CLP Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

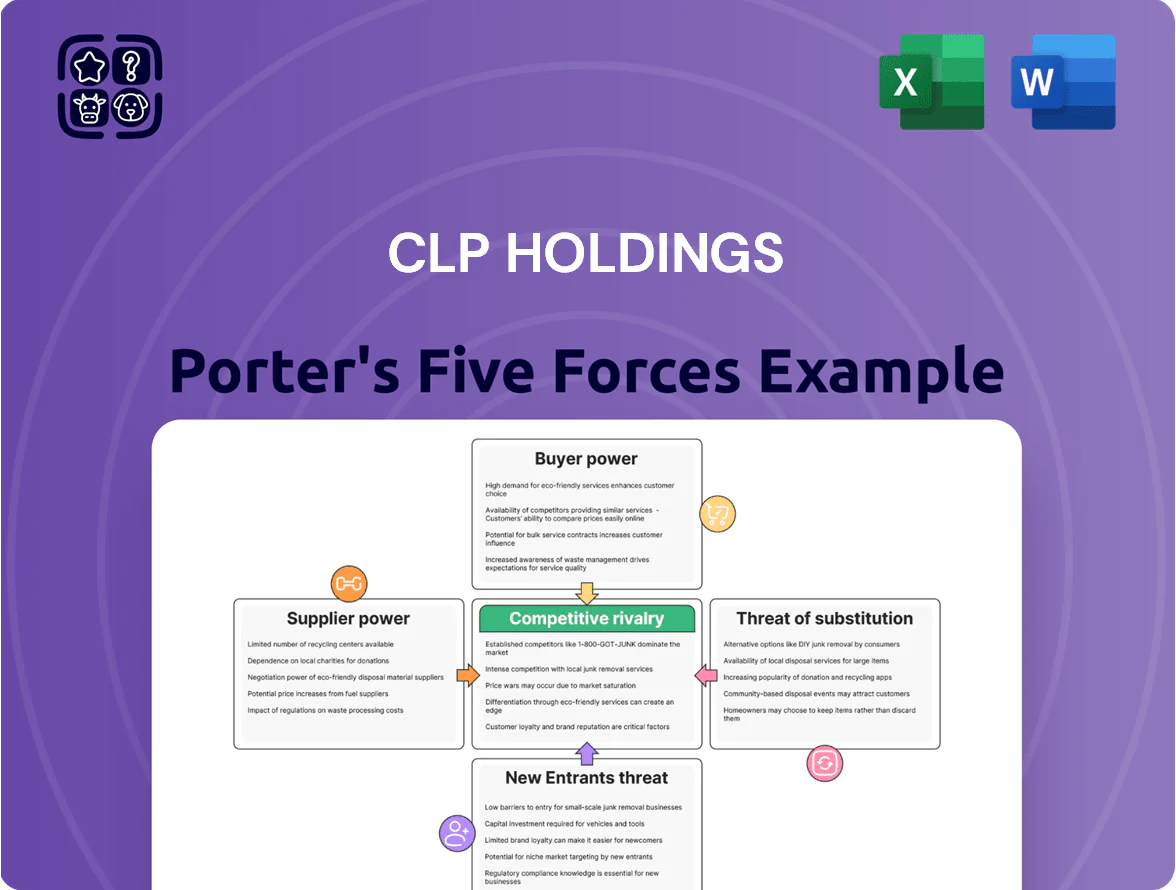

CLP Holdings faces moderate buyer power and regulatory pressures, while supplier influence and capital intensity limit margin expansion; competitive rivalry centers on pricing and renewable investment strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CLP Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Global Fuel Markets

CLP relies heavily on imported natural gas, coal and nuclear fuel across APAC; imported fuels made up ~68% of fuel costs in 2024, so suppliers hold strong leverage.

By late 2025, geopolitics and supply-chain limits pushed seaborne coal and LNG price volatility; LNG spot rose ~45% year‑on‑year in 2024–25, keeping OPEX elevated.

