CMC Porter's Five Forces Analysis

From Overview to Strategy Blueprint

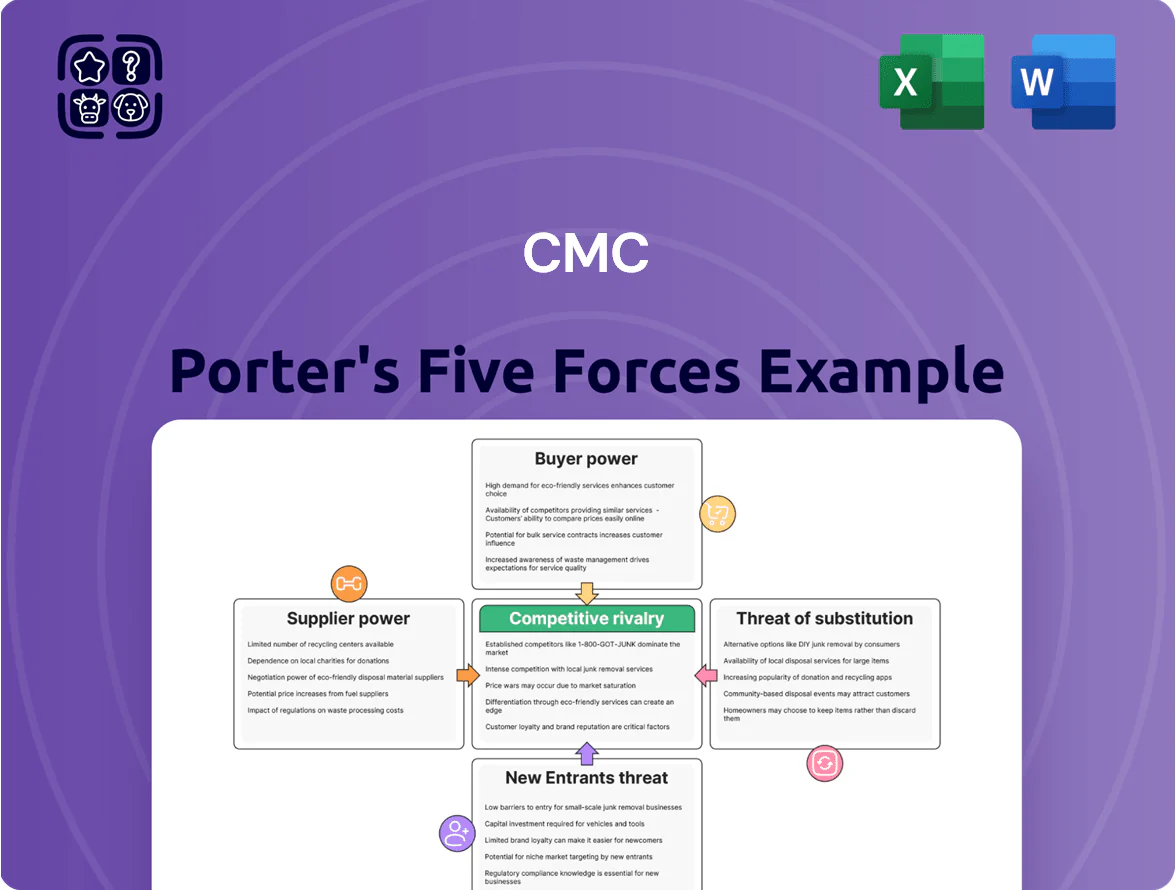

CMC’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of entrants, and substitute risks—showing where strategic pressure and opportunity collide.

Suppliers Bargaining Power

Vertical Integration of Scrap Supply

CMC’s vertical integration of scrap supply gives it ~60% of steel feedstock internally, cutting raw material spend by an estimated $420M in 2024 and shielding margins from the 18% year‑over‑year scrap price swings seen in 2022–24.

Energy and Utility Cost Volatility

Consumables and Specialized Raw Materials

Suppliers of graphite electrodes, ferroalloys, and refractories exert strong leverage over CMC due to narrow global capacity—top 5 graphite electrode producers control ~80% of capacity in 2024—making supply tight and prices volatile.

Any disruption can halt EAF (electric arc furnace) runs; a 10% shortage in 2024 raised spot electrode prices ~35%, risking multi-week mill stoppages and margin erosion.

By late 2025 geopolitical tensions—trade curbs and shipping bottlenecks—keep input prices elevated and delivery lead times stretched beyond 16–20 weeks for some grades.

Labor Market Constraints

The supply of skilled labor—engineers, mill operators, logistics pros—remains central to CMC’s efficiency; US manufacturing job openings hit 809,000 in Dec 2025, keeping labor tight.

Tight markets boost worker and union leverage over wages and benefits; average manufacturing hourly wages rose 4.2% year‑over‑year in 2025, raising CMC’s labor costs. CMC must invest in automation and training to offset rising human-capital expense.

