CMOC Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

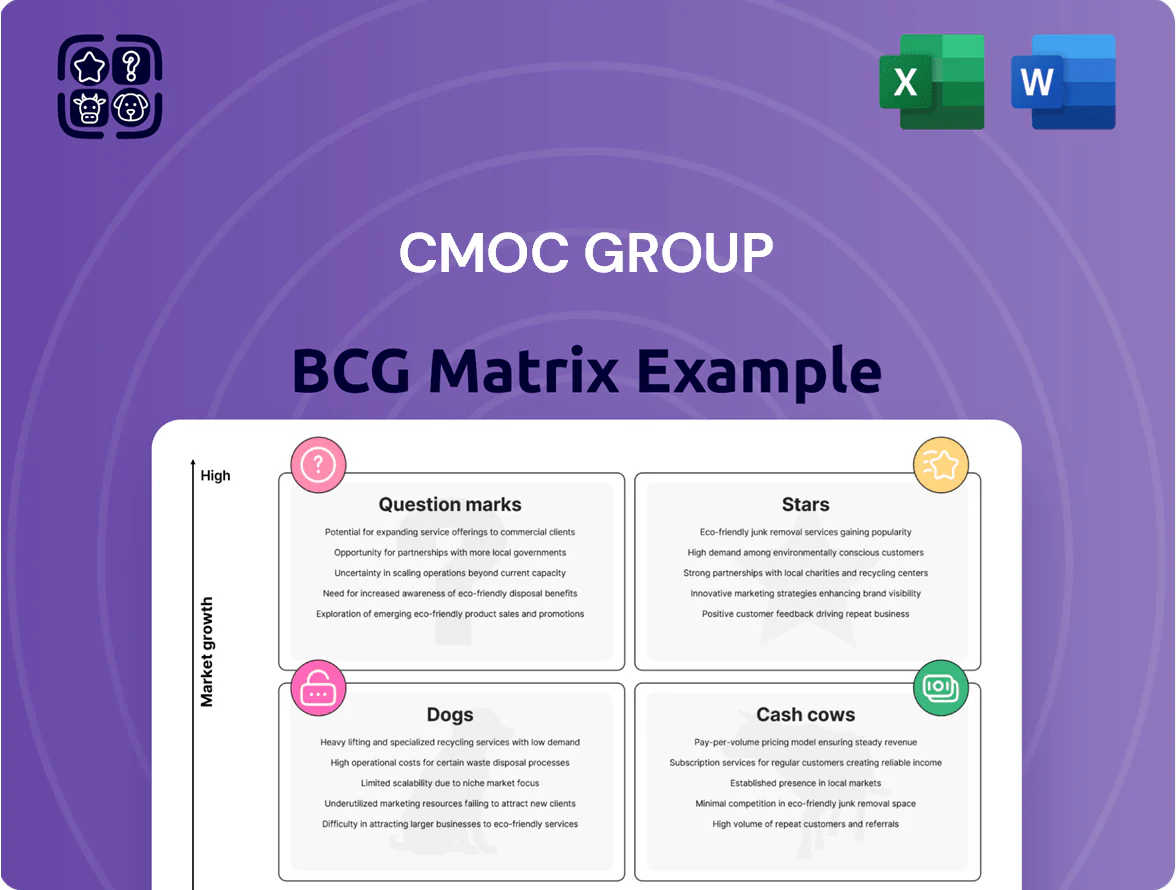

CMOC Group’s BCG Matrix preview highlights where key divisions fall amid shifting commodity cycles—identifying potential Stars in high-growth lithium and established Cash Cows in copper, while flagging lower-growth assets as Dogs or Question Marks. This snapshot frames strategic options for capital allocation and portfolio optimization. Purchase the full BCG Matrix to receive quadrant-by-quadrant placements, data-driven recommendations, and editable Word and Excel deliverables to guide investment and operational decisions.

Stars

TFM and KFM Copper Operations

By end-2025 CMOC (China Molybdenum Co., listed 3993.HK) cemented top-tier status after Tenke Fungurume (TFM) and Kisanfu (KFM) expansions lifted combined copper production to roughly 700 kt Cu eq in 2025, up ~60% vs 2022, capturing an estimated 4–5% of global refined copper supply.

Copper demand stayed strong—IEA and S&P Global projecting 2026 demand growth ~4–5% CAGR 2023–30—driven by EVs (global stock 26.6M in 2025), grid upgrades, and renewables, keeping prices supported (LME average ~US$8,900/t in 2025).