CLP uses long‑term contracts covering ~60–75% of volumes to smooth prices, but market swings still drive margin and tariff pressure.

Dependence on Specialized Technology Providers

The shift to renewables and grid upgrades needs high-tech gear like offshore turbines and utility-scale batteries; only about 5–10 global OEMs dominate these markets, giving suppliers strong leverage. In 2024 global offshore wind turbine shipments fell 8% while battery system demand rose 22%, pressuring lead times and prices. CLP must keep strategic partnerships and long-term contracts with these OEMs to secure timely delivery, maintenance and capex predictability.

Carbon Credit and Offset Markets

As Australia and Mainland China tighten decarbonization rules, demand for high‑quality carbon offsets and renewable energy certificates rose ~40% in 2023–24, pushing global voluntary offset prices up 60% to ~$12–20/tonne CO2e by end‑2024; suppliers of these assets gain leverage over CLP Holdings as the company scales to meet net‑zero targets, creating a secondary supply‑chain dependency that can spike compliance costs and affect ESG ratings.

Strategic Importance of Nuclear Power Supply

CLP’s Yangjiang stake ties it to specialist suppliers for nuclear fuel assemblies and safety systems, where a handful of vendors like Westinghouse and Framatome dominate global supply and service markets.

The sector’s strict regulation and technical barriers limit alternatives, so supplier switching costs and lead times stay high—global nuclear fuel market concentration remained around top-5 firms holding >70% share in 2024.

That concentration gives suppliers stable pricing power and leverage in contract negotiations, potentially pressuring CLP’s margins on capital-intensive nuclear operations.

- Yangjiang exposure: dependent on niche vendors

- Top-5 vendors ≈70% market share (2024)

- High switching costs, long lead times

- Supplier leverage can pressure nuclear margins

Labor Market Shortages for Technical Talent

The global buildout of renewables has created acute shortages of electrical engineers and renewables technicians; industry estimates put skilled labour gaps at ~200,000 workers in APAC by 2025, pushing wage premiums 10–25% in Australia and Hong Kong.

For CLP Holdings, suppliers of technical talent and specialist consultancies can demand higher fees as CLP races to meet 2025 project targets, raising development OPEX and schedule risk.

- APAC skilled-labour gap ~200,000 (2025 est)

- Wage premiums +10–25% in AU/HK

- Higher consultancy rates inflate OPEX

- Recruitment delays increase schedule risk

Suppliers wield power: fuel import dependency, soaring LNG, vendor concentration, APAC skill gap

Suppliers hold strong leverage: imported fuels ≈68% of fuel costs (2024); LNG spot +45% YoY (2024–25); long‑term contracts cover ~60–75% volumes but volatility hits margins; top‑5 nuclear vendors >70% market share (2024); 5–10 OEMs dominate offshore wind/batteries; APAC skilled‑labour gap ≈200,000 (2025), wage premiums +10–25% AU/HK.

| Metric | Value |

|---|---|

| Imported fuel share | ~68% (2024) |

| LNG spot change | +45% (2024–25) |

| Long‑term cover | 60–75% |

| Top‑5 nuclear share | >70% (2024) |

| APAC skilled gap | ~200,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for CLP Holdings revealing competitive intensity, customer and supplier power, substitution risks, and barriers protecting incumbency to inform strategic positioning and risk mitigation.

Instant, one-sheet Porter's Five Forces for CLP Holdings—quickly spot power imbalances across suppliers, buyers, entrants, substitutes, and rivalry to guide strategic moves.

Customers Bargaining Power

Regulated Pricing in the Hong Kong Market

The Scheme of Control Agreement (SOCA) in Hong Kong, covering CLP Holdings’ ~73% 2024 revenue share from the territory, limits CLP’s ability to set tariffs, effectively capping allowed returns (ROE cap ~8.5% under recent SOCA terms) and tying price changes to regulator-approved adjustments.