- 809,000 US mfg job openings (Dec 2025)

- Manufacturing wages +4.2% YoY in 2025

- Automation + workforce dev reduces labor cost risk

Logistics and Transportation Providers

CMC depends on third-party rail, truck, and ship carriers to move scrap and finished steel; in 2024 freight surcharges added roughly 4–7% to transport costs industry-wide and peak-season capacity shortfalls raised spot rates by up to 35% (American Trucking Associations, 2024).

For low value-to-weight items like rebar, these cost swings cut gross margins materially; CMC’s logistics management and contract hedges are therefore critical to preserve margins and delivery reliability.

- Heavy reliance on 3PLs

- Fuel surcharges +4–7% (2024)

- Peak spot rates +up to 35%

- Rebar: high weight, low price sensitivity

- Logistics = margin lever

Suppliers tighten grip: 60% scrap saves $420M but electrodes, energy, freight pose risks

Suppliers hold strong leverage: CMC sources ~60% scrap internally saving ~$420M in 2024, but energy (400–600 MWh/kt EAF; $20–40/ton gas) and critical inputs (top‑5 electrode producers ~80% capacity) create vulnerability—2024 spot electrode spike +35%; freight surcharges +4–7% (2024); US mfg job openings 809,000 (Dec 2025) push wages +4.2% (2025).

| Metric | Value |

|---|---|

| Internal scrap | ~60% |

| 2024 raw savings | $420M |

| Electrode market | Top‑5 ~80% |

| Energy use | 400–600 MWh/kt |

| Freight surcharge | +4–7% (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for CMC, uncovering competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications to protect and grow market share.

Clear, one-sheet Porter's Five Forces summary with customizable pressure levels and a built-in spider chart—perfect for fast strategic decisions and plug-and-play use in decks or Excel dashboards.

Customers Bargaining Power

Concentration of Construction Distributors

Price Sensitivity in Commodity Steel

Standard steel products like rebar and merchant bar trade as commodities, so price drives buying; global rebar spot prices averaged about $620/ton in 2024, making small deltas decisive for buyers.

Customers switch suppliers for price differences under $10–20/ton, cutting CMC’s pricing power and capping margin expansion.

This high sensitivity forces CMC to keep unit cash costs low—benchmark integrated mills ran at ~$450–520/ton in 2024—else risk market-share loss.

Infrastructure Project Procurement Processes

Government-funded infrastructure projects, CMC's major end market, use rigid public tenders—Pakistan's 2024 Public Procurement Regulatory Authority reports 72% of large contracts awarded via open tenders—giving institutional buyers leverage to demand strict technical specs and low pricing.

Reliance on these large-scale contracts forces CMC to match buyer timelines and budgets; delayed compliance risks forfeiting projects where bid margins often fall below 8% on average in 2023-24 road and power tenders.

Availability of Transparent Market Pricing

Customization and Fabrication Services

CMC’s downstream customization and fabrication services reduce buyer power by bundling value-added design and assembly, raising switching costs—projects with integrated fabrication show retention increases of ~18% in 2024 industry surveys.

For complex EPC (engineering, procurement, construction) jobs, CMC’s end-to-end offerings make replacement costly in time and risk, helping secure longer contracts and higher margins—fabrication-linked projects delivered 12–15% higher gross margin in 2023 for comparable peers.

This strategic move builds stickier ties with major contractors and developers: repeat-business share for firms offering fabrication rose to 62% in 2024, strengthening negotiation leverage for CMC in downstream markets.

- Raises switching costs via integrated design+assembly

- Retention ~18% higher on fabricated projects (2024)

- Fabrication projects yield +12–15% gross margin (peer 2023 data)

- Repeat-business share 62% for fabrication providers (2024)

High buyer concentration forces CMC to cut costs to $450–520/t as fabrication boosts retention

| Metric | Value (Year) |

|---|---|

| Buyer concentration | 55% (2024) |

| Rebar price | $620/t (2024) |

| Buyer discounts | 6–8% (2025) |

| Cost benchmark | $450–520/t (2024) |

| Retention (fabrication) | +18% (2024) |

| Repeat business | 62% (2024) |

What You See Is What You Get

CMC Porter's Five Forces Analysis

This preview shows the exact CMC Porter's Five Forces analysis you'll receive instantly after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

CMC’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of entrants, and substitute risks—showing where strategic pressure and opportunity collide.

Suppliers Bargaining Power

Vertical Integration of Scrap Supply

CMC’s vertical integration of scrap supply gives it ~60% of steel feedstock internally, cutting raw material spend by an estimated $420M in 2024 and shielding margins from the 18% year‑over‑year scrap price swings seen in 2022–24.

Energy and Utility Cost Volatility

Consumables and Specialized Raw Materials

Suppliers of graphite electrodes, ferroalloys, and refractories exert strong leverage over CMC due to narrow global capacity—top 5 graphite electrode producers control ~80% of capacity in 2024—making supply tight and prices volatile.

