Clune Construction Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

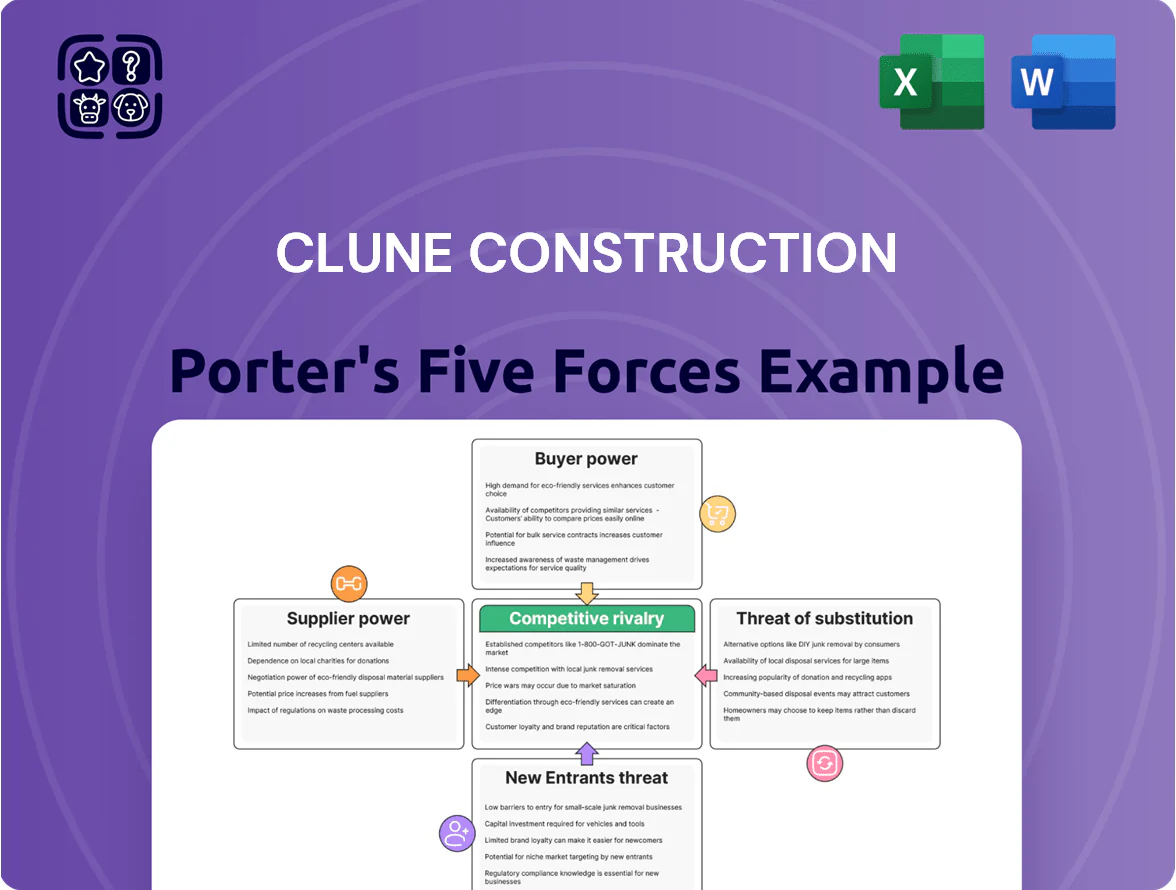

Clune Construction faces moderate buyer power and supplier concentration, while entry barriers and substitute threats remain mixed due to project specialization and regional demand variability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clune Construction’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consolidation of specialized subcontractors

The market for high-end interior and mission-critical subcontractors is highly specialized, giving these firms significant leverage over pricing and schedules; industry data shows top-tier trades command 10–25% price premiums and 4–8 week lead times as of 2025. As part of STO Building Group, Clune relies on a limited pool of elite tradespeople, so supplier booking gaps can push project timelines by 2–6 weeks and increase costs by up to 12%.