Intense Retail Competition in Australia

In Australia’s deregulated retail market, CLP’s EnergyAustralia faces high churn—national switching hit 17% in 2024—since consumers can move across 60+ retailers easily.

Price transparency tools and the government’s comparison site boosted switching intent; 42% of households used comparison sites in 2024 to find lower tariffs.

To defend share in 2025, CLP must invest in digital UX and CRM plus competitive bundles; analysts estimate a 5–8% uplift in retention for each A$10 monthly price-equivalent improvement.

Negotiation Leverage of Industrial Off-takers

Large industrial off-takers in Mainland China and India sign long-term PPAs, often 10–20 years, committing 50–500 MW+; in 2024 China corporate PPAs reached ~18 TWh and India cross-border/industrial deals rose ~30% YoY. These buyers are sophisticated, benchmarking bids across multiple renewable developers and pushing for lower tariffs, indexation, and strict reliability SLAs. CLP must deliver low-carbon capacity at scale—its 2024 renewable pipeline ~6 GW helps, but winning contracts requires competitive pricing, firm delivery guarantees, and grid-integration solutions. High-volume PPAs concentrate bargaining power, squeezing margins unless CLP secures operational and financing advantages.

The Rise of Energy Prosumers

Advancements in rooftop solar and residential batteries let customers generate and store power, cutting reliance on CLP’s grid; Hong Kong saw household solar installs grow ~40% from 2021–2024 to ~12 MW cumulative capacity, pressuring utility margins.

Prosumers now sell excess back to the grid via feed-in and virtual net metering pilots, shifting CLP from one-way supplier to platform partner and increasing customer bargaining power.

By 2025, distributed energy resources (DERs) forced CLP to rethink residential tariffs, demand charges, and value-added services to retain revenue and grid relevance.

- Household solar ~12 MW (2024)

- Solar installs +40% (2021–2024)

- Prosumers enable two-way flows, raising bargaining power

- CLP revises tariffs and offers services to protect margins

Demand Side Management and Smart Integration

Widespread smart meter and IoT adoption lets CLP customers shift load and join demand-response programs, reducing peak consumption—Hong Kong saw smart meter rollout reach ~65% of households by end-2024, enabling measurable peak cuts of 5–9% in pilots.

Customers now negotiate usage reduction for rebates or time-of-use rates, pushing CLP to offer granular hourly data, API access, and flexible tariffs to retain price-sensitive, tech-savvy users.

- ~65% smart meter household penetration (HK, 2024)

- Demand-response peak cut 5–9% in pilots

- Higher churn risk if hourly data or flexible tariffs absent

- CLP must invest in data platforms and dynamic pricing

Regulatory caps and rising DERs boost customer bargaining power, pressuring margins

Customers hold moderate–high bargaining power: SOCA caps CLP’s HK pricing (ROE ~8.5%, ~73% revenue 2024), Australian retail churn=17% (2024) with 42% using comparison sites, large PPAs (China ~18 TWh corporate PPAs 2024) squeeze margins, DERs (HK household solar ~12 MW, +40% 2021–24) and smart meters (~65% HK households 2024) boost switching and demand-response leverage.

| Metric | 2024 value |

|---|---|

| HK revenue share under SOCA | ~73% |

| SOCA ROE cap | ~8.5% |

| AU retail switching | 17% |

| Comparison-site use (households) | 42% |

| China corporate PPAs | ~18 TWh |

| HK household solar (cumulative) | ~12 MW |

| HK smart meter penetration | ~65% |

Same Document Delivered

CLP Holdings Porter's Five Forces Analysis

This preview shows the exact CLP Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is the fully formatted, professionally written file covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. You'll get instant access to this identical file upon payment, ready for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

CLP Holdings faces moderate buyer power and regulatory pressures, while supplier influence and capital intensity limit margin expansion; competitive rivalry centers on pricing and renewable investment strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CLP Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Global Fuel Markets

CLP relies heavily on imported natural gas, coal and nuclear fuel across APAC; imported fuels made up ~68% of fuel costs in 2024, so suppliers hold strong leverage.

