Cheetah Mobile PESTLE Analysis

Your Competitive Advantage Starts with This Report

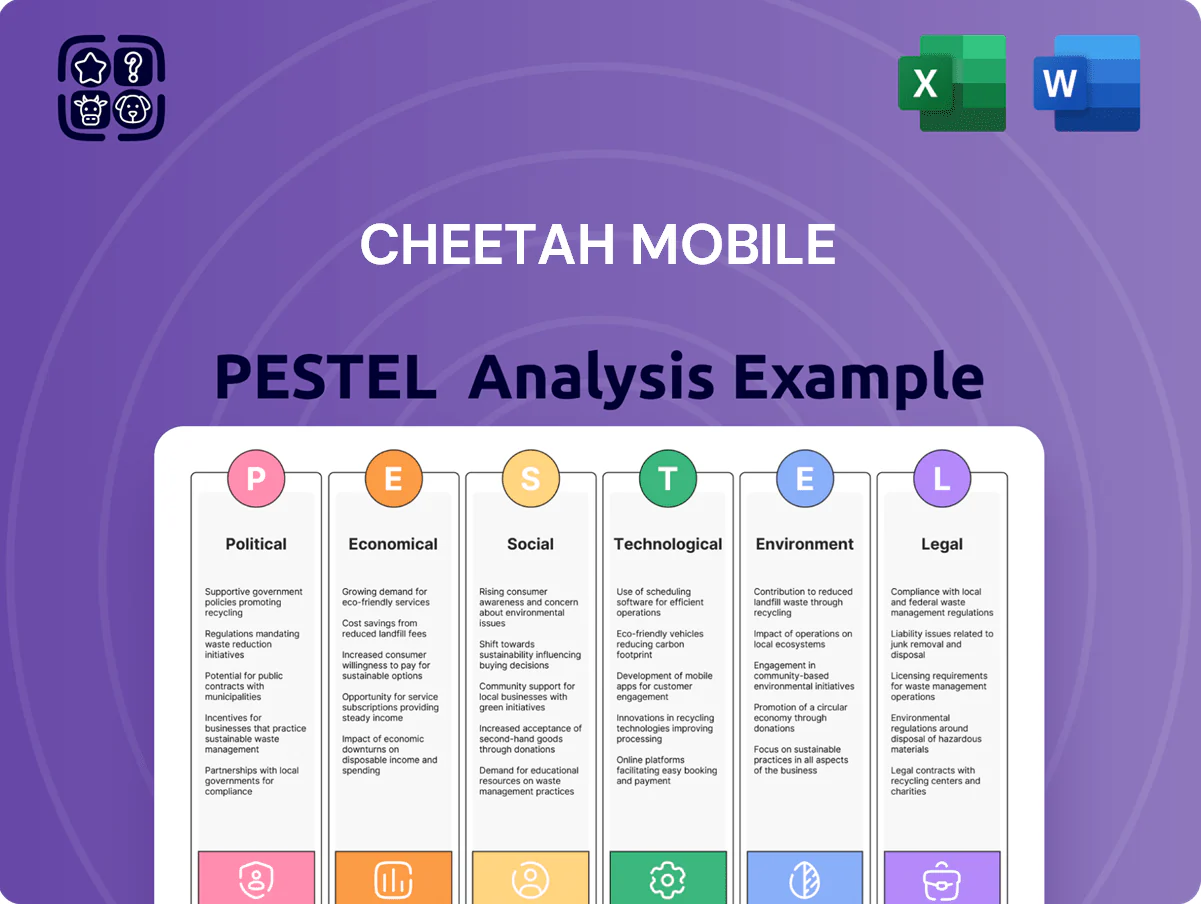

Uncover how political, economic, social, technological, legal, and environmental forces are reshaping Cheetah Mobile’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full analysis for a detailed, ready-to-use report and actionable insights you can deploy immediately.

Political factors

US-China Geopolitical Tensions

US-China geopolitical tensions have constrained Cheetah Mobile’s Western operations, with US Entity List additions and app bans contributing to a 28% decline in overseas revenue from 2019 to 2023; trade restrictions and proposed app prohibitions heighten uncertainty across its international portfolio.