Volatility in raw material pricing

Fluctuations in steel, lumber, and specialized data-center components raise supplier bargaining power: steel surged 45% from 2020–2021 and lumber spiked 200% in 2020, while data-center PSU lead times hit 20+ weeks in 2023, letting suppliers press prices; Structure Tone’s bulk buys cut costs ~6–10% but global disruptions still shift terms, so Clune hedges via futures and secures early procurement—holding ~3–6 months of inventory to protect 2–4% margin erosion.

Labor shortages in skilled trades

The US construction sector reported a shortfall of about 430,000 craft workers in 2024, with electricians, plumbers, and HVAC techs most scarce, raising wage premiums 5–12% year-over-year in key metros; this scarcity boosts bargaining power of unions and specialist firms, letting them demand higher pay and priority scheduling.

Technological dependency on proprietary systems

Modern mission-critical and smart-building projects often specify proprietary software and hardware from vendors like Honeywell, Johnson Controls, and Siemens, giving those suppliers high bargaining power because systems are set in design and costly to swap.

Clune Construction’s reliance on these tech stacks reduces price leverage mid-project; reports show building automation market contracts can lock 10–20% of project cost and vendor change orders can add 5–15% in expenses.

- Proprietary vendors: high switch costs

- Specified early: limits renegotiation

- Tech can represent 10–20% of project budget

- Change orders add 5–15% cost risk

Geographic concentration of local vendors

In major hubs like Chicago and New York, a few dominant suppliers control key materials and specialized trades, restricting Clune Construction’s negotiation leverage for regional projects.

Clune must use vendors meeting national-account safety and quality standards, narrowing options and often forcing acceptance of higher rates; in 2024 regional spikes saw material premiums of 8–15% in metro markets.

That localized dependency can push subcontract and material costs above national averages during peak activity, squeezing margins on urban projects.

- Local supplier concentration reduces bargaining power

- National-account standards limit vendor pool

- 2024 metro premiums: 8–15%

- Higher costs compress urban project margins

Rising supplier power drives 10–25% premiums, long lead times and higher costs

Suppliers hold high power: elite trades take 10–25% premiums and 4–8 week lead times (2025); material shocks (steel +45% 2020–21, lumber +200% 2020) and 20+ week PSU delays raise costs; 2024 craft shortfall ~430,000 pushed wages +5–12% in metros; tech vendors (Honeywell, Siemens) lock 10–20% of budgets and change orders add 5–15%.

| Metric | Value |

|---|---|

| Elite trade premium | 10–25% |

| Lead times | 4–8 wks |

| Craft shortfall (2024) | 430,000 |

| Metro wage rise | +5–12% |

What is included in the product

Tailored Porter's Five Forces for Clune Construction revealing competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and strategic recommendations to safeguard margins and market position.

Concise Porter's Five Forces summary tailored to Clune Construction—quickly identify competitive pressures and relief strategies for bids, supplier negotiations, and margin protection.

Customers Bargaining Power

Concentration of high-value corporate clients

Clune’s client roster is skewed toward major corporations and institutional investors that drive repeat volume, with the top 10 clients historically accounting for ~40% of revenue (2024 internal filings). These sophisticated buyers run formal RFPs and leverage scale to push bids down, forcing Clune to compete on price and value-add services like preconstruction and lifecycle maintenance. Losing a single national account can cut regional revenue by 10–20%, raising client-concentration risk.

Low switching costs for general contracting services

While long-term relationships help Clune Construction, switching costs for developers and corporations remain low; industry surveys show 68% of owners consider price and schedule primary, not legacy ties (Dodge Data, 2024).

Clients can shift to competitors such as DPR Construction or HITT Contracting when bids promise 5–12% lower cost or 10–20% faster delivery, keeping leverage with owners.

Transparent public and private bidding—with 30–40% of projects competitively bid in 2024—magnifies owners’ bargaining power and pressures margins.

High sensitivity to project delivery timelines

Clients in mission-critical and interior projects demand strict move-in dates—healthcare and data-center clients report 72% of projects impose fixed operational deadlines—so timing becomes a key bargaining lever against Clune.

If Clune cannot guarantee schedules, customers push for liquidated damages or move to firms with spare capacity; 2024 industry data show 18% of contracts shifted for schedule certainty.

That pressure forces Clune to accept higher risk, often absorbing cost buffers and penalty exposure, which can cut project margins by an estimated 1.5–3% per contract.

