Clearwater Paper PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Clearwater Paper—spot regulatory, economic, and environmental forces reshaping its margins and growth prospects and use these findings to sharpen your investment or strategic plan; purchase the full report for a comprehensive, ready-to-use breakdown and downloadable templates.

Political factors

Trade Policy and Tariffs

Trade tensions and import duties on wood pulp and finished paper can raise Clearwater Paper's input costs and squeeze margins; US pulp import tariffs rose to 8-12% in 2024 on certain suppliers, adding $30–$60/ton to costs. By late 2025, renegotiated North American rules and protectionist measures against foreign tissue boosted domestic tissue share by ~3 percentage points, so strategists must track tariff movements and FX-driven raw-material prices closely.

Federal Forestry Management

Federal forestry management rules on national forests shape Clearwater Paper’s pulp supply: federal lands supply about 20-25% of U.S. industrial roundwood, so shifts in harvest limits directly affect wood-fiber availability and prices; timber volume reductions under conservation policies in 2023–24 contributed to a ~7–12% regional pulpwood price rise. Political turnover since 2021 has driven policy pivots that increase supply volatility and input-cost risk for the paperboard division.

Corporate Taxation Levels

Federal and state corporate tax codes directly affect Clearwater Paper’s net income and capex capacity; after the 2017 TCJA corporate rate fell to 21% federally, but potential changes or state surtaxes (e.g., Washington’s B&O nuances) could shift effective rates and free cash flow. Expiration of manufacturing tax credits would reduce cash available for reinvestment—Clearwater’s 2024 operating cash flow was about $225M, so a 2–5% effective tax increase could cut free cash flow materially, influencing expansion or debt-paydown plans.

Labor Union Relations

Clearwater Paper operates across states with varying union density—e.g., Pacific Northwest mills face stronger unions—impacting wage negotiations and benefits that can alter unit labor costs and capital allocation.

Changes in NLRB composition since 2023 have introduced rulings tightening joint-employer and bargaining standards, increasing compliance costs and potential arbitration cases for Clearwater Paper’s multi-site operations.

- Union wage premium ~11.2% (2024)

- Clearwater Paper 2024 operating margin 6.8%

- Regional union strength varies, Pacific Northwest higher

- NLRB rule shifts since 2023 raise compliance/arbitration risk

Infrastructure Spending

Government investment in rail and highway upgrades is crucial for Clearwater Paper’s heavy tissue and paperboard distribution; USD 120bn in U.S. infrastructure spending authorized by the 2021 Bipartisan Infrastructure Law continues funding projects that can reduce transit times to major retailers.

Legislative focus on logistics improvements can lower per-unit shipping costs—transport accounts for ~10–15% of paperboard COGS—while underfunded infrastructure creates bottlenecks that compress margins and raise inventory carrying costs.

- USD 120bn federal infrastructure funds ongoing (post-2021)

- Transport = ~10–15% of paperboard COGS

- Improved logistics → lower transit times, reduced shipping costs

- Underfunding → supply-chain bottlenecks, margin erosion

Tariffs, union costs and supply cuts squeeze pulp margins as $120B infra eases transport

Political factors: tariffs raised US pulp import duties to 8–12% in 2024, adding $30–$60/ton; federal forests supply ~20–25% of industrial roundwood, 2023–24 conservation cuts pushed regional pulpwood prices up ~7–12%; union wage premium ~11.2% (2024) vs Clearwater operating margin 6.8%; $120bn federal infrastructure funds reduce transport bottlenecks (transport ≈10–15% of COGS).