Regulatory pressure raises the risk of sudden delistings and lost distribution channels, forcing higher compliance costs and potential revenue write-downs for affected apps.

Consequently, Cheetah Mobile is compelled to pivot toward China and neutral markets—where it reported 72% of 2024 revenue—reducing exposure to Western market exclusion.

Government Subsidies for AI and Robotics

The Chinese government’s push for self-reliance in high-tech sectors gives Cheetah Mobile potential access to research grants and tax breaks; Beijing allocated 1.4 trillion CNY to tech and innovation programs in 2024, boosting available subsidies for AI and robotics firms. Aligning its shift to AI-driven hardware and service robots with national policies—Made in China 2025 follow-ups and recent AI development plans—can unlock funding and preferential procurement. Such political incentives help offset steep R&D costs, with autonomous system development often exceeding tens of millions USD per project.

Cross-Border Data Sovereignty Laws

Governments tightened data sovereignty rules—e.g., China’s CSL and India’s proposed PDPB—pushing Cheetah Mobile to localize storage and processing; localized cloud/server costs can raise capex by 10–20% and increase operating compliance costs (estimated $20–50M annually for mid-sized app firms).

Content Regulation and Censorship

Operating in mobile gaming and content requires Cheetah Mobile to follow evolving Chinese Communist Party regulations; in 2023 China limited under-18 gaming to 3 hours/weekend restrictions and renewed content oversight across apps.

Political directives on minors' playtime and ideological content force product, UX and monetization redesigns; regulatory fines or delistings can cut revenue—China ad/consumer apps faced $1.7B in sector penalties 2022–24.

Cheetah Mobile must run sophisticated internal monitoring and compliance controls, using automated filters and audit trails to meet domestic mandates and avoid platform bans or revenue loss.

- Must enforce minors' play limits and content ideology rules

- Regulatory enforcement risk: sector fines ~$1.7B (2022–24)

- Requires automated monitoring, audit logs, rapid content takedown

National Security Scrutiny

Cheetah Mobile remains under intense national security scrutiny over potential data harvesting via utility and security apps; U.S. and EU concerns contributed to 2019-2020 removals that cut app-store distribution and helped drive GMV-linked advertising revenue down—company ad revenue fell by ~35% YoY in segments after delistings. Restoring access and advertiser confidence will likely require full transparency, GDPR-like compliance, and independent third-party audits to satisfy foreign political stakeholders.

- 2019-2020 app removals correlated with ~35% drop in ad revenue in affected segments

- Requires third-party audits and transparent data-handling to regain app-store placement

- Compliance with GDPR/US security reviews essential to restore advertiser trust

China Pivot: 72% Revenue Share Amid 28% Overseas Drop, Rising Compliance Costs

US-China tensions and Western app bans drove a 28% drop in overseas revenue (2019–23) and ~35% ad revenue decline in affected segments; 72% of 2024 revenue came from China as the firm reoriented. Beijing’s 2024 tech budget (1.4 trillion CNY) and AI/robotics incentives support R&D but data-localization rules (CSL) and youth gaming limits raise compliance costs (~$20–50M/yr; capex +10–20%).

| Metric | Value |

|---|---|

| Overseas revenue decline (2019–23) | 28% |

| Ad revenue hit post-removals | ~35% |

| 2024 China revenue share | 72% |

| China 2024 tech allocation | 1.4 trillion CNY |

| Estimated compliance cost | $20–50M/yr |

| Localized infra capex impact | +10–20% |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Cheetah Mobile, with data-driven, region- and industry-specific insights that identify risks, opportunities, and forward-looking scenarios to inform strategy, investor communications, and operational planning.

A concise, shareable PESTLE snapshot of Cheetah Mobile that highlights key political, economic, social, technological, legal, and environmental factors for quick alignment during meetings or presentations.

Economic factors

Transition to AI-Driven Revenue Streams

Cheetah Mobile is shifting revenue mix from mobile ad downturns toward AI and robotics, investing heavily after 2023 when ad revenue fell mid-teens; 2024 R&D and capex rose ~40% year-over-year to support hardware development.

