CNA Business Model Canvas

Explore CNA's Business Model Canvas — Download the Ready-to-Use Blueprint

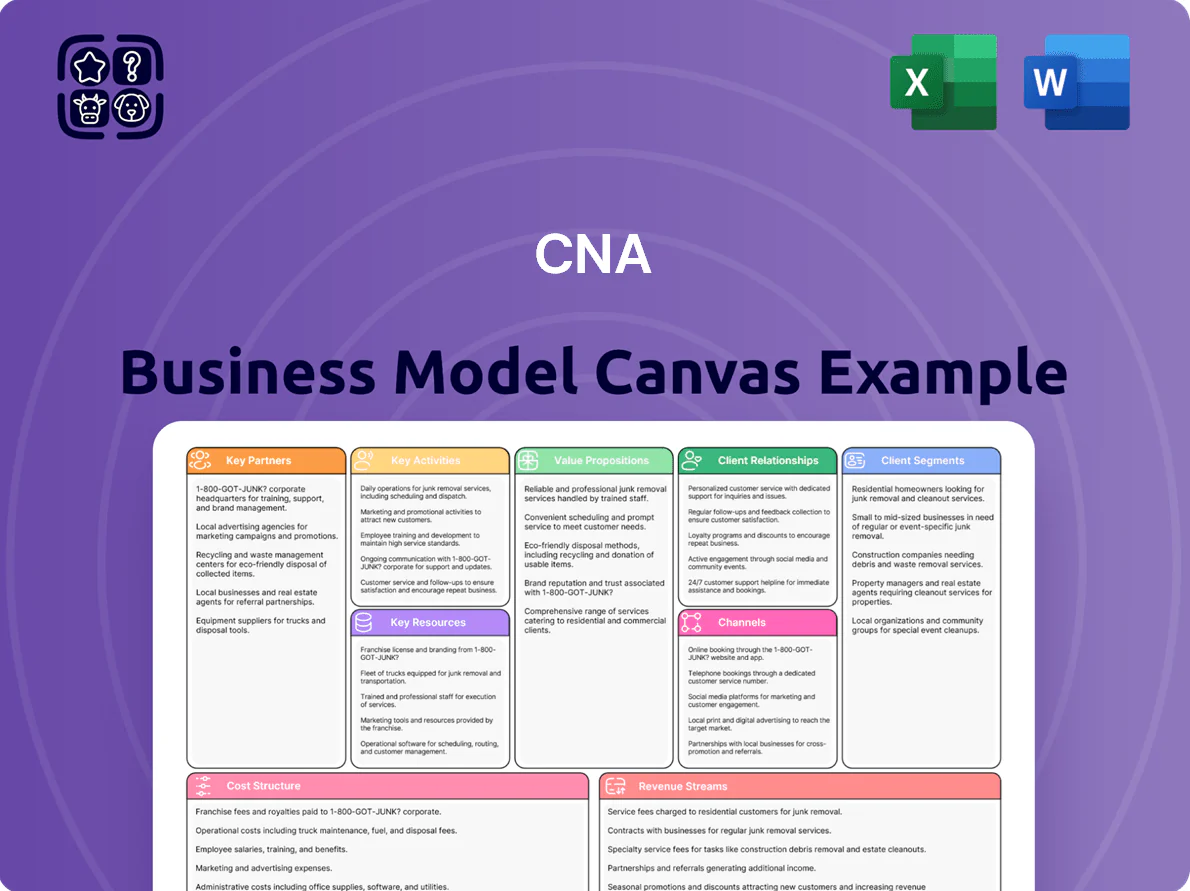

Unlock the full strategic blueprint behind CNA's business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue streams to reveal how CNA creates and captures value; download the complete Word/Excel canvas for a ready-to-use, section-by-section guide ideal for investors, consultants, and entrepreneurs.

Partnerships

Independent Brokerage Network

The independent agent and broker network is CNA’s primary distribution engine, linking the firm to diverse commercial clients and delivering local market expertise to tailor complex insurance packages; brokers accounted for about 65% of CNA’s 2024 commercial new written premium of $9.2 billion, supporting steady pipelines and a 2024 retention rate near 85%.

Reinsurance Providers

Strategic partnerships with global reinsurers let CNA trim capital volatility and limit catastrophic exposure; in 2024 CNA ceded about 18% of net written premium to reinsurers, supporting peak event capacity.

Those reinsurers provide the financial cushion that lets CNA underwrite high-limit corporate policies—helping preserve solvency and sustain its A- (S&P) equivalent rating as of Dec 31, 2024.

