CLP Holdings PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Explore how regulatory shifts, energy transition, and technological innovation are reshaping CLP Holdings’ strategic outlook—our concise PESTLE snapshot highlights key external forces and immediate risks. Dive deeper with the full PESTLE analysis to access actionable insights, scenario impacts, and tactical recommendations tailored for investors and strategists. Purchase the complete report now for an instantly downloadable, editable briefing you can use in decision-making.

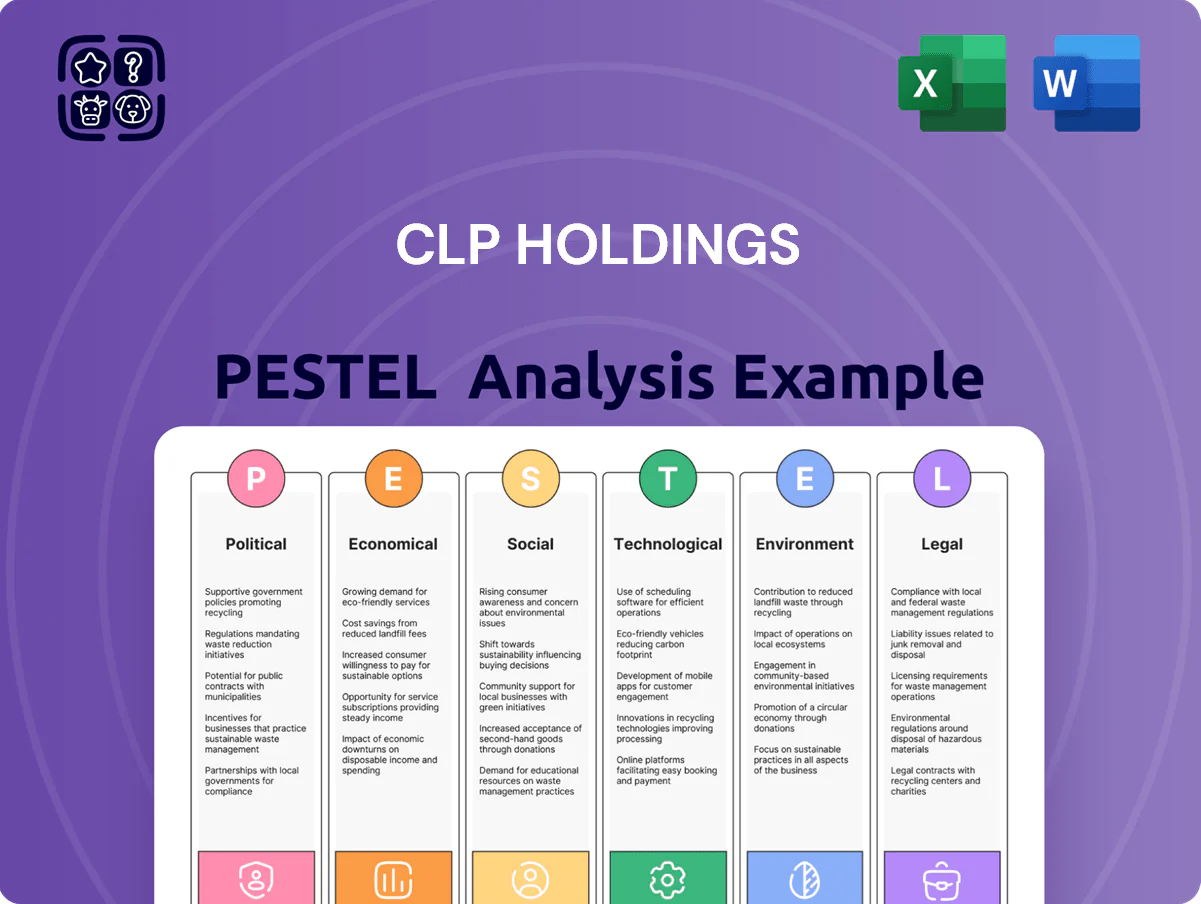

Political factors

Hong Kong regulatory stability

The Scheme of Control Agreement, in force through 2025, remains CLP’s primary regulatory framework in Hong Kong, guaranteeing a fixed return on average net fixed assets and supporting earnings visibility—CLP reported HK$7.9bn regulated asset base income in FY2024. This stability mitigates political volatility but requires active government engagement as public scrutiny on tariff hikes and energy security rose after 2023 power supply incidents. Maintaining strong relations is essential to manage tariff adjustment debates and policy shifts affecting future returns.