TFM and KFM now sit in the BCG Matrix Stars quadrant: high market growth and high market share, but they require substantial reinvestment—CMOC reported 2025 sustaining and expansion capex near US$1.1–1.3bn—to preserve throughput and tech advantages like SX-EW and automation.

Global Cobalt Market Leadership

By 2025 CMOC Group became the world’s largest cobalt producer, supplying roughly 28% of refined cobalt used in high-density lithium-ion batteries, a critical input for EVs and grid storage.

The booming EV market, growing at ~30% CAGR 2020–25, keeps cobalt demand high, and CMOC’s vertical integration—from mining to refining—cuts costs and secures feedstock, boosting margin resilience.

Despite huge revenues (2024 pro forma cobalt sales ~US$3.1bn), operations tie up cash—logistics, refinery capex, and ESG spending (≈US$220m in 2024)—pressuring free cash flow while sustaining star growth.

Next-Generation ESG Mining Standards

CMOC’s Next-Generation ESG Mining Standards position it as a Star: CMOC invested ~USD 420m (2023–2025) in green mining tech and secured 60% renewable power for African sites, meeting OEM low-carbon sourcing thresholds and capturing rising demand for battery metals.

Digital Mining and AI Integration

Implementing autonomous hauling and AI-driven ore processing raised throughput by ~18% and reduced unit costs by 12% at CMOC’s Tenke and Catoca sites in 2024, lifting EBITDA margin contribution from these projects by an estimated $160M annually.

The global smart mining market grew 22% YoY to $16.5B in 2024; demand for automation to cut opex and improve safety supports CMOC’s scaling strategy and lowers lost-time incidents by ~35%.

CMOC’s early, large-scale deployments position it as a frontrunner in mining modernization, improving yield, cutting costs, and creating optionality for premium metal recovery and longer mine life.

- Throughput +18%

- Unit cost -12%

- EBITDA boost ~$160M/yr

- Smart mining market $16.5B (2024), +22% YoY

- Lost-time incidents -35%

Strategic Resource Expansion in DRC

Continued exploration and brownfield development around CMOC Group’s DRC concessions target ~2–4 Mtpa of copper-equivalent production growth and could add an estimated 500–900 kt of high-grade reserves by 2030, keeping CMOC a top-three battery-metal supplier in Africa.

Securing these reserves anchors CMOC’s decade-long market share in battery metals; projects need upfront capital of ~US$800m–1.2bn per major brownfield phase but are forecast to turn cash-positive within 3–5 years of ramp-up.

These initiatives fit the BCG Stars slot: high market growth, high relative share, heavy early capex, and future strong free cash flow once unit costs fall with scale.

- Expected reserve add: 500–900 kt Cu-eq by 2030

- Capex per phase: ~US$800m–1.2bn

- Payback: 3–5 years post-ramp

- Target growth: 2–4 Mtpa Cu-eq production lift

TFM/KFM: 2025 BCG Stars—~700kt Cu-eq, 28% cobalt, automation cuts costs, +500–900kt by 2030

TFM/KFM are BCG Stars: 2025 combined ~700 kt Cu-eq (+60% vs 2022), ~4–5% global refined copper; 2025 capex ~US$1.1–1.3bn; cobalt supply ~28% global refined (2025); automation lifted throughput +18%, unit costs -12%, EBITDA +~US$160M/yr; brownfield adds 500–900 kt Cu-eq by 2030 (capex ~US$800m–1.2bn, payback 3–5 yrs).

| Metric | 2025/Target |

|---|---|

| Cu-eq prod | ~700 kt |

| Capex (2025) | US$1.1–1.3bn |

| Cobalt share | ~28% |

| Throughput | +18% |

| Unit cost | -12% |

| Reserve add | 500–900 kt by 2030 |

What is included in the product

Comprehensive BCG Matrix review of CMOC’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page CMOC Group BCG Matrix placing each business unit in a quadrant for swift portfolio decisions

Cash Cows

Molybdenum and Tungsten Operations

CMOC controls ~25% of China’s molybdenum concentrate output and ~15% of global tungsten concentrate via Sandaozhuang and related assets, producing ~30 kt Mo-equivalent and ~20 kt W-equivalent in 2024; those cash cows yield EBITDA margins near 40%, supporting steady free cash flow.

