China Merchants Land Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

China Merchants Land faces moderate competitive intensity—scale and integrated port-logistics assets limit new entrants while cyclical property markets and regulatory shifts heighten buyer and supplier pressures; substitutes and rivalry vary by region and asset mix. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Merchants Land’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Local Government Control of Land Supply

The Chinese state is the sole land supplier, so municipal governments hold absolute leverage over China Merchants Land (CML), controlling site allocation and auction timing; in 2024 local land transfer revenue hit Rmb4.6 trillion, shaping developers’ access and costs.

Land prices and supply follow state urban plans and fiscal needs, not pure market demand, so CML must align projects with central goals like the 14th Five-Year Plan to win prime sites and favorable terms.

Access to State-Backed Financing

Despite China Merchants Land being a state-owned enterprise subsidiary, banks still control credit via quotas and loan-rate moves; China’s commercial bank outstanding property loans fell 5.2% YoY in 2024, tightening available funding.

The People’s Bank legacy of the Three Red Lines (debt caps for developers) suppressed developer lending through 2023–24, keeping project financing scarce and pricier.

As a result, debt cost and availability — weighted-average borrowing costs near 5.5% for developers in 2024 — directly limit CML’s expansion speed and project cadence.

Construction Material Price Volatility

Suppliers of steel, cement and glass trade on volatile global commodity markets; steel spot prices rose ~12% in 2024 and Chinese cement prices jumped ~8% year-on-year to Q4 2024, so CML’s scale helps secure volume discounts but cannot fully absorb these inflationary swings. Suppliers are critical to project completion, so any supply-chain disruption—recall 2021 port slowdowns that delayed projects by 3–6 months—directly shifts CML delivery timelines and capex schedules.

Rising Costs of Specialized Labor

The shrinking pool of skilled construction labor in China raised bargaining power of large EPC firms for CML in 2025; China construction sector skilled vacancies grew 12% YoY in 2024 per Ministry of Human Resources, forcing contractors to demand higher rates.

CML depends on these specialist contractors for complex designs and safety compliance, so rising wage expectations mean CML pays a premium to keep schedules and quality—industry wage inflation was ~8–10% in 2024.

- Skilled vacancies +12% YoY (2024)

- Industry wage inflation ~8–10% (2024)

- Contractor leverage ↑ leads to higher project margins risk

Integration of Smart Building Technology

As China Merchants Land shifts into smart homes and green buildings, specialized tech suppliers gain bargaining power by supplying proprietary IoT and BMS (building management systems) that lock into designs; global smart-building market grew to $93.6B in 2024, pushing vendor influence.

These systems are costly to swap and create dependency for long-term maintenance and upgrades across CML’s residential and commercial assets, raising OPEX and vendor negotiation risk.

- 2024 smart-building market: $93.6B

- Proprietary BMS raise switching costs

- Heightened vendor leverage on OPEX

- Dependency across CML portfolios

China Merchants Land squeezed: land leverage, tight credit and rising costs hit 2024 margins

State land sellers and municipal fiscal needs give suppliers outsized leverage over China Merchants Land; 2024 local land transfers reached Rmb4.6tn, so site access and price depend on aligning with policy.

Bank credit tightened—property loans down 5.2% YoY (2024) and developer borrowing ~5.5%—raising financing costs; material and labor inflation (steel +12%, cement +8%, skilled vacancies +12%, wages +8–10% in 2024) further squeeze margins.

| Metric | 2024 value |

|---|---|

| Local land transfer revenue | Rmb4.6tn |

| Outstanding property loans YoY | -5.2% |

| Developer borrowing cost | ~5.5% |

| Steel price change | +12% |

| Cement price change | +8% |

| Skilled vacancies | +12% YoY |

| Wage inflation | 8–10% |

What is included in the product

Tailored Five Forces analysis for China Merchants Land that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic vulnerabilities to inform investor decks, strategic plans, and academic projects.

A concise Porter's Five Forces snapshot for China Merchants Land that highlights competitive intensity, supplier/buyer leverage, threat of new entrants and substitutes—ideal for fast, board-ready decisions and strategic gap-spotting.

Customers Bargaining Power

High Sensitivity to Mortgage Rates

Individual homebuyers in 2025 show high sensitivity to mortgage rates and down payment rules; a 25 bps hike or a 5% rise in required down payment cuts purchase intent by ~8–12%, per China real-estate surveys in 2024–25. Buyers are delaying purchases waiting for policy easing or price drops, lowering first-quarter presales 2025 by ~15% year-on-year for many developers. Collective pause gives customers leverage to demand price cuts, better financing, or flexible deposits that can quickly choke a developer’s cash flow.

