China Merchants Energy Shipping Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

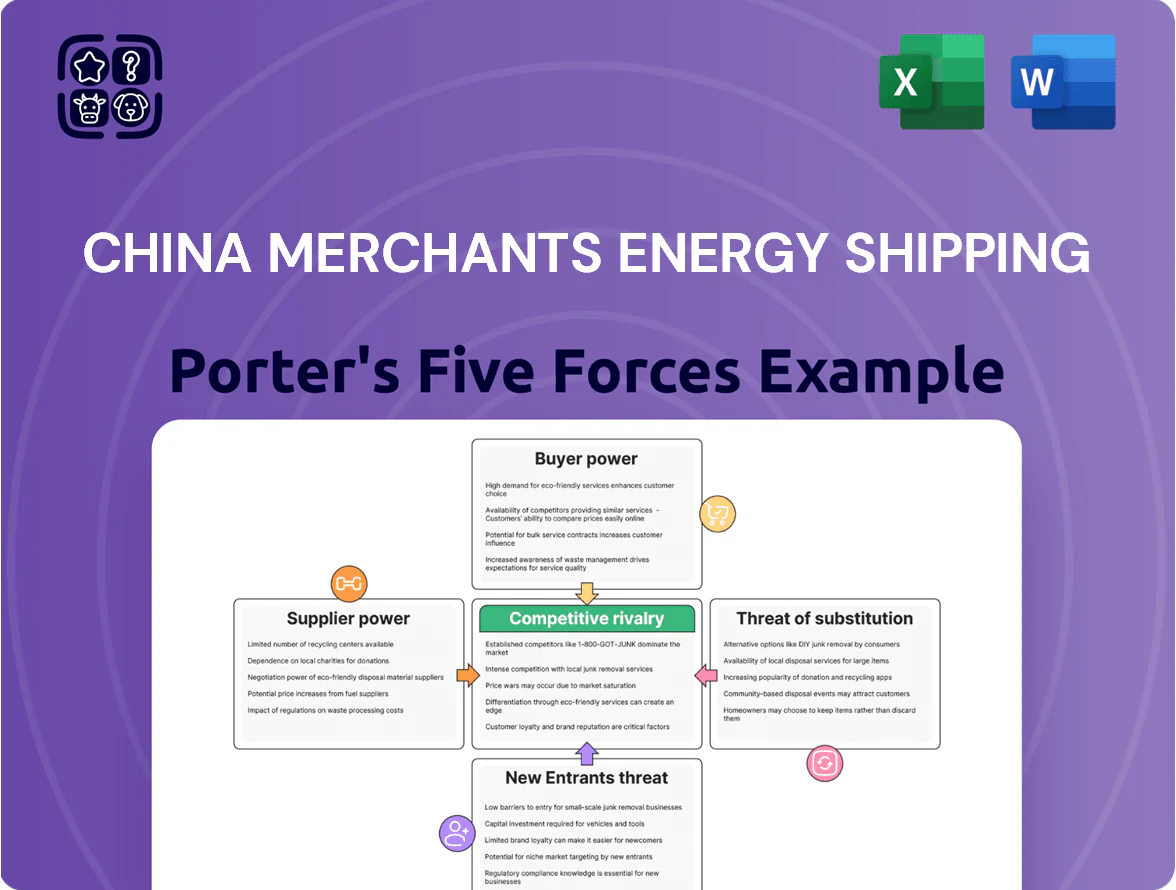

China Merchants Energy Shipping operates in a capital-intensive, cyclical shipping sector where buyer price sensitivity and fuel/supply costs exert strong pressure, while high entry barriers and scale advantages moderate new-entrant threats—this snapshot hints at complex strategic trade-offs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Merchants Energy Shipping’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Shipyard Concentration and Pricing

The global shipbuilding market is concentrated: China, South Korea and Japan built 88% of new tonnage in 2024, cutting CMES bargaining power as yards set prices and terms.

By late 2025 yards charge premiums—reported 15–30% higher—for LNG carriers and methanol-ready tankers to meet IMO/GHG rules, raising CMES capex per vessel.

Concentration lets suppliers dictate delivery schedules and payment terms during 2023–25 fleet renewal peaks; average lead times stretched to 24–36 months and advance payments rose to 20–30%.

