CapitaMall Trust SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

CapitaLand Mall Trust shows resilient retail assets and strong tenant mix, yet faces rental pressure from shifting consumer patterns and e‑commerce—our full SWOT unpacks these dynamics with financial metrics and scenario analysis. Discover strategic opportunities, risks, and portfolio-level recommendations to inform investment or advisory decisions; purchase the complete, editable SWOT report (Word + Excel) to plan with confidence.

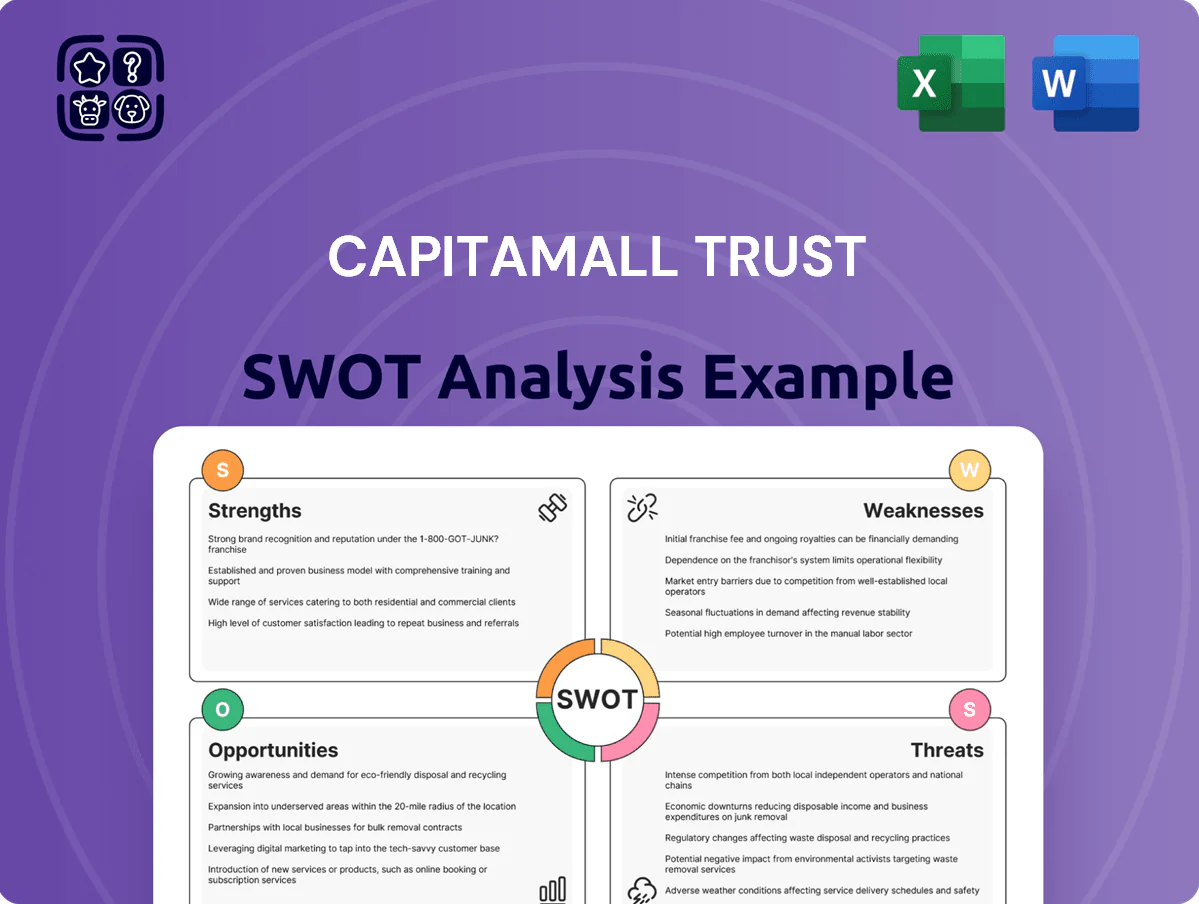

Strengths

Dominant Singapore Market Position

CICT is Singapore’s largest REIT by market cap—about SGD 11.5bn as of Dec 31, 2025—giving it scale to shape rent benchmarks across prime and suburban malls.

That scale helps secure high-quality tenants like NTUC, Uniqlo and Uniqlo-owner Fast Retailing, and supports average portfolio occupancy near 97% in 2025.

CICT’s control of ~15% of islandwide retail GFA keeps it a cornerstone of Singapore’s commercial landscape and strengthens lease negotiation leverage.