Geopolitical tensions in Australia

CLP’s subsidiary EnergyAustralia operates amid contested state and federal energy debates, with Australia’s 2030 emissions target of 43% below 2005 levels and 2024 renewable generation rising to ~40% of NEM electricity shaping policy timing.

Geopolitical shifts and domestic mandates accelerate coal plant retirements—Australia retired ~6.2 GW of coal capacity since 2017—and affect access to transition subsidies such as A$20–50/MWh federal support schemes.

Managing these political currents is critical to preserving AU assets valued at billions and to securing permits and funding for renewables and storage investments through 2030.

Mainland China energy policy alignment

CLP’s Mainland China investments are guided by the 14th Five-Year Plan and Beijing’s dual-carbon targets—peaking emissions before 2030 and achieving carbon neutrality by 2060—shaping project approvals and tariff frameworks affecting ~HKD 60bn of regional assets under management. Political backing for nuclear, wind and solar supports CLP’s diversified pipeline (over 4 GW renewables capacity planned by 2028), creating steady revenue visibility. Alignment with national energy-security objectives positions CLP as a preferred cross-border partner, facilitating grid access and long-term PPAs.

Energy security mandates in Southeast Asia

Political stability in Thailand and Vietnam is vital for CLP's regional expansion and the durability of PPAs; Thailand recorded a 2024 GDP growth of about 2.6% and Vietnam 2024 GDP ~5.3%, underpinning rising power demand but exposing CLP to policy shifts.

Governments balance affordable base-load supply with decarbonization pressures—Vietnam targets 43% renewables by 2030; Thailand aims for 30% renewables—forcing CLP to adapt asset mixes and contract terms.

Changing administrations and evolving national energy master plans (e.g., Vietnam Power Development Plan 8 revisions) increase political risk for market entry and project approvals, requiring local stakeholder engagement and flexible investment structures.

- Thailand GDP 2024 ~2.6%; Vietnam GDP 2024 ~5.3%

- Vietnam renewable target ~43% by 2030; Thailand ~30%

- Risk: PPA longevity, master plan revisions, admin changes

Decarbonization and international climate diplomacy

As an international energy player, CLP is exposed to outcomes of climate summits that drive the energy transition; COP26/27 commitments and the 2023 Glasgow Financial Alliance for Net Zero influence policy timelines that shape demand for renewables versus coal.

Political moves to phase out coal finance and boost renewable uptake affect CLP’s capital allocation—CLP reported HKD 6.8bn capex on low-carbon transition in 2023, signalling reallocation toward clean assets.

Compliance with international mandates also conditions CLP’s access to global capital and ESG funds: over 40% of major asset managers in 2024 applied net-zero screens, tightening financing for coal-linked firms.

- Global summit outcomes set transition pace

- Coal finance phase-out shifts CAPEX to renewables (HKD 6.8bn in 2023)

- Escalating ESG screens (40%+ asset managers using net-zero criteria in 2024) affect capital access

CLP: Stable HK RAB, AU coal exits & renewables surge, China/SE Asia growth pipeline

Political stability and regulatory frameworks (HK SoCA to 2025; HK$7.9bn RAB income FY2024) underpin CLP’s revenues, while Australia’s 43% 2030 target and ~40% renewables in NEM (2024) force coal retirements (~6.2GW since 2017) and reshape subsidies; China’s dual‑carbon goals back ~4GW pipeline to 2028 and ~HKD60bn AUM; Thailand/Vietnam growth (2024 GDP ~2.6%/5.3%) raise demand but heighten PPA/master‑plan risks.

| Item | Figure |

|---|---|

| HK regulated income FY2024 | HK$7.9bn |

| CLP low‑carbon capex 2023 | HK$6.8bn |

| Australia renewables NEM 2024 | ~40% |

| Coal retired AU since 2017 | ~6.2GW |

What is included in the product

Explores how macro-environmental forces uniquely impact CLP Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to the company’s regional power-market dynamics.

Condensed CLP Holdings PESTLE insights organized by category for quick reference in meetings or presentations, helping teams align on external risks and strategic positioning.

Economic factors

Interest rate sensitivity and financing costs

As a capital-intensive utility, CLP's performance is highly sensitive to global interest rates which raised average debt servicing costs; Hong Kong HIBOR and global yields surged in 2022–2024, lifting financing costs for large projects. Elevated rates through 2025 increased funding expenses for CLP's renewable roll-out and grid investments, with net debt of HKD 100–110 billion (2024) amplifying exposure. Investors monitor CLP's credit metrics—2024 adjusted net debt/EBITDA ~3.5x—and credit rating to limit borrowing spreads.

