Climb Global Solutions Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

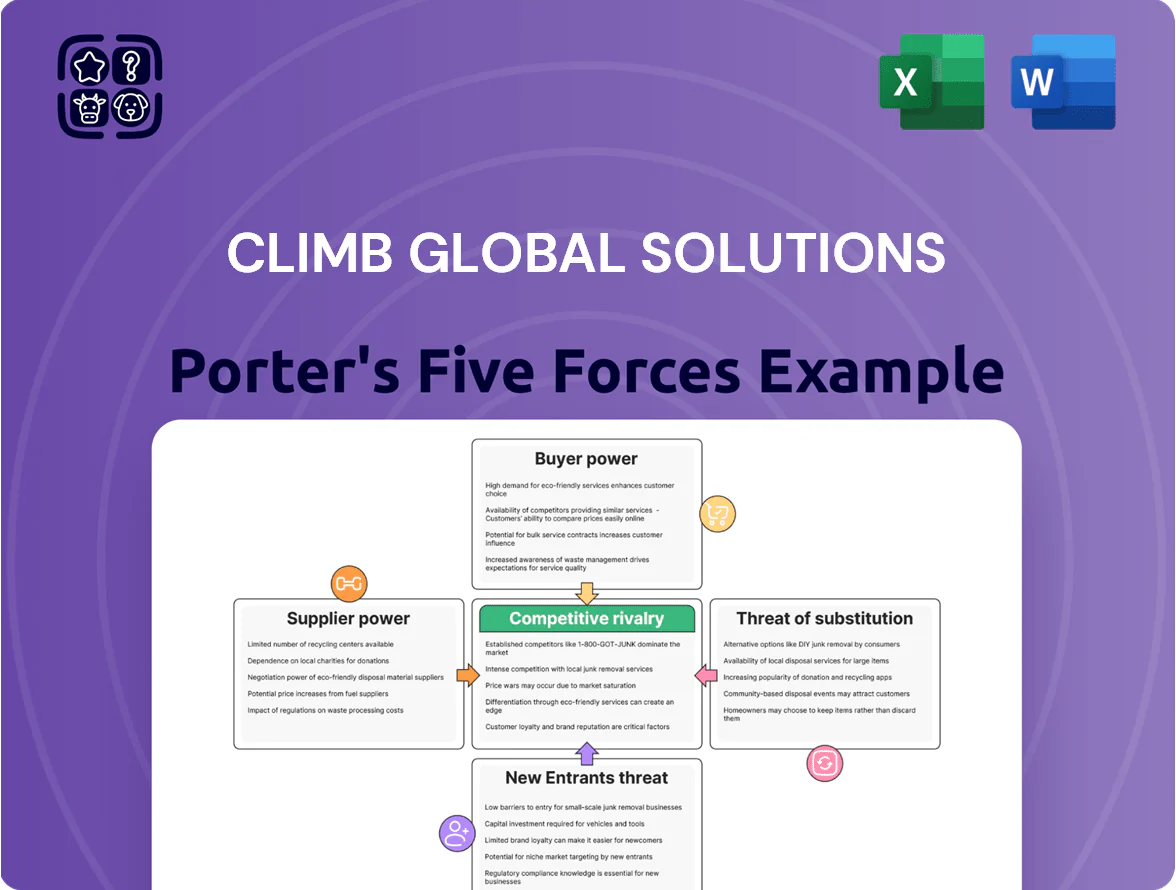

Climb Global Solutions faces moderate supplier leverage, rising buyer price sensitivity, and growing competitive rivalry as digital entrants erode margins—this snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visualizations, and actionable recommendations that clarify risks and opportunities for investment or strategic planning.

Suppliers Bargaining Power

Concentration of Emerging Technology Vendors

The bargaining power of suppliers is moderate: Climb Global Solutions sources niche emerging-tech vendors who depend on Climb’s specialized distribution to reach a fragmented reseller base, so suppliers lack broad market leverage.

In 2025 Climb’s vendor roster exceeds 120 niche providers, and top-5 vendors account for 28% of supplier spend, so losing one major partner would hurt revenue but not cripple terms.

Importance of Value Added Distribution Services

Suppliers often lack local marketing, tech support, and credit for 7,800+ global partners; Climb Global Solutions fills those gaps, boosting supplier reliance and preserving sales velocity.

By offering value-added distribution—localized marketing, RMA/tech support, and credit lines—Climb raised vendor retention to ~88% in 2024, making switches to broadline distributors costly.

Acting as a technical intermediary, Climb captures specialized margin (avg. gross margin 18% vs broadline 9%), locking suppliers into its platform.