Diversified Integrated Development Portfolio

CapitaLand Mall Trust manages integrated mixed-use assets like Raffles City and Funan that combine retail, office and hospitality, creating steady cross‑traffic and higher tenant retention; Funan recorded ~10.8 million annual mall visits in 2023 and Raffles City Singapore reported retail occupancy >99% in FY2024. This diversification cushions rental volatility across sectors and supported CMT’s portfolio occupancy of 97.2% and distributable income growth of 2.5% in FY2024.

Strong Sponsor Support from CapitaLand

Being sponsored by CapitaLand Investment (CLI) gives CapitaMall Trust access to CLI’s pipeline—CLI had S$2.6bn of Singapore retail assets under active recycling in 2024—plus professional property management and development expertise, enabling steady acquisition flow and funding for large redevelopments (CICT raised S$500m in 2023–24 equity/debt support). This institutional backing boosts investor confidence and cushions volatility, lowering perceived execution and refinancing risk.

High Portfolio Occupancy and Retention

Throughout 2025, CICT sustained portfolio occupancy of about 98.5%, driven by high demand for its prime suburban malls and urban nodes.

Proactive asset management—frequent tenant engagement, staggered lease renewals, and rapid space fit-outs—kept retention above 92% and transition downtime under 30 days.

This operational efficiency reflects asset quality and a leasing team that preserved gross rental income and limited vacancy loss to under 1.5% of revenue.

- Occupancy ~98.5%

- Retention >92%

- Avg downtime <30 days

- Vacancy loss <1.5% of revenue

Robust Capital Management Framework

CICT maintains a disciplined balance sheet with a 4.1 years weighted average debt maturity and gearing ~35% as at 31 Dec 2025, supporting liquidity and flexibility.

The trust tapped diverse funding channels—S$500m green bonds (2024) and S$400m perpetual securities—to lower average cost of debt and preserve headroom for M&A or AEI without overleveraging.

CICT: SGD11.5bn retail anchor—98.5% occupancy, >92% retention, disciplined balance sheet

CICT’s scale (Mkt cap ~SGD11.5bn, 15% island retail GFA) anchors high occupancy (~98.5% in 2025), strong tenant mix (NTUC, Uniqlo), retention >92% and low vacancy loss <1.5%; disciplined balance sheet (gearing ~35%, WADM 4.1 yrs) and CLI sponsorship (S$500m green bonds, S$400m perpetuals) support acquisitions and AEI.

| Metric | Value |

|---|---|

| Market cap | SGD11.5bn (Dec 31, 2025) |

| Occupancy | ~98.5% (2025) |

| Retention | >92% |

| Gearing | ~35% |

What is included in the product

Delivers a strategic overview of CapitaMall Trust’s internal strengths and weaknesses alongside external opportunities and threats, mapping its competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise CapitaMall Trust SWOT matrix for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

High Geographic Concentration in Singapore

Despite a 2021 acquisition in Germany, about 95% of CapitaLand Integrated Commercial Trusts (CICT) gross rental income and 92% of assets by value remained in Singapore as of FY2024, leaving the portfolio highly concentrated in one city-state.

This limited geographic diversification raises material exposure to Singapore GDP swings—retail sales fell 3.8% y/y in Q3 2024—and to policy shifts.

A sudden rise in property tax or a change to land use rules could cut distributable income significantly; for example, a 100 basis-point increase in effective property tax could reduce NPI by an estimated 4–6% based on FY2024 margins.

Sensitivity to Interest Rate Fluctuations

As a REIT, CapitaMall Trust (CICT) is highly sensitive to interest rates; a 100bp rise typically increases financing costs and can lower market yield appeal—CICT’s weighted average cost of debt was 2.8% in FY2024, with hedges covering about 70% of exposure. Prolonged high rates would raise unhedged borrowing costs and squeeze distributable income; after the 2022–2023 rate cycle, many Singapore retail REITs saw DPU pressure of 3–8%. Investors seeking stable yields view this sensitivity as a key risk amid uncertain global monetary policy.

Exposure to Overseas Operational Risks

CapitaLand Mall Trust’s push into Germany’s office sector adds FX risk: EUR/SGD volatility swung ~8% in 2023–2024, which can erode distributable income from €420m of overseas assets reported in FY2024.

Operating in Germany brings regulatory and compliance complexity and needs local asset management expertise the trust lacks, raising operating cost and execution risk.

Geopolitical exposure and different office-use trends—German office vacancies hit ~6.5% in 2024 versus Singapore’s ~2.8%—could compress rents and lower yields.

High Capital Expenditure for Maintenance

Maintaining premium status of CapitaMall Trust’s flagship malls needs heavy, ongoing capex for asset enhancements; Singapore-listed CMT spent S$120m on AEI (asset enhancement initiatives) in FY2024, reflecting this push.

As properties age, upgrades to meet 2030 ESG targets and tenant expectations raise costs, pressuring cash flow and possibly reducing distributable income if unchecked.