| Metric | Value |

|---|---|

| Pulp tariffs (2024) | 8–12% (+$30–$60/ton) |

| Federal roundwood share | 20–25% |

| Pulpwood price rise (2023–24) | 7–12% |

| Union premium (2024) | 11.2% |

| Clearwater op. margin (2024) | 6.8% |

| Infra funds | $120bn |

| Transport % of COGS | 10–15% |

What is included in the product

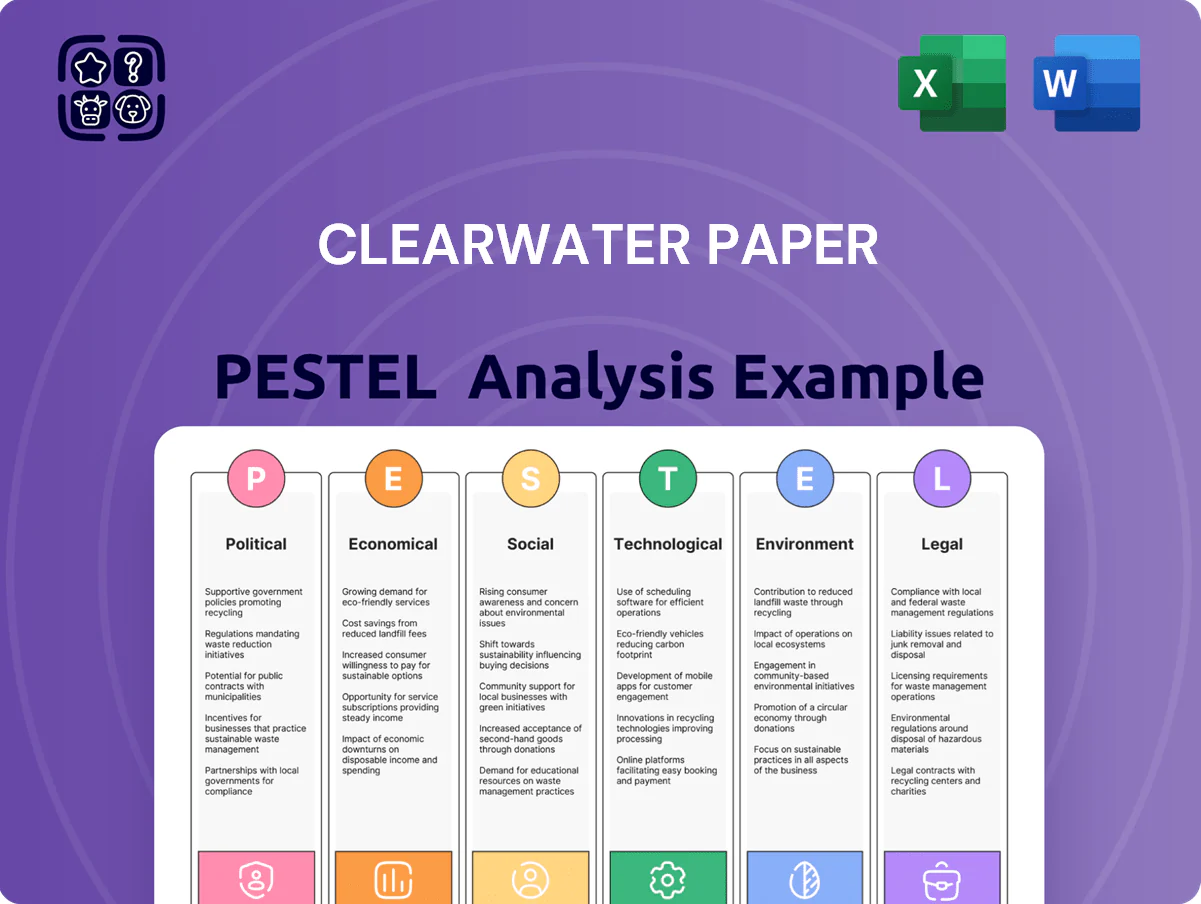

Explores how external macro-environmental factors uniquely affect Clearwater Paper across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each supported by current trends and data to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary tailored for Clearwater Paper that highlights external risks and opportunities by category, ideal for quick insertion into presentations, team briefings, or strategy folders to streamline decision-making and stakeholder alignment.