Transition demands substantial capex and a multi-year horizon—management targets break-even on robotics unit economics by 2027, assuming annual production grows to 200k units and gross margins reach ~25%.

Scaling manufacturing and cost control are critical: achieving a price point near $350–$450 per service robot is needed to compete in the Asia-Pacific home/SMB market and protect margin versus lower-cost rivals.

Global Advertising Market Volatility

Global digital ad spend grew to an estimated $738 billion in 2024 but faced volatility with a 2–3% slowdown vs 2023; utility-app revenues like Cheetah Mobile’s are highly sensitive to such swings and to advertiser shifts toward Meta and TikTok, which captured ~45% of incremental spend in 2023–24.

Economic downturns can cut CPMs sharply—programmatic CPMs fell ~8% in 2023—exposing legacy product revenue to rapid erosion unless Cheetah Mobile continually optimizes its ad-tech stack to sustain yields in a crowded, increasingly automated marketplace.

Currency Exchange Rate Fluctuations

As Cheetah Mobile reports in RMB while earning significantly abroad, USD/RMB volatility directly affects translated revenues and 2024 operating profit sensitivity; a 5% RMB depreciation vs USD could swing reported overseas income materially given 30-40% of revenues tied to international markets. Exchange swings also raise costs for imported robotic components, where USD pricing rose ~8% YoY in 2024; robust hedging—forwards/options—remains essential to stabilize margins.

Semiconductor and Component Costs

The economic viability of Cheetah Mobile’s robotic products depends on global chip and sensor supply; semiconductor prices rose ~18% in 2021–2022 and while easing, foundry lead times remained 12–20 weeks in 2024, risking margin pressure on devices like GreetBot.

Raw-material and component cost volatility—sensor module prices up to 10–15% in 2023 for some suppliers—can squeeze hardware margins; efficient procurement, multi-sourcing and inventory hedging are essential to avoid past industry shortages.

- Semiconductor price spike ~18% (2021–22); fab lead times 12–20 weeks (2024)

- Sensor module cost rises 10–15% for some suppliers in 2023

- Mitigation: multi-sourcing, strategic inventory, contract hedging

Consumer Spending on Digital Entertainment

The performance of Cheetah Mobile’s gaming division is sensitive to global smartphone users’ discretionary income; global consumer spending on mobile games fell 3.7% year-on-year in H1 2025 to about $36.2bn, signaling tighter in-app purchase demand during downturns.

During economic contractions consumers reduce microtransactions, directly pressuring Cheetah’s gaming revenue—its games contributed an estimated 28% of total revenue in 2024.

Cheetah must diversify toward resilient monetization—subscription, ad-supported hybrid models, and live-ops—to offset volatility and protect ARPU.

- Mobile game spending down 3.7% H1 2025 (~$36.2bn)

- Games ~28% of Cheetah Mobile 2024 revenue

- Priority: subscription, ad-hybrid, live-ops to stabilize ARPU

Cheetah Mobile ramps R&D +40% to pivot into robotics; breakeven by 2027 amid supply shocks

Cheetah Mobile faces margin pressure from ad-market volatility and FX exposure; 2024 R&D/capex +40% to pivot into robotics, targeting robotics breakeven by 2027 at 200k units and ~25% gross margin. Supply-chain cost shocks (semis +18% in 2021–22; fab lead times 12–20 wks in 2024) and component hikes (sensors +10–15% in 2023) make multi-sourcing and hedging essential.

| Metric | Value |

|---|---|

| 2024 R&D/capex growth | +40% |

| Robotics target | 200k units by 2027, ~25% GM |

| Semiconductor spike | +18% (2021–22) |

| Sensor cost rise | 10–15% (2023) |

Preview Before You Purchase

Cheetah Mobile PESTLE Analysis

The preview shown here is the exact Cheetah Mobile PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how political, economic, social, technological, legal, and environmental forces are reshaping Cheetah Mobile’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full analysis for a detailed, ready-to-use report and actionable insights you can deploy immediately.

