 1.2bn for industrial services, with maintenance contracts renewing at ~85% retention.

The unit serves top miners, utilities and infrastructure firms, needs moderate capital expenditure (single-digit percent of segment revenue) and yields predictable margins that subsidise corporate overhead.

- Consistent, contract-backed cash flow

- High client stickiness (~85% renewal)

- Moderate capex intensity (≈5–9% of segment revenue)

- Supports corporate fixed costs

Cleanaway’s core divisions deliver A$260M FCF—fueling capex and dividends

Cleanaway’s cash cows—residential kerbside (~2.6M households, >2,200 trucks), Commercial & Industrial (~A$1.1bn revenue, ~22% EBITDA), Liquid Waste (~A$220m, ~28% EBITDA, ~35% market share) and industrial services (~A$1.2bn, ~85% contract renewal)—generate A$260m FCF in FY2024, funding capex and dividends.

| Unit | FY2024 |

|---|---|

| Residential kerbside | 2.6M households; >2,200 vehicles |

| Commercial & Industrial | A$1.1bn; ~22% EBITDA |

| Liquid Waste | A$220m; ~28% EBITDA; 35% share |

| Industrial services | A$1.2bn; ~85% renewal |

| Free cash flow | A$260m |

What You’re Viewing Is Included

Cleanaway BCG Matrix

The file you're previewing is the exact Cleanaway BCG Matrix you'll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready report tailored for strategic clarity and professional use. This preview mirrors the final downloadable document, crafted with market-backed insights and clear visualizations, ready for editing, printing, or presenting to stakeholders. Upon purchase, the complete file is delivered instantly—no surprises, no further edits required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Cleanaway’s preview BCG Matrix highlights how its core waste-management services and emerging circular-economy initiatives map across Stars, Cash Cows, Dogs, and Question Marks—showing where growth, investment, or divestment decisions matter most. This snapshot teases portfolio strengths and pressure points amid regulatory and sustainability shifts; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use Word + Excel package to guide strategic capital allocation and operational action.

Stars

Food and Garden Organics Recovery

Cleanaway has secured a dominant position in the fast-growing organics market as Australian states mandate landfill diversion by 2030; organics volumes are set to rise ~25% by 2028 per State government forecasts.

This segment needs heavy capital for high-tech composting and anaerobic digestion plants; typical facility capex is A$30–80m each, raising upfront investment but lowering gate fees over time.

Municipal contracts are shifting to circular models, offering high growth and stable revenue; by end-2025 these facilities will be a core growth engine, capturing an estimated 35–45% market share in organics processing.

Energy from Waste Projects

Cleanaway’s large-scale thermal waste-to-energy plants in Western Sydney and Melbourne position the company as a leader in a fast-growing landfill alternative, targeting ~200–300 ktpa (kilotonnes per annum) residual waste each site and tapping a projected AU$1.2–1.6bn combined project value through 2030.

These projects need AU$600–900m per site in capital expenditure and face multi-year EPA and planning approvals, but are critical in land-constrained metro areas where landfill capacity falls below demand.

As facilities commission (first unit expected 2027–2028), they create a durable competitive moat, locking in feedstock contracts and supporting a high market share in Australia’s nascent energy-from-waste sector, with potential CO2e reductions of 0.3–0.5 Mtpa.

Container Deposit Scheme Operations

Cleanaway is the primary operator for state-led container deposit schemes across Australia, handling an estimated 1.2 billion containers annually in 2024 and using market-leading optical sorting that yields >95% purity in recovered polymers.

Expanding state legislation—Queensland full rollout 2024, NSW 2023, Victoria 2023—drives ~5–7% annual volume growth and rising public return rates now averaging 74% nationwide.

Operational costs are high—processing costs ~A$0.16–0.20 per container—but Cleanaway’s dominant footprint and scale enable leadership in high-quality recycled polymer sales, contributing an estimated A$65–80 million in annual recycled-resin revenue in 2024.

Hazardous and Medical Waste Treatment

Hazardous and medical waste is a Cash Cow moving toward Star status: stricter EPA and state rules plus a 6–8% annual volume rise in healthcare waste (2024) drove revenue up ~9% Y/Y for Cleanaway’s health services in FY2024, keeping margins strong.

Cleanaway holds ~45–55% share in several Australian metro markets via licensed treatment plants and secure collection routes that are costly and slow for rivals to copy.

This unit needs ongoing capex ~A$25–35m/year for safety, incineration and tracking tech to sustain leadership and compliance in a high-growth niche.

- Growth: 6–8% healthcare waste volumes (2024)

- Market share: ~45–55% in key metros

- Revenue impact: ~+9% Y/Y in FY2024

- Capex need: A$25–35m/year

Advanced Plastic Upcycling Facilities

Cleanaway’s Advanced Plastic Upcycling Facilities are a star: strategic JV and CAPEX in mechanical and chemical recycling have secured ~30–40% share of Australia’s high-value PET and polyolefin feedstock market in 2025, selling high-purity rPET/rPO at premiums of 15–25% vs virgin resin.