Loews Corporation

As parent company, Loews Corporation provides CNA with capital support and strategic oversight, backing $12.1 billion of Loews invested assets at year-end 2024 and enabling access to broader capital markets and reinsurance capacity.

The conglomerate alignment boosts resilience during downturns—Loews’ consolidated surplus rose 8% in 2024, helping CNA absorb underwriting volatility and maintain stable combined ratios versus standalone peers.

Insurtech and Data Vendors

CNA partners with insurtechs and data vendors to boost underwriting accuracy and cut claims costs, using AI and big-data tools that can reduce loss adjustment expense by ~10% and speed claims handling 20% per 2024 industry benchmarks.

These alliances funded ~2–3% of CNA’s 2024 tech spend and keep the firm competitive as commercial-insurance digital adoption rises to ~45% of premiums.

- AI-enabled triage: ~20% faster claims

- Data feeds: +10% underwriting precision

- Tech spend: 2–3% of 2024 budget

Industry Regulatory Bodies

Maintaining active engagement with state and federal insurance regulators ensures CNA meets evolving policyholder-protection and capital standards across all 50 states and Puerto Rico; in 2024 CNA’s statutory surplus was roughly $6.5 billion, helping meet risk-based capital requirements and avoid regulatory actions.

Regular filings and audits—quarterly financial statements, annual NAIC disclosures, and Solvency II-equivalent reviews for international exposure—reduce fines (industry median penalty for major violations was $12.4M in 2023) and protect CNA’s license to operate.

- Active regulator engagement across 51 jurisdictions

- 2024 statutory surplus ≈ $6.5B

- Quarterly filings, annual NAIC reports

- Reduces regulatory fines (industry median $12.4M in 2023)

CNA partnerships boost capacity, cut volatility, and speed underwriting & claims

CNA’s key partnerships—65% broker-distributed commercial premium ($9.2B new written, 2024), ~18% ceded to reinsurers, Loews backing $12.1B invested assets, $6.5B statutory surplus (2024), and 2–3% tech spend with insurtechs—stabilize capacity, lower volatility, raise underwriting accuracy (~+10%) and speed claims (~+20%).

| Partnership | 2024 Metric |

|---|---|

| Broker channel | 65% of new premium; $9.2B |

| Reinsurance | 18% ceded |

| Parent capital | Loews $12.1B invested assets |

| Statutory surplus | $6.5B |

| Tech partnerships | 2–3% tech spend; +10% UW accuracy; +20% claims speed |

What is included in the product

A concise, pre-written Business Model Canvas for CNA that maps nine BMC blocks with detailed value propositions, customer segments, channels, revenue streams and key activities, linking each block to competitive advantages, SWOT insights and real-world operational plans to support presentations, funding discussions and strategic validation.

Condenses CNA's strategy into a digestible one-page canvas to quickly identify core components, save hours of setup, and support collaborative iteration for boardrooms or team workshops.

Activities

Underwriting and Pricing

The core activity rigorously evaluates commercial risks to set coverage terms and premiums; CNA’s 2024 combined ratio was 89.8%, showing disciplined underwriting drove technical profitability. Actuaries and underwriters use stochastic and catastrophe models—CNA reported $2.3B net written premium in Q4 2024—to align pricing with claim probability and severity, keeping CNA competitive in specialty commercial lines.

Claims Management

CNA processes and settles claims quickly to deliver financial protection, combining empathetic customer service with forensic investigations to curb fraud; in 2024 CNA reported a combined ratio near 104%, so claims efficiency directly affects underwriting losses and profitability.

Risk Control Services

The company delivers proactive safety and loss-prevention consulting—site inspections, safety training, and industry-specific risk assessments—that cut client accident rates; CNA reported a 12% reduction in commercial client loss frequency in 2024 after expanded risk control programs, lowering claims costs and improving retention by 6 percentage points year-over-year.

Product Development

Product development at CNA focuses on continuous innovation to counter rising cyber risk, climate-driven losses, and shifting professional liabilities; CNA launched 12 cyber endorsements and updated pollution coverages in 2024 after a 38% rise in cyber claims severity since 2019.

The company uses market research and loss-data analytics to design new forms and endorsements so the commercial product portfolio stays relevant amid a 6% annual growth in specialty commercial premiums (2023–24).

