Clear Channel Outdoor Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

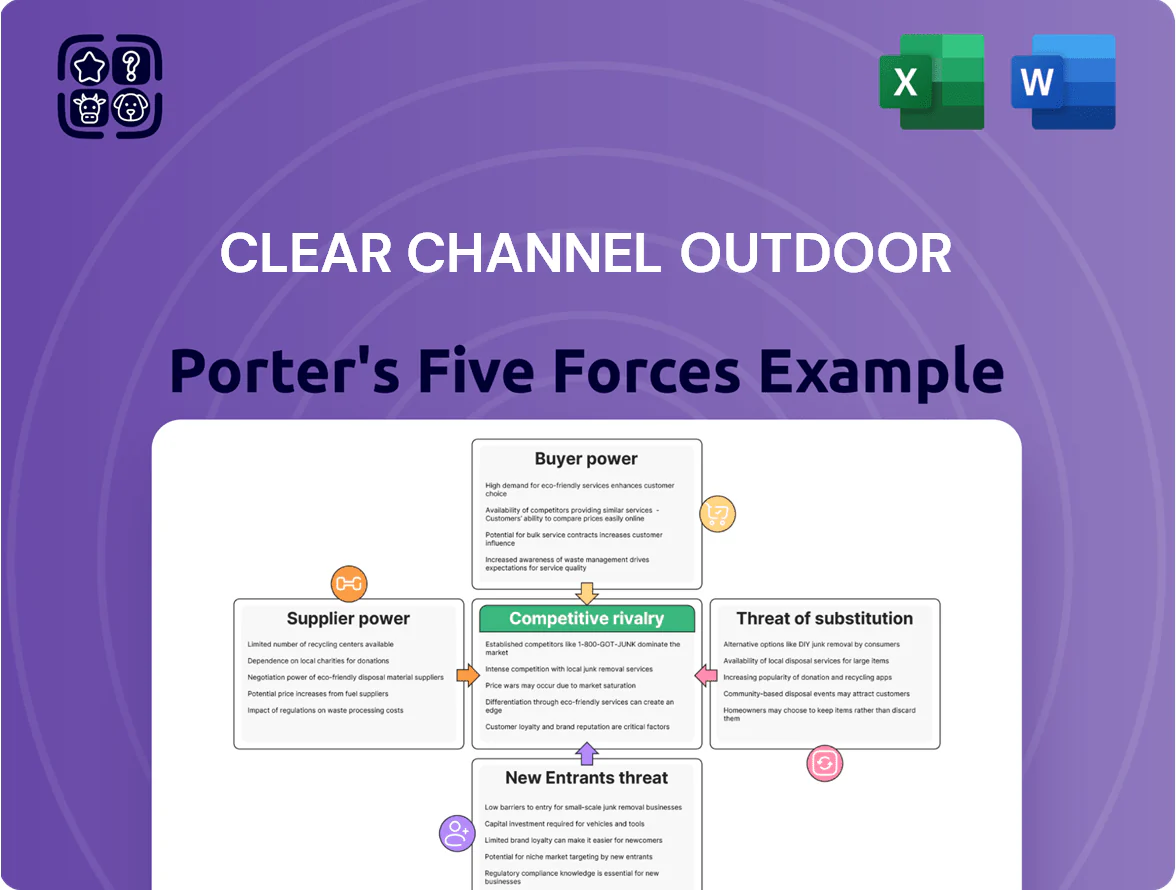

Clear Channel Outdoor faces moderate buyer power, steady supplier relationships, and significant rivalry driven by urban ad spend and digital transition, while barriers to entry and substitutes create both threats and opportunities.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Clear Channel Outdoor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Premium Real Estate Locations

Primary suppliers—private landowners and government agencies that lease space for billboards and transit displays—gain leverage as prime urban inventory nears saturation by late 2025; research shows street-level digital panel availability in top 25 US DMAs fell ~18% from 2021–2024, pushing average urban billboard rents up ~12% in 2024; landlords can demand higher rents or larger revenue shares at renewals, squeezing Clear Channel Outdoor’s margins.

Dependence on Digital Display Manufacturers

Clear Channel’s shift to digital out-of-home ties it to a small set of LED and hardware makers; top suppliers like Samsung and Leyard (market share leaders in 2024) dominate high-durability, energy-efficient screens, concentrating supplier power.

Because premium displays account for roughly 40% of new capital expenditure in 2024 for major OOH firms, price or lead-time swings from these vendors can move Clear Channel’s capex by millions per quarter.