Fuel price volatility and inflation

Fluctuations in global coal and natural gas prices directly affect CLP's fuel costs and the tariffs passed to customers; LNG spot prices jumped over 200% year-on-year in 2022 and remained elevated into 2024, contributing to CLP Power Hong Kong's fuel cost adjustments totaling HKD 6.8 billion in 2023.

Hong Kong's regulatory framework permits partial fuel-cost recovery, but rapid price spikes caused temporary cash-flow pressure for CLP, with fuel cost variance swings of HKD ±1–2 billion quarterly in 2023–24 attracting public scrutiny.

Inflation pushed up labor and materials costs — Hong Kong CPI rose about 3.7% in 2023 and construction materials prices increased ~8% in 2024 — raising O&M and grid upgrade expenditures for CLP.

Economic growth trends in Asia Pacific

Electricity demand for CLP closely tracks GDP: Greater Bay Area GDP grew 5.4% in 2023 and China's 2024 target ~5% supports demand, while APAC emerging markets with 3–4% slowdowns cut industrial consumption and revenue forecasts by several percentage points.

Slower growth in selected ASEAN markets in 2024 reduced industrial load factors; CLP guidance models show sensitivity where a 1% GDP dip can lower demand ~0.6%.

Hong Kong’s rapid expansion of data centers—colocation capacity up ~20% YoY in 2023—and growth in advanced manufacturing provide durable upside to long‑term electricity demand for CLP.

Currency exchange rate fluctuations

CLP reports in HKD while earning material revenue in AUD and INR; in FY2024 about 12% of revenue came from Australia and 8% from India, exposing earnings to FX swings between HKD-AUD and HKD-INR.

Sharp AUD or INR devaluations cause translational losses—CLP noted a HKD 450m FX translation impact in 2024 sensitivity analysis—pressuring consolidated profit and ROE.

Active hedging (forwards, options, natural hedges) is therefore critical; CLP’s 2024 disclosures show hedges covering ~60% of forecasted foreign-currency cash flows for 12 months.

- Reporting currency: HKD; material operations in AUD, INR

- FY2024 exposure: ~12% Australia, ~8% India

- 2024 sensitivity: ~HKD 450m translation impact

- Hedging coverage: ~60% of 12-month FX cash flows

Capital expenditure for energy transition

The shift to net zero demands massive CAPEX: global clean energy investment hit about US$1.7trn in 2023 and Asia-Pacific grid spending is rising; CLP faces multi-billion HKD investments to expand renewables and modernize grids while maintaining FY2024 dividends of HKD0.85 per share. Project economics hinge on Hong Kong and regional incentives, carbon pricing signals, and continued declines in solar/wind LCOE—solar module costs fell ~40% since 2020.

- Global clean energy investment: US$1.7trn (2023)

- CLP FY2024 dividend: HKD0.85/share

- Solar module costs down ~40% since 2020

- Investment viability tied to subsidies and carbon pricing

CLP under pressure: rising rates, cost spikes & heavy renewables capex strain balance sheet

CLP faces higher financing costs after 2022–24 rate rises (net debt HKD100–110bn; 2024 adj net debt/EBITDA ~3.5x), volatile fuel costs (LNG spikes → HKD6.8bn 2023 adjustments), inflation-driven O&M/CAPEX pressure (HK CPI 3.7% in 2023; construction materials +8% in 2024), FX exposure (FY2024: ~12% Australia, ~8% India; ~HKD450m translation sensitivity) and large renewables CAPEX needs (global clean energy US$1.7trn 2023).

| Metric | Value (2024) |

|---|---|

| Net debt | HKD100–110bn |

| Adj net debt/EBITDA | ~3.5x |

| Fuel cost adj (2023) | HKD6.8bn |

| HK CPI (2023) | 3.7% |

| Construction materials (2024) | +8% |

| Revenue by market | AUD ~12%, INR ~8% |

| FX sensitivity | ~HKD450m |

| Hedging | ~60% 12‑month cover |

| Global clean energy spend | US$1.7trn (2023) |

Same Document Delivered

CLP Holdings PESTLE Analysis

The preview shown here is the exact CLP Holdings PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Explore how regulatory shifts, energy transition, and technological innovation are reshaping CLP Holdings’ strategic outlook—our concise PESTLE snapshot highlights key external forces and immediate risks. Dive deeper with the full PESTLE analysis to access actionable insights, scenario impacts, and tactical recommendations tailored for investors and strategists. Purchase the complete report now for an instantly downloadable, editable briefing you can use in decision-making.

