CapitaMall Trust Business Model Canvas

CapitaMall Trust BMC: How the REIT Captures Value in Retail Markets

Unlock the full strategic blueprint behind CapitaMall Trust’s business model—this concise Business Model Canvas maps customer segments, revenue streams, key partnerships, and cost drivers to reveal how the REIT creates and captures value in competitive retail markets.

Partnerships

Strategic Sponsorship with CapitaLand Investment

CICT’s sponsor CapitaLand Investment Limited supplies a steady pipeline of premium assets and operational know-how, having contributed to CICT’s S$5.9bn asset base (2025 pro forma) and enabling three acquisitions totalling ~S$1.2bn in 2024–25.

Banking and Financial Institutions

The REIT works with local and international banks to access diverse funding—including a S$350m green loan and S$500m sustainability-linked bond issued in 2024—supporting a strong balance sheet and lowering average cost of debt (3.1% in 2024).

These lender ties enable interest-rate hedging (55% fixed/hedged as of Dec 2024) and provide liquidity for capital recycling and acquisitions, backing CICT’s S$1.2bn acquisition capacity in stressed markets.

Joint Venture Partners

Government and Regulatory Bodies

CICT works with agencies like the Urban Redevelopment Authority and Building and Construction Authority to secure zoning approvals, permits, and meet 2025 green-build standards; in 2024 CICT reported S$2.3bn assets under management requiring ongoing compliance and periodic asset enhancement works.

- Ensures zoning and redevelopment approvals

- Facilitates permits for S$100m+ capex projects (example 2023–24)

- Aligns AEI (asset enhancement initiatives) with national urban plans

- Maintains compliance with evolving environmental codes

Property and Facility Service Providers

The REIT hires specialized property and facility service firms to run security, cleaning, and technical maintenance across its S$9.3bn portfolio (CICT market cap ~S$5.1bn as of Dec 31, 2025), keeping uptime high and tenant satisfaction steady.

Outsourcing cuts operating costs—management fee ratio held ~10.8% in FY2024—and lets CICT focus on leasing and asset rotation while preserving service quality.

- Portfolio value: S$9.3bn (2025)

- Market cap: ~S$5.1bn (Dec 31, 2025)

- Management fee ratio: ~10.8% (FY2024)

CICT scales to S$5.9bn with green finance, 55% hedged debt and 3.1% funding cost

CICT leverages CapitaLand Investment Limited for asset pipeline and know‑how (S$5.9bn assets pro forma, 2025) and works with banks and capital partners to secure funding—S$350m green loan, S$500m sustainability bond (2024); 55% fixed/hedged debt; 3.1% avg cost (2024)—while outsourcing operations to reduce costs (management fee ~10.8% FY2024).

