CNO Financial Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

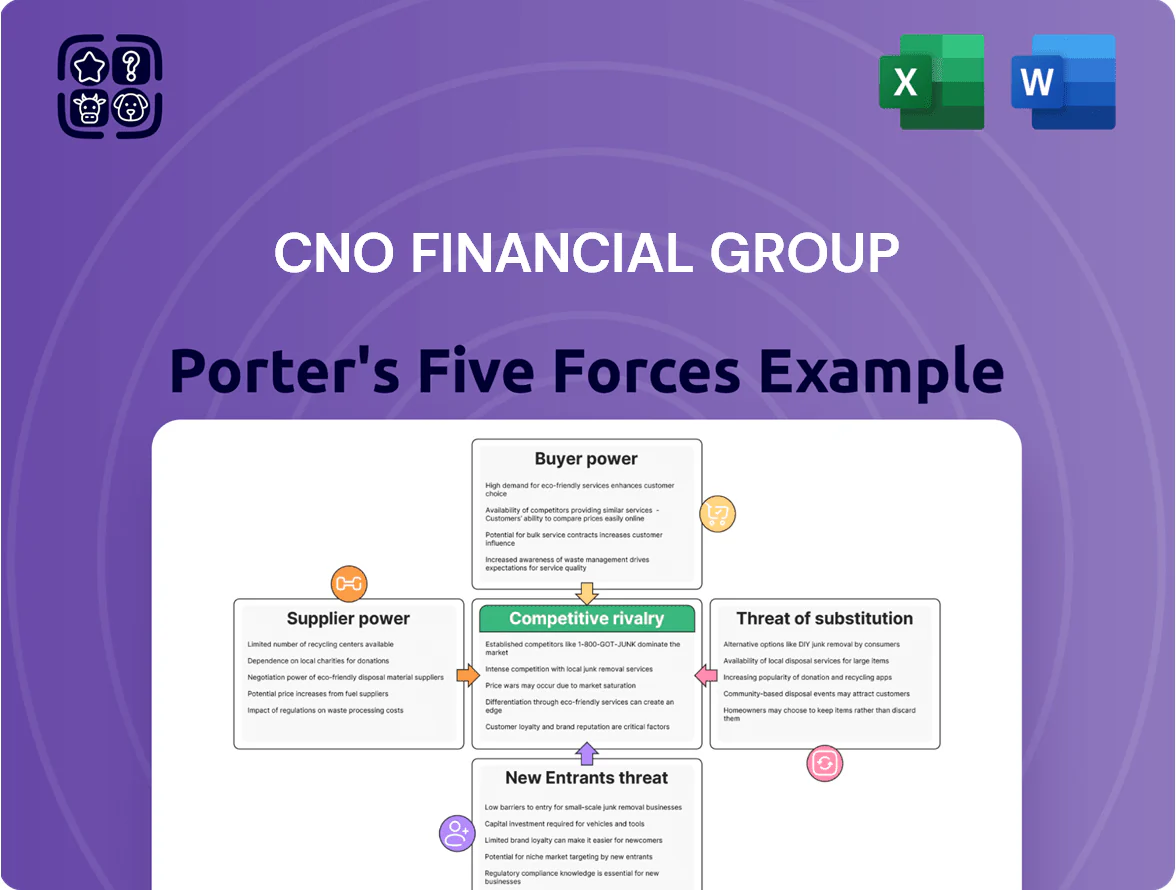

CNO Financial Group faces moderate buyer power and regulatory pressure, with limited supplier influence but notable threats from digital insurers and substitutes in the life and health segments.

Competitive rivalry is intensified by niche players and price-sensitive distribution channels, while barriers to entry remain moderate due to capital and regulatory requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CNO Financial Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Capacity and Pricing

Reinsurers act as critical suppliers by absorbing risk and providing capital relief to CNO Financial Group, and tightening global capacity by end-2025 pushed market premiums up roughly 10–15% year-over-year per Aon data, while treaty attachment points rose too.

This pricing squeeze forces CNO to pay higher ceded premiums and accept stricter terms, compressing underwriting margins and raising capital costs; CNO reported reinsurance expense increases in 2024–25 that reduced operating margins by an estimated 50–100 basis points.

Access to Financial Capital and Interest Rates

The providers of debt and equity capital exert moderate bargaining power over CNO Financial Group, constraining strategic moves and M&A scope; as of Q4 2025, CNO carried about $2.3 billion of long-term debt and a net leverage ratio near 1.8x, so borrowing costs at stabilized higher rates (around 4.5–5.5% in late 2025) keep interest expense material. Lenders and bondholders can impose covenants that influence liquidity, capital allocation, and CNOs investment-grade standing.