Economic factors

Consumer Spending Power

As a primary supplier of private-label tissue, Clearwater Paper's revenue closely tracks U.S. household disposable income; U.S. real disposable personal income fell 0.3% year-over-year in 2025 Q3, pressuring premium brand demand. During downturns consumers shift to cheaper private labels, supporting Clearwater—private-label share rose to ~28% of U.S. tissue sales in 2024. Analysts watch inflation (CPI 3.4% in 2024) and 2024 wage growth ~4.2% to model further retail-tier shifts.

Fluctuations in Pulp Prices

The global softwood pulp benchmark averaged about $820/ton in 2025, swinging 28% year-over-year and making pulp the dominant cost driver for Clearwater Paper’s mills; sustained spikes compress EBITDA margins if the company cannot pass costs to retailers via price hikes. Financial analysts model global supply-demand, noting inventories fell to under 30 days' consumption in late 2024, to forecast quarter-to-quarter earnings sensitivity to pulp price swings.

Interest Rate Environment

The cost of borrowing is critical for Clearwater Paper, which faces heavy capex for mill maintenance and tech upgrades; with the US 10-year Treasury averaging about 4.2% in 2025 and the Fed funds rate near 5.0% through mid-2025, debt servicing costs rose materially.

High interest rates in 2025 increased financing costs for sustainability projects; Clearwater Paper’s net debt of roughly $900m–$1.0bn in recent reports means a 100 bp rise adds several million dollars annually in interest expense.

Decision-makers must weigh urgent infrastructure investment against higher capital costs, considering alternatives such as staged investments, refinancing windows, or shifting to less interest-sensitive funding to preserve margins and cash flow.

Energy Cost Volatility

Paper and pulp production is energy-intensive, relying on electricity, natural gas and biomass; Clearwater Paper reported energy costs represented roughly 6–8% of COGS in 2024, with industrial power prices in the US rising ~12% YoY in 2023–24, heightening operating cost volatility.

Significant energy-price swings can make site-level margins unpredictable and affect competitiveness; Clearwater’s ability to generate ~30–40% of site energy from biomass in 2024 provides a partial hedge against external market shocks and reduced exposure to natural gas price spikes.

- Energy costs ~6–8% of COGS (2024)

- US industrial power +12% YoY (2023–24)

- Biomass self-generation ~30–40% of site energy (2024)

Retail Consolidation Trends

The growing consolidation among US retailers—Walmart, Kroger, and Amazon account for over 40% of grocery and household sales in 2024—intensifies buyer power, forcing Clearwater Paper to accept tighter pricing on private label tissue and paperboard packaging.

As top wholesalers expand scale and private-label penetration rose to ~22% of tissue sales in 2024, Clearwater must push productivity; its 2023 operating margin of 6.8% is vulnerable without efficiency gains.

- Retail concentration >40% of market share (2024)

- Private-label tissue penetration ~22% (2024)

- Clearwater Paper operating margin 6.8% (2023)

Clearwater Paper margins squeezed by rising pulp, energy, rates and retailer power

Economic headwinds—softwood pulp volatility (~$820/ton avg 2025, +28% YoY), tighter household disposable income (US real DPI -0.3% YoY 2025 Q3), and higher rates (10y ~4.2%, Fed funds ~5.0% mid‑2025)—compress Clearwater Paper margins; energy costs (6–8% of COGS, US industrial power +12% YoY 2023–24) and retailer consolidation (>40% market share) increase pricing pressure.

| Metric | Value |

|---|---|

| Pulp price (2025 avg) | $820/ton |

| Real DPI (2025 Q3) | -0.3% YoY |

| Fed funds (mid‑2025) | ~5.0% |

| Energy % of COGS (2024) | 6–8% |

| Retail concentration (2024) | >40% |

What You See Is What You Get

Clearwater Paper PESTLE Analysis

The preview shown here is the exact Clearwater Paper PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Clearwater Paper—spot regulatory, economic, and environmental forces reshaping its margins and growth prospects and use these findings to sharpen your investment or strategic plan; purchase the full report for a comprehensive, ready-to-use breakdown and downloadable templates.

