CNPC Capital PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political dynamics, market cycles, and technological shifts are shaping CNPC Capital’s strategic outlook in our concise PESTLE snapshot—designed to give investors and strategists a quick, actionable read; purchase the full PESTLE for complete risk scoring, scenario analysis, and ready-to-use slides to inform decisions instantly.

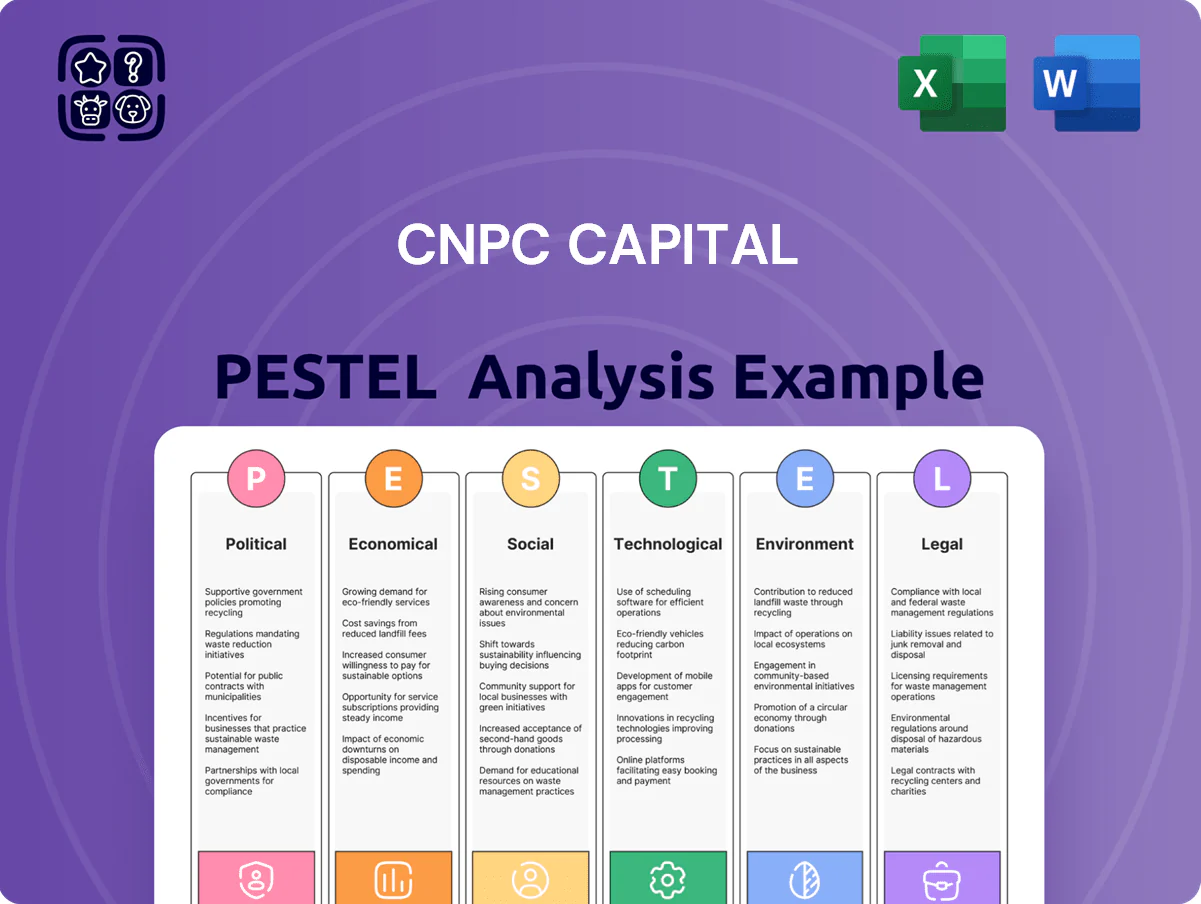

Political factors

State Owned Enterprise Strategic Alignment

CNPC Capital functions as the primary financial arm of China National Petroleum, aligning investment flows with Beijing’s energy security and industrial modernization goals; by end-2025 it channels an estimated CNY 200–300 billion in directed capital annually toward strategic projects.