Any disruption can halt EAF (electric arc furnace) runs; a 10% shortage in 2024 raised spot electrode prices ~35%, risking multi-week mill stoppages and margin erosion.

By late 2025 geopolitical tensions—trade curbs and shipping bottlenecks—keep input prices elevated and delivery lead times stretched beyond 16–20 weeks for some grades.

Labor Market Constraints

The supply of skilled labor—engineers, mill operators, logistics pros—remains central to CMC’s efficiency; US manufacturing job openings hit 809,000 in Dec 2025, keeping labor tight.

Tight markets boost worker and union leverage over wages and benefits; average manufacturing hourly wages rose 4.2% year‑over‑year in 2025, raising CMC’s labor costs. CMC must invest in automation and training to offset rising human-capital expense.

- 809,000 US mfg job openings (Dec 2025)

- Manufacturing wages +4.2% YoY in 2025

- Automation + workforce dev reduces labor cost risk

Logistics and Transportation Providers

CMC depends on third-party rail, truck, and ship carriers to move scrap and finished steel; in 2024 freight surcharges added roughly 4–7% to transport costs industry-wide and peak-season capacity shortfalls raised spot rates by up to 35% (American Trucking Associations, 2024).

For low value-to-weight items like rebar, these cost swings cut gross margins materially; CMC’s logistics management and contract hedges are therefore critical to preserve margins and delivery reliability.

- Heavy reliance on 3PLs

- Fuel surcharges +4–7% (2024)

- Peak spot rates +up to 35%

- Rebar: high weight, low price sensitivity

- Logistics = margin lever

Suppliers tighten grip: 60% scrap saves $420M but electrodes, energy, freight pose risks

Suppliers hold strong leverage: CMC sources ~60% scrap internally saving ~$420M in 2024, but energy (400–600 MWh/kt EAF; $20–40/ton gas) and critical inputs (top‑5 electrode producers ~80% capacity) create vulnerability—2024 spot electrode spike +35%; freight surcharges +4–7% (2024); US mfg job openings 809,000 (Dec 2025) push wages +4.2% (2025).

| Metric | Value |

|---|---|

| Internal scrap | ~60% |

| 2024 raw savings | $420M |

| Electrode market | Top‑5 ~80% |

| Energy use | 400–600 MWh/kt |

| Freight surcharge | +4–7% (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for CMC, uncovering competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications to protect and grow market share.

Clear, one-sheet Porter's Five Forces summary with customizable pressure levels and a built-in spider chart—perfect for fast strategic decisions and plug-and-play use in decks or Excel dashboards.

Customers Bargaining Power

Concentration of Construction Distributors

Price Sensitivity in Commodity Steel

Standard steel products like rebar and merchant bar trade as commodities, so price drives buying; global rebar spot prices averaged about $620/ton in 2024, making small deltas decisive for buyers.

Customers switch suppliers for price differences under $10–20/ton, cutting CMC’s pricing power and capping margin expansion.

This high sensitivity forces CMC to keep unit cash costs low—benchmark integrated mills ran at ~$450–520/ton in 2024—else risk market-share loss.

Infrastructure Project Procurement Processes

Government-funded infrastructure projects, CMC's major end market, use rigid public tenders—Pakistan's 2024 Public Procurement Regulatory Authority reports 72% of large contracts awarded via open tenders—giving institutional buyers leverage to demand strict technical specs and low pricing.

Reliance on these large-scale contracts forces CMC to match buyer timelines and budgets; delayed compliance risks forfeiting projects where bid margins often fall below 8% on average in 2023-24 road and power tenders.

Availability of Transparent Market Pricing

Customization and Fabrication Services

CMC’s downstream customization and fabrication services reduce buyer power by bundling value-added design and assembly, raising switching costs—projects with integrated fabrication show retention increases of ~18% in 2024 industry surveys.

For complex EPC (engineering, procurement, construction) jobs, CMC’s end-to-end offerings make replacement costly in time and risk, helping secure longer contracts and higher margins—fabrication-linked projects delivered 12–15% higher gross margin in 2023 for comparable peers.

This strategic move builds stickier ties with major contractors and developers: repeat-business share for firms offering fabrication rose to 62% in 2024, strengthening negotiation leverage for CMC in downstream markets.

- Raises switching costs via integrated design+assembly

- Retention ~18% higher on fabricated projects (2024)

- Fabrication projects yield +12–15% gross margin (peer 2023 data)

- Repeat-business share 62% for fabrication providers (2024)

High buyer concentration forces CMC to cut costs to $450–520/t as fabrication boosts retention

| Metric | Value (Year) |

|---|---|

| Buyer concentration | 55% (2024) |

| Rebar price | $620/t (2024) |

| Buyer discounts | 6–8% (2025) |

| Cost benchmark | $450–520/t (2024) |

| Retention (fabrication) | +18% (2024) |

| Repeat business | 62% (2024) |

What You See Is What You Get

CMC Porter's Five Forces Analysis

This preview shows the exact CMC Porter's Five Forces analysis you'll receive instantly after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.