Global supply disruptions—chip shortages in 2021–22 showed component-sensitive pricing up 15–30%—mean procurement risk translates directly into margin pressure and project delays for Clear Channel.

Municipal and Transit Authority Contracts

Municipal and transit agencies manage long-term concessions that cover roughly 30–40% of Clear Channel Outdoor’s street furniture and transit inventory, giving them strong supplier power since they grant exclusive operating rights via competitive bids.

Losing one major city contract can cut regional revenue by double-digit percentages; for example, a single U.S. metropolitan concession has accounted for up to an estimated $25–40M in annual revenue in recent deals.

Specialized Programmatic Software Providers

As programmatic buying grows, Clear Channel depends on third-party programmatic ad-serving and analytics vendors that power connections to demand-side platforms; in 2024 programmatic accounted for about 38% of global OOH ad transactions, underscoring this reliance.

These suppliers supply the core infrastructure—SSP wrappers, ad servers, identity graphs—making integration essential and often costly, with enterprise licensing and data fees that can run into millions annually for large networks.

Clear Channel builds internal tools but must maintain compatibility with industry-standard platforms (e.g., The Trade Desk, Magnite), so vendor lock-in and switching costs remain high and strategic.

- 2024 programmatic ~38% of OOH transactions

- Third-party licensing/data fees: often millions/year

- High switching costs due to integration and identity needs

Energy and Utility Providers

Energy and utility companies are critical suppliers for Clear Channel Outdoor, powering thousands of digital screens and illuminated boards that consumed an estimated 1.2 TWh in 2024 across the US and Europe.

By 2025 higher utility prices—US industrial electricity up ~9% YoY in 2024—and tighter carbon rules (EU ETS prices ~€85/ton in 2025) have raised suppliers’ bargaining power.

Clear Channel must manage rising bills and invest in on-site solar, batteries, and power‑purchase agreements to cut costs, lower emissions, and meet regulator and supplier demands.

- 2024 est. energy use 1.2 TWh

- US industrial power +9% YoY (2024)

- EU ETS ~€85/ton CO2 (2025)

- Mitigation: solar, batteries, PPAs

Supplier squeeze: panel shortages, rising rents, programmatic growth and energy costs

Suppliers (landlords, LED makers, utilities, municipalities, programmatic vendors) hold elevated bargaining power: urban inventory scarcity cut panel availability ~18% (2021–24) and raised rents ~12% (2024); LED vendors (Samsung, Leyard) concentrated market; programmatic ~38% of OOH transactions (2024); energy use ~1.2 TWh (2024) and US industrial power +9% YoY (2024) squeeze margins.

| Metric | Value |

|---|---|

| Panel availability decline | ~18% (2021–24) |

| Urban rent change | +12% (2024) |

| Programmatic share | 38% (2024) |

| Energy use | 1.2 TWh (2024) |

| US industrial power | +9% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Clear Channel Outdoor that uncovers competitive intensity, buyer and supplier leverage, substitution risks, and barriers to entry—highlighting disruptive threats, regulatory impacts, and strategic levers to defend market share.

A concise, one-sheet Porter's Five Forces for Clear Channel Outdoor that highlights competitive pressures and strategic levers—perfect for fast boardroom decisions or investor briefs.

Customers Bargaining Power

Concentration of Large Advertising Agencies

Availability of Alternative Media Channels

Customers face many alternatives—social media (Meta, TikTok), search (Google), and TV—where global digital ad spend hit $514B in 2023 and was forecast near $570B for 2025, so Clear Channel Outdoor (CCO) competes for portions of that budget.

If CCO raises rates too far, advertisers can shift to digital channels offering granular targeting and measurable ROI; programmatic channels saw 72% of US digital display spend in 2024, showing easy reallocation.

High price elasticity means CCO must keep pricing aligned with digital CPMs (US OOH CPMs averaged $6–12 in 2024 vs. programmatic $2–8), pressuring margins and forcing competitive rate-setting.

Demand for Real-Time Programmatic Flexibility

Increased Expectations for Attribution Data

Modern advertisers demand attribution to prove ROI for outdoor ads; 68% of CMOs in 2024 said measurability drives media spend decisions, so buyers press Clear Channel Outdoor for granular audience analytics, foot‑traffic conversion metrics, and mobile retargeting.

If CCO fails to supply these advanced metrics, clients shift to rivals: digital and programmatic OOH vendors reported a 22% revenue gain in 2023 from offering real‑time measurement.