- 12 new cyber endorsements (2024)

- 38% rise in cyber claim severity since 2019

- 6% annual specialty premium growth (2023–24)

Investment Portfolio Management

Managing CNA’s premium float—about $18.3 billion invested at year-end 2024—means deploying cash into bonds, equities, and alternatives to earn investment income that offsets underwriting shortfalls and boosts net income.

In 2024 investment income contributed roughly $1.2 billion, helping narrow combined ratio pressures from underwriting; effective duration and credit positioning were key.

- Premiums invested: ~$18.3B (YE 2024)

- Investment income: ~$1.2B (2024)

- Asset mix: fixed-income, equities, alternatives

- Role: offset underwriting losses, raise net income

CNA: Disciplined underwriting (89.8% CR), lower losses, $1.2B investment income

CNA evaluates commercial risk and prices to a disciplined 89.8% combined ratio (2024), settles claims with forensic teams (claims pushed combined ratio near 104% in parts of 2024), runs risk-control programs that cut client loss frequency 12% and raised retention +6ppt, launched 12 cyber endorsements (2024) after a 38% rise in cyber severity since 2019, and invests ~$18.3B float to generate ~$1.2B investment income (2024).

| Metric | 2024 |

|---|---|

| Combined ratio | 89.8% |

| Claims-pressured ratio | ~104% |

| Loss frequency change | -12% |

| Retention change | +6 ppt |

| Cyber endorsements | 12 |

| Cyber severity change since 2019 | +38% |

| Premiums invested (float) | $18.3B |

| Investment income | $1.2B |

What You See Is What You Get

Business Model Canvas

The preview you see is the authentic CNA Business Model Canvas file—not a mockup or sample—and it matches the exact document you will receive after purchase.

When you complete your order, you’ll get the full, ready-to-edit Business Model Canvas in the same format and layout shown here, with all sections and content included.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Explore CNA's Business Model Canvas — Download the Ready-to-Use Blueprint

Unlock the full strategic blueprint behind CNA's business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue streams to reveal how CNA creates and captures value; download the complete Word/Excel canvas for a ready-to-use, section-by-section guide ideal for investors, consultants, and entrepreneurs.

Partnerships

Independent Brokerage Network

The independent agent and broker network is CNA’s primary distribution engine, linking the firm to diverse commercial clients and delivering local market expertise to tailor complex insurance packages; brokers accounted for about 65% of CNA’s 2024 commercial new written premium of $9.2 billion, supporting steady pipelines and a 2024 retention rate near 85%.

Reinsurance Providers

Strategic partnerships with global reinsurers let CNA trim capital volatility and limit catastrophic exposure; in 2024 CNA ceded about 18% of net written premium to reinsurers, supporting peak event capacity.

Those reinsurers provide the financial cushion that lets CNA underwrite high-limit corporate policies—helping preserve solvency and sustain its A- (S&P) equivalent rating as of Dec 31, 2024.

Loews Corporation

As parent company, Loews Corporation provides CNA with capital support and strategic oversight, backing $12.1 billion of Loews invested assets at year-end 2024 and enabling access to broader capital markets and reinsurance capacity.

The conglomerate alignment boosts resilience during downturns—Loews’ consolidated surplus rose 8% in 2024, helping CNA absorb underwriting volatility and maintain stable combined ratios versus standalone peers.

Insurtech and Data Vendors

CNA partners with insurtechs and data vendors to boost underwriting accuracy and cut claims costs, using AI and big-data tools that can reduce loss adjustment expense by ~10% and speed claims handling 20% per 2024 industry benchmarks.

These alliances funded ~2–3% of CNA’s 2024 tech spend and keep the firm competitive as commercial-insurance digital adoption rises to ~45% of premiums.

- AI-enabled triage: ~20% faster claims

- Data feeds: +10% underwriting precision

- Tech spend: 2–3% of 2024 budget

Industry Regulatory Bodies

Maintaining active engagement with state and federal insurance regulators ensures CNA meets evolving policyholder-protection and capital standards across all 50 states and Puerto Rico; in 2024 CNA’s statutory surplus was roughly $6.5 billion, helping meet risk-based capital requirements and avoid regulatory actions.

Regular filings and audits—quarterly financial statements, annual NAIC disclosures, and Solvency II-equivalent reviews for international exposure—reduce fines (industry median penalty for major violations was $12.4M in 2023) and protect CNA’s license to operate.

