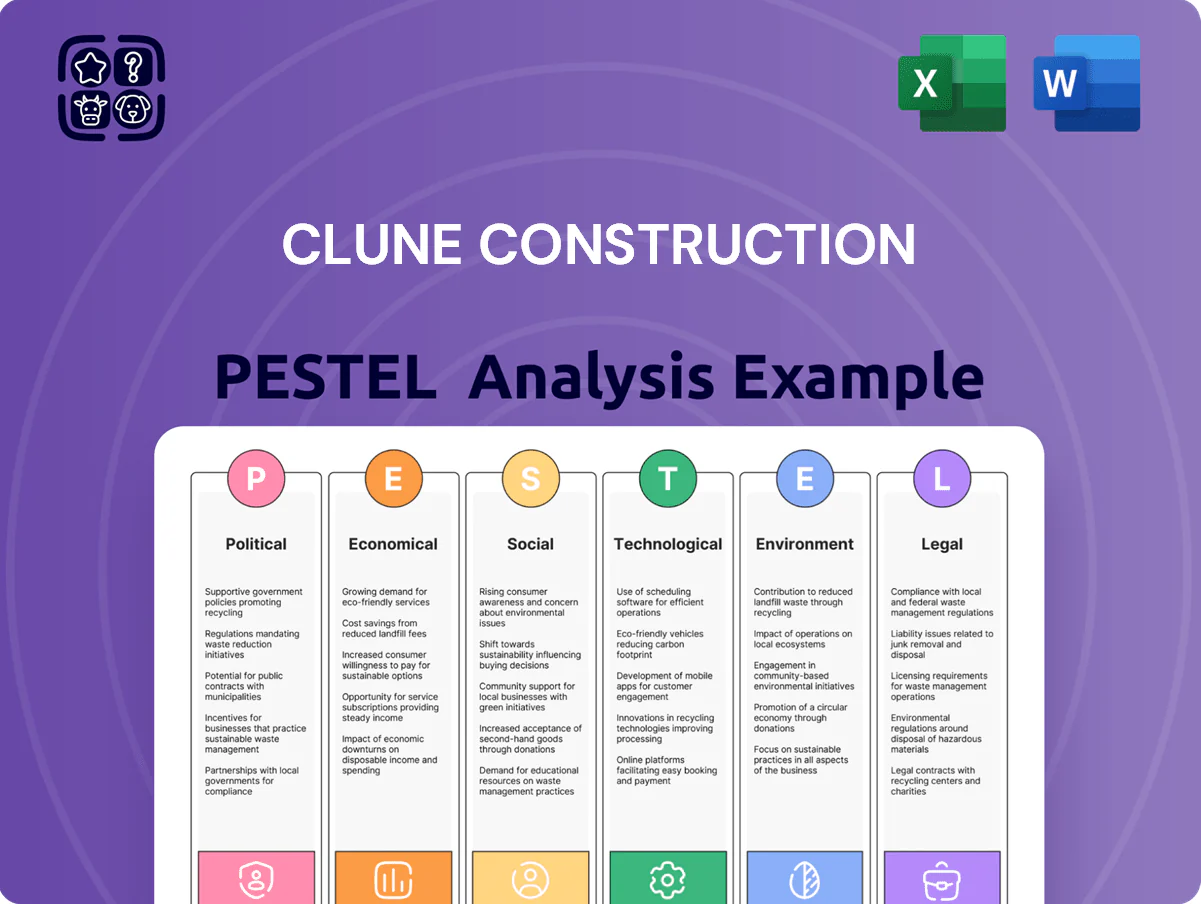

Clune Construction PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our expert PESTLE Analysis of Clune Construction—uncover how regulatory shifts, economic cycles, and technological advances are reshaping its prospects and where opportunities or risks lie. Ideal for investors, consultants, and strategists, this concise briefing points you to actionable insights fast. Purchase the full, editable report to access the complete deep-dive and precise recommendations.

Political factors

Federal Infrastructure Policy Implementation

By late 2025, continued rollout of the Bipartisan Infrastructure Law and CHIPS+ funding has generated a $450B-plus federal pipeline for construction, creating steady demand for large-scale construction managers.