Political factors

Trade Policy and Tariffs

Trade tensions and import duties on wood pulp and finished paper can raise Clearwater Paper's input costs and squeeze margins; US pulp import tariffs rose to 8-12% in 2024 on certain suppliers, adding $30–$60/ton to costs. By late 2025, renegotiated North American rules and protectionist measures against foreign tissue boosted domestic tissue share by ~3 percentage points, so strategists must track tariff movements and FX-driven raw-material prices closely.

Federal Forestry Management

Federal forestry management rules on national forests shape Clearwater Paper’s pulp supply: federal lands supply about 20-25% of U.S. industrial roundwood, so shifts in harvest limits directly affect wood-fiber availability and prices; timber volume reductions under conservation policies in 2023–24 contributed to a ~7–12% regional pulpwood price rise. Political turnover since 2021 has driven policy pivots that increase supply volatility and input-cost risk for the paperboard division.

Corporate Taxation Levels

Federal and state corporate tax codes directly affect Clearwater Paper’s net income and capex capacity; after the 2017 TCJA corporate rate fell to 21% federally, but potential changes or state surtaxes (e.g., Washington’s B&O nuances) could shift effective rates and free cash flow. Expiration of manufacturing tax credits would reduce cash available for reinvestment—Clearwater’s 2024 operating cash flow was about $225M, so a 2–5% effective tax increase could cut free cash flow materially, influencing expansion or debt-paydown plans.

Labor Union Relations

Clearwater Paper operates across states with varying union density—e.g., Pacific Northwest mills face stronger unions—impacting wage negotiations and benefits that can alter unit labor costs and capital allocation.

Changes in NLRB composition since 2023 have introduced rulings tightening joint-employer and bargaining standards, increasing compliance costs and potential arbitration cases for Clearwater Paper’s multi-site operations.

- Union wage premium ~11.2% (2024)

- Clearwater Paper 2024 operating margin 6.8%

- Regional union strength varies, Pacific Northwest higher

- NLRB rule shifts since 2023 raise compliance/arbitration risk

Infrastructure Spending

Government investment in rail and highway upgrades is crucial for Clearwater Paper’s heavy tissue and paperboard distribution; USD 120bn in U.S. infrastructure spending authorized by the 2021 Bipartisan Infrastructure Law continues funding projects that can reduce transit times to major retailers.

Legislative focus on logistics improvements can lower per-unit shipping costs—transport accounts for ~10–15% of paperboard COGS—while underfunded infrastructure creates bottlenecks that compress margins and raise inventory carrying costs.

- USD 120bn federal infrastructure funds ongoing (post-2021)

- Transport = ~10–15% of paperboard COGS

- Improved logistics → lower transit times, reduced shipping costs

- Underfunding → supply-chain bottlenecks, margin erosion

Tariffs, union costs and supply cuts squeeze pulp margins as $120B infra eases transport

Political factors: tariffs raised US pulp import duties to 8–12% in 2024, adding $30–$60/ton; federal forests supply ~20–25% of industrial roundwood, 2023–24 conservation cuts pushed regional pulpwood prices up ~7–12%; union wage premium ~11.2% (2024) vs Clearwater operating margin 6.8%; $120bn federal infrastructure funds reduce transport bottlenecks (transport ≈10–15% of COGS).

| Metric | Value |

|---|---|

| Pulp tariffs (2024) | 8–12% (+$30–$60/ton) |

| Federal roundwood share | 20–25% |

| Pulpwood price rise (2023–24) | 7–12% |

| Union premium (2024) | 11.2% |

| Clearwater op. margin (2024) | 6.8% |

| Infra funds | $120bn |

| Transport % of COGS | 10–15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Clearwater Paper across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each supported by current trends and data to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary tailored for Clearwater Paper that highlights external risks and opportunities by category, ideal for quick insertion into presentations, team briefings, or strategy folders to streamline decision-making and stakeholder alignment.