By late 2025, geopolitics and supply-chain limits pushed seaborne coal and LNG price volatility; LNG spot rose ~45% year‑on‑year in 2024–25, keeping OPEX elevated.

CLP uses long‑term contracts covering ~60–75% of volumes to smooth prices, but market swings still drive margin and tariff pressure.

Dependence on Specialized Technology Providers

The shift to renewables and grid upgrades needs high-tech gear like offshore turbines and utility-scale batteries; only about 5–10 global OEMs dominate these markets, giving suppliers strong leverage. In 2024 global offshore wind turbine shipments fell 8% while battery system demand rose 22%, pressuring lead times and prices. CLP must keep strategic partnerships and long-term contracts with these OEMs to secure timely delivery, maintenance and capex predictability.

Carbon Credit and Offset Markets

As Australia and Mainland China tighten decarbonization rules, demand for high‑quality carbon offsets and renewable energy certificates rose ~40% in 2023–24, pushing global voluntary offset prices up 60% to ~$12–20/tonne CO2e by end‑2024; suppliers of these assets gain leverage over CLP Holdings as the company scales to meet net‑zero targets, creating a secondary supply‑chain dependency that can spike compliance costs and affect ESG ratings.

Strategic Importance of Nuclear Power Supply

CLP’s Yangjiang stake ties it to specialist suppliers for nuclear fuel assemblies and safety systems, where a handful of vendors like Westinghouse and Framatome dominate global supply and service markets.

The sector’s strict regulation and technical barriers limit alternatives, so supplier switching costs and lead times stay high—global nuclear fuel market concentration remained around top-5 firms holding >70% share in 2024.

That concentration gives suppliers stable pricing power and leverage in contract negotiations, potentially pressuring CLP’s margins on capital-intensive nuclear operations.

- Yangjiang exposure: dependent on niche vendors

- Top-5 vendors ≈70% market share (2024)

- High switching costs, long lead times

- Supplier leverage can pressure nuclear margins

Labor Market Shortages for Technical Talent

The global buildout of renewables has created acute shortages of electrical engineers and renewables technicians; industry estimates put skilled labour gaps at ~200,000 workers in APAC by 2025, pushing wage premiums 10–25% in Australia and Hong Kong.

For CLP Holdings, suppliers of technical talent and specialist consultancies can demand higher fees as CLP races to meet 2025 project targets, raising development OPEX and schedule risk.

- APAC skilled-labour gap ~200,000 (2025 est)

- Wage premiums +10–25% in AU/HK

- Higher consultancy rates inflate OPEX

- Recruitment delays increase schedule risk

Suppliers wield power: fuel import dependency, soaring LNG, vendor concentration, APAC skill gap

Suppliers hold strong leverage: imported fuels ≈68% of fuel costs (2024); LNG spot +45% YoY (2024–25); long‑term contracts cover ~60–75% volumes but volatility hits margins; top‑5 nuclear vendors >70% market share (2024); 5–10 OEMs dominate offshore wind/batteries; APAC skilled‑labour gap ≈200,000 (2025), wage premiums +10–25% AU/HK.

| Metric | Value |

|---|---|

| Imported fuel share | ~68% (2024) |

| LNG spot change | +45% (2024–25) |

| Long‑term cover | 60–75% |

| Top‑5 nuclear share | >70% (2024) |

| APAC skilled gap | ~200,000 (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for CLP Holdings revealing competitive intensity, customer and supplier power, substitution risks, and barriers protecting incumbency to inform strategic positioning and risk mitigation.

Instant, one-sheet Porter's Five Forces for CLP Holdings—quickly spot power imbalances across suppliers, buyers, entrants, substitutes, and rivalry to guide strategic moves.