Increased transparency through digital procurement

Increased use of digital bidding platforms and project-tracking software lets Clune Construction clients compare bids and contractor KPIs in real time, shrinking information gaps and pressuring margins.

By 2025, procurement platforms showed a 35% faster bid-turnaround and clients report seeing average subcontractor margin ranges (8–18%), upending traditional secrecy.

Information symmetry gives customers stronger bargaining power, forcing Clune to compete on price, speed, and verifiable performance metrics.

- 35% faster bid turnaround (2025)

- Subcontractor margin visibility: 8–18%

- Real-time KPI comparison reduces premium pricing

Demand for comprehensive sustainable building certifications

Concentrated clients, rising bids and green costs squeeze Clune margins and revenue

Major clients (top 10 ≈40% revenue, 2024) wield high leverage—competitive RFPs, 30–40% public bidding (2024), and 35% faster bid turnaround (2025) push Clune to cut price or add services; losing one national account can cut regional revenue 10–20% and trims margins ~1.5–3% per contract. Sustainability clauses (38% leases, 2024) add $150k–$500k costs, with only 3–5% fee uplift.

| Metric | Value |

|---|---|

| Top-10 client share (2024) | ~40% |

| Public/competitive bids (2024) | 30–40% |

| Bid turnaround improvement (2025) | 35% |

| Revenue hit if lose 1 national account | 10–20% |

| Margin hit per risky contract | 1.5–3% |

| Leases with sustainability clauses (2024) | 38% |

| Certification cost | $150k–$500k |

| Fee uplift for green | 3–5% |

What You See Is What You Get

Clune Construction Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Clune Construction you’ll receive upon purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Clune Construction faces moderate buyer power and supplier concentration, while entry barriers and substitute threats remain mixed due to project specialization and regional demand variability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clune Construction’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consolidation of specialized subcontractors

The market for high-end interior and mission-critical subcontractors is highly specialized, giving these firms significant leverage over pricing and schedules; industry data shows top-tier trades command 10–25% price premiums and 4–8 week lead times as of 2025. As part of STO Building Group, Clune relies on a limited pool of elite tradespeople, so supplier booking gaps can push project timelines by 2–6 weeks and increase costs by up to 12%.

Volatility in raw material pricing

Fluctuations in steel, lumber, and specialized data-center components raise supplier bargaining power: steel surged 45% from 2020–2021 and lumber spiked 200% in 2020, while data-center PSU lead times hit 20+ weeks in 2023, letting suppliers press prices; Structure Tone’s bulk buys cut costs ~6–10% but global disruptions still shift terms, so Clune hedges via futures and secures early procurement—holding ~3–6 months of inventory to protect 2–4% margin erosion.

Labor shortages in skilled trades

The US construction sector reported a shortfall of about 430,000 craft workers in 2024, with electricians, plumbers, and HVAC techs most scarce, raising wage premiums 5–12% year-over-year in key metros; this scarcity boosts bargaining power of unions and specialist firms, letting them demand higher pay and priority scheduling.

Technological dependency on proprietary systems

Modern mission-critical and smart-building projects often specify proprietary software and hardware from vendors like Honeywell, Johnson Controls, and Siemens, giving those suppliers high bargaining power because systems are set in design and costly to swap.

Clune Construction’s reliance on these tech stacks reduces price leverage mid-project; reports show building automation market contracts can lock 10–20% of project cost and vendor change orders can add 5–15% in expenses.

- Proprietary vendors: high switch costs

- Specified early: limits renegotiation

- Tech can represent 10–20% of project budget

- Change orders add 5–15% cost risk

Geographic concentration of local vendors

In major hubs like Chicago and New York, a few dominant suppliers control key materials and specialized trades, restricting Clune Construction’s negotiation leverage for regional projects.

Clune must use vendors meeting national-account safety and quality standards, narrowing options and often forcing acceptance of higher rates; in 2024 regional spikes saw material premiums of 8–15% in metro markets.

That localized dependency can push subcontract and material costs above national averages during peak activity, squeezing margins on urban projects.