- 68% of CMOs (2024) value measurability

- 22% revenue gain for measurability-focused OOH vendors (2023)

- Key asks: audience analytics, foot-traffic conversion, mobile retargeting

Low Switching Costs Between Media Owners

In major U.S. markets where Clear Channel Outdoor competes with Lamar Advertising and Outfront, switching a campaign is cheap and fast, so advertisers hold bargaining power; Q3 2025 OOH industry pricing shows spot rates varying +/-15% across providers for similar urban corridors, letting brands shift for price or inventory reasons.

Many billboards cluster on the same high-traffic routes, so advertisers trade based on short-term availability rather than vendor lock-in, keeping Clear Channel’s churn risk elevated when its fill rate drops below local average (usually ~85%).

- Multiple rivals in top 20 DMAs

- Spot rate variance ~15%

- Typical fill rate benchmark ~85%

- Low tech/integration switching cost

Buyer Power Soars: Agencies Drive 70% Spend, Programmatic OOH Fuels Price Pressure

| Metric | Value (year) |

|---|---|

| Agency share of global ad spend | ~70% (2024) |

| CCO programmatic revenue growth | +28% (2024) |

| OOH programmatic share | 46% (2025 proj.) |

| CMOs valuing measurability | 68% (2024) |

| Spot rate variance | ±15% (Q3 2025) |

What You See Is What You Get

Clear Channel Outdoor Porter's Five Forces Analysis

This preview shows the exact Clear Channel Outdoor Porter's Five Forces analysis you'll receive—no placeholders or samples, fully formatted and ready for download immediately after purchase.

The document displayed here is the complete, professionally written file included with your order, so what you see is precisely what you'll get upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Clear Channel Outdoor faces moderate buyer power, steady supplier relationships, and significant rivalry driven by urban ad spend and digital transition, while barriers to entry and substitutes create both threats and opportunities.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Clear Channel Outdoor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Premium Real Estate Locations

Primary suppliers—private landowners and government agencies that lease space for billboards and transit displays—gain leverage as prime urban inventory nears saturation by late 2025; research shows street-level digital panel availability in top 25 US DMAs fell ~18% from 2021–2024, pushing average urban billboard rents up ~12% in 2024; landlords can demand higher rents or larger revenue shares at renewals, squeezing Clear Channel Outdoor’s margins.

Dependence on Digital Display Manufacturers

Clear Channel’s shift to digital out-of-home ties it to a small set of LED and hardware makers; top suppliers like Samsung and Leyard (market share leaders in 2024) dominate high-durability, energy-efficient screens, concentrating supplier power.

Because premium displays account for roughly 40% of new capital expenditure in 2024 for major OOH firms, price or lead-time swings from these vendors can move Clear Channel’s capex by millions per quarter.

Global supply disruptions—chip shortages in 2021–22 showed component-sensitive pricing up 15–30%—mean procurement risk translates directly into margin pressure and project delays for Clear Channel.

Municipal and Transit Authority Contracts

Municipal and transit agencies manage long-term concessions that cover roughly 30–40% of Clear Channel Outdoor’s street furniture and transit inventory, giving them strong supplier power since they grant exclusive operating rights via competitive bids.

Losing one major city contract can cut regional revenue by double-digit percentages; for example, a single U.S. metropolitan concession has accounted for up to an estimated $25–40M in annual revenue in recent deals.

Specialized Programmatic Software Providers

As programmatic buying grows, Clear Channel depends on third-party programmatic ad-serving and analytics vendors that power connections to demand-side platforms; in 2024 programmatic accounted for about 38% of global OOH ad transactions, underscoring this reliance.

These suppliers supply the core infrastructure—SSP wrappers, ad servers, identity graphs—making integration essential and often costly, with enterprise licensing and data fees that can run into millions annually for large networks.

Clear Channel builds internal tools but must maintain compatibility with industry-standard platforms (e.g., The Trade Desk, Magnite), so vendor lock-in and switching costs remain high and strategic.

- 2024 programmatic ~38% of OOH transactions

- Third-party licensing/data fees: often millions/year

- High switching costs due to integration and identity needs

Energy and Utility Providers

Energy and utility companies are critical suppliers for Clear Channel Outdoor, powering thousands of digital screens and illuminated boards that consumed an estimated 1.2 TWh in 2024 across the US and Europe.

By 2025 higher utility prices—US industrial electricity up ~9% YoY in 2024—and tighter carbon rules (EU ETS prices ~€85/ton in 2025) have raised suppliers’ bargaining power.