Bunker Fuel Price Volatility

Fuel is a top cost for China Merchants Energy Shipping (CMES): bunker accounted for ~28% of operating expenses in 2024, so CMES is tightly exposed to global fuel markets and supplier pricing.

Hedging cuts volatility but the 2020–25 shift to IMO 2020 low-sulfur fuel and growing LNG/HSFO demand raises bargaining power of specialized suppliers with few large refiners controlling supply.

Geopolitical shocks (e.g., 2022–23 supply disruptions from the Black Sea and Red Sea incidents) quickly lift bunker prices; CMES has limited immediate alternatives to traditional or certified green bunkering services.

Specialized Labor and Crewing

The global maritime sector faces a shortage of senior officers and engineers for LNG and VLCC ships; BIMCO/ICS 2024 estimated a gap of 40,000 officers by 2026, boosting supplier leverage. Crewing firms and maritime academies thus command pricing power because CMES’s safety and regulatory compliance hinge on certified personnel. CMES competes globally, pushing seafarer wage inflation—reported 8–12% higher pay for LNG-qualified officers in 2025—and greater use of specialized recruiters.

Financing and Capital Costs

Shipping is capital‑heavy: global fleet financing reached about $210 billion in 2024, and CMES relies on large banks and lease financiers for newbuilds and retrofits.

State‑owned status eases access to Chinese policy banks, but CMES still faces global rate swings (2024 average interbank rates up 150–200 bps) and ESG‑linked loan covenants that raise refinancing costs.

Lenders can force strategic choices—like decommissioning older vessels—to meet credit conditions and carbon targets, affecting fleet renewal timing and capex.

- 2024 ship finance market ≈ $210B

- Interest rates +150–200 bps vs 2023

- ESG covenants tie refinancing to emissions cuts

- Lenders influence decommissioning and capex

Technological and Regulatory Equipment Providers

Suppliers of specialized maritime tech—carbon capture units and advanced navigation software—gain leverage as IMO 2023/2024 rules tighten emissions and EEXI/CII targets; about 70% of deepwater retrofit bids in 2024 cited few qualified vendors, raising supplier power.

As CMES (China Merchants Energy Shipping) adopts digital route-optimization and emission-monitoring, dependence on a small vendor pool rises; replacing integrated ship-management systems can cost 1–3% of vessel value and create weeks of downtime, boosting supplier bargaining power.

- ~70% retrofit bids cite limited vendors

- Switch cost: 1–3% vessel value

- Downtime: weeks per swap

- IMO tightening increased demand 2023–25

Suppliers Tighten the Screws on CMES: Shipyards, Fuel & Crew Create Major Cost Risks

Suppliers hold strong leverage over CMES: concentrated shipyards (China/SK/Japan 88% newbuilds in 2024), long lead times (24–36 months) and 15–30% premiums for LNG/methanol ships raise capex; bunker made ~28% of opex in 2024 with few refiners controlling low‑sulfur/LNG fuel; crewing gaps (BIMCO/ICS gap ~40,000 officers by 2026) and scarce retrofit vendors (≈70% bids cite limited suppliers) further tighten supplier power.

| Metric | Value (year) |

|---|---|

| Shipyard market share | 88% (2024) |

| Lead times | 24–36 months (2023–25) |

| Fuel share of opex | ~28% (2024) |

| Officer shortfall | ~40,000 by 2026 (BIMCO/ICS) |

| Retrofit vendor scarcity | ≈70% bids (2024) |

What is included in the product

Tailored exclusively for China Merchants Energy Shipping, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer influence on pricing, barriers deterring new entrants, threats from substitutes and disruptors, and strategic implications for the company’s market positioning.

A concise Porter's Five Forces one-sheet for China Merchants Energy Shipping—quickly spot competitive pressures, supplier/customer leverage, and regulatory threats to inform swift strategic moves.

Customers Bargaining Power

Concentration of Major Energy Clients

About 60–70% of China Merchants Energy Shipping’s (CMES) bulk crude and product volumes in 2024 came from large state-owned and global majors such as Sinopec and PetroChina, giving these customers strong leverage to demand lower freight and tighter charter terms.