Belt and Road Initiative Financial Support

CNPC Capital provides specialized financing, cross-border settlements and risk management for Belt and Road energy projects, underwriting an estimated $18–25 billion in outbound project finance between 2020–2024 and supporting pipelines, LNG and power assets across 30+ countries.

As cooperation frameworks evolved through 2025, CNPC Capital scaled syndicated loans and ECA-backed facilities, contributing to China’s $1.3 trillion BRI financing stockpile while facilitating RMB settlement growth to 12–15% of project trade flows.

This political mandate expands CNPC Capital’s global footprint but raises exposure to emerging-market sovereign debt risks, with non-performing loan pressures rising in some BRI markets where sovereign debt-to-GDP ratios exceeded 70% by 2024.

Energy Security and Supply Chain Policy

As China pushes for greater energy self-sufficiency, CNPC Capital has increased financing for domestic upstream projects, allocating an estimated CNY 45–60 billion in 2024–25 toward exploration and production improvements to meet National Energy Administration targets.

Political priority on oil and gas supply-chain security shifts lending and leasing to upstream tech upgrades, with 38% of new credit lines in 2024 earmarked for seismic, drilling and enhanced recovery equipment.

CNPC Capital’s strategy is guided by NEA long-term plans and 2030 resource security quotas, binding it to performance metrics and capital deployment that support China’s goal of reducing import dependence from roughly 73% of oil consumption in 2023.

Regulatory Oversight and Centralized Control

By 2025 the National Financial Regulatory Administration has centralized oversight of financial holding firms, imposing stricter capital adequacy and risk-isolation rules; banks and holdings face minimum CET1-like metrics and stress-test thresholds—China’s large financial groups now commonly target >10% core capital buffers per regulator guidance.

CNPC Capital must comply with tight controls on related-party transactions with CNPC parent and affiliates, curbing intra-group capital transfers and requiring ring-fencing for non-core activities, reducing deployment flexibility despite ensuring systemic stability.

- Centralized regulator: NFRA oversight by 2025

- Capital standards: target >10% core buffers

- Risk isolation: mandated ring-fencing of non-bank assets

- Related-party limits: stricter approval and disclosure rules

Geopolitical Tensions and Sanctions Risk

The evolving China-West tensions raise sanctions risk for CNPC Capital’s overseas finance; in 2024 China faced 45 major trade disputes with OECD partners and 18 targeted financial restrictions affecting Chinese banks.

CNPC Capital must build alternative payment rails and diversify currency exposure—RMB cross-border payments rose 28% in 2024, yet USD still dominates 88% of global FX reserves.

Strategic planning must model liquidity shocks from trade disputes that could reduce subsidiary funding access by an estimated 10–20% under severe sanction scenarios.

- 45 major 2024 China-OECD trade disputes; 18 targeted financial measures

- RMB cross-border payments +28% in 2024; USD ~88% of reserves

- Plan for 10–20% subsidiary liquidity shortfalls under severe sanctions

CNPC Capital directs CNY200–300bn to strategic energy; NFRA buffers >10%, RMB cross‑border +28%

CNPC Capital’s political mandate channels CNY 200–300bn pa (2025) into strategic energy projects, backed by NFRA oversight with >10% core buffers and ring-fencing rules; outbound project finance reached $18–25bn (2020–24) amid 45 China‑OECD trade disputes in 2024 and 18 targeted measures, prompting 28% growth in RMB cross‑border payments and planning for 10–20% subsidiary liquidity shocks.

| Metric | Value |

|---|---|

| Directed capital (2025) | CNY 200–300bn |

| Outbound finance (2020–24) | $18–25bn |

| NFRA core buffer target | >10% |

| China‑OECD disputes (2024) | 45 |

| RMB XB payments growth (2024) | +28% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact CNPC Capital, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented CNPC Capital PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory shifts, and market positioning while allowing for brief, context-specific notes.

Economic factors

Interest Rate Environment and Margin Compression

By end-2025, the PBOC balances modest easing and targeted support with debt deleveraging, keeping one-year loan prime rate near 3.95% and five-year LPR around 4.45%, creating a nuanced rate backdrop.