Economic factors

Consumer Spending Power

As a primary supplier of private-label tissue, Clearwater Paper's revenue closely tracks U.S. household disposable income; U.S. real disposable personal income fell 0.3% year-over-year in 2025 Q3, pressuring premium brand demand. During downturns consumers shift to cheaper private labels, supporting Clearwater—private-label share rose to ~28% of U.S. tissue sales in 2024. Analysts watch inflation (CPI 3.4% in 2024) and 2024 wage growth ~4.2% to model further retail-tier shifts.

Fluctuations in Pulp Prices

The global softwood pulp benchmark averaged about $820/ton in 2025, swinging 28% year-over-year and making pulp the dominant cost driver for Clearwater Paper’s mills; sustained spikes compress EBITDA margins if the company cannot pass costs to retailers via price hikes. Financial analysts model global supply-demand, noting inventories fell to under 30 days' consumption in late 2024, to forecast quarter-to-quarter earnings sensitivity to pulp price swings.

Interest Rate Environment

The cost of borrowing is critical for Clearwater Paper, which faces heavy capex for mill maintenance and tech upgrades; with the US 10-year Treasury averaging about 4.2% in 2025 and the Fed funds rate near 5.0% through mid-2025, debt servicing costs rose materially.

High interest rates in 2025 increased financing costs for sustainability projects; Clearwater Paper’s net debt of roughly $900m–$1.0bn in recent reports means a 100 bp rise adds several million dollars annually in interest expense.

Decision-makers must weigh urgent infrastructure investment against higher capital costs, considering alternatives such as staged investments, refinancing windows, or shifting to less interest-sensitive funding to preserve margins and cash flow.

Energy Cost Volatility

Paper and pulp production is energy-intensive, relying on electricity, natural gas and biomass; Clearwater Paper reported energy costs represented roughly 6–8% of COGS in 2024, with industrial power prices in the US rising ~12% YoY in 2023–24, heightening operating cost volatility.

Significant energy-price swings can make site-level margins unpredictable and affect competitiveness; Clearwater’s ability to generate ~30–40% of site energy from biomass in 2024 provides a partial hedge against external market shocks and reduced exposure to natural gas price spikes.

- Energy costs ~6–8% of COGS (2024)

- US industrial power +12% YoY (2023–24)

- Biomass self-generation ~30–40% of site energy (2024)

Retail Consolidation Trends

The growing consolidation among US retailers—Walmart, Kroger, and Amazon account for over 40% of grocery and household sales in 2024—intensifies buyer power, forcing Clearwater Paper to accept tighter pricing on private label tissue and paperboard packaging.

As top wholesalers expand scale and private-label penetration rose to ~22% of tissue sales in 2024, Clearwater must push productivity; its 2023 operating margin of 6.8% is vulnerable without efficiency gains.

- Retail concentration >40% of market share (2024)

- Private-label tissue penetration ~22% (2024)

- Clearwater Paper operating margin 6.8% (2023)

Clearwater Paper margins squeezed by rising pulp, energy, rates and retailer power

Economic headwinds—softwood pulp volatility (~$820/ton avg 2025, +28% YoY), tighter household disposable income (US real DPI -0.3% YoY 2025 Q3), and higher rates (10y ~4.2%, Fed funds ~5.0% mid‑2025)—compress Clearwater Paper margins; energy costs (6–8% of COGS, US industrial power +12% YoY 2023–24) and retailer consolidation (>40% market share) increase pricing pressure.

| Metric | Value |

|---|---|

| Pulp price (2025 avg) | $820/ton |

| Real DPI (2025 Q3) | -0.3% YoY |

| Fed funds (mid‑2025) | ~5.0% |

| Energy % of COGS (2024) | 6–8% |

| Retail concentration (2024) | >40% |

What You See Is What You Get

Clearwater Paper PESTLE Analysis

The preview shown here is the exact Clearwater Paper PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.