These high-volume clients negotiate long-term contracts that underpin vessel utilization—losing a single major account could cut utilization by 10–20% and hit EBITDA by an estimated 15–25% based on 2024 margins.

Low Switching Costs for Commodity Transport

In the spot market, crude and dry-bulk shipping are treated as commodities, so charterers switch carriers on price; ClarkSea index volatility shows spot rates fell 38% in 2023, forcing CMES to match market pricing to secure cargoes.

Customers compare rates via indices (Baltic Dry Index, TTF) and platforms; over 60% of Asian chartering now uses digital freight platforms, boosting buyer visibility and bargaining power against CMES.

Transparency of Freight Rates

Real-time Baltic Dry Index and tanker-rate feeds (BDI ~1,200 on 2025-12-15; VLCC TC1 average $28,000/day in 2025 H2) give shippers full visibility, eroding CMES’s pricing power.

With rate transparency, customers time cargoes and demand discounts during vessel oversupply—global containership idle tonnage hit ~6.5% in 2025 Q3—so CMES must justify premiums via faster transit, integrated logistics or top safety metrics.

Demand for Green Shipping Solutions

By late 2025, major corporate clients tracking Scope 3 emissions push CMES to offer low-carbon shipping; top shippers now demand newer dual-fuel or scrubber-equipped vessels, threatening contracts with older high-emission tonnage.

This customer power forces CMES to speed CAPEX on green tech—2024–25 industry estimates show retrofit/newbuild costs of $20k–$50k per TEU-equivalent, raising near-term capex needs to stay eligible for top-tier global clients.

- Scope 3 pressure rising among Fortune 500 buyers

- Demand for dual-fuel/LNG, methanol-ready or scrubbed ships

- Retention requires accelerated CAPEX: ~$20k–$50k/TEU-eq

- Older fleet faces contract attrition

Vertical Integration by Cargo Owners

Large miners and energy firms like BHP Group and China Shenhua Energy ran or contracted captive fleets; in 2024 BHP disclosed about 8% of its seaborne coal and iron ore tonnage under long-term charter, showing real backward-integration risk to CMES.

Such vertical integration shrinks CMES's addressable market; if captive shipping handles even 5–10% more volumes, CMES faces direct revenue pressure and lower spot rates for remaining third-party cargoes.

Here’s the quick math: if CMES handled 100 Mtpa and customer-owned fleets take 7 Mtpa, that’s a 7% revenue hit before price effects; churn on contract renewals rises too.

- 2024: BHP ~8% long-term charter exposure

- Scenario: 5–10% captive shift cuts CMES TAM by same amount

- Immediate impact: lower spot rates, higher competition

Concentrated buyers squeeze rates; losing one client could cut EBITDA ~15–25%

Large state-owned and global energy clients supply 60–70% of CMES 2024 volumes, giving them strong leverage to demand lower rates and tighter terms; losing one could cut utilization 10–20% and EBITDA ~15–25% (2024 margins). Spot-price transparency (BDI, ClarkSea; VLCC TC1 ~$28k/day in 2025 H2) and digital chartering (>60% Asia) boost buyer power, while Scope 3 rules push demand for dual‑fuel/low‑carbon tonnage, forcing $20k–$50k/TEU‑eq CAPEX to retain top clients.

| Metric | Value |

|---|---|

| Customer share of volumes (2024) | 60–70% |

| Utilization risk per lost account | 10–20% |

| EBITDA impact estimate | 15–25% |

| VLCC TC1 (2025 H2 avg) | $28,000/day |

| CAPEX for low‑carbon tonnage | $20k–$50k/TEU‑eq |

Preview Before You Purchase

China Merchants Energy Shipping Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Merchants Energy Shipping you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file ready for download and immediate use once you complete payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

China Merchants Energy Shipping operates in a capital-intensive, cyclical shipping sector where buyer price sensitivity and fuel/supply costs exert strong pressure, while high entry barriers and scale advantages moderate new-entrant threats—this snapshot hints at complex strategic trade-offs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Merchants Energy Shipping’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Shipyard Concentration and Pricing

The global shipbuilding market is concentrated: China, South Korea and Japan built 88% of new tonnage in 2024, cutting CMES bargaining power as yards set prices and terms.