Technological and Data Service Providers

CNO depends on third-party cloud, cybersecurity, and analytics vendors for digital distribution; in 2024 roughly 60–70% of enterprise insurance workloads ran on the Big Three cloud providers, concentrating supplier power.

That concentration raises bargaining leverage: large tech firms can push higher prices and stricter SLAs, and enterprise cloud IaaS/PaaS price increases of 5–10% in 2023–24 raised vendor cost risk for insurers.

Switching costs are high because integrating legacy policy admin systems with modern APIs takes 9–18 months and $2–10m per major system, locking CNO into existing vendors and limiting negotiation room.

Specialized Actuarial and Digital Talent

- Actuary demand up 22% (BLS to 2029)

- AI/insurtech pay premium 20–40%

- Recruiter fees 20–30% of first-year salary

- Time-to-fill extends hiring cost and project delays

Regulatory and Rating Agency Compliance

State insurance regulators and credit rating agencies provide the operational legitimacy CNO Financial Group needs; their power is absolute because CNO cannot issue policies without meeting capital reserve rules and maintaining ratings.

Regulatory changes through late 2025 pushed insurers to raise compliance spending; US insurers increased compliance budgets ~18% YoY in 2024–25, and CNO’s statutory RBC (risk-based capital) ratio must stay above regulatory action levels to avoid intervention.

Unfavorable rating actions raise funding costs; a one-notch downgrade typically lifts insurance borrowing spreads by ~75–125 bps, squeezing CNO’s M&A and growth options.

- Regulators = gatekeepers; noncompliance halts sales

- Compliance costs +18% YoY industry-wide (2024–25)

- RBC ratio must exceed action thresholds to avoid state receivership

- One-notch downgrade → ~75–125 bps higher borrowing cost

Supplier squeeze: rising reinsurance, debt, cloud concentration, talent & compliance costs

Reinsurers, debt/equity providers, Big Three cloud vendors, talent recruiters, and state regulators exert meaningful supplier power over CNO, raising costs and limiting strategic flexibility; reinsurance pricing rose ~10–15% by end-2025, CNO long-term debt ≈ $2.3B (net leverage ~1.8x), cloud workload concentration 60–70%, actuary demand +22% to 2029, and compliance budgets +18% YoY (2024–25).

| Supplier | Key metric |

|---|---|

| Reinsurers | Premiums +10–15% (end‑2025) |

| Capital | $2.3B debt; leverage ~1.8x |

| Cloud vendors | 60–70% workloads |

| Talent | Actuary demand +22% (to 2029) |

| Regulators | Compliance +18% YoY (2024–25) |

What is included in the product

Tailored exclusively for CNO Financial Group, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for CNO Financial Group—quickly identify competitive threats and profitability levers to inform underwriting, pricing, and M&A decisions.

Customers Bargaining Power

Price Sensitivity of Middle-Income Consumers

CNO targets middle-income Americans who, per 2025 BLS data, saw median household real wages flat while CPI-U rose ~3.4% in 2024–25, making premium hikes highly sensitive; industry lapse rates for supplemental policies rose to ~7–9% in 2024 when carriers pushed 5–7% increases, so CNO’s pricing power is constrained—raising premiums risks meaningful lapses and lost sales amid tight household budgets and rising inflation.

Digital Transparency and Comparison Tools

By 2025, online insurance marketplaces and comparison engines let buyers compare premiums, riders, and benefits across dozens of carriers in minutes, cutting purchase time by ~40% versus 2018 (McKinsey 2024 digital insurance report) and lowering search costs.

This transparency shrinks information asymmetry that once favored insurers, raising buyer leverage and pressuring CNO Financial Group’s pricing and margin flexibility; 55% of US adults used comparison sites for insurance quotes in 2024 (J.D. Power).

Low Switching Costs for New Policies

Many CNO Financial Group customers face low switching costs for supplemental health and annuity products, letting 28% of policyholders shop annually for better rates or digital experiences; competitors lure buyers with 5–15% introductory discounts and faster online onboarding. This mobility pressures CNO to spend on retention—CNO reported $210 million in acquisition and retention costs in 2024—and to expand loyalty and digital investments to reduce churn.

Influence of Independent Insurance Agents

A significant share of CNO Financial Groups premiums—about 60% in 2024—flows through independent agents who represent buyer interests and can steer clients to rivals if CNOs commissions or product terms lag market rates.