| Metric | Value |

|---|---|

| Pro forma assets (2025) | S$5.9bn |

| Portfolio value (2025) | S$9.3bn |

| Green loan (2024) | S$350m |

| Sustainability bond (2024) | S$500m |

| Avg cost of debt (2024) | 3.1% |

| Hedged/fixed debt (Dec 2024) | 55% |

| Management fee ratio (FY2024) | 10.8% |

What is included in the product

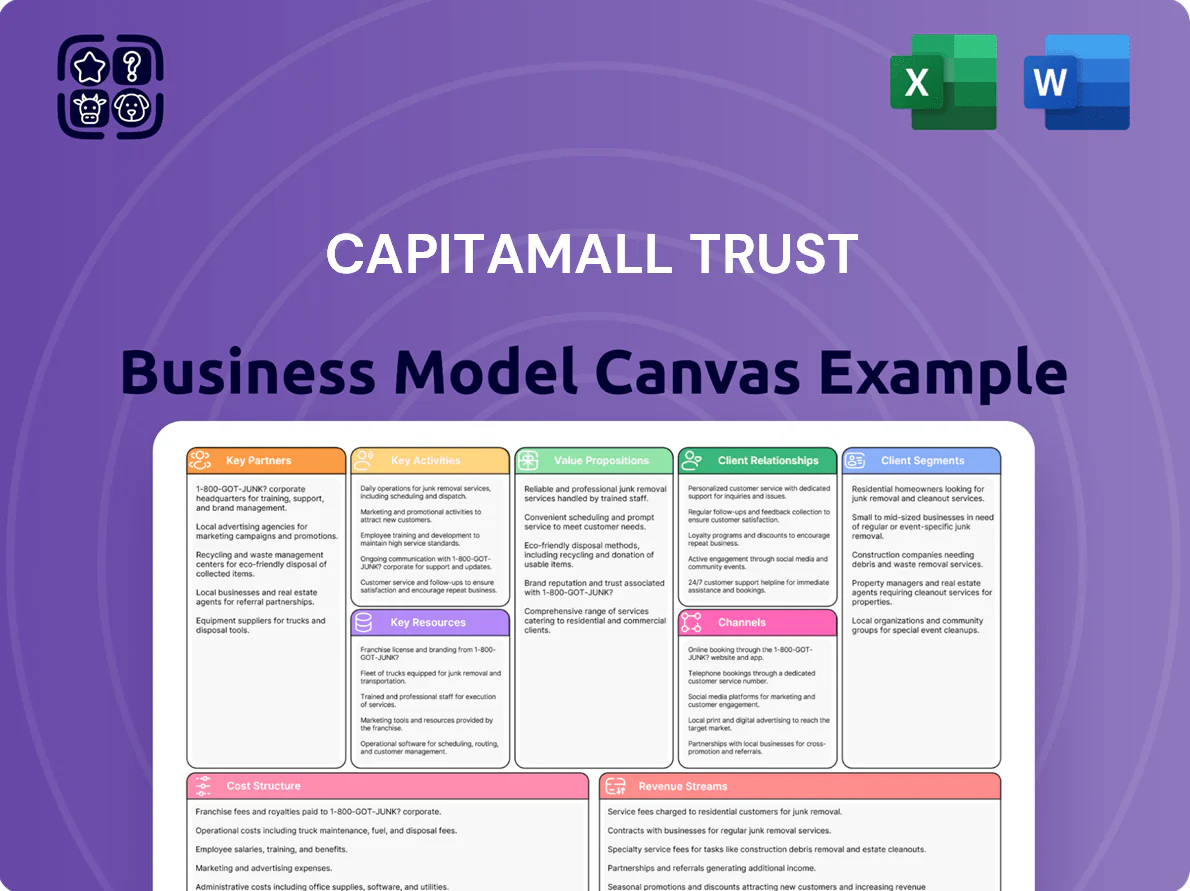

A concise Business Model Canvas for CapitaMall Trust outlining its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting mall-centric REIT operations, tenant mix strategies, asset management, and income-generation for investors.

High-level view of CapitaMall Trust’s mall-focused business model with editable cells to quickly pinpoint revenue drivers, tenant mix challenges, and footfall strategies for boardroom-ready planning.

Activities

Active Asset Management

Strategic Acquisitions and Divestments

CICT (CapitaLand Integrated Commercial Trust) actively recycles capital by divesting non-core malls and buying high-potential assets; in 2024 it divested five suburban assets for S$450m and acquired a mixed-use integrated development for S$320m, freeing liquidity to lift portfolio yield.

Asset Enhancement Initiatives

CICT runs Asset Enhancement Initiatives (AEIs) — from facade refreshes to full redevelopments — to raise net lettable area (NLA) and cut energy use; recent AEIs (e.g., 2023 VivoCity precinct works) boosted NLA by ~3–5% and helped lift portfolio rent reversion to +2.8% in FY2024.

Prudent Capital Management

Management monitors CapitaLand Mall Trust’s debt maturity and gearing (36.8% LTV as of 31 Dec 2025) to keep stability and flexibility, issuing equity or SGD-denominated bonds when markets are favourable and hedging interest-rate exposure with swaps and caps.

Effective capital management preserves dry powder for acquisitions and asset enhancements, reducing volatility risk and supporting growth—e.g., S$200m standby facilities and S$500m undrawn revolver as of Dec 2025.