By late 2025 yards charge premiums—reported 15–30% higher—for LNG carriers and methanol-ready tankers to meet IMO/GHG rules, raising CMES capex per vessel.

Concentration lets suppliers dictate delivery schedules and payment terms during 2023–25 fleet renewal peaks; average lead times stretched to 24–36 months and advance payments rose to 20–30%.

Bunker Fuel Price Volatility

Fuel is a top cost for China Merchants Energy Shipping (CMES): bunker accounted for ~28% of operating expenses in 2024, so CMES is tightly exposed to global fuel markets and supplier pricing.

Hedging cuts volatility but the 2020–25 shift to IMO 2020 low-sulfur fuel and growing LNG/HSFO demand raises bargaining power of specialized suppliers with few large refiners controlling supply.

Geopolitical shocks (e.g., 2022–23 supply disruptions from the Black Sea and Red Sea incidents) quickly lift bunker prices; CMES has limited immediate alternatives to traditional or certified green bunkering services.

Specialized Labor and Crewing

The global maritime sector faces a shortage of senior officers and engineers for LNG and VLCC ships; BIMCO/ICS 2024 estimated a gap of 40,000 officers by 2026, boosting supplier leverage. Crewing firms and maritime academies thus command pricing power because CMES’s safety and regulatory compliance hinge on certified personnel. CMES competes globally, pushing seafarer wage inflation—reported 8–12% higher pay for LNG-qualified officers in 2025—and greater use of specialized recruiters.

Financing and Capital Costs

Shipping is capital‑heavy: global fleet financing reached about $210 billion in 2024, and CMES relies on large banks and lease financiers for newbuilds and retrofits.

State‑owned status eases access to Chinese policy banks, but CMES still faces global rate swings (2024 average interbank rates up 150–200 bps) and ESG‑linked loan covenants that raise refinancing costs.

Lenders can force strategic choices—like decommissioning older vessels—to meet credit conditions and carbon targets, affecting fleet renewal timing and capex.

- 2024 ship finance market ≈ $210B

- Interest rates +150–200 bps vs 2023

- ESG covenants tie refinancing to emissions cuts

- Lenders influence decommissioning and capex

Technological and Regulatory Equipment Providers

Suppliers of specialized maritime tech—carbon capture units and advanced navigation software—gain leverage as IMO 2023/2024 rules tighten emissions and EEXI/CII targets; about 70% of deepwater retrofit bids in 2024 cited few qualified vendors, raising supplier power.

As CMES (China Merchants Energy Shipping) adopts digital route-optimization and emission-monitoring, dependence on a small vendor pool rises; replacing integrated ship-management systems can cost 1–3% of vessel value and create weeks of downtime, boosting supplier bargaining power.

- ~70% retrofit bids cite limited vendors

- Switch cost: 1–3% vessel value

- Downtime: weeks per swap

- IMO tightening increased demand 2023–25

Suppliers Tighten the Screws on CMES: Shipyards, Fuel & Crew Create Major Cost Risks

Suppliers hold strong leverage over CMES: concentrated shipyards (China/SK/Japan 88% newbuilds in 2024), long lead times (24–36 months) and 15–30% premiums for LNG/methanol ships raise capex; bunker made ~28% of opex in 2024 with few refiners controlling low‑sulfur/LNG fuel; crewing gaps (BIMCO/ICS gap ~40,000 officers by 2026) and scarce retrofit vendors (≈70% bids cite limited suppliers) further tighten supplier power.

| Metric | Value (year) |

|---|---|

| Shipyard market share | 88% (2024) |

| Lead times | 24–36 months (2023–25) |

| Fuel share of opex | ~28% (2024) |

| Officer shortfall | ~40,000 by 2026 (BIMCO/ICS) |

| Retrofit vendor scarcity | ≈70% bids (2024) |

What is included in the product

Tailored exclusively for China Merchants Energy Shipping, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer influence on pricing, barriers deterring new entrants, threats from substitutes and disruptors, and strategic implications for the company’s market positioning.