Because agents act as customer proxies, they pressure CNO to keep commissions and features competitive; CNO trimmed lapse rates to 8.2% in 2024 after product and commission adjustments, showing this leverage.

- ~60% premiums via independents (2024)

- 8.2% lapse rate after adjustments (2024)

- Agents can shift sales quickly if offerings slip

Demand for Personalized and Flexible Coverage

Modern consumers expect insurance tailored to lifestyle and health; by end-2025 demand for modular policies rose ~22% year-over-year, shifting purchasing power to buyers and pressuring price sensitivity.

CNO Financial Group must shorten product development cycles—its 2024 new-product lead time ~14 months—or risk share loss as 48% of buyers prefer customizable riders.

- Demand up ~22% by 2025

- CNO 2024 product lead time ~14 months

- 48% of buyers prefer customizable riders

Buyers Dictate Terms: Comparison Shopping, High Lapses Drive $210M Retention Push

Buyers have strong leverage: flat real wages (2025 BLS), CPI-U +3.4% (2024–25), high lapse sensitivity (7–9% industry; CNO 8.2% after changes), 55% used comparison sites (2024), 60% premiums via independents, and 28% shop annually—forcing CNO to protect margins with retention spend ($210M in 2024) and faster product cycles (14 months in 2024).

| Metric | Value |

|---|---|

| Comparison-site use (2024) | 55% |

| Premiums via independents (2024) | 60% |

| CNO lapse rate (2024) | 8.2% |

| Retention/acq spend (2024) | $210M |

| Product lead time (2024) | 14 months |

Full Version Awaits

CNO Financial Group Porter's Five Forces Analysis

This preview shows the exact CNO Financial Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You’re previewing the final deliverable: the same in-depth competitive assessment ready for immediate use upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CNO Financial Group faces moderate buyer power and regulatory pressure, with limited supplier influence but notable threats from digital insurers and substitutes in the life and health segments.

Competitive rivalry is intensified by niche players and price-sensitive distribution channels, while barriers to entry remain moderate due to capital and regulatory requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CNO Financial Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Capacity and Pricing

Reinsurers act as critical suppliers by absorbing risk and providing capital relief to CNO Financial Group, and tightening global capacity by end-2025 pushed market premiums up roughly 10–15% year-over-year per Aon data, while treaty attachment points rose too.

This pricing squeeze forces CNO to pay higher ceded premiums and accept stricter terms, compressing underwriting margins and raising capital costs; CNO reported reinsurance expense increases in 2024–25 that reduced operating margins by an estimated 50–100 basis points.

Access to Financial Capital and Interest Rates

The providers of debt and equity capital exert moderate bargaining power over CNO Financial Group, constraining strategic moves and M&A scope; as of Q4 2025, CNO carried about $2.3 billion of long-term debt and a net leverage ratio near 1.8x, so borrowing costs at stabilized higher rates (around 4.5–5.5% in late 2025) keep interest expense material. Lenders and bondholders can impose covenants that influence liquidity, capital allocation, and CNOs investment-grade standing.

Technological and Data Service Providers

CNO depends on third-party cloud, cybersecurity, and analytics vendors for digital distribution; in 2024 roughly 60–70% of enterprise insurance workloads ran on the Big Three cloud providers, concentrating supplier power.

That concentration raises bargaining leverage: large tech firms can push higher prices and stricter SLAs, and enterprise cloud IaaS/PaaS price increases of 5–10% in 2023–24 raised vendor cost risk for insurers.

Switching costs are high because integrating legacy policy admin systems with modern APIs takes 9–18 months and $2–10m per major system, locking CNO into existing vendors and limiting negotiation room.

Specialized Actuarial and Digital Talent

- Actuary demand up 22% (BLS to 2029)

- AI/insurtech pay premium 20–40%

- Recruiter fees 20–30% of first-year salary

- Time-to-fill extends hiring cost and project delays

Regulatory and Rating Agency Compliance

State insurance regulators and credit rating agencies provide the operational legitimacy CNO Financial Group needs; their power is absolute because CNO cannot issue policies without meeting capital reserve rules and maintaining ratings.

Regulatory changes through late 2025 pushed insurers to raise compliance spending; US insurers increased compliance budgets ~18% YoY in 2024–25, and CNO’s statutory RBC (risk-based capital) ratio must stay above regulatory action levels to avoid intervention.

Unfavorable rating actions raise funding costs; a one-notch downgrade typically lifts insurance borrowing spreads by ~75–125 bps, squeezing CNO’s M&A and growth options.