CNPC Capital faces net interest margin compression as competition for top-tier industrial borrowers tightens; sector NIMs narrowed ~20–35 bps in 2024 across Chinese mid-tier banks.

The firm must optimize liabilities—shorten funding tenor, diversify wholesale and RMB bond channels—to protect returns amid volatile benchmark rates and market-oriented pricing.

Energy Market Volatility and Credit Risk

CNPC Capital's performance is tightly tied to energy sector health; a 2024 Brent range of 70–100 USD/bbl and China LNG spot volatility ±30% year-on-year directly affect parent and subsidiary cash flows.

Crude price collapses in 2020 showed impairment risk; a 50% price drop can raise nonperforming loan ratios sharply, increasing credit stress on lending and leasing portfolios.

As of 2025 Q1, CNPC group debt-service coverage sensitivity to a 20% revenue shock requires higher provisioning and tighter covenants.

RMB Internationalization and Cross-border Trade

As RMB use in global energy trade rose—Chinese trade settlement in RMB reached 34% of global FX trade in 2024—CNPC Capital gains higher demand for RMB-denominated settlement and clearing, boosting fee income and liquidity management.

Leveraging its energy value‑chain role, CNPC Capital reduces partners’ conversion costs via RMB settlement corridors, supporting cross-border contracts and trade finance volumes.

Growth of Kunlun Bank—which saw international RMB deposits grow ~22% in 2024—strengthens CNPC Capital’s niche market and alternative payment route capabilities.

Industrial Sector Growth and Capital Demand

The shift to high-end manufacturing and green energy in China expands capital deployment opportunities; green investment reached 1.4 trillion RMB in 2024, supporting CNPC Capital's focus on hydrogen infrastructure and carbon capture projects.

CNPC Capital targets emerging industrial clusters—hydrogen, CCUS, battery manufacturing—where demand for specialized financial leasing and asset management is rising, offsetting slower heavy-industry financing.

- 2024 green investment: 1.4 trillion RMB

- Hydrogen project financing growth: ~28% YoY (2024)

- CCUS capacity target: 10 MtCO2/year by 2030

Inflationary Pressures and Operational Costs

Persistent global inflation, with IMF forecasting 2025 global inflation around 5.8% in emerging markets, is raising CNPC Capital's labor and procurement costs, including a 6–8% annual rise in fintech subscription and cloud expenses observed in 2024–25.

CNPC Capital must balance higher operational expenditures with competitive service pricing for internal and external clients to protect margins and client retention amid fee sensitivity.

Automation of back-office functions and strict cost controls are essential to preserve efficiency ratios; industry peers reported up to 15% reduction in back-office costs after RPA and cloud migration in 2024.

- Global EM inflation ~5.8% (IMF 2025)

- Fintech/cloud costs +6–8% YoY (2024–25)

- Back-office cost cut up to 15% via automation (2024)

Global headwinds: easing rates, squeezed margins, oil volatility, green spend boosts

Economic headwinds: modest PBOC easing with 1y LPR ~3.95%/5y ~4.45%; NIMs compressed 20–35bps (2024); Brent 70–100 USD/bbl (2024) with ±30% LNG volatility; green investment 1.4 tn RMB (2024); EM inflation ~5.8% (2025); fintech/cloud costs +6–8% YoY (2024–25); back‑office cuts up to 15% via automation (2024).

| Metric | Value |

|---|---|

| 1y/5y LPR | 3.95% / 4.45% |

| NIM compression | 20–35bps (2024) |

| Brent 2024 | 70–100 USD/bbl |

| Green invest 2024 | 1.4 tn RMB |

| EM inflation 2025 | ~5.8% |

Full Version Awaits

CNPC Capital PESTLE Analysis

The preview shown here is the exact CNPC Capital PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political dynamics, market cycles, and technological shifts are shaping CNPC Capital’s strategic outlook in our concise PESTLE snapshot—designed to give investors and strategists a quick, actionable read; purchase the full PESTLE for complete risk scoring, scenario analysis, and ready-to-use slides to inform decisions instantly.