Niobium Production in Brazil

CMOC Group’s Brazilian niobium assets hold ~80% global market share in niobium (2024 estimate), selling into mature high-strength alloy markets and generating steady EBITDA margins near 40%—producing roughly $320m free cash flow in 2024 from low capex operations.

Phosphate Fertilizer Business

The phosphate fertilizer business in Brazil leverages a mature market with annual fertilizer demand near 20 million tonnes in 2024, giving CMOC predictable regional sales. CMOC holds a top-3 national position and reported phosphate segment EBITDA margins around 28% in FY2024, reflecting high operational efficiency. Output volumes stayed stable at ~1.2 million tonnes P2O5 equivalent in 2024, making it a defensive cash cow versus volatile tech-metal units. This unit delivered roughly $220 million in operating cash flow in 2024, cushioning group earnings.

IXM Global Trading Platform

IXM Global Trading, CMOC Group’s metals trading arm, delivers stable, high-volume revenue by trading ore and refined metals from CMOC’s ~1.2 Mt copper-equivalent annual production and third-party flows; in 2024 IXM reported >$5.0bn in gross merchandise value, underpinning low-margins but steady cash.

As a mature trading unit, IXM offers market access and hedging services with modest incremental capital; its operating leverage helps smooth CMOC’s capex swings—trading liquidity funded ~15–20% of CMOC’s 2024 free cash flow needs.

- High-volume revenue: >$5.0bn GMV (2024)

- Supports ~1.2 Mt copper-equivalent supply

- Low incremental capex, mature margins

- Provides 15–20% of 2024 free cash flow coverage

Established Domestic Chinese Refining

CMOCs established Chinese refining and processing units operate in mature industrial hubs with optimized unit costs; in 2024 these domestic plants delivered an estimated RMB 3.1 billion in operating cash flow, reflecting steady margins and local market leadership.

High regional market share and low capex needs—routine maintenance capex ~RMB 150–200 million annually in 2024—make these cash cows funding CMOCs international expansion and R&D into battery and specialty-mineral applications.

- 2024 operating cash flow ~RMB 3.1bn

- Routine maintenance capex RMB 150–200m/yr

- High regional market share in concentrate-to-refine chain

- Funds earmarked for overseas M&A and mineral-R&D

CMOC 2024: High-EBITDA moly/tungsten & dominant niobium fuel $1B+ FCF engine

CMOC cash cows (2024): moly/tungsten ~30 kt Mo-eq/20 kt W-eq, EBITDA ~40%; Brazilian niobium ~80% share, ~$320m FCF; Brazilian phosphate ~1.2 Mt P2O5, EBITDA ~28%, ~$220m OCF; IXM GMV >$5.0bn, funds 15–20% FCF; China refining OCF ~RMB 3.1bn, maintenance capex RMB150–200m.

| Unit | Key 2024 data | Cash/FCF |

|---|---|---|

| Moly/Tungsten | 30 kt Mo-eq /20 kt W-eq; 40% EBITDA | Steady |

| Niobium (Brazil) | ~80% global; low capex | $320m FCF |

| Phosphate (Brazil) | 1.2 Mt P2O5; 28% EBITDA | $220m OCF |

| IXM Trading | >$5.0bn GMV | 15–20% FCF cover |

| China refineries | OCF RMB 3.1bn; capex 150–200m | Funds growth |

What You’re Viewing Is Included

CMOC Group BCG Matrix

The file you're previewing on this page is the final CMOC Group BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

This preview is the exact same BCG Matrix document sent to your inbox post-purchase, crafted with market-backed insights and ready for immediate editing, printing, or presentation—no surprises, no revisions needed.

What you see is the actual CMOC Group BCG Matrix file included with your one-time purchase; professionally designed by strategy experts and formatted for seamless integration into planning, decks, or client briefings.

You're viewing the real deliverable: a polished, ready-to-use BCG Matrix report that becomes instantly downloadable after payment, enabling immediate application in competitive and portfolio analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

CMOC Group’s BCG Matrix preview highlights where key divisions fall amid shifting commodity cycles—identifying potential Stars in high-growth lithium and established Cash Cows in copper, while flagging lower-growth assets as Dogs or Question Marks. This snapshot frames strategic options for capital allocation and portfolio optimization. Purchase the full BCG Matrix to receive quadrant-by-quadrant placements, data-driven recommendations, and editable Word and Excel deliverables to guide investment and operational decisions.