- Regulators = gatekeepers; noncompliance halts sales

- Compliance costs +18% YoY industry-wide (2024–25)

- RBC ratio must exceed action thresholds to avoid state receivership

- One-notch downgrade → ~75–125 bps higher borrowing cost

Supplier squeeze: rising reinsurance, debt, cloud concentration, talent & compliance costs

Reinsurers, debt/equity providers, Big Three cloud vendors, talent recruiters, and state regulators exert meaningful supplier power over CNO, raising costs and limiting strategic flexibility; reinsurance pricing rose ~10–15% by end-2025, CNO long-term debt ≈ $2.3B (net leverage ~1.8x), cloud workload concentration 60–70%, actuary demand +22% to 2029, and compliance budgets +18% YoY (2024–25).

| Supplier | Key metric |

|---|---|

| Reinsurers | Premiums +10–15% (end‑2025) |

| Capital | $2.3B debt; leverage ~1.8x |

| Cloud vendors | 60–70% workloads |

| Talent | Actuary demand +22% (to 2029) |

| Regulators | Compliance +18% YoY (2024–25) |

What is included in the product

Tailored exclusively for CNO Financial Group, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for CNO Financial Group—quickly identify competitive threats and profitability levers to inform underwriting, pricing, and M&A decisions.

Customers Bargaining Power

Price Sensitivity of Middle-Income Consumers

CNO targets middle-income Americans who, per 2025 BLS data, saw median household real wages flat while CPI-U rose ~3.4% in 2024–25, making premium hikes highly sensitive; industry lapse rates for supplemental policies rose to ~7–9% in 2024 when carriers pushed 5–7% increases, so CNO’s pricing power is constrained—raising premiums risks meaningful lapses and lost sales amid tight household budgets and rising inflation.

Digital Transparency and Comparison Tools

By 2025, online insurance marketplaces and comparison engines let buyers compare premiums, riders, and benefits across dozens of carriers in minutes, cutting purchase time by ~40% versus 2018 (McKinsey 2024 digital insurance report) and lowering search costs.

This transparency shrinks information asymmetry that once favored insurers, raising buyer leverage and pressuring CNO Financial Group’s pricing and margin flexibility; 55% of US adults used comparison sites for insurance quotes in 2024 (J.D. Power).

Low Switching Costs for New Policies

Many CNO Financial Group customers face low switching costs for supplemental health and annuity products, letting 28% of policyholders shop annually for better rates or digital experiences; competitors lure buyers with 5–15% introductory discounts and faster online onboarding. This mobility pressures CNO to spend on retention—CNO reported $210 million in acquisition and retention costs in 2024—and to expand loyalty and digital investments to reduce churn.

Influence of Independent Insurance Agents

A significant share of CNO Financial Groups premiums—about 60% in 2024—flows through independent agents who represent buyer interests and can steer clients to rivals if CNOs commissions or product terms lag market rates.

Because agents act as customer proxies, they pressure CNO to keep commissions and features competitive; CNO trimmed lapse rates to 8.2% in 2024 after product and commission adjustments, showing this leverage.

- ~60% premiums via independents (2024)

- 8.2% lapse rate after adjustments (2024)

- Agents can shift sales quickly if offerings slip

Demand for Personalized and Flexible Coverage

Modern consumers expect insurance tailored to lifestyle and health; by end-2025 demand for modular policies rose ~22% year-over-year, shifting purchasing power to buyers and pressuring price sensitivity.

CNO Financial Group must shorten product development cycles—its 2024 new-product lead time ~14 months—or risk share loss as 48% of buyers prefer customizable riders.

- Demand up ~22% by 2025

- CNO 2024 product lead time ~14 months

- 48% of buyers prefer customizable riders

Buyers Dictate Terms: Comparison Shopping, High Lapses Drive $210M Retention Push

Buyers have strong leverage: flat real wages (2025 BLS), CPI-U +3.4% (2024–25), high lapse sensitivity (7–9% industry; CNO 8.2% after changes), 55% used comparison sites (2024), 60% premiums via independents, and 28% shop annually—forcing CNO to protect margins with retention spend ($210M in 2024) and faster product cycles (14 months in 2024).

| Metric | Value |

|---|---|

| Comparison-site use (2024) | 55% |

| Premiums via independents (2024) | 60% |

| CNO lapse rate (2024) | 8.2% |

| Retention/acq spend (2024) | $210M |

| Product lead time (2024) | 14 months |

Full Version Awaits

CNO Financial Group Porter's Five Forces Analysis

This preview shows the exact CNO Financial Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You’re previewing the final deliverable: the same in-depth competitive assessment ready for immediate use upon payment.