Political factors

State Owned Enterprise Strategic Alignment

CNPC Capital functions as the primary financial arm of China National Petroleum, aligning investment flows with Beijing’s energy security and industrial modernization goals; by end-2025 it channels an estimated CNY 200–300 billion in directed capital annually toward strategic projects.

Belt and Road Initiative Financial Support

CNPC Capital provides specialized financing, cross-border settlements and risk management for Belt and Road energy projects, underwriting an estimated $18–25 billion in outbound project finance between 2020–2024 and supporting pipelines, LNG and power assets across 30+ countries.

As cooperation frameworks evolved through 2025, CNPC Capital scaled syndicated loans and ECA-backed facilities, contributing to China’s $1.3 trillion BRI financing stockpile while facilitating RMB settlement growth to 12–15% of project trade flows.

This political mandate expands CNPC Capital’s global footprint but raises exposure to emerging-market sovereign debt risks, with non-performing loan pressures rising in some BRI markets where sovereign debt-to-GDP ratios exceeded 70% by 2024.

Energy Security and Supply Chain Policy

As China pushes for greater energy self-sufficiency, CNPC Capital has increased financing for domestic upstream projects, allocating an estimated CNY 45–60 billion in 2024–25 toward exploration and production improvements to meet National Energy Administration targets.

Political priority on oil and gas supply-chain security shifts lending and leasing to upstream tech upgrades, with 38% of new credit lines in 2024 earmarked for seismic, drilling and enhanced recovery equipment.

CNPC Capital’s strategy is guided by NEA long-term plans and 2030 resource security quotas, binding it to performance metrics and capital deployment that support China’s goal of reducing import dependence from roughly 73% of oil consumption in 2023.

Regulatory Oversight and Centralized Control

By 2025 the National Financial Regulatory Administration has centralized oversight of financial holding firms, imposing stricter capital adequacy and risk-isolation rules; banks and holdings face minimum CET1-like metrics and stress-test thresholds—China’s large financial groups now commonly target >10% core capital buffers per regulator guidance.

CNPC Capital must comply with tight controls on related-party transactions with CNPC parent and affiliates, curbing intra-group capital transfers and requiring ring-fencing for non-core activities, reducing deployment flexibility despite ensuring systemic stability.

- Centralized regulator: NFRA oversight by 2025

- Capital standards: target >10% core buffers

- Risk isolation: mandated ring-fencing of non-bank assets

- Related-party limits: stricter approval and disclosure rules

Geopolitical Tensions and Sanctions Risk

The evolving China-West tensions raise sanctions risk for CNPC Capital’s overseas finance; in 2024 China faced 45 major trade disputes with OECD partners and 18 targeted financial restrictions affecting Chinese banks.

CNPC Capital must build alternative payment rails and diversify currency exposure—RMB cross-border payments rose 28% in 2024, yet USD still dominates 88% of global FX reserves.

Strategic planning must model liquidity shocks from trade disputes that could reduce subsidiary funding access by an estimated 10–20% under severe sanction scenarios.

- 45 major 2024 China-OECD trade disputes; 18 targeted financial measures

- RMB cross-border payments +28% in 2024; USD ~88% of reserves

- Plan for 10–20% subsidiary liquidity shortfalls under severe sanctions

CNPC Capital directs CNY200–300bn to strategic energy; NFRA buffers >10%, RMB cross‑border +28%

CNPC Capital’s political mandate channels CNY 200–300bn pa (2025) into strategic energy projects, backed by NFRA oversight with >10% core buffers and ring-fencing rules; outbound project finance reached $18–25bn (2020–24) amid 45 China‑OECD trade disputes in 2024 and 18 targeted measures, prompting 28% growth in RMB cross‑border payments and planning for 10–20% subsidiary liquidity shocks.

| Metric | Value |

|---|---|

| Directed capital (2025) | CNY 200–300bn |

| Outbound finance (2020–24) | $18–25bn |

| NFRA core buffer target | >10% |

| China‑OECD disputes (2024) | 45 |

| RMB XB payments growth (2024) | +28% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact CNPC Capital, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented CNPC Capital PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory shifts, and market positioning while allowing for brief, context-specific notes.