Stars

TFM and KFM Copper Operations

By end-2025 CMOC (China Molybdenum Co., listed 3993.HK) cemented top-tier status after Tenke Fungurume (TFM) and Kisanfu (KFM) expansions lifted combined copper production to roughly 700 kt Cu eq in 2025, up ~60% vs 2022, capturing an estimated 4–5% of global refined copper supply.

Copper demand stayed strong—IEA and S&P Global projecting 2026 demand growth ~4–5% CAGR 2023–30—driven by EVs (global stock 26.6M in 2025), grid upgrades, and renewables, keeping prices supported (LME average ~US$8,900/t in 2025).

TFM and KFM now sit in the BCG Matrix Stars quadrant: high market growth and high market share, but they require substantial reinvestment—CMOC reported 2025 sustaining and expansion capex near US$1.1–1.3bn—to preserve throughput and tech advantages like SX-EW and automation.

Global Cobalt Market Leadership

By 2025 CMOC Group became the world’s largest cobalt producer, supplying roughly 28% of refined cobalt used in high-density lithium-ion batteries, a critical input for EVs and grid storage.

The booming EV market, growing at ~30% CAGR 2020–25, keeps cobalt demand high, and CMOC’s vertical integration—from mining to refining—cuts costs and secures feedstock, boosting margin resilience.

Despite huge revenues (2024 pro forma cobalt sales ~US$3.1bn), operations tie up cash—logistics, refinery capex, and ESG spending (≈US$220m in 2024)—pressuring free cash flow while sustaining star growth.

Next-Generation ESG Mining Standards

CMOC’s Next-Generation ESG Mining Standards position it as a Star: CMOC invested ~USD 420m (2023–2025) in green mining tech and secured 60% renewable power for African sites, meeting OEM low-carbon sourcing thresholds and capturing rising demand for battery metals.

Digital Mining and AI Integration

Implementing autonomous hauling and AI-driven ore processing raised throughput by ~18% and reduced unit costs by 12% at CMOC’s Tenke and Catoca sites in 2024, lifting EBITDA margin contribution from these projects by an estimated $160M annually.

The global smart mining market grew 22% YoY to $16.5B in 2024; demand for automation to cut opex and improve safety supports CMOC’s scaling strategy and lowers lost-time incidents by ~35%.

CMOC’s early, large-scale deployments position it as a frontrunner in mining modernization, improving yield, cutting costs, and creating optionality for premium metal recovery and longer mine life.

- Throughput +18%

- Unit cost -12%

- EBITDA boost ~$160M/yr

- Smart mining market $16.5B (2024), +22% YoY

- Lost-time incidents -35%

Strategic Resource Expansion in DRC

Continued exploration and brownfield development around CMOC Group’s DRC concessions target ~2–4 Mtpa of copper-equivalent production growth and could add an estimated 500–900 kt of high-grade reserves by 2030, keeping CMOC a top-three battery-metal supplier in Africa.

Securing these reserves anchors CMOC’s decade-long market share in battery metals; projects need upfront capital of ~US$800m–1.2bn per major brownfield phase but are forecast to turn cash-positive within 3–5 years of ramp-up.

These initiatives fit the BCG Stars slot: high market growth, high relative share, heavy early capex, and future strong free cash flow once unit costs fall with scale.

- Expected reserve add: 500–900 kt Cu-eq by 2030

- Capex per phase: ~US$800m–1.2bn

- Payback: 3–5 years post-ramp

- Target growth: 2–4 Mtpa Cu-eq production lift

TFM/KFM: 2025 BCG Stars—~700kt Cu-eq, 28% cobalt, automation cuts costs, +500–900kt by 2030

TFM/KFM are BCG Stars: 2025 combined ~700 kt Cu-eq (+60% vs 2022), ~4–5% global refined copper; 2025 capex ~US$1.1–1.3bn; cobalt supply ~28% global refined (2025); automation lifted throughput +18%, unit costs -12%, EBITDA +~US$160M/yr; brownfield adds 500–900 kt Cu-eq by 2030 (capex ~US$800m–1.2bn, payback 3–5 yrs).

| Metric | 2025/Target |

|---|---|

| Cu-eq prod | ~700 kt |

| Capex (2025) | US$1.1–1.3bn |

| Cobalt share | ~28% |

| Throughput | +18% |

| Unit cost | -12% |

| Reserve add | 500–900 kt by 2030 |

What is included in the product

Comprehensive BCG Matrix review of CMOC’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page CMOC Group BCG Matrix placing each business unit in a quadrant for swift portfolio decisions

Cash Cows

Molybdenum and Tungsten Operations

CMOC controls ~25% of China’s molybdenum concentrate output and ~15% of global tungsten concentrate via Sandaozhuang and related assets, producing ~30 kt Mo-equivalent and ~20 kt W-equivalent in 2024; those cash cows yield EBITDA margins near 40%, supporting steady free cash flow.