- Active regulator engagement across 51 jurisdictions

- 2024 statutory surplus ≈ $6.5B

- Quarterly filings, annual NAIC reports

- Reduces regulatory fines (industry median $12.4M in 2023)

CNA partnerships boost capacity, cut volatility, and speed underwriting & claims

CNA’s key partnerships—65% broker-distributed commercial premium ($9.2B new written, 2024), ~18% ceded to reinsurers, Loews backing $12.1B invested assets, $6.5B statutory surplus (2024), and 2–3% tech spend with insurtechs—stabilize capacity, lower volatility, raise underwriting accuracy (~+10%) and speed claims (~+20%).

| Partnership | 2024 Metric |

|---|---|

| Broker channel | 65% of new premium; $9.2B |

| Reinsurance | 18% ceded |

| Parent capital | Loews $12.1B invested assets |

| Statutory surplus | $6.5B |

| Tech partnerships | 2–3% tech spend; +10% UW accuracy; +20% claims speed |

What is included in the product

A concise, pre-written Business Model Canvas for CNA that maps nine BMC blocks with detailed value propositions, customer segments, channels, revenue streams and key activities, linking each block to competitive advantages, SWOT insights and real-world operational plans to support presentations, funding discussions and strategic validation.

Condenses CNA's strategy into a digestible one-page canvas to quickly identify core components, save hours of setup, and support collaborative iteration for boardrooms or team workshops.

Activities

Underwriting and Pricing

The core activity rigorously evaluates commercial risks to set coverage terms and premiums; CNA’s 2024 combined ratio was 89.8%, showing disciplined underwriting drove technical profitability. Actuaries and underwriters use stochastic and catastrophe models—CNA reported $2.3B net written premium in Q4 2024—to align pricing with claim probability and severity, keeping CNA competitive in specialty commercial lines.

Claims Management

CNA processes and settles claims quickly to deliver financial protection, combining empathetic customer service with forensic investigations to curb fraud; in 2024 CNA reported a combined ratio near 104%, so claims efficiency directly affects underwriting losses and profitability.

Risk Control Services

The company delivers proactive safety and loss-prevention consulting—site inspections, safety training, and industry-specific risk assessments—that cut client accident rates; CNA reported a 12% reduction in commercial client loss frequency in 2024 after expanded risk control programs, lowering claims costs and improving retention by 6 percentage points year-over-year.

Product Development

Product development at CNA focuses on continuous innovation to counter rising cyber risk, climate-driven losses, and shifting professional liabilities; CNA launched 12 cyber endorsements and updated pollution coverages in 2024 after a 38% rise in cyber claims severity since 2019.

The company uses market research and loss-data analytics to design new forms and endorsements so the commercial product portfolio stays relevant amid a 6% annual growth in specialty commercial premiums (2023–24).

- 12 new cyber endorsements (2024)

- 38% rise in cyber claim severity since 2019

- 6% annual specialty premium growth (2023–24)

Investment Portfolio Management

Managing CNA’s premium float—about $18.3 billion invested at year-end 2024—means deploying cash into bonds, equities, and alternatives to earn investment income that offsets underwriting shortfalls and boosts net income.

In 2024 investment income contributed roughly $1.2 billion, helping narrow combined ratio pressures from underwriting; effective duration and credit positioning were key.

- Premiums invested: ~$18.3B (YE 2024)

- Investment income: ~$1.2B (2024)

- Asset mix: fixed-income, equities, alternatives

- Role: offset underwriting losses, raise net income

CNA: Disciplined underwriting (89.8% CR), lower losses, $1.2B investment income

CNA evaluates commercial risk and prices to a disciplined 89.8% combined ratio (2024), settles claims with forensic teams (claims pushed combined ratio near 104% in parts of 2024), runs risk-control programs that cut client loss frequency 12% and raised retention +6ppt, launched 12 cyber endorsements (2024) after a 38% rise in cyber severity since 2019, and invests ~$18.3B float to generate ~$1.2B investment income (2024).

| Metric | 2024 |

|---|---|

| Combined ratio | 89.8% |

| Claims-pressured ratio | ~104% |

| Loss frequency change | -12% |

| Retention change | +6 ppt |

| Cyber endorsements | 12 |

| Cyber severity change since 2019 | +38% |

| Premiums invested (float) | $18.3B |

| Investment income | $1.2B |

What You See Is What You Get

Business Model Canvas

The preview you see is the authentic CNA Business Model Canvas file—not a mockup or sample—and it matches the exact document you will receive after purchase.

When you complete your order, you’ll get the full, ready-to-edit Business Model Canvas in the same format and layout shown here, with all sections and content included.