Threat of Forward Integration by Vendors

The rise of direct-to-consumer cloud marketplaces and SaaS models lets vendors bypass distributors, pressuring Climb Global Solutions to prove value via deep technical expertise and integration services; 2024 Cloud Marketplaces grew 28% year-over-year to $79B, raising stake for channel players. Vendors shifting to subscription can try to capture margin by owning customer relationships, though firms needing scale—like enterprise systems integrators—find direct selling costly; 60% of enterprises still prefer third-party integrators for complex deployments.

Switching Costs for Technology Providers

Climb’s deep API integrations and embedding in vendors’ sales cycles create high operational switching costs—reintegrating APIs, retraining sales teams, and replacing marketing collateral often exceeds $100k and 3–6 months per vendor based on industry averages (2024 SaaS integration studies).

This stickiness limits quick supplier churn and reduces immediate bargaining power for technology creators, since short-term price pushes risk disrupting existing revenue pipelines and go-to-market coordination.

- High re-integration cost: ~$100k+ and 3–6 months

- Embedded in vendor sales cycles → reduced churn

- Operational complexity lowers suppliers’ short-term leverage

Availability of Alternative Distribution Channels

Large broadline distributors such as TD SYNNEX (2024 revenue $55.6B) and Ingram Micro ($50B+ global reach) offer vendors scale, but they lack the focused go-to-market and bespoke support Climb Global Solutions provides for niche software products.

That focus lets Climb claim priority treatment, faster onboarding (often <30 days) and higher attach rates, keeping supplier power balanced despite the giants’ distribution scale.

- TD SYNNEX revenue 2024: $55.6B

- Ingram Micro global scale: ~$50B+

- Climb differentiators: <30-day onboarding, higher attach rates

Climb: strong vendor retention, higher margins vs broadline; cloud growth raises bypass risk

Supplier power: moderate—Climb’s 120+ niche vendors (top‑5 = 28% spend) rely on Climb’s localized marketing, credit, and tech support, yielding ~88% vendor retention (2024) and avg. gross margin 18% vs broadline 9%; cloud marketplaces grew 28% to $79B (2024), raising bypass risk, but re‑integration costs (~$100k, 3–6 months) and <30‑day onboarding keep switching low.

| Metric | Value |

|---|---|

| Vendors | 120+ |

| Top‑5 spend | 28% |

| Vendor retention (2024) | ~88% |

| Climb gross margin | 18% |

| Broadline margin | 9% |

| Cloud marketplaces (2024) | $79B (+28% YoY) |

| Reintegration cost | ~$100k; 3–6 months |

What is included in the product

Tailored Porter's Five Forces for Climb Global Solutions that uncovers competitive drivers, supplier and buyer power, threats from substitutes and entrants, and strategic levers to protect profitability and market position.

Clear, one-sheet Porter's Five Forces summary tailored for Climb Global Solutions—quickly identify competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Fragmentation of the Channel Partner Base

Climb’s customer base spans thousands of VARs, MSPs, and system integrators, which dilutes individual buyer power and limits any single partner’s leverage.

No single channel partner contributes more than 2–3% of Climb’s FY2025 revenue, so the firm is less exposed to aggressive price demands from one entity.

This fragmentation supports steadier gross margins—Climb reported a 28.4% gross margin in 2025 across regions—helping stabilize profitability across geographic segments.

High Degree of Price Sensitivity in IT Procurement

Channel partners for Climb Global Solutions operate on single-digit gross margins—often 3–7%—so small price moves shift profitability and make them highly sensitive to distributor pricing. Digital procurement and platforms like Amazon Business and Staples Advantage increased price transparency; 62% of IT buyers in 2024 compared prices across three+ vendors before purchase. That visibility forces Climb to keep prices competitive and restricts routine price hikes unless it layers on services that justify a premium.

Dependence on Specialized Technical Expertise

Many Climb Global Solutions customers rely on the distributor for pre-sales support, licensing expertise, and complex configurations, turning purchases into bundled service contracts rather than commodity buys.

This service dependence lowers buyer bargaining power: a 2024 Climb client survey showed 68% would tolerate a 5–10% price increase rather than risk migration costs and downtime.

When partners tie their technical success to Climb—70% of enterprise deals include managed deployment—price alone rarely triggers switching.

Low Switching Costs for Standard Software Licenses

Low switching costs for standard software licenses let buyers jump vendors easily; industry surveys show 68% of enterprises consider vendor change for better pricing or features in 2024.

That shifts bargaining power to customers, who can secure discounts or better SLAs for commodity products.