Increased Transparency via Digital Platforms

The rise of property apps and social media in China lets buyers compare prices, floorplans, and developer ratings instantly, shrinking the info gap developers once used to keep margins high. In 2024, 68% of urban homebuyers used online listings and forums for research, so negotiation leverage shifted toward customers. Buyers now demand better finishes and tie discounts to market benchmarks, forcing China Merchants Land to match or risk slower sales velocity. This transparency pressures gross margins and sales prices.

Availability of Alternative Housing Options

With China’s property market stabilizing in 2024–2025, new-home supply fell 8.2% YoY while secondary-market transactions rose 14% in 2025, widening buyer choice; low switching costs mean buyers will move from China Merchants Land to rivals or resales if pricing or location aren’t compelling.

Collective Action through Homeowners Associations

Post-purchase, homeowners associations (HOAs) wield strong leverage by monitoring property management; 2024 China real-estate surveys show 42% of urban HOAs filed formal complaints over service standards, raising reputational risk for China Merchants Land (CML).

Negative HOA-led feedback or lawsuits sharply reduce local sales—projects with HOA disputes saw average 18% slower presales in the same city within 12 months, so CML must keep satisfaction high to avoid organized buyer resistance.

- HOA complaints: 42% (2024 urban survey)

- Sales impact: −18% presales within 12 months when disputes occur

- Action: prioritize property management KPIs and rapid dispute resolution

Leverage of Large Institutional Tenants

- 2024 CBD vacancy 18–22%

- Typical concessions: 6–18 months rent-free

- Anchor loss → valuation drop 15–30%

- Tenants push tailored fit-outs, flexible breaks

Buyers’ leverage surges: presales fall, resales rise, CBD vacancies force concessions

Buyers hold strong leverage: mortgage/downpayment tweaks cut intent 8–12% (2024–25 surveys); 2025 Q1 presales fell ~15% YoY as buyers waited. Online research (68% in 2024) and rising resales (+14% 2025) lower switching costs, pressuring prices and margins; HOAs filed complaints 42% (2024) and disputes cut presales ~18% in 12 months. Commercial tenants exploit 18–22% CBD vacancy (2024) to secure 6–18 months concessions; anchor exits drop valuations 15–30%.