Clune Construction gains from incentives for high-tech manufacturing and mission-critical facilities—securing projects tied to $52B in semiconductor and advanced manufacturing grants that favor specialized interior build-outs.

This political push to strengthen domestic industrial capacity prioritizes contractors with national reach, positioning Clune as a key partner in projects aligned with economic security goals and federal spending priorities.

Trade Policies and Material Costs

The political landscape on trade continues to drive volatility in steel and aluminum prices—US hot-rolled coil rose ~18% in 2024 while aluminum LME averaged $2,400/ton—forcing Clune to adopt hedging and diversified sourcing to protect margins; shifting tariffs (eg US Section 232 renewals, EU anti-dumping) and renegotiated FTAs require agile procurement to keep base-building schedules, as 30–45 day shipping delays and 10–20% cost swings can otherwise derail budgets.

Local Zoning and Permitting Regulations

Municipal political shifts in hubs like New York and Chicago have cut average interior renovation permitting times by up to 15% in 2024, accelerating project starts; delays still vary by borough and district. Local zoning incentives now target office-to-residential conversions—NYC approved 3,200+ conversion units in 2023 and Chicago pilots added 1,100 potential units. Clune Construction must align bidding and resource plans with these local priorities to capture growing redevelopment revenues.

Mission Critical Security Mandates

Government emphasis on data sovereignty and cybersecurity has increased mandates for mission-critical construction; U.S. federal guidance tightened after 2020, with federal IT security budgets rising to about $120B in 2024, driving stricter requirements for data centers.

Clune faces rigorous federal vetting and compliance (e.g., FISMA, DoD SRG) and must meet enhanced physical and cyber protections, impacting project timelines and compliance costs—industry estimates show security-related CAPEX additions of 5–12% per project in 2023–24.

These regulations ensure data center infrastructure adheres to high-level security protocols to protect national digital assets, increasing demand for verified contractors and creating competitive advantage for compliant firms like Clune.

- Federal IT budget ~ $120B (2024)

- Security CAPEX +5–12% (2023–24)

- Mandates: FISMA, DoD SRG, data sovereignty rules

Public-Private Partnership Initiatives

The expansion of public-private partnerships (P3s) enables Clune, with parent Structure Tone, to pursue large institutional projects; US P3 activity reached $32bn in 2023, signaling growing opportunities for base building and infrastructure work.

Political backing for P3s promotes shared risk and streamlined financing — typical P3 financing can cover 30–70% of project costs — aiding delivery of complex projects.

This collaborative climate lets Clune leverage construction management expertise on high-profile public sector developments, increasing bid competitiveness and revenue potential.

- 2023 US P3 market: $32bn

- P3 financing share: 30–70% of project costs

- Parent support: Structure Tone scale and capital access

Federal infrastructure & CHIPS funding fuel build-outs; material volatility spurs hedging

Federal infrastructure and CHIPS+ funding (>$450B pipeline by 2025) plus $52B in semiconductor grants boost demand for specialized interior build-outs; trade-driven material cost volatility (HRC +18% in 2024; aluminum ~$2,400/ton) forces hedging; municipal permitting cuts (~15% in 2024) and P3 growth ($32B in 2023) expand redevelopment and institutional opportunities; federal IT budget ~$120B (2024) raises security CAPEX +5–12%.

| Metric | Value |

|---|---|

| Federal construction pipeline | >$450B (by 2025) |

| Semiconductor grants | $52B |

| US P3 market | $32B (2023) |

| US federal IT budget | ~$120B (2024) |

| HRC price change | +18% (2024) |

| Aluminum LME | ~$2,400/ton (2024) |

| Security CAPEX impact | +5–12% (2023–24) |

What is included in the product

Explores how macro-environmental factors uniquely impact Clune Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-driven insights tailored to the construction industry and region.

Provides a concise, PESTLE-segmented summary of Clune Construction’s external risks and opportunities for easy insertion into presentations, team briefings, or consulting reports to speed decision-making and alignment.