- Debt-to-equity: LTV 36.8% (31 Dec 2025)

- Liquidity: S$200m standby + S$500m undrawn revolver

- Instruments: equity placements, SGD bonds, interest-rate swaps/caps

Sustainability and ESG Integration

CICT embeds ESG across operations, cutting carbon via LED retrofits, solar and BMS (building management systems) to target a 30% energy intensity reduction by 2028 and net-zero scope 1–2 ambition by 2050.

CICT runs community programs and governance upgrades to boost sustainability ratings, helping attract institutional investors—ESG-aligned funds now hold ~25% of Singapore REIT flows—and reducing operating costs by an estimated 8–12% from efficiency measures.

- Target: 30% energy intensity cut by 2028

- Net-zero scope 1–2 by 2050

- Measures: LED, solar, BMS

- ESG-aligned capital ≈25% of SG REIT flows

- Estimated OpEx savings 8–12%

Solid fundamentals: S$8.3bn AUM, S$1.23 NAV, 96.8% occupancy, 36.8% LTV

| Metric | Value |

|---|---|

| AUM | S$8.3bn |

| NAV/unit | S$1.23 (FY2024) |

| Occupancy | 96.8% (FY2024) |

| Rent reversion | +2.8% (FY2024) |

| LTV | 36.8% (31 Dec 2025) |

| Liquidity | S$700m (S$200m standby + S$500m revolver) |

| AEI NLA uplift | +3–5% (VivoCity 2023) |

| ESG target | ‑30% energy intensity by 2028 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the authentic CapitaMall Trust Business Model Canvas—not a mockup—and it is the exact file you will receive upon purchase.

When you complete your order, you’ll get the full, editable document in Word and Excel formats, structured and formatted just as shown here.

No extras or placeholders—what you see is the complete deliverable, ready for use in analysis, presentations, or editing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

CapitaMall Trust BMC: How the REIT Captures Value in Retail Markets

Unlock the full strategic blueprint behind CapitaMall Trust’s business model—this concise Business Model Canvas maps customer segments, revenue streams, key partnerships, and cost drivers to reveal how the REIT creates and captures value in competitive retail markets.

Partnerships

Strategic Sponsorship with CapitaLand Investment

CICT’s sponsor CapitaLand Investment Limited supplies a steady pipeline of premium assets and operational know-how, having contributed to CICT’s S$5.9bn asset base (2025 pro forma) and enabling three acquisitions totalling ~S$1.2bn in 2024–25.

Banking and Financial Institutions

The REIT works with local and international banks to access diverse funding—including a S$350m green loan and S$500m sustainability-linked bond issued in 2024—supporting a strong balance sheet and lowering average cost of debt (3.1% in 2024).

These lender ties enable interest-rate hedging (55% fixed/hedged as of Dec 2024) and provide liquidity for capital recycling and acquisitions, backing CICT’s S$1.2bn acquisition capacity in stressed markets.

Joint Venture Partners

Government and Regulatory Bodies

CICT works with agencies like the Urban Redevelopment Authority and Building and Construction Authority to secure zoning approvals, permits, and meet 2025 green-build standards; in 2024 CICT reported S$2.3bn assets under management requiring ongoing compliance and periodic asset enhancement works.

- Ensures zoning and redevelopment approvals

- Facilitates permits for S$100m+ capex projects (example 2023–24)

- Aligns AEI (asset enhancement initiatives) with national urban plans

- Maintains compliance with evolving environmental codes

Property and Facility Service Providers

The REIT hires specialized property and facility service firms to run security, cleaning, and technical maintenance across its S$9.3bn portfolio (CICT market cap ~S$5.1bn as of Dec 31, 2025), keeping uptime high and tenant satisfaction steady.

Outsourcing cuts operating costs—management fee ratio held ~10.8% in FY2024—and lets CICT focus on leasing and asset rotation while preserving service quality.