Political factors

US-China Geopolitical Tensions

US-China geopolitical tensions have constrained Cheetah Mobile’s Western operations, with US Entity List additions and app bans contributing to a 28% decline in overseas revenue from 2019 to 2023; trade restrictions and proposed app prohibitions heighten uncertainty across its international portfolio.

Regulatory pressure raises the risk of sudden delistings and lost distribution channels, forcing higher compliance costs and potential revenue write-downs for affected apps.

Consequently, Cheetah Mobile is compelled to pivot toward China and neutral markets—where it reported 72% of 2024 revenue—reducing exposure to Western market exclusion.

Government Subsidies for AI and Robotics

The Chinese government’s push for self-reliance in high-tech sectors gives Cheetah Mobile potential access to research grants and tax breaks; Beijing allocated 1.4 trillion CNY to tech and innovation programs in 2024, boosting available subsidies for AI and robotics firms. Aligning its shift to AI-driven hardware and service robots with national policies—Made in China 2025 follow-ups and recent AI development plans—can unlock funding and preferential procurement. Such political incentives help offset steep R&D costs, with autonomous system development often exceeding tens of millions USD per project.

Cross-Border Data Sovereignty Laws

Governments tightened data sovereignty rules—e.g., China’s CSL and India’s proposed PDPB—pushing Cheetah Mobile to localize storage and processing; localized cloud/server costs can raise capex by 10–20% and increase operating compliance costs (estimated $20–50M annually for mid-sized app firms).

Content Regulation and Censorship

Operating in mobile gaming and content requires Cheetah Mobile to follow evolving Chinese Communist Party regulations; in 2023 China limited under-18 gaming to 3 hours/weekend restrictions and renewed content oversight across apps.

Political directives on minors' playtime and ideological content force product, UX and monetization redesigns; regulatory fines or delistings can cut revenue—China ad/consumer apps faced $1.7B in sector penalties 2022–24.

Cheetah Mobile must run sophisticated internal monitoring and compliance controls, using automated filters and audit trails to meet domestic mandates and avoid platform bans or revenue loss.

- Must enforce minors' play limits and content ideology rules

- Regulatory enforcement risk: sector fines ~$1.7B (2022–24)

- Requires automated monitoring, audit logs, rapid content takedown

National Security Scrutiny

Cheetah Mobile remains under intense national security scrutiny over potential data harvesting via utility and security apps; U.S. and EU concerns contributed to 2019-2020 removals that cut app-store distribution and helped drive GMV-linked advertising revenue down—company ad revenue fell by ~35% YoY in segments after delistings. Restoring access and advertiser confidence will likely require full transparency, GDPR-like compliance, and independent third-party audits to satisfy foreign political stakeholders.

- 2019-2020 app removals correlated with ~35% drop in ad revenue in affected segments

- Requires third-party audits and transparent data-handling to regain app-store placement

- Compliance with GDPR/US security reviews essential to restore advertiser trust

China Pivot: 72% Revenue Share Amid 28% Overseas Drop, Rising Compliance Costs

US-China tensions and Western app bans drove a 28% drop in overseas revenue (2019–23) and ~35% ad revenue decline in affected segments; 72% of 2024 revenue came from China as the firm reoriented. Beijing’s 2024 tech budget (1.4 trillion CNY) and AI/robotics incentives support R&D but data-localization rules (CSL) and youth gaming limits raise compliance costs (~$20–50M/yr; capex +10–20%).

| Metric | Value |

|---|---|

| Overseas revenue decline (2019–23) | 28% |

| Ad revenue hit post-removals | ~35% |

| 2024 China revenue share | 72% |

| China 2024 tech allocation | 1.4 trillion CNY |

| Estimated compliance cost | $20–50M/yr |

| Localized infra capex impact | +10–20% |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Cheetah Mobile, with data-driven, region- and industry-specific insights that identify risks, opportunities, and forward-looking scenarios to inform strategy, investor communications, and operational planning.

A concise, shareable PESTLE snapshot of Cheetah Mobile that highlights key political, economic, social, technological, legal, and environmental factors for quick alignment during meetings or presentations.