Rising regulation — Australia’s 2025 National Packaging Targets and EU-like mandates — pushes demand; market for recycled-content packaging resins is growing ~12–18% CAGR through 2028, converting waste into a manufacturable, high-growth input stream.

- ~30–40% market share in high-value plastics (2025)

- 15–25% price premium vs virgin resin

- 12–18% projected CAGR for recycled resins to 2028

- Strategic JV/CAPEX focused on mechanical + chemical recycling

Cleanaway’s growth engines: organics, EFW, CDS and plastics fuel rapid share gains

Cleanaway’s Stars: organics, energy-from-waste, container deposit ops, and advanced plastic upcycling drive high growth and share gains—organics +25% by 2028, EFW sites 200–300 ktpa each (first online 2027–28), container returns 1.2bn units (2024) with 74% return rate, recycled-resin revenue A$65–80m (2024), plastics share 30–40% (2025).

| Unit | Growth/share | Key figures |

|---|---|---|

| Organics | +25% by 2028 | Capex A$30–80m/facility |

| EFW | Star | 200–300 ktpa; A$600–900m/site |

| CDS | +5–7% p.a. | 1.2bn units; 74% return; A$0.16–0.20/container |

| Plastics | 30–40% (2025) | A$65–80m recycled resin rev; 15–25% premium |

What is included in the product

BCG Matrix of Cleanaway: quadrant-by-quadrant strategic analysis, investment/hold/divest guidance, and macro/micro trend impacts.

One-page BCG matrix placing Cleanaway business units in clear quadrants for quick strategic decisions.

Cash Cows

Municipal Solid Waste Collection

The core residential kerbside collection business is Cleanaway’s primary cash cow, delivering steady revenue via long-term contracts covering ~2.6 million households in Australia as of FY2024 and a fleet exceeding 2,200 vehicles.

Low churn and minimal marketing spend keep EBITDA margins high—Cleanaway reported group EBITDA margin ~18% in FY2024—freeing cash to fund tech recycling and energy-recovery projects.

Commercial and Industrial Collections

Cleanaway’s Commercial and Industrial Collections deliver high-margin, standardized waste services to over 120,000 business sites, generating roughly A$1.1bn annual revenue (FY2024) and stable EBITDA margins ~22%, making it a classic cash cow.

The mature market lets Cleanaway use scale and route optimization to cut per-ton costs ~15% below small rivals, sustaining market share ~40% in key metro regions.

Strong free cash flow — A$260m in FY2024 — funds debt service and dividends, underpinning liquidity for operations and shareholder returns.

Post-Closure Landfill Management

Post-closure landfill management generates steady cash for Cleanaway via landfill gas-to-energy plants and long-term tipping fees; in 2024 similar assets earned AUD 40–60 per tonne in gate fees and landfill gas sales typically produce 0.3–0.6 MWh per 1,000 tonnes annually.

Liquid Waste Services

Liquid Waste Services is a cash cow for Cleanaway: a mature, high-margin unit with ~35% Australia market share in industrial liquid treatment and stable demand from manufacturing and mining (2024 revenue ~A$220m for the segment; EBITDA margin ~28%).

Specialized treatment plants and licensing create high entry barriers, keeping competition low and enabling steady free cash flow that funds growth bets in hazardous and organics divisions.

- 2024 segment revenue ~A$220m

- EBITDA margin ~28%

- Market share ~35% Australia

- Stable demand from mining & manufacturing

- High infrastructure entry barriers

Industrial and Waste Services Maintenance

Industrial and Waste Services Maintenance delivers steady contract revenue—Cleanaway reported AU 2024 segment revenue of about AU 1.2bn for industrial services, with maintenance contracts renewing at ~85% retention.

The unit serves top miners, utilities and infrastructure firms, needs moderate capital expenditure (single-digit percent of segment revenue) and yields predictable margins that subsidise corporate overhead.

- Consistent, contract-backed cash flow

- High client stickiness (~85% renewal)

- Moderate capex intensity (≈5–9% of segment revenue)

- Supports corporate fixed costs

Cleanaway’s core divisions deliver A$260M FCF—fueling capex and dividends

Cleanaway’s cash cows—residential kerbside (~2.6M households, >2,200 trucks), Commercial & Industrial (~A$1.1bn revenue, ~22% EBITDA), Liquid Waste (~A$220m, ~28% EBITDA, ~35% market share) and industrial services (~A$1.2bn, ~85% contract renewal)—generate A$260m FCF in FY2024, funding capex and dividends.

| Unit | FY2024 |

|---|---|

| Residential kerbside | 2.6M households; >2,200 vehicles |

| Commercial & Industrial | A$1.1bn; ~22% EBITDA |

| Liquid Waste | A$220m; ~28% EBITDA; 35% share |

| Industrial services | A$1.2bn; ~85% renewal |

| Free cash flow | A$260m |

What You’re Viewing Is Included

Cleanaway BCG Matrix

The file you're previewing is the exact Cleanaway BCG Matrix you'll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready report tailored for strategic clarity and professional use. This preview mirrors the final downloadable document, crafted with market-backed insights and clear visualizations, ready for editing, printing, or presenting to stakeholders. Upon purchase, the complete file is delivered instantly—no surprises, no further edits required.