- FY2024 AEI S$120m

- ESG retrofit costs up to 5–8% of asset value

- Short-term liquidity may tighten

Structural Shifts in Office Demand

The rise of hybrid work cuts demand for traditional offices in CapitaLand Integrated Commercial Trust (CICT), where office assets made up about 28% of portfolio value as of 2025; reduced footprints by corporates raise vacancy risk and pressure rental growth.

Premium offices still attract tenants, but longer vacancy periods or rental concessions are likelier—CICT reported 12-month rolling office occupancy dipped to ~89% in 2024 versus 94% in 2019.

Converting large offices to flexible or coworking formats needs capex and repositioning, which may compress yields short-term and require strategic pivoting.

- 28% portfolio exposure to offices (2025)

- Occupancy fell to ~89% (2024)

- Conversion capex required—short-term yield pressure

High Singapore concentration, retail softness & rate/FX risks threaten DPU; Germany office drag

High Singapore concentration (~92% assets FY2024) and retail sensitivity (retail sales -3.8% y/y Q3 2024) raise GDP/policy risk; interest-rate exposure (WACD 2.8% FY2024, 70% hedged) and FX swings (~8% EUR/SGD 2023–24) threaten DPU; Germany office move adds vacancy/repositioning risk (office 28% portfolio 2025; occupancy ~89% 2024) and capex/ESG costs (AEI S$120m FY2024).

| Metric | Value |

|---|---|

| Assets in SG | ~92% (FY2024) |

| Retail sales Q3 2024 | -3.8% y/y |

| WACD | 2.8% (FY2024) |

| Hedged | ~70% |

| EUR/SGD vol | ~8% (2023–24) |

| Office share | 28% (2025) |

| Office occ | ~89% (2024) |

| AEI | S$120m (FY2024) |

Same Document Delivered

CapitaMall Trust SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

CapitaLand Mall Trust shows resilient retail assets and strong tenant mix, yet faces rental pressure from shifting consumer patterns and e‑commerce—our full SWOT unpacks these dynamics with financial metrics and scenario analysis. Discover strategic opportunities, risks, and portfolio-level recommendations to inform investment or advisory decisions; purchase the complete, editable SWOT report (Word + Excel) to plan with confidence.

Strengths

Dominant Singapore Market Position

CICT is Singapore’s largest REIT by market cap—about SGD 11.5bn as of Dec 31, 2025—giving it scale to shape rent benchmarks across prime and suburban malls.

That scale helps secure high-quality tenants like NTUC, Uniqlo and Uniqlo-owner Fast Retailing, and supports average portfolio occupancy near 97% in 2025.

CICT’s control of ~15% of islandwide retail GFA keeps it a cornerstone of Singapore’s commercial landscape and strengthens lease negotiation leverage.

Diversified Integrated Development Portfolio

CapitaLand Mall Trust manages integrated mixed-use assets like Raffles City and Funan that combine retail, office and hospitality, creating steady cross‑traffic and higher tenant retention; Funan recorded ~10.8 million annual mall visits in 2023 and Raffles City Singapore reported retail occupancy >99% in FY2024. This diversification cushions rental volatility across sectors and supported CMT’s portfolio occupancy of 97.2% and distributable income growth of 2.5% in FY2024.

Strong Sponsor Support from CapitaLand

Being sponsored by CapitaLand Investment (CLI) gives CapitaMall Trust access to CLI’s pipeline—CLI had S$2.6bn of Singapore retail assets under active recycling in 2024—plus professional property management and development expertise, enabling steady acquisition flow and funding for large redevelopments (CICT raised S$500m in 2023–24 equity/debt support). This institutional backing boosts investor confidence and cushions volatility, lowering perceived execution and refinancing risk.

High Portfolio Occupancy and Retention

Throughout 2025, CICT sustained portfolio occupancy of about 98.5%, driven by high demand for its prime suburban malls and urban nodes.

Proactive asset management—frequent tenant engagement, staggered lease renewals, and rapid space fit-outs—kept retention above 92% and transition downtime under 30 days.

This operational efficiency reflects asset quality and a leasing team that preserved gross rental income and limited vacancy loss to under 1.5% of revenue.

- Occupancy ~98.5%

- Retention >92%

- Avg downtime <30 days

- Vacancy loss <1.5% of revenue

Robust Capital Management Framework

CICT maintains a disciplined balance sheet with a 4.1 years weighted average debt maturity and gearing ~35% as at 31 Dec 2025, supporting liquidity and flexibility.

The trust tapped diverse funding channels—S$500m green bonds (2024) and S$400m perpetual securities—to lower average cost of debt and preserve headroom for M&A or AEI without overleveraging.