Niobium Production in Brazil

CMOC Group’s Brazilian niobium assets hold ~80% global market share in niobium (2024 estimate), selling into mature high-strength alloy markets and generating steady EBITDA margins near 40%—producing roughly $320m free cash flow in 2024 from low capex operations.

Phosphate Fertilizer Business

The phosphate fertilizer business in Brazil leverages a mature market with annual fertilizer demand near 20 million tonnes in 2024, giving CMOC predictable regional sales. CMOC holds a top-3 national position and reported phosphate segment EBITDA margins around 28% in FY2024, reflecting high operational efficiency. Output volumes stayed stable at ~1.2 million tonnes P2O5 equivalent in 2024, making it a defensive cash cow versus volatile tech-metal units. This unit delivered roughly $220 million in operating cash flow in 2024, cushioning group earnings.

IXM Global Trading Platform

IXM Global Trading, CMOC Group’s metals trading arm, delivers stable, high-volume revenue by trading ore and refined metals from CMOC’s ~1.2 Mt copper-equivalent annual production and third-party flows; in 2024 IXM reported >$5.0bn in gross merchandise value, underpinning low-margins but steady cash.

As a mature trading unit, IXM offers market access and hedging services with modest incremental capital; its operating leverage helps smooth CMOC’s capex swings—trading liquidity funded ~15–20% of CMOC’s 2024 free cash flow needs.

- High-volume revenue: >$5.0bn GMV (2024)

- Supports ~1.2 Mt copper-equivalent supply

- Low incremental capex, mature margins

- Provides 15–20% of 2024 free cash flow coverage

Established Domestic Chinese Refining

CMOCs established Chinese refining and processing units operate in mature industrial hubs with optimized unit costs; in 2024 these domestic plants delivered an estimated RMB 3.1 billion in operating cash flow, reflecting steady margins and local market leadership.

High regional market share and low capex needs—routine maintenance capex ~RMB 150–200 million annually in 2024—make these cash cows funding CMOCs international expansion and R&D into battery and specialty-mineral applications.

- 2024 operating cash flow ~RMB 3.1bn

- Routine maintenance capex RMB 150–200m/yr

- High regional market share in concentrate-to-refine chain

- Funds earmarked for overseas M&A and mineral-R&D

CMOC 2024: High-EBITDA moly/tungsten & dominant niobium fuel $1B+ FCF engine

CMOC cash cows (2024): moly/tungsten ~30 kt Mo-eq/20 kt W-eq, EBITDA ~40%; Brazilian niobium ~80% share, ~$320m FCF; Brazilian phosphate ~1.2 Mt P2O5, EBITDA ~28%, ~$220m OCF; IXM GMV >$5.0bn, funds 15–20% FCF; China refining OCF ~RMB 3.1bn, maintenance capex RMB150–200m.

| Unit | Key 2024 data | Cash/FCF |

|---|---|---|

| Moly/Tungsten | 30 kt Mo-eq /20 kt W-eq; 40% EBITDA | Steady |

| Niobium (Brazil) | ~80% global; low capex | $320m FCF |

| Phosphate (Brazil) | 1.2 Mt P2O5; 28% EBITDA | $220m OCF |

| IXM Trading | >$5.0bn GMV | 15–20% FCF cover |

| China refineries | OCF RMB 3.1bn; capex 150–200m | Funds growth |

What You’re Viewing Is Included

CMOC Group BCG Matrix

The file you're previewing on this page is the final CMOC Group BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

This preview is the exact same BCG Matrix document sent to your inbox post-purchase, crafted with market-backed insights and ready for immediate editing, printing, or presentation—no surprises, no revisions needed.

What you see is the actual CMOC Group BCG Matrix file included with your one-time purchase; professionally designed by strategy experts and formatted for seamless integration into planning, decks, or client briefings.

You're viewing the real deliverable: a polished, ready-to-use BCG Matrix report that becomes instantly downloadable after payment, enabling immediate application in competitive and portfolio analysis.