Economic factors

Interest Rate Trajectory and Financing

As of end-2025, US 10-year Treasury yields settled near 4.2%, and the Federal Reserve signaled rate stability, creating predictable borrowing costs for real estate developers and corporate clients.

Lower volatility in borrowing—mortgage rates averaging ~6.5% for commercial loans in 2025—encourages investment in base building projects and large-scale office renovations.

Clune Construction leverages this stability to secure multi-year contracts and deliver preconstruction cost estimates with tighter contingencies, reducing client price uncertainty.

Commercial Office Market Evolution

The shift to hybrid work cut traditional office demand—US downtown office vacancy rose to about 18% in 2024—driving tenants toward premium, amenity-rich spaces; Clune can capture higher per-square-foot interiors as clients upgrade. Companies increased office upgrade spending, with US corporate real estate renovation budgets rising ~6–8% in 2024, supporting steady demand for sophisticated interior construction. Despite occupancy volatility, the flight-to-quality sustains margins for firms like Clune focused on high-end fit-outs.

Skilled Labor Market Shortages

The US construction sector faces a 2024 skilled labor shortfall—an estimated 650,000 workers—pushing craft wages up ~6–8% year-over-year and raising total labor cost lines by 3–5%; Clune must bid competitively and leverage STO Building Group’s scale and training resources to attract top-tier talent. Managing these rising labor costs is critical to protect Clune’s on-time, on-budget delivery and preserve profit margins.

Supply Chain Resilience and Inflation

While headline US inflation eased to 3.4% by December 2025, supply chains for steel and electrical components remain volatile after 2022–24 shocks, with global steel prices up 12% in H1 2025 in some regions.

Clune mitigates these risks via early procurement and strategic warehousing, maintaining inventory covering ~4–6 months of critical materials to avoid price spikes during build phases.

This proactive approach has kept mission-critical projects on schedule, reducing delay-related costs by an estimated 2–3% of project value in 2024–25.

- Headline inflation 3.4% (Dec 2025)

- Regional steel price rise ~12% (H1 2025)

- Inventory buffer: 4–6 months of critical materials

- Estimated delay-cost reduction 2–3% of project value

Data Center Investment Growth

The AI and cloud boom drove global data center capex to an estimated $200–220 billion in 2024, with hyperscaler spending up ~18% YoY; Clune's mission-critical construction expertise positions it to capture a meaningful share of this high-margin segment.

This tailwind buffers slower sectors, diversifying revenue and supporting margin resilience amid broader construction cyclical risks.

- Global data center capex: ~$200–220B (2024)

- Hyperscaler spend growth: ~18% YoY (2024)

- Clune advantage: mission-critical expertise → higher-margin projects

Stable rates and CRE flight-to-quality boost premium interiors amid labor pressures

Stable rates (10y ~4.2%, Fed rate guidance steady) and commercial mortgage ~6.5% in 2025 support multi-year contracts; office flight-to-quality keeps demand for premium interiors (downtown vacancy ~18%, CRE renovation budgets +6–8% in 2024). Skilled labor shortfall (~650k) lifted craft wages +6–8%, raising labor lines 3–5%; inventory buffers (4–6 months) and data-center capex ~$200–220B (2024) provide margin diversification.

| Metric | Value |

|---|---|

| US 10y yield (end-2025) | ~4.2% |

| Commercial mortgage rate (2025) | ~6.5% |

| Downtown office vacancy (2024) | ~18% |

| CRE renovation budgets (2024) | +6–8% |

| Skilled labor gap (2024) | ~650,000 |

| Craft wage rise | +6–8% |

| Inventory buffer | 4–6 months |

| Data center capex (2024) | $200–220B |

What You See Is What You Get

Clune Construction PESTLE Analysis

The preview shown here is the exact Clune Construction PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our expert PESTLE Analysis of Clune Construction—uncover how regulatory shifts, economic cycles, and technological advances are reshaping its prospects and where opportunities or risks lie. Ideal for investors, consultants, and strategists, this concise briefing points you to actionable insights fast. Purchase the full, editable report to access the complete deep-dive and precise recommendations.