CICT: SGD11.5bn retail anchor—98.5% occupancy, >92% retention, disciplined balance sheet

CICT’s scale (Mkt cap ~SGD11.5bn, 15% island retail GFA) anchors high occupancy (~98.5% in 2025), strong tenant mix (NTUC, Uniqlo), retention >92% and low vacancy loss <1.5%; disciplined balance sheet (gearing ~35%, WADM 4.1 yrs) and CLI sponsorship (S$500m green bonds, S$400m perpetuals) support acquisitions and AEI.

| Metric | Value |

|---|---|

| Market cap | SGD11.5bn (Dec 31, 2025) |

| Occupancy | ~98.5% (2025) |

| Retention | >92% |

| Gearing | ~35% |

What is included in the product

Delivers a strategic overview of CapitaMall Trust’s internal strengths and weaknesses alongside external opportunities and threats, mapping its competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a concise CapitaMall Trust SWOT matrix for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

High Geographic Concentration in Singapore

Despite a 2021 acquisition in Germany, about 95% of CapitaLand Integrated Commercial Trusts (CICT) gross rental income and 92% of assets by value remained in Singapore as of FY2024, leaving the portfolio highly concentrated in one city-state.

This limited geographic diversification raises material exposure to Singapore GDP swings—retail sales fell 3.8% y/y in Q3 2024—and to policy shifts.

A sudden rise in property tax or a change to land use rules could cut distributable income significantly; for example, a 100 basis-point increase in effective property tax could reduce NPI by an estimated 4–6% based on FY2024 margins.

Sensitivity to Interest Rate Fluctuations

As a REIT, CapitaMall Trust (CICT) is highly sensitive to interest rates; a 100bp rise typically increases financing costs and can lower market yield appeal—CICT’s weighted average cost of debt was 2.8% in FY2024, with hedges covering about 70% of exposure. Prolonged high rates would raise unhedged borrowing costs and squeeze distributable income; after the 2022–2023 rate cycle, many Singapore retail REITs saw DPU pressure of 3–8%. Investors seeking stable yields view this sensitivity as a key risk amid uncertain global monetary policy.

Exposure to Overseas Operational Risks

CapitaLand Mall Trust’s push into Germany’s office sector adds FX risk: EUR/SGD volatility swung ~8% in 2023–2024, which can erode distributable income from €420m of overseas assets reported in FY2024.

Operating in Germany brings regulatory and compliance complexity and needs local asset management expertise the trust lacks, raising operating cost and execution risk.

Geopolitical exposure and different office-use trends—German office vacancies hit ~6.5% in 2024 versus Singapore’s ~2.8%—could compress rents and lower yields.

High Capital Expenditure for Maintenance

Maintaining premium status of CapitaMall Trust’s flagship malls needs heavy, ongoing capex for asset enhancements; Singapore-listed CMT spent S$120m on AEI (asset enhancement initiatives) in FY2024, reflecting this push.

As properties age, upgrades to meet 2030 ESG targets and tenant expectations raise costs, pressuring cash flow and possibly reducing distributable income if unchecked.

- FY2024 AEI S$120m

- ESG retrofit costs up to 5–8% of asset value

- Short-term liquidity may tighten

Structural Shifts in Office Demand

The rise of hybrid work cuts demand for traditional offices in CapitaLand Integrated Commercial Trust (CICT), where office assets made up about 28% of portfolio value as of 2025; reduced footprints by corporates raise vacancy risk and pressure rental growth.

Premium offices still attract tenants, but longer vacancy periods or rental concessions are likelier—CICT reported 12-month rolling office occupancy dipped to ~89% in 2024 versus 94% in 2019.

Converting large offices to flexible or coworking formats needs capex and repositioning, which may compress yields short-term and require strategic pivoting.

- 28% portfolio exposure to offices (2025)

- Occupancy fell to ~89% (2024)

- Conversion capex required—short-term yield pressure

High Singapore concentration, retail softness & rate/FX risks threaten DPU; Germany office drag

High Singapore concentration (~92% assets FY2024) and retail sensitivity (retail sales -3.8% y/y Q3 2024) raise GDP/policy risk; interest-rate exposure (WACD 2.8% FY2024, 70% hedged) and FX swings (~8% EUR/SGD 2023–24) threaten DPU; Germany office move adds vacancy/repositioning risk (office 28% portfolio 2025; occupancy ~89% 2024) and capex/ESG costs (AEI S$120m FY2024).

| Metric | Value |

|---|---|

| Assets in SG | ~92% (FY2024) |

| Retail sales Q3 2024 | -3.8% y/y |

| WACD | 2.8% (FY2024) |

| Hedged | ~70% |

| EUR/SGD vol | ~8% (2023–24) |

| Office share | 28% (2025) |

| Office occ | ~89% (2024) |

| AEI | S$120m (FY2024) |

Same Document Delivered

CapitaMall Trust SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.