| Metric | Value |

|---|---|

| Buyer online research (2024) | 68% |

| Presales change Q1 2025 YoY | −15% |

| Resales change (2025) | +14% |

| HOA complaints (2024) | 42% |

| Presales impact from disputes | −18% (12m) |

| CBD vacancy (2024) | 18–22% |

| Typical tenant concessions | 6–18 months rent‑free |

| Anchor exit valuation hit | 15–30% |

Preview the Actual Deliverable

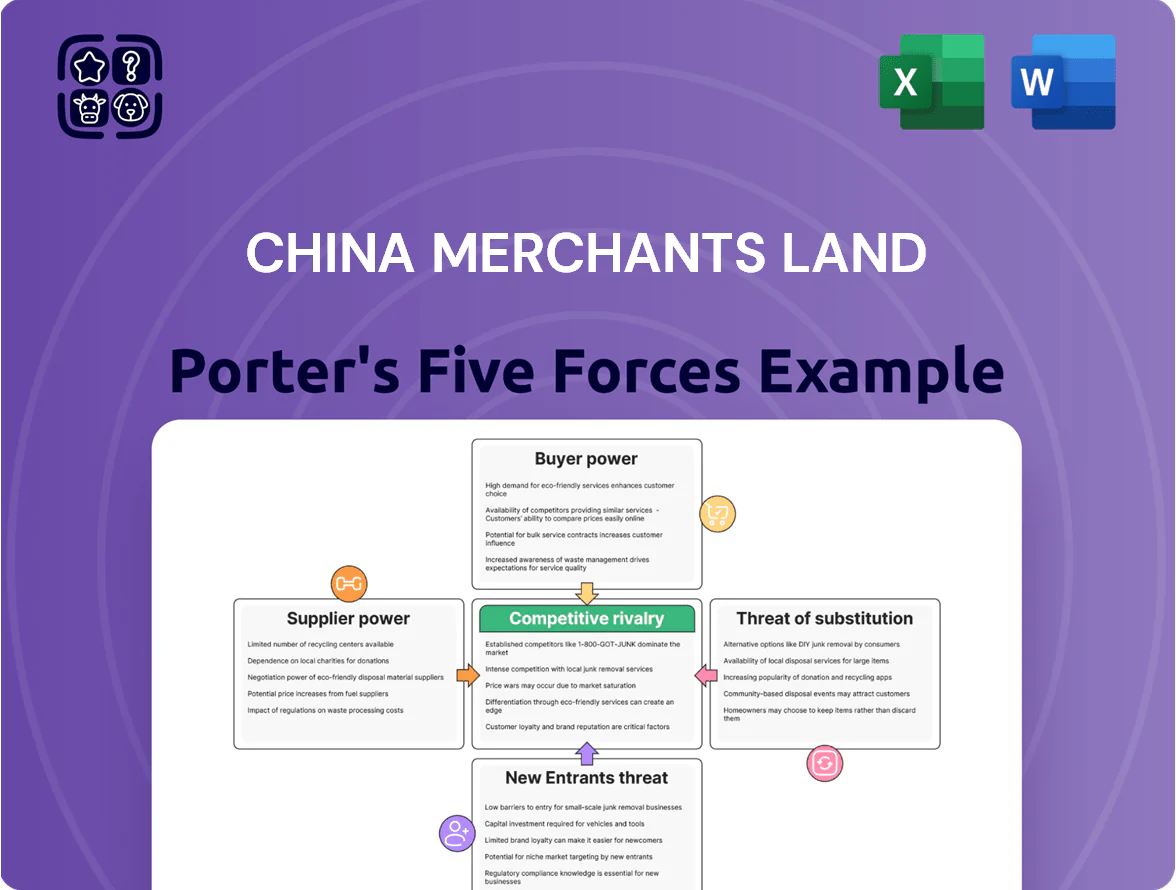

China Merchants Land Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China Merchants Land you'll receive immediately after purchase—no surprises, no placeholders. The document is the professionally written, fully formatted deliverable, ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute threats. Instant access to this exact file is granted upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

China Merchants Land faces moderate competitive intensity—scale and integrated port-logistics assets limit new entrants while cyclical property markets and regulatory shifts heighten buyer and supplier pressures; substitutes and rivalry vary by region and asset mix. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Merchants Land’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Local Government Control of Land Supply

The Chinese state is the sole land supplier, so municipal governments hold absolute leverage over China Merchants Land (CML), controlling site allocation and auction timing; in 2024 local land transfer revenue hit Rmb4.6 trillion, shaping developers’ access and costs.

Land prices and supply follow state urban plans and fiscal needs, not pure market demand, so CML must align projects with central goals like the 14th Five-Year Plan to win prime sites and favorable terms.

Access to State-Backed Financing

Despite China Merchants Land being a state-owned enterprise subsidiary, banks still control credit via quotas and loan-rate moves; China’s commercial bank outstanding property loans fell 5.2% YoY in 2024, tightening available funding.

The People’s Bank legacy of the Three Red Lines (debt caps for developers) suppressed developer lending through 2023–24, keeping project financing scarce and pricier.

As a result, debt cost and availability — weighted-average borrowing costs near 5.5% for developers in 2024 — directly limit CML’s expansion speed and project cadence.

Construction Material Price Volatility

Suppliers of steel, cement and glass trade on volatile global commodity markets; steel spot prices rose ~12% in 2024 and Chinese cement prices jumped ~8% year-on-year to Q4 2024, so CML’s scale helps secure volume discounts but cannot fully absorb these inflationary swings. Suppliers are critical to project completion, so any supply-chain disruption—recall 2021 port slowdowns that delayed projects by 3–6 months—directly shifts CML delivery timelines and capex schedules.

Rising Costs of Specialized Labor

The shrinking pool of skilled construction labor in China raised bargaining power of large EPC firms for CML in 2025; China construction sector skilled vacancies grew 12% YoY in 2024 per Ministry of Human Resources, forcing contractors to demand higher rates.

CML depends on these specialist contractors for complex designs and safety compliance, so rising wage expectations mean CML pays a premium to keep schedules and quality—industry wage inflation was ~8–10% in 2024.

- Skilled vacancies +12% YoY (2024)

- Industry wage inflation ~8–10% (2024)

- Contractor leverage ↑ leads to higher project margins risk

Integration of Smart Building Technology

As China Merchants Land shifts into smart homes and green buildings, specialized tech suppliers gain bargaining power by supplying proprietary IoT and BMS (building management systems) that lock into designs; global smart-building market grew to $93.6B in 2024, pushing vendor influence.

These systems are costly to swap and create dependency for long-term maintenance and upgrades across CML’s residential and commercial assets, raising OPEX and vendor negotiation risk.