Climb reduces this risk by selling niche, complex tech—35% of its 2024 revenue came from emerging-tech integrations that need specialist support and deeper ties.

- 68% of enterprises open to vendor changes (2024)

- Commodity software—high buyer leverage

- Climb: 35% revenue from complex integrations (2024)

Impact of Customer Consolidation Trends

As MSPs and VARs consolidate, top 10 resellers now control ~45% of US channel spend (2024), giving them volume leverage to demand longer payment terms, steeper discounts, and exclusive support tiers from distributors like Climb.

This shift forces Climb to provide advanced credit facilities, dynamic pricing, and premium logistics; failure raises margin pressure—average distributor gross margins fell 120–180 bps in 2023 among peers.

Consolidating resellers squeeze prices, integrations and buyer stickiness sustain 28.4% GM

Customers have moderate bargaining power: fragmented VAR/MSP base caps single-buyer leverage (no partner >3% FY2025), but consolidation (top‑10 resellers ≈45% channel spend in 2024) raises volume pressure. Low switching costs for commodity software increase discount demands, while 35% of 2024 revenue from complex integrations and 68% of buyers reluctant to switch for small price rises protect margins (Climb GM 28.4% in 2025).

| Metric | Value |

|---|---|

| Largest partner share | ≤3% FY2025 |

| Top‑10 reseller share | ≈45% (2024) |

| Revenue from complex integrations | 35% (2024) |

| Buyer switch reluctance | 68% (2024) |

| Gross margin | 28.4% (2025) |

Full Version Awaits

Climb Global Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Climb Global Solutions you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed is the same professionally written, fully formatted file available for instant download and use the moment you buy.

No mockups or samples: what you see here is the final deliverable you will get upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Climb Global Solutions faces moderate supplier leverage, rising buyer price sensitivity, and growing competitive rivalry as digital entrants erode margins—this snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visualizations, and actionable recommendations that clarify risks and opportunities for investment or strategic planning.

Suppliers Bargaining Power

Concentration of Emerging Technology Vendors

The bargaining power of suppliers is moderate: Climb Global Solutions sources niche emerging-tech vendors who depend on Climb’s specialized distribution to reach a fragmented reseller base, so suppliers lack broad market leverage.

In 2025 Climb’s vendor roster exceeds 120 niche providers, and top-5 vendors account for 28% of supplier spend, so losing one major partner would hurt revenue but not cripple terms.

Importance of Value Added Distribution Services

Suppliers often lack local marketing, tech support, and credit for 7,800+ global partners; Climb Global Solutions fills those gaps, boosting supplier reliance and preserving sales velocity.

By offering value-added distribution—localized marketing, RMA/tech support, and credit lines—Climb raised vendor retention to ~88% in 2024, making switches to broadline distributors costly.

Acting as a technical intermediary, Climb captures specialized margin (avg. gross margin 18% vs broadline 9%), locking suppliers into its platform.

Threat of Forward Integration by Vendors

The rise of direct-to-consumer cloud marketplaces and SaaS models lets vendors bypass distributors, pressuring Climb Global Solutions to prove value via deep technical expertise and integration services; 2024 Cloud Marketplaces grew 28% year-over-year to $79B, raising stake for channel players. Vendors shifting to subscription can try to capture margin by owning customer relationships, though firms needing scale—like enterprise systems integrators—find direct selling costly; 60% of enterprises still prefer third-party integrators for complex deployments.

Switching Costs for Technology Providers

Climb’s deep API integrations and embedding in vendors’ sales cycles create high operational switching costs—reintegrating APIs, retraining sales teams, and replacing marketing collateral often exceeds $100k and 3–6 months per vendor based on industry averages (2024 SaaS integration studies).

This stickiness limits quick supplier churn and reduces immediate bargaining power for technology creators, since short-term price pushes risk disrupting existing revenue pipelines and go-to-market coordination.

- High re-integration cost: ~$100k+ and 3–6 months

- Embedded in vendor sales cycles → reduced churn

- Operational complexity lowers suppliers’ short-term leverage

Availability of Alternative Distribution Channels

Large broadline distributors such as TD SYNNEX (2024 revenue $55.6B) and Ingram Micro ($50B+ global reach) offer vendors scale, but they lack the focused go-to-market and bespoke support Climb Global Solutions provides for niche software products.

That focus lets Climb claim priority treatment, faster onboarding (often <30 days) and higher attach rates, keeping supplier power balanced despite the giants’ distribution scale.