Customers Bargaining Power

Regulated Pricing in the Hong Kong Market

The Scheme of Control Agreement (SOCA) in Hong Kong, covering CLP Holdings’ ~73% 2024 revenue share from the territory, limits CLP’s ability to set tariffs, effectively capping allowed returns (ROE cap ~8.5% under recent SOCA terms) and tying price changes to regulator-approved adjustments.

Intense Retail Competition in Australia

In Australia’s deregulated retail market, CLP’s EnergyAustralia faces high churn—national switching hit 17% in 2024—since consumers can move across 60+ retailers easily.

Price transparency tools and the government’s comparison site boosted switching intent; 42% of households used comparison sites in 2024 to find lower tariffs.

To defend share in 2025, CLP must invest in digital UX and CRM plus competitive bundles; analysts estimate a 5–8% uplift in retention for each A$10 monthly price-equivalent improvement.

Negotiation Leverage of Industrial Off-takers

Large industrial off-takers in Mainland China and India sign long-term PPAs, often 10–20 years, committing 50–500 MW+; in 2024 China corporate PPAs reached ~18 TWh and India cross-border/industrial deals rose ~30% YoY. These buyers are sophisticated, benchmarking bids across multiple renewable developers and pushing for lower tariffs, indexation, and strict reliability SLAs. CLP must deliver low-carbon capacity at scale—its 2024 renewable pipeline ~6 GW helps, but winning contracts requires competitive pricing, firm delivery guarantees, and grid-integration solutions. High-volume PPAs concentrate bargaining power, squeezing margins unless CLP secures operational and financing advantages.

The Rise of Energy Prosumers

Advancements in rooftop solar and residential batteries let customers generate and store power, cutting reliance on CLP’s grid; Hong Kong saw household solar installs grow ~40% from 2021–2024 to ~12 MW cumulative capacity, pressuring utility margins.

Prosumers now sell excess back to the grid via feed-in and virtual net metering pilots, shifting CLP from one-way supplier to platform partner and increasing customer bargaining power.

By 2025, distributed energy resources (DERs) forced CLP to rethink residential tariffs, demand charges, and value-added services to retain revenue and grid relevance.

- Household solar ~12 MW (2024)

- Solar installs +40% (2021–2024)

- Prosumers enable two-way flows, raising bargaining power

- CLP revises tariffs and offers services to protect margins

Demand Side Management and Smart Integration

Widespread smart meter and IoT adoption lets CLP customers shift load and join demand-response programs, reducing peak consumption—Hong Kong saw smart meter rollout reach ~65% of households by end-2024, enabling measurable peak cuts of 5–9% in pilots.

Customers now negotiate usage reduction for rebates or time-of-use rates, pushing CLP to offer granular hourly data, API access, and flexible tariffs to retain price-sensitive, tech-savvy users.

- ~65% smart meter household penetration (HK, 2024)

- Demand-response peak cut 5–9% in pilots

- Higher churn risk if hourly data or flexible tariffs absent

- CLP must invest in data platforms and dynamic pricing

Regulatory caps and rising DERs boost customer bargaining power, pressuring margins

Customers hold moderate–high bargaining power: SOCA caps CLP’s HK pricing (ROE ~8.5%, ~73% revenue 2024), Australian retail churn=17% (2024) with 42% using comparison sites, large PPAs (China ~18 TWh corporate PPAs 2024) squeeze margins, DERs (HK household solar ~12 MW, +40% 2021–24) and smart meters (~65% HK households 2024) boost switching and demand-response leverage.

| Metric | 2024 value |

|---|---|

| HK revenue share under SOCA | ~73% |

| SOCA ROE cap | ~8.5% |

| AU retail switching | 17% |

| Comparison-site use (households) | 42% |

| China corporate PPAs | ~18 TWh |

| HK household solar (cumulative) | ~12 MW |

| HK smart meter penetration | ~65% |

Same Document Delivered

CLP Holdings Porter's Five Forces Analysis

This preview shows the exact CLP Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is the fully formatted, professionally written file covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. You'll get instant access to this identical file upon payment, ready for download and use.