- Local supplier concentration reduces bargaining power

- National-account standards limit vendor pool

- 2024 metro premiums: 8–15%

- Higher costs compress urban project margins

Rising supplier power drives 10–25% premiums, long lead times and higher costs

Suppliers hold high power: elite trades take 10–25% premiums and 4–8 week lead times (2025); material shocks (steel +45% 2020–21, lumber +200% 2020) and 20+ week PSU delays raise costs; 2024 craft shortfall ~430,000 pushed wages +5–12% in metros; tech vendors (Honeywell, Siemens) lock 10–20% of budgets and change orders add 5–15%.

| Metric | Value |

|---|---|

| Elite trade premium | 10–25% |

| Lead times | 4–8 wks |

| Craft shortfall (2024) | 430,000 |

| Metro wage rise | +5–12% |

What is included in the product

Tailored Porter's Five Forces for Clune Construction revealing competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and strategic recommendations to safeguard margins and market position.

Concise Porter's Five Forces summary tailored to Clune Construction—quickly identify competitive pressures and relief strategies for bids, supplier negotiations, and margin protection.

Customers Bargaining Power

Concentration of high-value corporate clients

Clune’s client roster is skewed toward major corporations and institutional investors that drive repeat volume, with the top 10 clients historically accounting for ~40% of revenue (2024 internal filings). These sophisticated buyers run formal RFPs and leverage scale to push bids down, forcing Clune to compete on price and value-add services like preconstruction and lifecycle maintenance. Losing a single national account can cut regional revenue by 10–20%, raising client-concentration risk.

Low switching costs for general contracting services

While long-term relationships help Clune Construction, switching costs for developers and corporations remain low; industry surveys show 68% of owners consider price and schedule primary, not legacy ties (Dodge Data, 2024).

Clients can shift to competitors such as DPR Construction or HITT Contracting when bids promise 5–12% lower cost or 10–20% faster delivery, keeping leverage with owners.

Transparent public and private bidding—with 30–40% of projects competitively bid in 2024—magnifies owners’ bargaining power and pressures margins.

High sensitivity to project delivery timelines

Clients in mission-critical and interior projects demand strict move-in dates—healthcare and data-center clients report 72% of projects impose fixed operational deadlines—so timing becomes a key bargaining lever against Clune.

If Clune cannot guarantee schedules, customers push for liquidated damages or move to firms with spare capacity; 2024 industry data show 18% of contracts shifted for schedule certainty.

That pressure forces Clune to accept higher risk, often absorbing cost buffers and penalty exposure, which can cut project margins by an estimated 1.5–3% per contract.

Increased transparency through digital procurement

Increased use of digital bidding platforms and project-tracking software lets Clune Construction clients compare bids and contractor KPIs in real time, shrinking information gaps and pressuring margins.

By 2025, procurement platforms showed a 35% faster bid-turnaround and clients report seeing average subcontractor margin ranges (8–18%), upending traditional secrecy.

Information symmetry gives customers stronger bargaining power, forcing Clune to compete on price, speed, and verifiable performance metrics.

- 35% faster bid turnaround (2025)

- Subcontractor margin visibility: 8–18%

- Real-time KPI comparison reduces premium pricing

Demand for comprehensive sustainable building certifications

Concentrated clients, rising bids and green costs squeeze Clune margins and revenue

Major clients (top 10 ≈40% revenue, 2024) wield high leverage—competitive RFPs, 30–40% public bidding (2024), and 35% faster bid turnaround (2025) push Clune to cut price or add services; losing one national account can cut regional revenue 10–20% and trims margins ~1.5–3% per contract. Sustainability clauses (38% leases, 2024) add $150k–$500k costs, with only 3–5% fee uplift.

| Metric | Value |

|---|---|

| Top-10 client share (2024) | ~40% |

| Public/competitive bids (2024) | 30–40% |

| Bid turnaround improvement (2025) | 35% |

| Revenue hit if lose 1 national account | 10–20% |

| Margin hit per risky contract | 1.5–3% |

| Leases with sustainability clauses (2024) | 38% |

| Certification cost | $150k–$500k |

| Fee uplift for green | 3–5% |

What You See Is What You Get

Clune Construction Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Clune Construction you’ll receive upon purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.