Political factors

Hong Kong regulatory stability

The Scheme of Control Agreement, in force through 2025, remains CLP’s primary regulatory framework in Hong Kong, guaranteeing a fixed return on average net fixed assets and supporting earnings visibility—CLP reported HK$7.9bn regulated asset base income in FY2024. This stability mitigates political volatility but requires active government engagement as public scrutiny on tariff hikes and energy security rose after 2023 power supply incidents. Maintaining strong relations is essential to manage tariff adjustment debates and policy shifts affecting future returns.

Geopolitical tensions in Australia

CLP’s subsidiary EnergyAustralia operates amid contested state and federal energy debates, with Australia’s 2030 emissions target of 43% below 2005 levels and 2024 renewable generation rising to ~40% of NEM electricity shaping policy timing.

Geopolitical shifts and domestic mandates accelerate coal plant retirements—Australia retired ~6.2 GW of coal capacity since 2017—and affect access to transition subsidies such as A$20–50/MWh federal support schemes.

Managing these political currents is critical to preserving AU assets valued at billions and to securing permits and funding for renewables and storage investments through 2030.

Mainland China energy policy alignment

CLP’s Mainland China investments are guided by the 14th Five-Year Plan and Beijing’s dual-carbon targets—peaking emissions before 2030 and achieving carbon neutrality by 2060—shaping project approvals and tariff frameworks affecting ~HKD 60bn of regional assets under management. Political backing for nuclear, wind and solar supports CLP’s diversified pipeline (over 4 GW renewables capacity planned by 2028), creating steady revenue visibility. Alignment with national energy-security objectives positions CLP as a preferred cross-border partner, facilitating grid access and long-term PPAs.

Energy security mandates in Southeast Asia

Political stability in Thailand and Vietnam is vital for CLP's regional expansion and the durability of PPAs; Thailand recorded a 2024 GDP growth of about 2.6% and Vietnam 2024 GDP ~5.3%, underpinning rising power demand but exposing CLP to policy shifts.

Governments balance affordable base-load supply with decarbonization pressures—Vietnam targets 43% renewables by 2030; Thailand aims for 30% renewables—forcing CLP to adapt asset mixes and contract terms.

Changing administrations and evolving national energy master plans (e.g., Vietnam Power Development Plan 8 revisions) increase political risk for market entry and project approvals, requiring local stakeholder engagement and flexible investment structures.

- Thailand GDP 2024 ~2.6%; Vietnam GDP 2024 ~5.3%

- Vietnam renewable target ~43% by 2030; Thailand ~30%

- Risk: PPA longevity, master plan revisions, admin changes

Decarbonization and international climate diplomacy

As an international energy player, CLP is exposed to outcomes of climate summits that drive the energy transition; COP26/27 commitments and the 2023 Glasgow Financial Alliance for Net Zero influence policy timelines that shape demand for renewables versus coal.

Political moves to phase out coal finance and boost renewable uptake affect CLP’s capital allocation—CLP reported HKD 6.8bn capex on low-carbon transition in 2023, signalling reallocation toward clean assets.

Compliance with international mandates also conditions CLP’s access to global capital and ESG funds: over 40% of major asset managers in 2024 applied net-zero screens, tightening financing for coal-linked firms.

- Global summit outcomes set transition pace

- Coal finance phase-out shifts CAPEX to renewables (HKD 6.8bn in 2023)

- Escalating ESG screens (40%+ asset managers using net-zero criteria in 2024) affect capital access

CLP: Stable HK RAB, AU coal exits & renewables surge, China/SE Asia growth pipeline

Political stability and regulatory frameworks (HK SoCA to 2025; HK$7.9bn RAB income FY2024) underpin CLP’s revenues, while Australia’s 43% 2030 target and ~40% renewables in NEM (2024) force coal retirements (~6.2GW since 2017) and reshape subsidies; China’s dual‑carbon goals back ~4GW pipeline to 2028 and ~HKD60bn AUM; Thailand/Vietnam growth (2024 GDP ~2.6%/5.3%) raise demand but heighten PPA/master‑plan risks.

| Item | Figure |

|---|---|

| HK regulated income FY2024 | HK$7.9bn |

| CLP low‑carbon capex 2023 | HK$6.8bn |

| Australia renewables NEM 2024 | ~40% |

| Coal retired AU since 2017 | ~6.2GW |

What is included in the product

Explores how macro-environmental forces uniquely impact CLP Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to the company’s regional power-market dynamics.

Condensed CLP Holdings PESTLE insights organized by category for quick reference in meetings or presentations, helping teams align on external risks and strategic positioning.