Economic factors

Transition to AI-Driven Revenue Streams

Cheetah Mobile is shifting revenue mix from mobile ad downturns toward AI and robotics, investing heavily after 2023 when ad revenue fell mid-teens; 2024 R&D and capex rose ~40% year-over-year to support hardware development.

Transition demands substantial capex and a multi-year horizon—management targets break-even on robotics unit economics by 2027, assuming annual production grows to 200k units and gross margins reach ~25%.

Scaling manufacturing and cost control are critical: achieving a price point near $350–$450 per service robot is needed to compete in the Asia-Pacific home/SMB market and protect margin versus lower-cost rivals.

Global Advertising Market Volatility

Global digital ad spend grew to an estimated $738 billion in 2024 but faced volatility with a 2–3% slowdown vs 2023; utility-app revenues like Cheetah Mobile’s are highly sensitive to such swings and to advertiser shifts toward Meta and TikTok, which captured ~45% of incremental spend in 2023–24.

Economic downturns can cut CPMs sharply—programmatic CPMs fell ~8% in 2023—exposing legacy product revenue to rapid erosion unless Cheetah Mobile continually optimizes its ad-tech stack to sustain yields in a crowded, increasingly automated marketplace.

Currency Exchange Rate Fluctuations

As Cheetah Mobile reports in RMB while earning significantly abroad, USD/RMB volatility directly affects translated revenues and 2024 operating profit sensitivity; a 5% RMB depreciation vs USD could swing reported overseas income materially given 30-40% of revenues tied to international markets. Exchange swings also raise costs for imported robotic components, where USD pricing rose ~8% YoY in 2024; robust hedging—forwards/options—remains essential to stabilize margins.

Semiconductor and Component Costs

The economic viability of Cheetah Mobile’s robotic products depends on global chip and sensor supply; semiconductor prices rose ~18% in 2021–2022 and while easing, foundry lead times remained 12–20 weeks in 2024, risking margin pressure on devices like GreetBot.

Raw-material and component cost volatility—sensor module prices up to 10–15% in 2023 for some suppliers—can squeeze hardware margins; efficient procurement, multi-sourcing and inventory hedging are essential to avoid past industry shortages.

- Semiconductor price spike ~18% (2021–22); fab lead times 12–20 weeks (2024)

- Sensor module cost rises 10–15% for some suppliers in 2023

- Mitigation: multi-sourcing, strategic inventory, contract hedging

Consumer Spending on Digital Entertainment

The performance of Cheetah Mobile’s gaming division is sensitive to global smartphone users’ discretionary income; global consumer spending on mobile games fell 3.7% year-on-year in H1 2025 to about $36.2bn, signaling tighter in-app purchase demand during downturns.

During economic contractions consumers reduce microtransactions, directly pressuring Cheetah’s gaming revenue—its games contributed an estimated 28% of total revenue in 2024.

Cheetah must diversify toward resilient monetization—subscription, ad-supported hybrid models, and live-ops—to offset volatility and protect ARPU.

- Mobile game spending down 3.7% H1 2025 (~$36.2bn)

- Games ~28% of Cheetah Mobile 2024 revenue

- Priority: subscription, ad-hybrid, live-ops to stabilize ARPU

Cheetah Mobile ramps R&D +40% to pivot into robotics; breakeven by 2027 amid supply shocks

Cheetah Mobile faces margin pressure from ad-market volatility and FX exposure; 2024 R&D/capex +40% to pivot into robotics, targeting robotics breakeven by 2027 at 200k units and ~25% gross margin. Supply-chain cost shocks (semis +18% in 2021–22; fab lead times 12–20 wks in 2024) and component hikes (sensors +10–15% in 2023) make multi-sourcing and hedging essential.

| Metric | Value |

|---|---|

| 2024 R&D/capex growth | +40% |

| Robotics target | 200k units by 2027, ~25% GM |

| Semiconductor spike | +18% (2021–22) |

| Sensor cost rise | 10–15% (2023) |

Preview Before You Purchase

Cheetah Mobile PESTLE Analysis

The preview shown here is the exact Cheetah Mobile PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.