A concise Porter's Five Forces one-sheet for China Merchants Energy Shipping—quickly spot competitive pressures, supplier/customer leverage, and regulatory threats to inform swift strategic moves.

Customers Bargaining Power

Concentration of Major Energy Clients

About 60–70% of China Merchants Energy Shipping’s (CMES) bulk crude and product volumes in 2024 came from large state-owned and global majors such as Sinopec and PetroChina, giving these customers strong leverage to demand lower freight and tighter charter terms.

These high-volume clients negotiate long-term contracts that underpin vessel utilization—losing a single major account could cut utilization by 10–20% and hit EBITDA by an estimated 15–25% based on 2024 margins.

Low Switching Costs for Commodity Transport

In the spot market, crude and dry-bulk shipping are treated as commodities, so charterers switch carriers on price; ClarkSea index volatility shows spot rates fell 38% in 2023, forcing CMES to match market pricing to secure cargoes.

Customers compare rates via indices (Baltic Dry Index, TTF) and platforms; over 60% of Asian chartering now uses digital freight platforms, boosting buyer visibility and bargaining power against CMES.

Transparency of Freight Rates

Real-time Baltic Dry Index and tanker-rate feeds (BDI ~1,200 on 2025-12-15; VLCC TC1 average $28,000/day in 2025 H2) give shippers full visibility, eroding CMES’s pricing power.

With rate transparency, customers time cargoes and demand discounts during vessel oversupply—global containership idle tonnage hit ~6.5% in 2025 Q3—so CMES must justify premiums via faster transit, integrated logistics or top safety metrics.

Demand for Green Shipping Solutions

By late 2025, major corporate clients tracking Scope 3 emissions push CMES to offer low-carbon shipping; top shippers now demand newer dual-fuel or scrubber-equipped vessels, threatening contracts with older high-emission tonnage.

This customer power forces CMES to speed CAPEX on green tech—2024–25 industry estimates show retrofit/newbuild costs of $20k–$50k per TEU-equivalent, raising near-term capex needs to stay eligible for top-tier global clients.

- Scope 3 pressure rising among Fortune 500 buyers

- Demand for dual-fuel/LNG, methanol-ready or scrubbed ships

- Retention requires accelerated CAPEX: ~$20k–$50k/TEU-eq

- Older fleet faces contract attrition

Vertical Integration by Cargo Owners

Large miners and energy firms like BHP Group and China Shenhua Energy ran or contracted captive fleets; in 2024 BHP disclosed about 8% of its seaborne coal and iron ore tonnage under long-term charter, showing real backward-integration risk to CMES.

Such vertical integration shrinks CMES's addressable market; if captive shipping handles even 5–10% more volumes, CMES faces direct revenue pressure and lower spot rates for remaining third-party cargoes.

Here’s the quick math: if CMES handled 100 Mtpa and customer-owned fleets take 7 Mtpa, that’s a 7% revenue hit before price effects; churn on contract renewals rises too.

- 2024: BHP ~8% long-term charter exposure

- Scenario: 5–10% captive shift cuts CMES TAM by same amount

- Immediate impact: lower spot rates, higher competition

Concentrated buyers squeeze rates; losing one client could cut EBITDA ~15–25%

Large state-owned and global energy clients supply 60–70% of CMES 2024 volumes, giving them strong leverage to demand lower rates and tighter terms; losing one could cut utilization 10–20% and EBITDA ~15–25% (2024 margins). Spot-price transparency (BDI, ClarkSea; VLCC TC1 ~$28k/day in 2025 H2) and digital chartering (>60% Asia) boost buyer power, while Scope 3 rules push demand for dual‑fuel/low‑carbon tonnage, forcing $20k–$50k/TEU‑eq CAPEX to retain top clients.

| Metric | Value |

|---|---|

| Customer share of volumes (2024) | 60–70% |

| Utilization risk per lost account | 10–20% |

| EBITDA impact estimate | 15–25% |

| VLCC TC1 (2025 H2 avg) | $28,000/day |

| CAPEX for low‑carbon tonnage | $20k–$50k/TEU‑eq |

Preview Before You Purchase

China Merchants Energy Shipping Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Merchants Energy Shipping you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file ready for download and immediate use once you complete payment.