Political factors

Federal Infrastructure Policy Implementation

By late 2025, continued rollout of the Bipartisan Infrastructure Law and CHIPS+ funding has generated a $450B-plus federal pipeline for construction, creating steady demand for large-scale construction managers.

Clune Construction gains from incentives for high-tech manufacturing and mission-critical facilities—securing projects tied to $52B in semiconductor and advanced manufacturing grants that favor specialized interior build-outs.

This political push to strengthen domestic industrial capacity prioritizes contractors with national reach, positioning Clune as a key partner in projects aligned with economic security goals and federal spending priorities.

Trade Policies and Material Costs

The political landscape on trade continues to drive volatility in steel and aluminum prices—US hot-rolled coil rose ~18% in 2024 while aluminum LME averaged $2,400/ton—forcing Clune to adopt hedging and diversified sourcing to protect margins; shifting tariffs (eg US Section 232 renewals, EU anti-dumping) and renegotiated FTAs require agile procurement to keep base-building schedules, as 30–45 day shipping delays and 10–20% cost swings can otherwise derail budgets.

Local Zoning and Permitting Regulations

Municipal political shifts in hubs like New York and Chicago have cut average interior renovation permitting times by up to 15% in 2024, accelerating project starts; delays still vary by borough and district. Local zoning incentives now target office-to-residential conversions—NYC approved 3,200+ conversion units in 2023 and Chicago pilots added 1,100 potential units. Clune Construction must align bidding and resource plans with these local priorities to capture growing redevelopment revenues.

Mission Critical Security Mandates

Government emphasis on data sovereignty and cybersecurity has increased mandates for mission-critical construction; U.S. federal guidance tightened after 2020, with federal IT security budgets rising to about $120B in 2024, driving stricter requirements for data centers.

Clune faces rigorous federal vetting and compliance (e.g., FISMA, DoD SRG) and must meet enhanced physical and cyber protections, impacting project timelines and compliance costs—industry estimates show security-related CAPEX additions of 5–12% per project in 2023–24.

These regulations ensure data center infrastructure adheres to high-level security protocols to protect national digital assets, increasing demand for verified contractors and creating competitive advantage for compliant firms like Clune.

- Federal IT budget ~ $120B (2024)

- Security CAPEX +5–12% (2023–24)

- Mandates: FISMA, DoD SRG, data sovereignty rules

Public-Private Partnership Initiatives

The expansion of public-private partnerships (P3s) enables Clune, with parent Structure Tone, to pursue large institutional projects; US P3 activity reached $32bn in 2023, signaling growing opportunities for base building and infrastructure work.

Political backing for P3s promotes shared risk and streamlined financing — typical P3 financing can cover 30–70% of project costs — aiding delivery of complex projects.

This collaborative climate lets Clune leverage construction management expertise on high-profile public sector developments, increasing bid competitiveness and revenue potential.

- 2023 US P3 market: $32bn

- P3 financing share: 30–70% of project costs

- Parent support: Structure Tone scale and capital access

Federal infrastructure & CHIPS funding fuel build-outs; material volatility spurs hedging

Federal infrastructure and CHIPS+ funding (>$450B pipeline by 2025) plus $52B in semiconductor grants boost demand for specialized interior build-outs; trade-driven material cost volatility (HRC +18% in 2024; aluminum ~$2,400/ton) forces hedging; municipal permitting cuts (~15% in 2024) and P3 growth ($32B in 2023) expand redevelopment and institutional opportunities; federal IT budget ~$120B (2024) raises security CAPEX +5–12%.

| Metric | Value |

|---|---|

| Federal construction pipeline | >$450B (by 2025) |

| Semiconductor grants | $52B |

| US P3 market | $32B (2023) |

| US federal IT budget | ~$120B (2024) |

| HRC price change | +18% (2024) |

| Aluminum LME | ~$2,400/ton (2024) |

| Security CAPEX impact | +5–12% (2023–24) |

What is included in the product

Explores how macro-environmental factors uniquely impact Clune Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-driven insights tailored to the construction industry and region.