Clear Channel must manage rising bills and invest in on-site solar, batteries, and power‑purchase agreements to cut costs, lower emissions, and meet regulator and supplier demands.

- 2024 est. energy use 1.2 TWh

- US industrial power +9% YoY (2024)

- EU ETS ~€85/ton CO2 (2025)

- Mitigation: solar, batteries, PPAs

Supplier squeeze: panel shortages, rising rents, programmatic growth and energy costs

Suppliers (landlords, LED makers, utilities, municipalities, programmatic vendors) hold elevated bargaining power: urban inventory scarcity cut panel availability ~18% (2021–24) and raised rents ~12% (2024); LED vendors (Samsung, Leyard) concentrated market; programmatic ~38% of OOH transactions (2024); energy use ~1.2 TWh (2024) and US industrial power +9% YoY (2024) squeeze margins.

| Metric | Value |

|---|---|

| Panel availability decline | ~18% (2021–24) |

| Urban rent change | +12% (2024) |

| Programmatic share | 38% (2024) |

| Energy use | 1.2 TWh (2024) |

| US industrial power | +9% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Clear Channel Outdoor that uncovers competitive intensity, buyer and supplier leverage, substitution risks, and barriers to entry—highlighting disruptive threats, regulatory impacts, and strategic levers to defend market share.

A concise, one-sheet Porter's Five Forces for Clear Channel Outdoor that highlights competitive pressures and strategic levers—perfect for fast boardroom decisions or investor briefs.

Customers Bargaining Power

Concentration of Large Advertising Agencies

Availability of Alternative Media Channels

Customers face many alternatives—social media (Meta, TikTok), search (Google), and TV—where global digital ad spend hit $514B in 2023 and was forecast near $570B for 2025, so Clear Channel Outdoor (CCO) competes for portions of that budget.

If CCO raises rates too far, advertisers can shift to digital channels offering granular targeting and measurable ROI; programmatic channels saw 72% of US digital display spend in 2024, showing easy reallocation.

High price elasticity means CCO must keep pricing aligned with digital CPMs (US OOH CPMs averaged $6–12 in 2024 vs. programmatic $2–8), pressuring margins and forcing competitive rate-setting.

Demand for Real-Time Programmatic Flexibility

Increased Expectations for Attribution Data

Modern advertisers demand attribution to prove ROI for outdoor ads; 68% of CMOs in 2024 said measurability drives media spend decisions, so buyers press Clear Channel Outdoor for granular audience analytics, foot‑traffic conversion metrics, and mobile retargeting.

If CCO fails to supply these advanced metrics, clients shift to rivals: digital and programmatic OOH vendors reported a 22% revenue gain in 2023 from offering real‑time measurement.

- 68% of CMOs (2024) value measurability

- 22% revenue gain for measurability-focused OOH vendors (2023)

- Key asks: audience analytics, foot-traffic conversion, mobile retargeting

Low Switching Costs Between Media Owners

In major U.S. markets where Clear Channel Outdoor competes with Lamar Advertising and Outfront, switching a campaign is cheap and fast, so advertisers hold bargaining power; Q3 2025 OOH industry pricing shows spot rates varying +/-15% across providers for similar urban corridors, letting brands shift for price or inventory reasons.

Many billboards cluster on the same high-traffic routes, so advertisers trade based on short-term availability rather than vendor lock-in, keeping Clear Channel’s churn risk elevated when its fill rate drops below local average (usually ~85%).

- Multiple rivals in top 20 DMAs

- Spot rate variance ~15%

- Typical fill rate benchmark ~85%

- Low tech/integration switching cost

Buyer Power Soars: Agencies Drive 70% Spend, Programmatic OOH Fuels Price Pressure

| Metric | Value (year) |

|---|---|

| Agency share of global ad spend | ~70% (2024) |

| CCO programmatic revenue growth | +28% (2024) |

| OOH programmatic share | 46% (2025 proj.) |

| CMOs valuing measurability | 68% (2024) |

| Spot rate variance | ±15% (Q3 2025) |

What You See Is What You Get

Clear Channel Outdoor Porter's Five Forces Analysis

This preview shows the exact Clear Channel Outdoor Porter's Five Forces analysis you'll receive—no placeholders or samples, fully formatted and ready for download immediately after purchase.

The document displayed here is the complete, professionally written file included with your order, so what you see is precisely what you'll get upon payment.