Economic factors

Interest Rate Environment and Margin Compression

By end-2025, the PBOC balances modest easing and targeted support with debt deleveraging, keeping one-year loan prime rate near 3.95% and five-year LPR around 4.45%, creating a nuanced rate backdrop.

CNPC Capital faces net interest margin compression as competition for top-tier industrial borrowers tightens; sector NIMs narrowed ~20–35 bps in 2024 across Chinese mid-tier banks.

The firm must optimize liabilities—shorten funding tenor, diversify wholesale and RMB bond channels—to protect returns amid volatile benchmark rates and market-oriented pricing.

Energy Market Volatility and Credit Risk

CNPC Capital's performance is tightly tied to energy sector health; a 2024 Brent range of 70–100 USD/bbl and China LNG spot volatility ±30% year-on-year directly affect parent and subsidiary cash flows.

Crude price collapses in 2020 showed impairment risk; a 50% price drop can raise nonperforming loan ratios sharply, increasing credit stress on lending and leasing portfolios.

As of 2025 Q1, CNPC group debt-service coverage sensitivity to a 20% revenue shock requires higher provisioning and tighter covenants.

RMB Internationalization and Cross-border Trade

As RMB use in global energy trade rose—Chinese trade settlement in RMB reached 34% of global FX trade in 2024—CNPC Capital gains higher demand for RMB-denominated settlement and clearing, boosting fee income and liquidity management.

Leveraging its energy value‑chain role, CNPC Capital reduces partners’ conversion costs via RMB settlement corridors, supporting cross-border contracts and trade finance volumes.

Growth of Kunlun Bank—which saw international RMB deposits grow ~22% in 2024—strengthens CNPC Capital’s niche market and alternative payment route capabilities.

Industrial Sector Growth and Capital Demand

The shift to high-end manufacturing and green energy in China expands capital deployment opportunities; green investment reached 1.4 trillion RMB in 2024, supporting CNPC Capital's focus on hydrogen infrastructure and carbon capture projects.

CNPC Capital targets emerging industrial clusters—hydrogen, CCUS, battery manufacturing—where demand for specialized financial leasing and asset management is rising, offsetting slower heavy-industry financing.

- 2024 green investment: 1.4 trillion RMB

- Hydrogen project financing growth: ~28% YoY (2024)

- CCUS capacity target: 10 MtCO2/year by 2030

Inflationary Pressures and Operational Costs

Persistent global inflation, with IMF forecasting 2025 global inflation around 5.8% in emerging markets, is raising CNPC Capital's labor and procurement costs, including a 6–8% annual rise in fintech subscription and cloud expenses observed in 2024–25.

CNPC Capital must balance higher operational expenditures with competitive service pricing for internal and external clients to protect margins and client retention amid fee sensitivity.

Automation of back-office functions and strict cost controls are essential to preserve efficiency ratios; industry peers reported up to 15% reduction in back-office costs after RPA and cloud migration in 2024.

- Global EM inflation ~5.8% (IMF 2025)

- Fintech/cloud costs +6–8% YoY (2024–25)

- Back-office cost cut up to 15% via automation (2024)

Global headwinds: easing rates, squeezed margins, oil volatility, green spend boosts

Economic headwinds: modest PBOC easing with 1y LPR ~3.95%/5y ~4.45%; NIMs compressed 20–35bps (2024); Brent 70–100 USD/bbl (2024) with ±30% LNG volatility; green investment 1.4 tn RMB (2024); EM inflation ~5.8% (2025); fintech/cloud costs +6–8% YoY (2024–25); back‑office cuts up to 15% via automation (2024).

| Metric | Value |

|---|---|

| 1y/5y LPR | 3.95% / 4.45% |

| NIM compression | 20–35bps (2024) |

| Brent 2024 | 70–100 USD/bbl |

| Green invest 2024 | 1.4 tn RMB |

| EM inflation 2025 | ~5.8% |

Full Version Awaits

CNPC Capital PESTLE Analysis

The preview shown here is the exact CNPC Capital PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.