Economic factors

Interest rate sensitivity and financing costs

As a capital-intensive utility, CLP's performance is highly sensitive to global interest rates which raised average debt servicing costs; Hong Kong HIBOR and global yields surged in 2022–2024, lifting financing costs for large projects. Elevated rates through 2025 increased funding expenses for CLP's renewable roll-out and grid investments, with net debt of HKD 100–110 billion (2024) amplifying exposure. Investors monitor CLP's credit metrics—2024 adjusted net debt/EBITDA ~3.5x—and credit rating to limit borrowing spreads.

Fuel price volatility and inflation

Fluctuations in global coal and natural gas prices directly affect CLP's fuel costs and the tariffs passed to customers; LNG spot prices jumped over 200% year-on-year in 2022 and remained elevated into 2024, contributing to CLP Power Hong Kong's fuel cost adjustments totaling HKD 6.8 billion in 2023.

Hong Kong's regulatory framework permits partial fuel-cost recovery, but rapid price spikes caused temporary cash-flow pressure for CLP, with fuel cost variance swings of HKD ±1–2 billion quarterly in 2023–24 attracting public scrutiny.

Inflation pushed up labor and materials costs — Hong Kong CPI rose about 3.7% in 2023 and construction materials prices increased ~8% in 2024 — raising O&M and grid upgrade expenditures for CLP.

Economic growth trends in Asia Pacific

Electricity demand for CLP closely tracks GDP: Greater Bay Area GDP grew 5.4% in 2023 and China's 2024 target ~5% supports demand, while APAC emerging markets with 3–4% slowdowns cut industrial consumption and revenue forecasts by several percentage points.

Slower growth in selected ASEAN markets in 2024 reduced industrial load factors; CLP guidance models show sensitivity where a 1% GDP dip can lower demand ~0.6%.

Hong Kong’s rapid expansion of data centers—colocation capacity up ~20% YoY in 2023—and growth in advanced manufacturing provide durable upside to long‑term electricity demand for CLP.

Currency exchange rate fluctuations

CLP reports in HKD while earning material revenue in AUD and INR; in FY2024 about 12% of revenue came from Australia and 8% from India, exposing earnings to FX swings between HKD-AUD and HKD-INR.

Sharp AUD or INR devaluations cause translational losses—CLP noted a HKD 450m FX translation impact in 2024 sensitivity analysis—pressuring consolidated profit and ROE.

Active hedging (forwards, options, natural hedges) is therefore critical; CLP’s 2024 disclosures show hedges covering ~60% of forecasted foreign-currency cash flows for 12 months.

- Reporting currency: HKD; material operations in AUD, INR

- FY2024 exposure: ~12% Australia, ~8% India

- 2024 sensitivity: ~HKD 450m translation impact

- Hedging coverage: ~60% of 12-month FX cash flows

Capital expenditure for energy transition

The shift to net zero demands massive CAPEX: global clean energy investment hit about US$1.7trn in 2023 and Asia-Pacific grid spending is rising; CLP faces multi-billion HKD investments to expand renewables and modernize grids while maintaining FY2024 dividends of HKD0.85 per share. Project economics hinge on Hong Kong and regional incentives, carbon pricing signals, and continued declines in solar/wind LCOE—solar module costs fell ~40% since 2020.

- Global clean energy investment: US$1.7trn (2023)

- CLP FY2024 dividend: HKD0.85/share

- Solar module costs down ~40% since 2020

- Investment viability tied to subsidies and carbon pricing

CLP under pressure: rising rates, cost spikes & heavy renewables capex strain balance sheet

CLP faces higher financing costs after 2022–24 rate rises (net debt HKD100–110bn; 2024 adj net debt/EBITDA ~3.5x), volatile fuel costs (LNG spikes → HKD6.8bn 2023 adjustments), inflation-driven O&M/CAPEX pressure (HK CPI 3.7% in 2023; construction materials +8% in 2024), FX exposure (FY2024: ~12% Australia, ~8% India; ~HKD450m translation sensitivity) and large renewables CAPEX needs (global clean energy US$1.7trn 2023).

| Metric | Value (2024) |

|---|---|

| Net debt | HKD100–110bn |

| Adj net debt/EBITDA | ~3.5x |

| Fuel cost adj (2023) | HKD6.8bn |

| HK CPI (2023) | 3.7% |

| Construction materials (2024) | +8% |

| Revenue by market | AUD ~12%, INR ~8% |

| FX sensitivity | ~HKD450m |

| Hedging | ~60% 12‑month cover |

| Global clean energy spend | US$1.7trn (2023) |

Same Document Delivered

CLP Holdings PESTLE Analysis

The preview shown here is the exact CLP Holdings PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout, with no placeholders or surprises.