Provides a concise, PESTLE-segmented summary of Clune Construction’s external risks and opportunities for easy insertion into presentations, team briefings, or consulting reports to speed decision-making and alignment.

Economic factors

Interest Rate Trajectory and Financing

As of end-2025, US 10-year Treasury yields settled near 4.2%, and the Federal Reserve signaled rate stability, creating predictable borrowing costs for real estate developers and corporate clients.

Lower volatility in borrowing—mortgage rates averaging ~6.5% for commercial loans in 2025—encourages investment in base building projects and large-scale office renovations.

Clune Construction leverages this stability to secure multi-year contracts and deliver preconstruction cost estimates with tighter contingencies, reducing client price uncertainty.

Commercial Office Market Evolution

The shift to hybrid work cut traditional office demand—US downtown office vacancy rose to about 18% in 2024—driving tenants toward premium, amenity-rich spaces; Clune can capture higher per-square-foot interiors as clients upgrade. Companies increased office upgrade spending, with US corporate real estate renovation budgets rising ~6–8% in 2024, supporting steady demand for sophisticated interior construction. Despite occupancy volatility, the flight-to-quality sustains margins for firms like Clune focused on high-end fit-outs.

Skilled Labor Market Shortages

The US construction sector faces a 2024 skilled labor shortfall—an estimated 650,000 workers—pushing craft wages up ~6–8% year-over-year and raising total labor cost lines by 3–5%; Clune must bid competitively and leverage STO Building Group’s scale and training resources to attract top-tier talent. Managing these rising labor costs is critical to protect Clune’s on-time, on-budget delivery and preserve profit margins.

Supply Chain Resilience and Inflation

While headline US inflation eased to 3.4% by December 2025, supply chains for steel and electrical components remain volatile after 2022–24 shocks, with global steel prices up 12% in H1 2025 in some regions.

Clune mitigates these risks via early procurement and strategic warehousing, maintaining inventory covering ~4–6 months of critical materials to avoid price spikes during build phases.

This proactive approach has kept mission-critical projects on schedule, reducing delay-related costs by an estimated 2–3% of project value in 2024–25.

- Headline inflation 3.4% (Dec 2025)

- Regional steel price rise ~12% (H1 2025)

- Inventory buffer: 4–6 months of critical materials

- Estimated delay-cost reduction 2–3% of project value

Data Center Investment Growth

The AI and cloud boom drove global data center capex to an estimated $200–220 billion in 2024, with hyperscaler spending up ~18% YoY; Clune's mission-critical construction expertise positions it to capture a meaningful share of this high-margin segment.

This tailwind buffers slower sectors, diversifying revenue and supporting margin resilience amid broader construction cyclical risks.

- Global data center capex: ~$200–220B (2024)

- Hyperscaler spend growth: ~18% YoY (2024)

- Clune advantage: mission-critical expertise → higher-margin projects

Stable rates and CRE flight-to-quality boost premium interiors amid labor pressures

Stable rates (10y ~4.2%, Fed rate guidance steady) and commercial mortgage ~6.5% in 2025 support multi-year contracts; office flight-to-quality keeps demand for premium interiors (downtown vacancy ~18%, CRE renovation budgets +6–8% in 2024). Skilled labor shortfall (~650k) lifted craft wages +6–8%, raising labor lines 3–5%; inventory buffers (4–6 months) and data-center capex ~$200–220B (2024) provide margin diversification.

| Metric | Value |

|---|---|

| US 10y yield (end-2025) | ~4.2% |

| Commercial mortgage rate (2025) | ~6.5% |

| Downtown office vacancy (2024) | ~18% |

| CRE renovation budgets (2024) | +6–8% |

| Skilled labor gap (2024) | ~650,000 |

| Craft wage rise | +6–8% |

| Inventory buffer | 4–6 months |

| Data center capex (2024) | $200–220B |

What You See Is What You Get

Clune Construction PESTLE Analysis

The preview shown here is the exact Clune Construction PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.