- 2024 smart-building market: $93.6B

- Proprietary BMS raise switching costs

- Heightened vendor leverage on OPEX

- Dependency across CML portfolios

China Merchants Land squeezed: land leverage, tight credit and rising costs hit 2024 margins

State land sellers and municipal fiscal needs give suppliers outsized leverage over China Merchants Land; 2024 local land transfers reached Rmb4.6tn, so site access and price depend on aligning with policy.

Bank credit tightened—property loans down 5.2% YoY (2024) and developer borrowing ~5.5%—raising financing costs; material and labor inflation (steel +12%, cement +8%, skilled vacancies +12%, wages +8–10% in 2024) further squeeze margins.

| Metric | 2024 value |

|---|---|

| Local land transfer revenue | Rmb4.6tn |

| Outstanding property loans YoY | -5.2% |

| Developer borrowing cost | ~5.5% |

| Steel price change | +12% |

| Cement price change | +8% |

| Skilled vacancies | +12% YoY |

| Wage inflation | 8–10% |

What is included in the product

Tailored Five Forces analysis for China Merchants Land that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic vulnerabilities to inform investor decks, strategic plans, and academic projects.

A concise Porter's Five Forces snapshot for China Merchants Land that highlights competitive intensity, supplier/buyer leverage, threat of new entrants and substitutes—ideal for fast, board-ready decisions and strategic gap-spotting.

Customers Bargaining Power

High Sensitivity to Mortgage Rates

Individual homebuyers in 2025 show high sensitivity to mortgage rates and down payment rules; a 25 bps hike or a 5% rise in required down payment cuts purchase intent by ~8–12%, per China real-estate surveys in 2024–25. Buyers are delaying purchases waiting for policy easing or price drops, lowering first-quarter presales 2025 by ~15% year-on-year for many developers. Collective pause gives customers leverage to demand price cuts, better financing, or flexible deposits that can quickly choke a developer’s cash flow.

Increased Transparency via Digital Platforms

The rise of property apps and social media in China lets buyers compare prices, floorplans, and developer ratings instantly, shrinking the info gap developers once used to keep margins high. In 2024, 68% of urban homebuyers used online listings and forums for research, so negotiation leverage shifted toward customers. Buyers now demand better finishes and tie discounts to market benchmarks, forcing China Merchants Land to match or risk slower sales velocity. This transparency pressures gross margins and sales prices.

Availability of Alternative Housing Options

With China’s property market stabilizing in 2024–2025, new-home supply fell 8.2% YoY while secondary-market transactions rose 14% in 2025, widening buyer choice; low switching costs mean buyers will move from China Merchants Land to rivals or resales if pricing or location aren’t compelling.

Collective Action through Homeowners Associations

Post-purchase, homeowners associations (HOAs) wield strong leverage by monitoring property management; 2024 China real-estate surveys show 42% of urban HOAs filed formal complaints over service standards, raising reputational risk for China Merchants Land (CML).

Negative HOA-led feedback or lawsuits sharply reduce local sales—projects with HOA disputes saw average 18% slower presales in the same city within 12 months, so CML must keep satisfaction high to avoid organized buyer resistance.

- HOA complaints: 42% (2024 urban survey)

- Sales impact: −18% presales within 12 months when disputes occur

- Action: prioritize property management KPIs and rapid dispute resolution

Leverage of Large Institutional Tenants

- 2024 CBD vacancy 18–22%

- Typical concessions: 6–18 months rent-free

- Anchor loss → valuation drop 15–30%

- Tenants push tailored fit-outs, flexible breaks

Buyers’ leverage surges: presales fall, resales rise, CBD vacancies force concessions

Buyers hold strong leverage: mortgage/downpayment tweaks cut intent 8–12% (2024–25 surveys); 2025 Q1 presales fell ~15% YoY as buyers waited. Online research (68% in 2024) and rising resales (+14% 2025) lower switching costs, pressuring prices and margins; HOAs filed complaints 42% (2024) and disputes cut presales ~18% in 12 months. Commercial tenants exploit 18–22% CBD vacancy (2024) to secure 6–18 months concessions; anchor exits drop valuations 15–30%.

| Metric | Value |

|---|---|

| Buyer online research (2024) | 68% |

| Presales change Q1 2025 YoY | −15% |

| Resales change (2025) | +14% |

| HOA complaints (2024) | 42% |

| Presales impact from disputes | −18% (12m) |

| CBD vacancy (2024) | 18–22% |

| Typical tenant concessions | 6–18 months rent‑free |

| Anchor exit valuation hit | 15–30% |

Preview the Actual Deliverable

China Merchants Land Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China Merchants Land you'll receive immediately after purchase—no surprises, no placeholders. The document is the professionally written, fully formatted deliverable, ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute threats. Instant access to this exact file is granted upon payment.