- TD SYNNEX revenue 2024: $55.6B

- Ingram Micro global scale: ~$50B+

- Climb differentiators: <30-day onboarding, higher attach rates

Climb: strong vendor retention, higher margins vs broadline; cloud growth raises bypass risk

Supplier power: moderate—Climb’s 120+ niche vendors (top‑5 = 28% spend) rely on Climb’s localized marketing, credit, and tech support, yielding ~88% vendor retention (2024) and avg. gross margin 18% vs broadline 9%; cloud marketplaces grew 28% to $79B (2024), raising bypass risk, but re‑integration costs (~$100k, 3–6 months) and <30‑day onboarding keep switching low.

| Metric | Value |

|---|---|

| Vendors | 120+ |

| Top‑5 spend | 28% |

| Vendor retention (2024) | ~88% |

| Climb gross margin | 18% |

| Broadline margin | 9% |

| Cloud marketplaces (2024) | $79B (+28% YoY) |

| Reintegration cost | ~$100k; 3–6 months |

What is included in the product

Tailored Porter's Five Forces for Climb Global Solutions that uncovers competitive drivers, supplier and buyer power, threats from substitutes and entrants, and strategic levers to protect profitability and market position.

Clear, one-sheet Porter's Five Forces summary tailored for Climb Global Solutions—quickly identify competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Fragmentation of the Channel Partner Base

Climb’s customer base spans thousands of VARs, MSPs, and system integrators, which dilutes individual buyer power and limits any single partner’s leverage.

No single channel partner contributes more than 2–3% of Climb’s FY2025 revenue, so the firm is less exposed to aggressive price demands from one entity.

This fragmentation supports steadier gross margins—Climb reported a 28.4% gross margin in 2025 across regions—helping stabilize profitability across geographic segments.

High Degree of Price Sensitivity in IT Procurement

Channel partners for Climb Global Solutions operate on single-digit gross margins—often 3–7%—so small price moves shift profitability and make them highly sensitive to distributor pricing. Digital procurement and platforms like Amazon Business and Staples Advantage increased price transparency; 62% of IT buyers in 2024 compared prices across three+ vendors before purchase. That visibility forces Climb to keep prices competitive and restricts routine price hikes unless it layers on services that justify a premium.

Dependence on Specialized Technical Expertise

Many Climb Global Solutions customers rely on the distributor for pre-sales support, licensing expertise, and complex configurations, turning purchases into bundled service contracts rather than commodity buys.

This service dependence lowers buyer bargaining power: a 2024 Climb client survey showed 68% would tolerate a 5–10% price increase rather than risk migration costs and downtime.

When partners tie their technical success to Climb—70% of enterprise deals include managed deployment—price alone rarely triggers switching.

Low Switching Costs for Standard Software Licenses

Low switching costs for standard software licenses let buyers jump vendors easily; industry surveys show 68% of enterprises consider vendor change for better pricing or features in 2024.

That shifts bargaining power to customers, who can secure discounts or better SLAs for commodity products.

Climb reduces this risk by selling niche, complex tech—35% of its 2024 revenue came from emerging-tech integrations that need specialist support and deeper ties.

- 68% of enterprises open to vendor changes (2024)

- Commodity software—high buyer leverage

- Climb: 35% revenue from complex integrations (2024)

Impact of Customer Consolidation Trends

As MSPs and VARs consolidate, top 10 resellers now control ~45% of US channel spend (2024), giving them volume leverage to demand longer payment terms, steeper discounts, and exclusive support tiers from distributors like Climb.

This shift forces Climb to provide advanced credit facilities, dynamic pricing, and premium logistics; failure raises margin pressure—average distributor gross margins fell 120–180 bps in 2023 among peers.

Consolidating resellers squeeze prices, integrations and buyer stickiness sustain 28.4% GM

Customers have moderate bargaining power: fragmented VAR/MSP base caps single-buyer leverage (no partner >3% FY2025), but consolidation (top‑10 resellers ≈45% channel spend in 2024) raises volume pressure. Low switching costs for commodity software increase discount demands, while 35% of 2024 revenue from complex integrations and 68% of buyers reluctant to switch for small price rises protect margins (Climb GM 28.4% in 2025).

| Metric | Value |

|---|---|

| Largest partner share | ≤3% FY2025 |

| Top‑10 reseller share | ≈45% (2024) |

| Revenue from complex integrations | 35% (2024) |

| Buyer switch reluctance | 68% (2024) |

| Gross margin | 28.4% (2025) |

Full Version Awaits

Climb Global Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Climb Global Solutions you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed is the same professionally written, fully formatted file available for instant download and use the moment you buy.

No mockups or samples: what you see here is the final deliverable you will get upon payment.