- Portfolio value: S$9.3bn (2025)

- Market cap: ~S$5.1bn (Dec 31, 2025)

- Management fee ratio: ~10.8% (FY2024)

CICT scales to S$5.9bn with green finance, 55% hedged debt and 3.1% funding cost

CICT leverages CapitaLand Investment Limited for asset pipeline and know‑how (S$5.9bn assets pro forma, 2025) and works with banks and capital partners to secure funding—S$350m green loan, S$500m sustainability bond (2024); 55% fixed/hedged debt; 3.1% avg cost (2024)—while outsourcing operations to reduce costs (management fee ~10.8% FY2024).

| Metric | Value |

|---|---|

| Pro forma assets (2025) | S$5.9bn |

| Portfolio value (2025) | S$9.3bn |

| Green loan (2024) | S$350m |

| Sustainability bond (2024) | S$500m |

| Avg cost of debt (2024) | 3.1% |

| Hedged/fixed debt (Dec 2024) | 55% |

| Management fee ratio (FY2024) | 10.8% |

What is included in the product

A concise Business Model Canvas for CapitaMall Trust outlining its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting mall-centric REIT operations, tenant mix strategies, asset management, and income-generation for investors.

High-level view of CapitaMall Trust’s mall-focused business model with editable cells to quickly pinpoint revenue drivers, tenant mix challenges, and footfall strategies for boardroom-ready planning.

Activities

Active Asset Management

Strategic Acquisitions and Divestments

CICT (CapitaLand Integrated Commercial Trust) actively recycles capital by divesting non-core malls and buying high-potential assets; in 2024 it divested five suburban assets for S$450m and acquired a mixed-use integrated development for S$320m, freeing liquidity to lift portfolio yield.

Asset Enhancement Initiatives

CICT runs Asset Enhancement Initiatives (AEIs) — from facade refreshes to full redevelopments — to raise net lettable area (NLA) and cut energy use; recent AEIs (e.g., 2023 VivoCity precinct works) boosted NLA by ~3–5% and helped lift portfolio rent reversion to +2.8% in FY2024.

Prudent Capital Management

Management monitors CapitaLand Mall Trust’s debt maturity and gearing (36.8% LTV as of 31 Dec 2025) to keep stability and flexibility, issuing equity or SGD-denominated bonds when markets are favourable and hedging interest-rate exposure with swaps and caps.

Effective capital management preserves dry powder for acquisitions and asset enhancements, reducing volatility risk and supporting growth—e.g., S$200m standby facilities and S$500m undrawn revolver as of Dec 2025.

- Debt-to-equity: LTV 36.8% (31 Dec 2025)

- Liquidity: S$200m standby + S$500m undrawn revolver

- Instruments: equity placements, SGD bonds, interest-rate swaps/caps

Sustainability and ESG Integration

CICT embeds ESG across operations, cutting carbon via LED retrofits, solar and BMS (building management systems) to target a 30% energy intensity reduction by 2028 and net-zero scope 1–2 ambition by 2050.

CICT runs community programs and governance upgrades to boost sustainability ratings, helping attract institutional investors—ESG-aligned funds now hold ~25% of Singapore REIT flows—and reducing operating costs by an estimated 8–12% from efficiency measures.

- Target: 30% energy intensity cut by 2028

- Net-zero scope 1–2 by 2050

- Measures: LED, solar, BMS

- ESG-aligned capital ≈25% of SG REIT flows

- Estimated OpEx savings 8–12%

Solid fundamentals: S$8.3bn AUM, S$1.23 NAV, 96.8% occupancy, 36.8% LTV

| Metric | Value |

|---|---|

| AUM | S$8.3bn |

| NAV/unit | S$1.23 (FY2024) |

| Occupancy | 96.8% (FY2024) |

| Rent reversion | +2.8% (FY2024) |

| LTV | 36.8% (31 Dec 2025) |

| Liquidity | S$700m (S$200m standby + S$500m revolver) |

| AEI NLA uplift | +3–5% (VivoCity 2023) |

| ESG target | ‑30% energy intensity by 2028 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the authentic CapitaMall Trust Business Model Canvas—not a mockup—and it is the exact file you will receive upon purchase.

When you complete your order, you’ll get the full, editable document in Word and Excel formats, structured and formatted just as shown here.

No extras or placeholders—what you see is the complete deliverable, ready for use in analysis, presentations, or editing.